- Energy Storage Solutions

- Lithium-ion Battery Market

Lithium-ion Battery Market Size, Share, and Growth Forecast, 2025 - 2032

Lithium-ion Battery Market By Cell Chemistry (NMC, LFP, NCA, Others), Form Factor (Cylindrical Cells, Others), Voltage Range (Below 12V, 12V-36V, Above 36V), Application (Automotive, Consumer Electronics, Others), and Regional Analysis for 2025 - 2032

Lithium-ion Battery Market Size and Trends Analysis

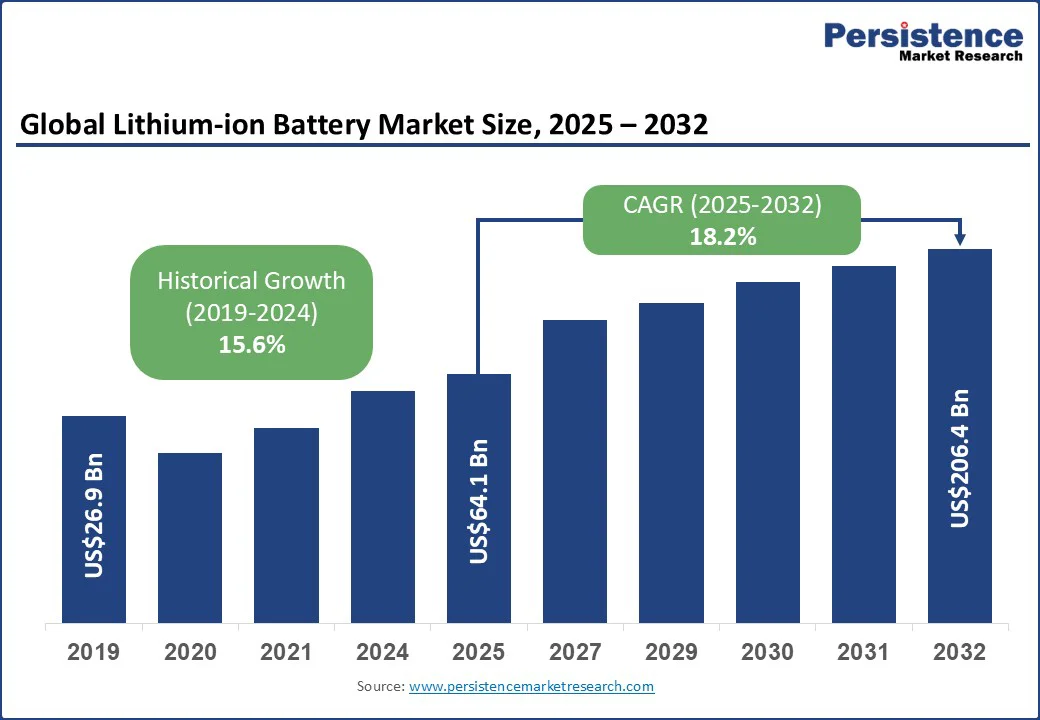

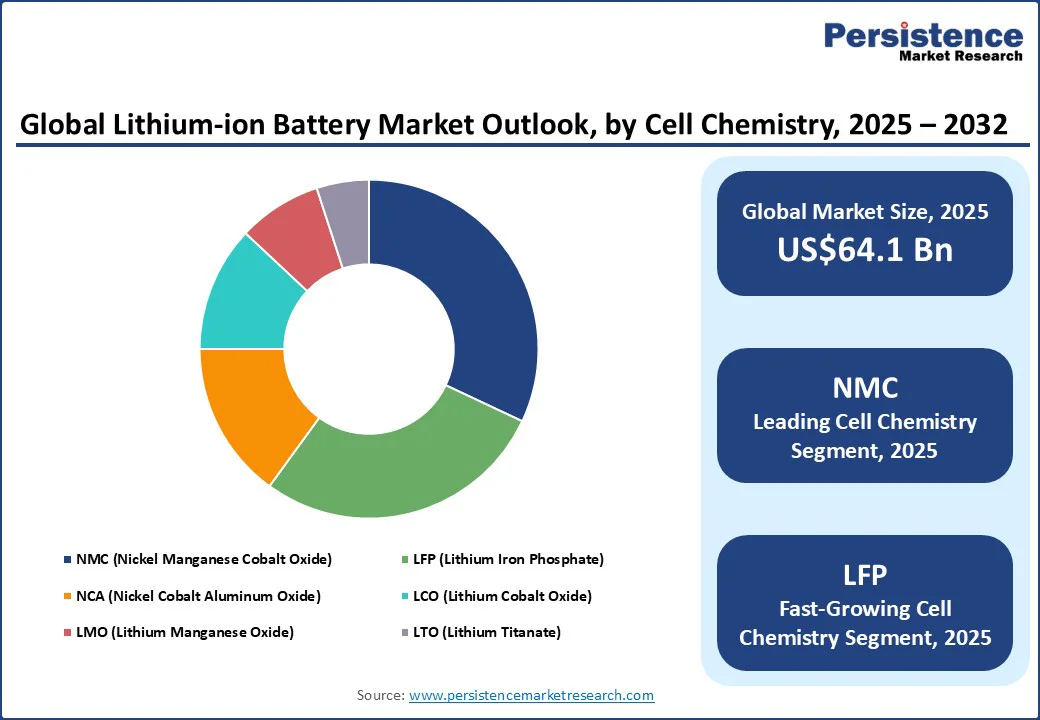

