- Smart Packaging

- Bagging Machine Market

Bagging Machine Market Size, Share, and Growth Forecast, 2026 - 2033

Bagging Machine Market by Machine Type (Valve Sack Bagging Machine, Open Mouth Bagging Machine, Others), Automation Level (Fully Automatic, Semi-Automatic, Others), Application, Capacity, and Regional Analysis for 2026 - 2033

Bagging Machine Market Size and Trends Analysis

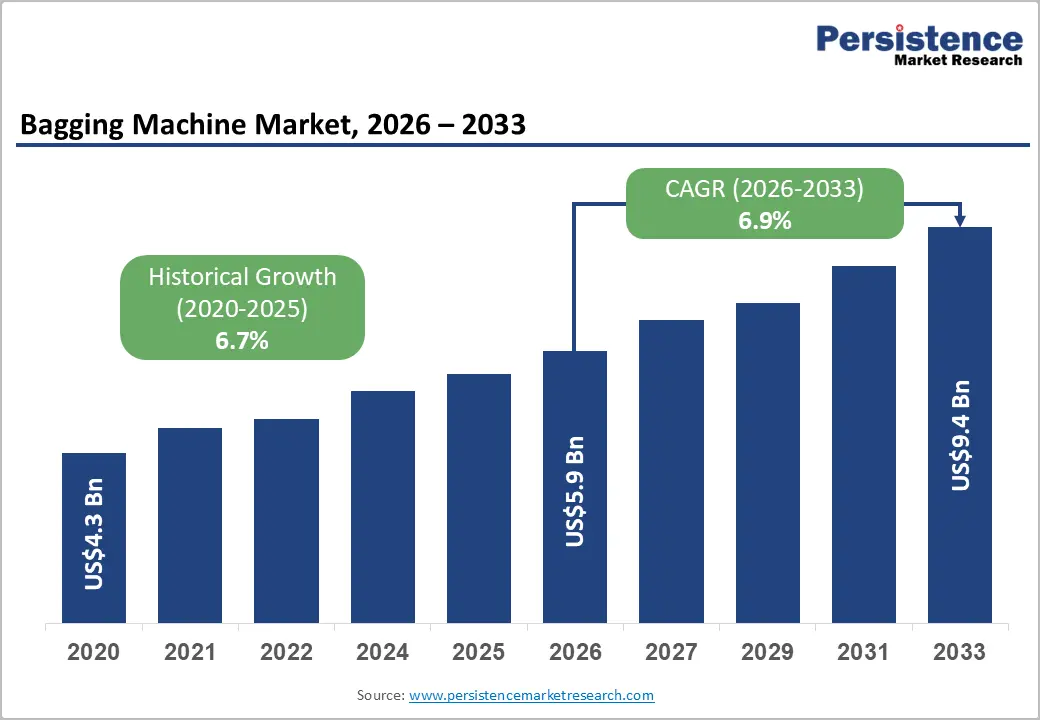

The global bagging machine market size is likely to be valued at US$5.9 billion in 2026 and is expected to reach US$9.4 billion by 2033, growing at a CAGR of 6.9% between 2026 and 2033, driven by accelerated automation across packaging lines, rising throughput requirements in food and construction sectors, and increased manufacturing capital expenditure in Asia Pacific and other emerging regions.

Regulatory focus on hygiene and traceability in food and pharmaceuticals is accelerating the replacement of legacy systems with integrated, digitally enabled bagging solutions. Consolidation across the packaging-equipment ecosystem is further driving adoption of turnkey bagging-to-palletizing lines.