The global lithium-ion battery market size is likely to be valued at US$64.1 Bn in 2025 and is expected to reach US$206.4 Bn by 2032, growing at a CAGR of 18.2% during the forecast period from 2025 to 2032.

Key Industry Highlights:

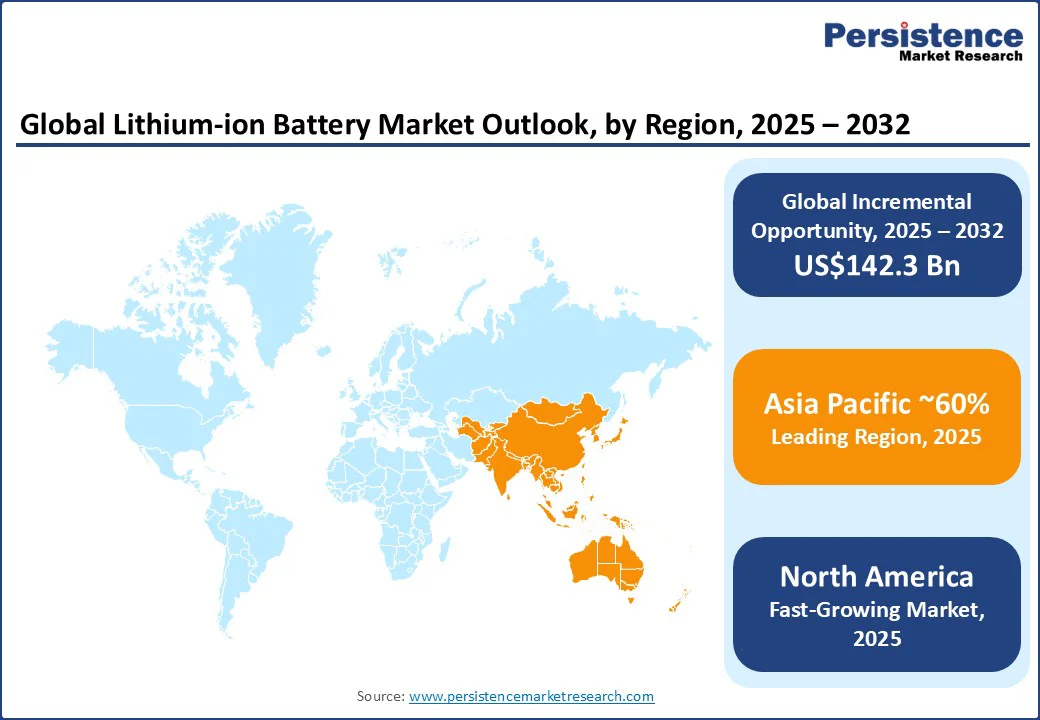

- Leading Region: Asia Pacific dominates the market with nearly 60% revenue share, led by China, Japan, and South Korea. Strong EV manufacturing ecosystems, raw material access, and government incentives drive large-scale production and exports.