Key Industry Highlights:

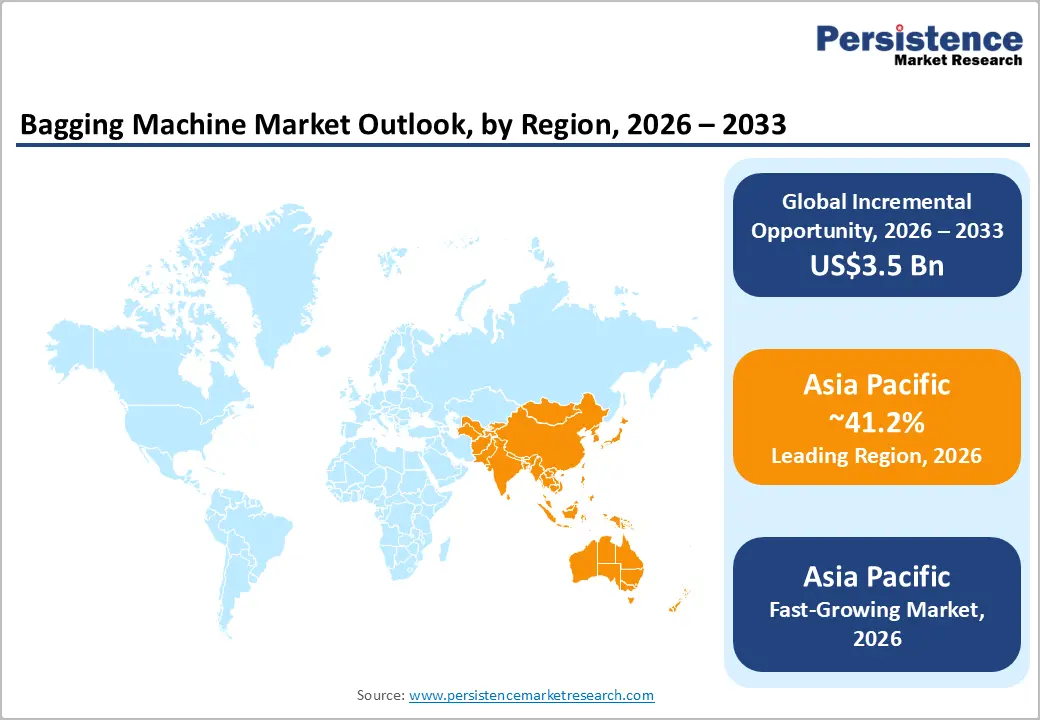

- Leading Region: Asia Pacific is projected to account for nearly 41.2% of the market, driven by large-scale manufacturing in China, rapid expansion of food processing in India, and strong demand for fertilizer and cement packaging across ASEAN.

- Fastest-Growing Region: Asia Pacific, supported by industrial modernization, automation adoption, and infrastructure development.

- Investment Plans: Capital allocation is focused on fully automated, high-capacity (>2001 bags) integrated bagging-to-palletizing lines, digital retrofits, and regional service center expansion, particularly across Asia-Pacific and North America.

- Dominant Machine Type: Valve sack bagging machines are expected to account for approximately 32.5% of the market, widely used in cement, chemical, and mineral bulk packaging applications.

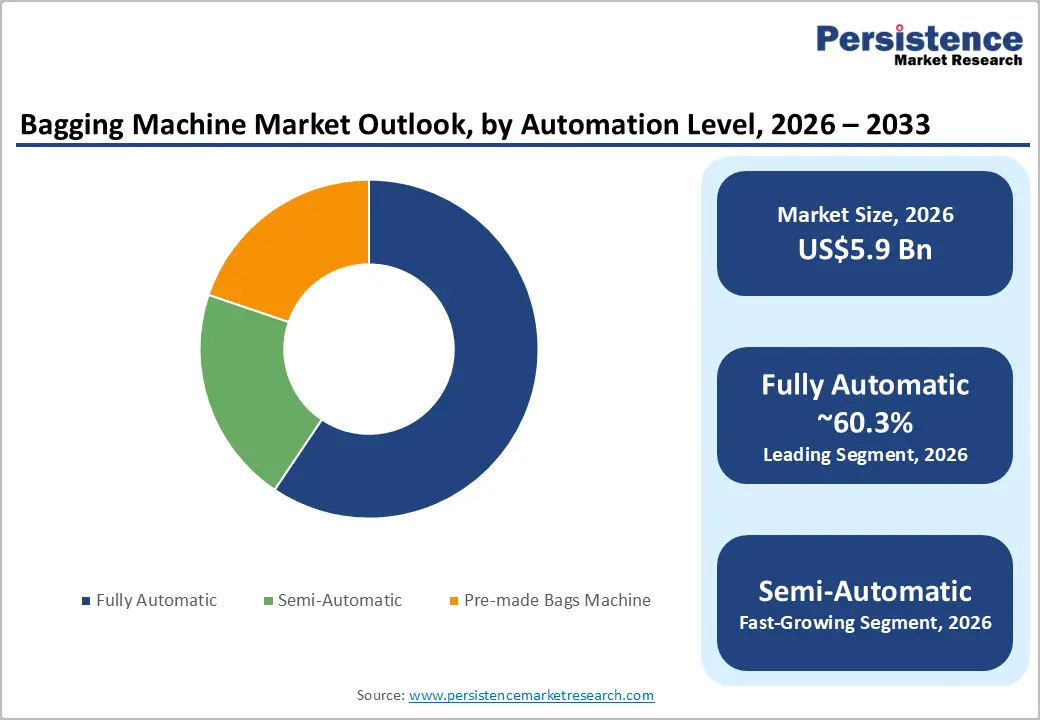

- Leading Automation Level: Fully automatic systems are estimated to account for approximately 60.3% of the market, favored by high-volume food, fertilizer, and construction material manufacturers for efficiency and traceability.

| Key Insights | Details |

|---|---|

| Bagging Machine Market Size (2026E) | US$5.9 Bn |

| Market Value Forecast (2033F) | US$9.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.7% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Industrial Automation and Labor-Cost Pressure

Manufacturers across food processing, cement, chemicals, and agriculture are accelerating automation investments to offset labor shortages and rising wage costs. In the U.S. and parts of Europe, manufacturing wages have risen steadily over the past five years, prompting capital expenditure in high-throughput automated systems. Bagging machines integrated with programmable logic controllers (PLCs), remote monitoring, and predictive maintenance capabilities are increasingly replacing manual or semi-manual systems.

Automation reduces product giveaway, improves filling accuracy, and enhances overall equipment effectiveness (OEE). In high-volume sectors such as cement and animal feed, where plants operate continuously, automated baggers significantly lower per-bag labor costs. The shift toward Industry 4.0 practices, including digital performance tracking and predictive diagnostics, is shortening replacement cycles and increasing demand for network-enabled bagging equipment globally.

Growth in Packaged Goods and Bulk Material Throughput

Urbanization, expanding retail infrastructure, and international trade are increasing demand for packaged food, fertilizers, construction materials, and chemicals. Global cement production continues to exceed 4 billion metric tons annually, creating substantial demand for high-capacity valve bagging systems. Similarly, growth in packaged grains, sugar, flour, and pet food drives investment in open-mouth and form-fill-seal (FFS) bagging machines. Higher throughput requirements push manufacturers toward systems capable of handling 600 to over 2000 bags per hour.

Bulk material producers favor robust valve sack systems for 20-50 kg bags, while food processors require flexible, hygienic solutions capable of handling varied SKUs. As infrastructure spending and packaged goods consumption rise in the Asia Pacific and parts of Africa, bagging equipment demand aligns closely with production output expansion.

Regulatory Emphasis on Hygiene and Traceability

Stricter food safety regulations, including hazard analysis and preventive control requirements, are driving equipment upgrades. Pharmaceutical serialization mandates and enhanced traceability standards require integrated inspection and labeling systems. Modern bagging machines now incorporate dust-control mechanisms, stainless-steel wash-down designs, in-line weighing systems, and vision inspection technologies. Regulatory compliance increases capital expenditure but enhances equipment value per installation.

Hygienic bagging solutions designed for easy cleaning and reduced risk of contamination are particularly important for dairy powders, infant nutrition, and pharmaceutical powders. These requirements have accelerated the replacement of legacy mechanical systems with digitally controlled, enclosed bag systems

ging platforms that ensure product integrity and regulatory conformity.

Barrier Analysis - High Upfront Capital Costs

Fully automated bagging lines represent significant capital investments, often requiring multi-year payback periods for small and medium-sized enterprises (SMEs). Equipment integration with palletizing, conveying, and inspection systems increases upfront expenditure. For smaller plants, return on investment typically depends on sustained high throughput over two to three years, delaying adoption in fragmented regional markets. High spare-parts costs and the need for skilled maintenance technicians further increase the total cost of ownership. These factors slow penetration in price-sensitive markets, particularly where labor remains comparatively inexpensive.