- Fastest-growing Region: North America is the fastest-growing region, driven by the leadership of the U.S. in electric vehicle adoption, strong federal incentives, and major investments in domestic battery manufacturing and supply chain development.

- Application Type: Automotive applications account for 46% of global demand, making it the largest revenue-generating segment. Rapid EV adoption, government subsidies, and stricter emission norms are fueling mass-scale deployment of lithium-ion batteries in passenger and commercial vehicles.

- Leading Voltage Segment Type: Above 36V batteries hold the largest voltage segment share at ~56%, propelled by electric vehicles and industrial-grade storage. Their ability to deliver high power density and longer ranges makes them critical in the automotive and renewable energy sectors.

- Leading and Fast-growing Cell Chemistry Type: Nickel Manganese Cobalt (NMC) batteries held the largest global market share of approximately 32-35% in 2024, while Lithium Iron Phosphate (LFP) emerged as the fastest-growing chemistry due to its cost-effectiveness, safety, and strong adoption in China’s EV and energy storage sectors.

- Energy Storage Systems (ESS) represent the fastest-growing segment with a CAGR of over 19.8%, driven by renewable energy integration, grid stabilization needs, and supportive policies in the U.S., Europe, and China for large-scale energy storage solutions.

- Cylindrical cells retain ~38% market share, benefiting from proven reliability and economies of scale. However, pouch and prismatic formats are expanding faster, driven by OEM preferences for higher energy density and design flexibility in EV applications.

| Market Attribute | Key Insights |

|---|---|

| Lithium-ion Battery Market Size (2025E) | US$64.1 Bn |

| Market Value Forecast (2032F) | US$206.4 Bn |

| Projected Growth (CAGR 2025 to 2032) | 18.2% |

| Historical Market Growth (CAGR 2019 to 2024) | 15.6% |

This expansion is propelled by the rapid adoption of electric vehicles (EVs), the increasing deployment of renewable energy storage solutions, and strong regulatory support for clean energy transitions. Ongoing innovation in high-density chemistries and cost-efficient production processes further enhances the market’s growth trajectory.

Market Dynamics

Driver - Rapid EV Adoption and Supportive Government Policies Accelerates Lithium-ion Battery Demand

The acceleration toward clean energy and electrification, particularly in the transportation and energy storage sectors drives EV adoption. Governments worldwide are implementing stringent emission regulations and offering subsidies for electric vehicles, while renewable integration is creating an urgent need for scalable storage solutions.

Technological advancements in lithium-ion cell chemistries, such as higher energy density, faster charging, and longer cycle life, have made them preferred choice across automotive, consumer electronics, and utility-scale storage applications. These structural shifts are reinforced by increasing private and public investment, as industries pursue sustainable mobility and carbon-neutral targets.

Statistical evidence highlights this momentum. The International Energy Agency (IEA) (2024) projects that global EV sales will surpass 45 million units annually by 2030, directly boosting lithium-ion demand. Similarly, the U.S. Department of Energy emphasizes grid-scale storage as a critical enabler of renewable adoption, aiming for 90% clean electricity by 2035.

Meanwhile, the European Commission’s Green Deal mandates significant decarbonization targets, further supported by battery recycling and manufacturing policies. Collectively, these government-backed initiatives and policy frameworks are cementing lithium-ion batteries as the backbone of global electrification.

Restraint - Supply Chain Volatility and Limited Raw Material Availability Continue to Challenge Global Battery Production

The global lithium-ion battery industry faces persistent supply chain vulnerability, largely tied to the concentration of critical raw materials such as lithium, cobalt, and nickel in a few geographies. Political instability, trade restrictions, and mining bottlenecks in these regions create volatility in material costs and hinder consistent supply, disrupting production schedules for battery manufacturers worldwide.

At the same time, environmental and recycling challenges are limiting adoption rates. The lack of standardized large-scale recycling infrastructure increases dependence on primary mining while raising concerns about waste management and sustainability. These factors slow the pace of scaling production, even as demand accelerates across automotive, energy storage, and electronics sectors.