Supply Chain Volatility for Electromechanical Components

Bagging systems rely heavily on motors, sensors, PLCs, servo drives, and control modules. Global supply disruptions in electronic components can extend delivery lead times from several months to nearly a year during peak-demand periods. Lead-time variability directly affects project planning and capital budgeting. Although vendors increasingly standardize modules to mitigate delays, supply-chain uncertainty remains a structural risk. Price fluctuations in electronic components and logistics constraints can increase system costs and compress manufacturers' margins.

Opportunity Analysis - Retrofit and Digital Upgrade Programs

A substantial installed base of legacy bagging machines across Asia Pacific, Latin America, and parts of Europe presents an attractive retrofit opportunity. If approximately 20-25% of installed units adopt digital upgrades annually, retrofit revenue could represent 10-15% of annual new-machine revenue over the next five years. Modular IoT-enabled packages, servo motor upgrades, and vision inspection add-ons allow operators to improve efficiency without replacing entire lines. Retrofit programs typically yield higher margins and strengthen long-term service contracts.

Emerging Market Expansion

Emerging economies such as India, Vietnam, Indonesia, and parts of Africa are investing in food processing, fertilizer production, and construction materials manufacturing. Semi-automatic and cost-effective automated systems tailored to local service environments are gaining traction. Emerging markets may account for approximately 30-40% of incremental unit growth through 2030. Vendors that localize production, establish spare-parts distribution centers, and offer financing solutions can capture significant market share in these high-growth regions.

Sustainability and Recyclable Packaging Compatibility

The transition toward recyclable paper-based and mono-material packaging creates demand for machines capable of handling thicker laminates and sustainable films. Equipment designed to reduce material waste and optimize sealing parameters provides cost and environmental benefits. Manufacturers investing in sustainable-compatible bagging solutions can command premium pricing and secure partnerships with environmentally focused brands. Lifecycle cost reductions and waste minimization further enhance value propositions.

Category-wise Analysis

Machine Type Insights

Valve sack bagging machines are projected to account for approximately 32.5% of the market in 2026, maintaining leadership in heavy bulk material applications such as cement, dry mortar, minerals, and specialty chemicals. Their ability to deliver high-speed, dust-controlled filling of 20-50 kg valve bags makes them essential for construction-oriented industries where throughput and environmental compliance are critical. Integrated solutions that connect silos, dosing systems, checkweighers, and robotic palletizers enhance plant efficiency and reduce product loss.

For example, major cement producers in India and Southeast Asia deploy fully enclosed valve bagging lines to meet stricter workplace dust regulations and export quality standards. In infrastructure-driven economies, these systems command higher average selling prices due to robust construction, advanced weighing technology, and compatibility with high-capacity operations exceeding 2,000 bags per hour.

Open-mouth and FFS bagging systems represent the fastest-growing machine category, driven by expanding demand in food processing, animal feed, and specialty chemicals. These systems support flexible packaging formats, including pillow bags, gusseted bags, and laminated sacks, enabling producers to manage multiple SKUs with rapid changeovers. For instance, grain processors and pet food manufacturers increasingly deploy vertical FFS lines integrated with multihead weighers to improve packaging speed and accuracy.

Growth is further supported by rising consumption of packaged staples such as flour, rice, sugar, and protein-based feed products across Asia Pacific and Latin America. Compared to heavy-duty valve systems, open-mouth and FFS machines typically require lower upfront capital investment, making them attractive to mid-sized processors modernizing operations in developing markets.

Automation Level Insights

Fully automatic bagging systems are expected to account for approximately 60.3% of the market, reflecting strong adoption among high-volume producers. These systems integrate product feeding, precision weighing, bag forming or placement, sealing, palletizing, and digital monitoring into a unified control architecture. Industries such as cement, fertilizer, and packaged food prioritize automation to reduce labor dependency, improve consistency, and achieve higher overall equipment effectiveness (OEE).