Opportunity - Electrification and Circular Innovation Unlock Long-Term Market Potential

Expanding electrification across transport and energy sectors presents one of the strongest opportunities for lithium-ion batteries. Growing policy alignment with net-zero goals is accelerating large-scale adoption, while sustainability commitments are reshaping how batteries are designed, produced, and recycled. As industries transition toward decarbonization, the push for cleaner mobility, renewable integration, and longer-lasting storage systems is creating demand for advanced chemistries and circular solutions.

Governments and manufacturers are already capitalizing on this shift. The European Union’s Battery Regulation enforces sustainability standards on recycling and carbon footprint, while U.S. initiatives under the Inflation Reduction Act incentivize domestic cell production.

Leading companies such as CATL and LG Energy Solution are investing heavily in solid-state research and closed-loop recycling partnerships, positioning themselves at the forefront of the next growth cycle. Together, these actions signal a forward-looking path where innovation and sustainability converge to expand the lithium-ion battery market’s long-term potential.

Category-wise Analysis

Cell Chemistry Insights

Nickel Manganese Cobalt (NMC) batteries are projected to account for the largest global share, estimated at around 32-35% in 2025. Their dominance is supported by high energy density, making them the preferred chemistry for passenger EVs in Europe and North America, where range and performance remain critical purchase drivers. The chemistry has also benefited from sustained R&D investments by leading automakers and cell producers aiming to optimize cobalt usage while maintaining efficiency.

Lithium Iron Phosphate (LFP), while holding a slightly lower share globally, is anticipated to be the fastest-growing chemistry, driven by its cost efficiency, safety profile, and strong adoption in China’s EV and energy storage markets. Its expansion is reinforced by policies such as China’s NEV subsidy programs and large-scale deployments by Tesla and BYD.

Other chemistries, including Lithium Nickel Cobalt Aluminum Oxide (NCA) and emerging solid-state platforms, continue to play important roles in specific application, such as high-performance EVs or next-generation storage, indicating that while NMC leads today, the market’s trajectory is shifting toward broader LFP adoption in the near future.

Application Insights

The automotive sector is anticipated to stand as the largest application area for lithium-ion batteries, accounting for more than ~46% of global revenue in 2025, with growth projected at a CAGR of over 19.2% through 2032. This dominance stems from the accelerating global shift toward electric mobility, bolstered by stringent emission regulations, carbon-neutrality targets, and massive investments by leading automakers in battery-powered vehicles.

Government-backed initiatives, such as China’s EV subsidy programs and the European Union’s “Fit for 55” package, further cement automotive demand, making it the centerpiece of the lithium-ion ecosystem.

Consumer electronics continues to represent a steady revenue contributor, fueled by rising smartphone penetration, laptop demand, and the surge in wearables. Policies promoting digital connectivity and 5G rollout indirectly stimulate this segment.

Energy storage systems (ESS) are emerging as the fastest-growing non-automotive application, driven by grid modernization, renewable energy integration, and supportive frameworks such as the U.S. Inflation Reduction Act and India’s National ESS Mission. Industrial applications, including power tools, aerospace, and medical devices, provide diversification to the market, benefiting from miniaturization and higher energy density advancements. Collectively, these applications ensure that lithium-ion batteries remain indispensable across industries, reinforcing their role in the global energy transition.

Regional Insights

Asia Pacific Lithium-ion Battery Market Trends - China at the Helm of Innovation and Scale

China firmly anchors Asia Pacific, commanding the largest share owing to its extensive manufacturing base, integrated supply chains, and aggressive government-backed EV adoption programs.

The country’s dominance is further reinforced by strategic developments such as Contemporary Amperex Technology Limited (CATL)’s recent joint venture with Stellantis to expand battery cell production capacity in 2024, ensuring both domestic supply security and global export strength. Strong state incentives, coupled with rapid EV penetration and large-scale grid energy storage deployments, make China the undisputed leader driving regional growth.

South Korea and Japan play pivotal roles as technology powerhouses, leveraging advanced R&D and global OEM partnerships. Companies such as LG Energy Solution, Samsung SDI, and Panasonic are expanding capacity while diversifying chemistries to meet both automotive and energy storage demands.

Meanwhile, India is fast emerging as a growth hotspot, propelled by the government’s PLI scheme for advanced chemistry cell manufacturing and increasing renewable energy integration, which are stimulating large-scale investments in localized gigafactories. Countries across Southeast Asia, including Thailand and Indonesia, are also stepping into the ecosystem, with Indonesia leveraging its abundant nickel reserves to attract foreign battery makers.

North America Lithium-ion Battery Market Trends - U.S. to Attract Major Growth

The U.S. leads in North America, supported by robust EV adoption, federal incentives, and large-scale manufacturing investments. The Inflation Reduction Act has catalyzed domestic supply chain growth, while a major milestone came in 2024 when General Motors partnered with Samsung SDI to establish a US$3 Bn battery plant in Indiana, expanding localized production.

Canada follows as a key contributor, leveraging rich reserves of nickel, cobalt, and lithium alongside national programs encouraging value-added processing and gigafactory investments. Its strategic role in supplying critical minerals to U.S. manufacturers further strengthens the region’s integration. With U.S. innovation and Canada’s resource depth, North America is advancing a resilient and self-reliant lithium-ion battery ecosystem.

Europe Lithium-ion Battery Market Trends - Germany at the Core of Expansion

Germany leads the European lithium-ion battery market, supported by its strong automotive sector and ambitious transition toward electric mobility. Backed by the European Union’s Green Deal, Germany has become a hub for gigafactory investments, with companies such as Northvolt expanding its Ettlingen facility through a partnership with Volkswagen in 2024, securing local supply chains for EV batteries.

The country’s dominance is further amplified by robust R&D initiatives and government subsidies that encourage both domestic production and technology innovation.

France and the U.K. are also accelerating their market presence through national electrification strategies and growing renewable integration. France benefits from state-backed funding programs, such as the European Battery Alliance, which has enabled large-scale projects for sustainable cell manufacturing.

The U.K., on the other hand, has intensified its focus on gigafactory development despite Brexit challenges, supported by its EV sales surge and net-zero commitments. Italy and Spain continue to advance steadily, driven by the rising demand for plug-in hybrids and supportive EU-wide funding for clean transport.

Meanwhile, the Nordic region, led by Sweden and Finland, is carving out a competitive edge in sustainable supply chains, with abundant access to raw materials and recycling initiatives positioning them as key enablers in Europe’s long-term battery ecosystem.

Competitive Landscape

The global lithium-ion battery market is becoming increasingly dynamic, with manufacturers racing to expand gigafactories, advance next-gen chemistries, and strengthen recycling capabilities. These moves not only intensify competition but also drive innovation and cost efficiency, ensuring that the industry stays aligned with soaring EV and energy storage demand.

On the supply side, tighter collaboration with raw material suppliers and distributors is reshaping the value chain. Localized sourcing and strategic logistics partnerships are improving resilience and reducing bottlenecks, fostering a healthier ecosystem that supports scalability and long-term growth.

Key Industry Developments:

- In April 2025, LG Energy Solution formed a joint venture with Derichebourg to build a state-of-the-art battery recycling plant in northern France, slated to open in 2027, with a 20,000-ton annual processing capacity. This reinforced circularity and regulatory compliance under the EU Battery Regulation.

- In December 2024, Stellantis and CATL announced a €4.1 Bn (US$4.8 Bn) joint venture to construct a 50 GWh LFP gigafactory in Zaragoza, Spain, targeted to start production by 2026. This investment localized EV battery supply and supported decentralized electrification in Europe.

Companies Covered in Lithium-ion Battery Market

- SK Innovation Co., Ltd.

- Panasonic

- LG Chem

- Samsung SDI

- Ultralife Corporation

- Saft Groupe

- BYD Company

- LG Energy Solution

- Toshiba Corporation

- CATL

- CALB

- EVE Energy

- Gotion High Tech

- Farasis Energy

Frequently Asked Questions

The lithium-ion battery market is projected to reach US$64.1 Bn in 2025.

Rapid adoption of EVs, supportive government policies, and increasing integration of energy storage solutions are accelerating the global demand for lithium-ion batteries.

The lithium-ion battery market is estimated to rise at a CAGR of 18.2% from 2025 to 2032.

Widespread electrification across industries and advancements in circular innovations, such as recycling and second-life battery applications, are unlocking long-term growth potential in the lithium-ion battery market.

The major players dominating the market are SK Innovation Co., Ltd., Panasonic, LG Chem, Samsung SDI, Ultralife Corporation, and Saft Groupe.