For example, multinational food manufacturers in North America and Europe deploy automated bagging-to-palletizing lines with real-time performance analytics and predictive maintenance modules to minimize downtime. Integrated data systems also facilitate compliance with traceability requirements in food and pharmaceutical packaging. While capital-intensive, these solutions deliver lower per-bag operating costs over time, reinforcing their dominant revenue position.

Semi-automatic bagging machines are projected to experience the fastest unit growth, particularly in emerging markets where cost sensitivity and phased automation strategies influence purchasing decisions. Small and medium-sized enterprises (SMEs) adopt semi-automatic systems to improve weighing accuracy and reduce manual handling without incurring the full investment required for end-to-end automation. In countries such as India, Vietnam, and Indonesia, regional food processors and fertilizer distributors are increasingly upgrading from manual filling to digitally assisted semi-automatic platforms.

Modular configurations allow future upgrades, such as automated stitching, sealing, or palletizing, supporting gradual scalability. Financing options, including equipment leasing and vendor-backed credit programs, further accelerate adoption among growing regional manufacturers seeking to improve operational efficiency.

Regional Market Insights

North America Bagging Machine Market Trends - Labor-Driven Automation, FSMA-Compliant Integrated Lines, and Digital Lifecycle Services Expansion

North America accounts for a substantial share of global bagging machine revenue, driven by high automation penetration and strict regulatory oversight. The U.S. leads the regional market, accounting for the majority of installations, driven by its advanced food processing, pet food, chemicals, cement, and pharmaceutical manufacturing industries. This sustained capital investment environment directly supports demand for fully integrated bagging systems. Automation adoption remains robust as manufacturers address labor shortages and rising wages.

The U.S. Bureau of Labor Statistics has reported persistent vacancies in production and material-handling occupations, spurring automation investments across bulk packaging operations. Major OEMs such as Paxiom Group (WeighPack Systems) and BW Flexible Systems (Barry-Wehmiller Group) continue to expand their North American presence with modular vertical form-fill-seal (VFFS) and open-mouth bagging solutions designed for high-mix production. These systems integrate checkweighing, metal detection, and palletizing robotics, aligning with regulatory requirements under the U.S. Food Safety Modernization Act (FSMA), which mandates traceability and hygienic processing standards.

Strategic developments in the region reinforce the shift toward integrated automation. In 2024-2025, several packaging system integrators expanded their digital service platforms to offer remote diagnostics and predictive maintenance. For example, BW Packaging strengthened its digital lifecycle services portfolio to enhance uptime for food and pet food processors. These initiatives increase aftermarket revenue streams while supporting customer retention. Robotics suppliers such as Fanuc America and ABB Robotics U.S. have also partnered with packaging line integrators to deploy high-speed palletizing cells downstream of bagging operations, improving throughput efficiency in fertilizer and cement plants.

Europe Bagging Machine Market Trends - Engineering Export Strength, EU Sustainability Compliance, and Energy-Efficient Material-Flexible FFS Systems

Europe remains a high-value and technology-intensive market characterized by engineering leadership and stringent environmental standards. Germany serves as both a major OEM hub and a significant buyer of automated bagging systems. German-headquartered companies such as HAVER & BOECKER, BEHN + BATES, Syntegon Technology, Krones AG, and KHS GmbH export globally while also serving strong domestic demand in the chemicals, cement, and food-processing sectors.

The German Mechanical Engineering Industry Association (VDMA) reports that packaging machinery exports consistently represent a large share of Germany’s mechanical engineering output, underlining the region’s manufacturing depth. Sustainability regulations strongly influence purchasing decisions. The European Union’s circular economy initiatives and packaging waste directives encourage the adoption of recyclable mono-material bags and paper-based packaging. This transition requires bagging machines capable of handling variable material thickness and maintaining seal integrity. In response, equipment suppliers have introduced energy-efficient servo-driven systems and material-flexible FFS platforms.

For instance, Syntegon has launched updated vertical packaging solutions designed to process recyclable films while reducing energy consumption, directly addressing EU sustainability targets. High labor costs across Western Europe incentivize automation. Food producers in France and Spain are increasingly deploying fully automated open-mouth bagging lines with robotic palletizing to remain competitive. In the U.K., modernization efforts in agro-food processing facilities continue despite broader economic adjustments, supporting replacement demand for hygienic packaging systems.

Asia Pacific Bagging Machine Market Trends - Cement and Agro-Industrial Scale Demand, Rapid Food Packaging Modernization, and Localization of OEM Services

Asia Pacific is projected to lead the market with nearly 41.2% of market share and demonstrates the fastest growth trajectory. China is the largest national market by volume, supported by its extensive cement, fertilizer, food-processing, and chemical manufacturing base. The China Cement Association reports sustained production volumes exceeding several billion tons annually, reinforcing demand for high-capacity valve sack bagging machines. Domestic manufacturers, alongside international suppliers such as HAVER & BOECKER, have expanded localized production and service operations to meet this scale-driven demand. India exhibits rapid modernization in food, feed, and agrochemical packaging.

Government-led initiatives to expand manufacturing and upgrade food-processing infrastructure have stimulated capital investment in packaging automation. Companies such as Nichrome India Ltd., a domestic packaging machinery manufacturer, continue expanding their VFFS and bagging portfolios to serve local and export markets. Rising labor costs and productivity targets in metropolitan industrial zones further accelerate the shift from manual to semi-automatic and fully automatic systems.

ASEAN countries, including Vietnam, Thailand, and Indonesia, are strengthening export-oriented food and agricultural production, increasing demand for flexible bagging equipment. Multinational food brands establishing regional production hubs require standardized, hygienic bagging systems that comply with international standards. Japanese and South Korean robotics providers contribute advanced automation modules integrated into bagging-to-palletizing lines across Southeast Asia.

Investment trends emphasize localization and service infrastructure. Global OEMs have established regional service centers in China and India to reduce lead times and enhance spare parts availability. Joint ventures between European technology providers and Asian manufacturers improve cost competitiveness while maintaining performance standards. Financing models and staged automation packages enable mid-sized producers to upgrade incrementally.

Competitive Landscape

The global bagging machine market is moderately concentrated among global OEMs specializing in fully automatic and integrated systems, while semi-automatic and entry-level segments remain fragmented. High-end valve and FFS technologies are dominated by established European and Japanese manufacturers. Regional players in Asia and Latin America serve cost-sensitive markets. Consolidation trends are strengthening tier-one suppliers through broader product portfolios.

Market leaders focus on innovation, service-led revenue models, and geographic expansion in the Asia Pacific. Modular system architecture, digital performance monitoring, and sustainability compatibility are key differentiators. Emerging players compete on cost efficiency and localized service capabilities.

Key Industry Developments:

- In September 2025, Sealed Air Corporation launched the AUTOBAG® 850HB Hybrid Bagging Machine, a flexible automated system capable of handling both paper and poly mailers to enhance throughput and sustainability in e-commerce and third-party logistics operations.

Companies Covered in Bagging Machine Market

- HAVER & BOECKER

- BEHN + BATES

- Syntegon Technology

- Ishida Co., Ltd.

- Paxiom Group

- Krones AG

- KHS GmbH

- GEA Group

- Moba Group

- Volpak (Coesia Group)

- Premier Tech

- All-Fill Inc.

- Nichrome India Ltd.

- Concetti S.p.A.

- BW Flexible Systems

- LoeschPack

- Gaogepak

- Kingrun Machinery

Frequently Asked Questions

The global bagging machine market is projected to be valued at US$5.9 billion in 2026.

The bagging machine market is expected to reach US$9.4 billion by 2033.

Key trends include increased adoption of fully automatic integrated bagging-to-palletizing lines, rising demand for hygienic and traceable packaging solutions in food and pharmaceuticals, expansion of high-capacity systems (>2001 bags), retrofit and digital upgrade programs for legacy installations, and growing compatibility with sustainable packaging materials such as recyclable mono-films and paper laminates.

Valve sack bagging machines are the leading segment, anticipated to hold 32.5% market share, driven by strong demand from cement, mineral, and chemical industries requiring precision filling and dust control.

The bagging machine market is projected to grow at a CAGR of 6.9% between 2026 and 2033.

Major players include HAVER & BOECKER, Syntegon Technology, Ishida Co., Ltd., Krones AG, and BW Flexible Systems.