- Pharmaceuticals

- Autoimmune Skin Diseases Treatment Market

Autoimmune Skin Diseases Treatment Market Size, Share, and Growth Forecast, 2026 - 2033

Autoimmune Skin Diseases Treatment Market by Disease Types (Psoriasis, Atopic Dermatitis, Vitiligo, Others), Therapy Types (Biologics, Corticosteroids, Others), End-user (Hospitals, Specialty Clinics, Homecare Settings, Others), and Regional Analysis for 2026 – 2033

Autoimmune Skin Diseases Treatment Market Size and Trends Analysis

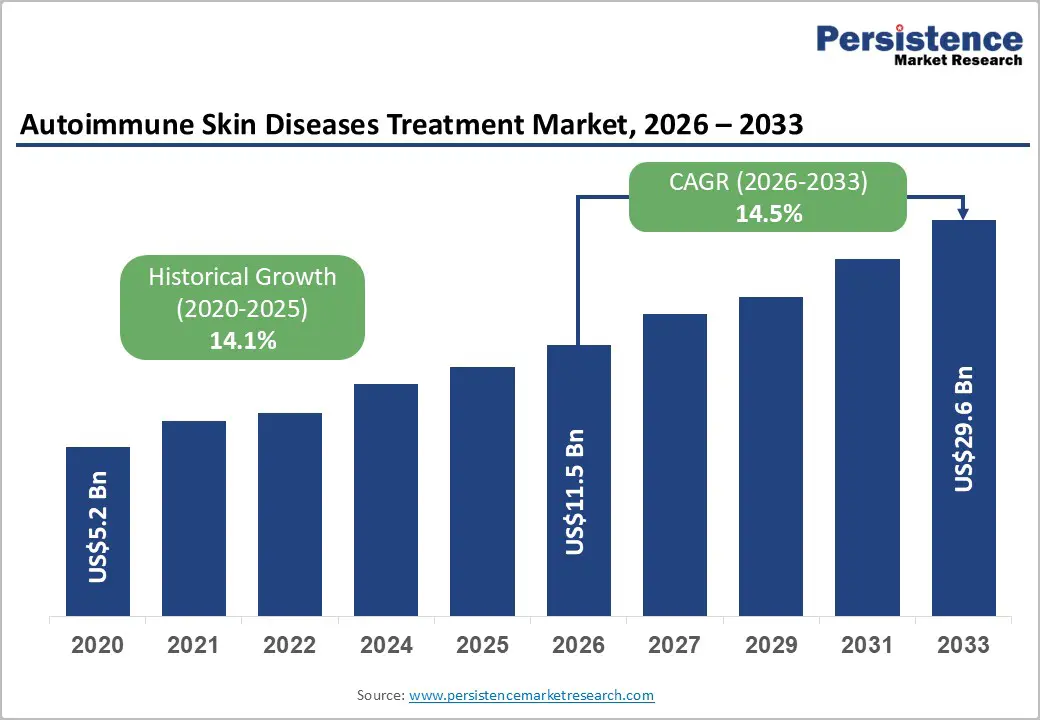

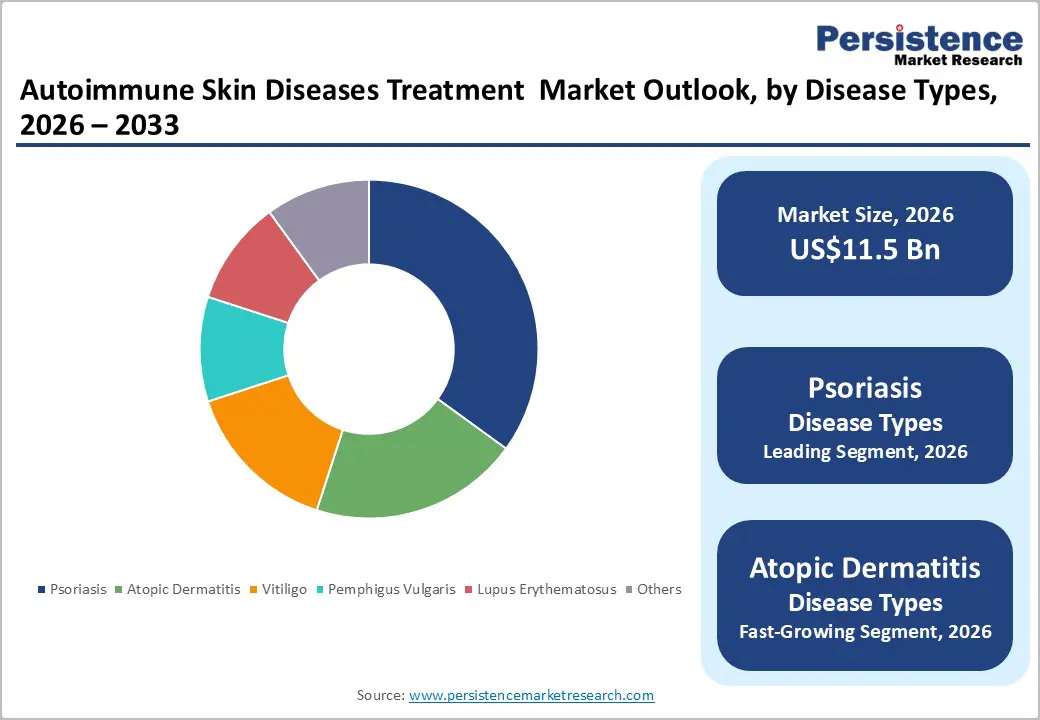

The global autoimmune skin diseases treatment market size is likely to be valued at US$11.5 billion in 2026, and is expected to reach US$29.6 billion by 2033, growing at a CAGR of 14.5% during the forecast period from 2026 to 2033, driven by the increasing prevalence of psoriasis and atopic dermatitis, rising adoption of biologics for targeted therapy, and advancements in small molecule drugs for chronic conditions.

Growing demand for effective, long-term treatments, especially for psoriasis and vitiligo, is accelerating the adoption of autoimmune skin disease treatment across demographics. Advances in biologics and immunosuppressants are further boosting uptake by offering better efficacy and fewer side effects. Increasing recognition of autoimmune skin diseases as chronic conditions requiring specialized care remains a major driver of market growth.

Key Industry Highlights:

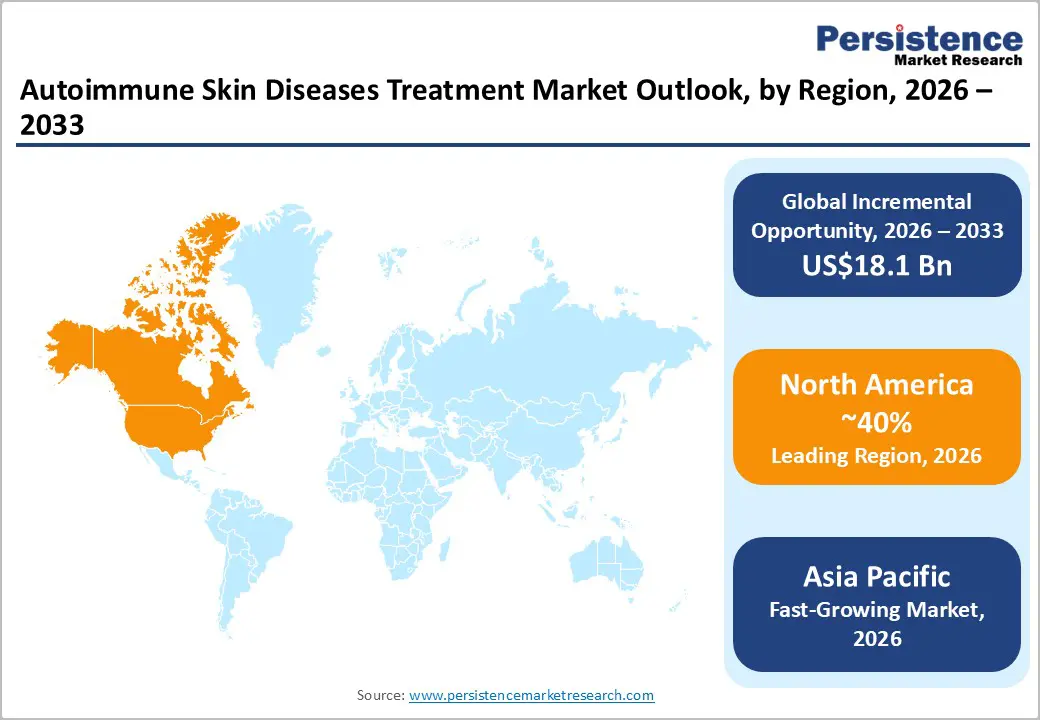

- Leading Region: North America, anticipated to account for a 40% market share in 2026, driven by advanced dermatology R&D, high prevalence of psoriasis, and strong regulatory support in the U.S.

- Fastest-growing Region: Asia Pacific, fueled by increasing healthcare access, rising awareness of autoimmune disorders, and growing investments in biotech in India and China.

- Dominant Disease Types: Psoriasis, to hold approximately 45% of the market share in 2026, as it affects millions globally with visible, chronic symptoms requiring ongoing treatment.

- Leading Therapy Types: Biologics, to account for over 50% of the market revenue in 2026, due to their targeted mechanism and high efficacy in moderate-to-severe cases.

- Leading End-user: Hospitals, to contribute nearly 45% of the market revenue in 2026, due to their advanced infrastructure and specialist availability for complex therapies.

| Key Insights | Details |

|---|---|

|

Autoimmune Skin Disease Treatment Market Size (2026E) |

US$11.5 Bn |

|

Market Value Forecast (2033F) |

US$29.6 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

14.5% |

|

Historical Market Growth (CAGR 2020 to 2025) |

14.1% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growing Demand for Targeted Biologics Due To Rising Cases of Psoriasis and Atopic Dermatitis

The growing prevalence of psoriasis and atopic dermatitis has emerged as a key driver of innovation and growth in targeted biologic therapies. These chronic inflammatory skin conditions are increasingly diagnosed in both adults and children, influenced by genetic factors, environmental triggers, urban lifestyles, and heightened awareness among patients and healthcare providers. Improved diagnosis rates, combined with the persistent and relapsing nature of these disorders, have created sustained demand for effective and long-lasting treatment options.

Traditional therapies, including topical corticosteroids and systemic immunosuppressants, often provide only limited relief and may cause adverse effects with prolonged use. This has accelerated the adoption of targeted biologics, which precisely regulate immune pathways involved in disease progression, such as interleukin and cytokine signaling. By addressing the underlying inflammatory mechanisms rather than just the surface symptoms, biologics offer higher efficacy, longer remission periods, and improved safety profiles for moderate-to-severe cases.

Patients and clinicians are increasingly favoring personalized treatment strategies that consider disease severity, comorbidities, and overall quality of life. Advances in molecular research and immunology have enabled the development of highly specific biologics, expanding therapeutic options and supporting earlier intervention in disease management.

High Treatment Costs and Limited Affordability

High treatment costs and limited affordability represent a major restraint in the autoimmune skin disease treatment market, particularly for conditions such as psoriasis and atopic dermatitis. Advanced therapies, including biologics and targeted immunomodulators, are costly to develop, manufacture, and distribute due to their complex production processes, stringent quality requirements, and cold-chain logistics. These costs are ultimately reflected in high therapy prices, making long-term treatment financially burdensome for many patients.

Autoimmune skin diseases are chronic in nature and often require continuous or lifelong management rather than short-term therapy. Cumulative treatment expenses can be substantial, discouraging adherence and leading some patients to discontinue therapy or rely on less effective conventional options. In regions with limited insurance coverage or restrictive reimbursement policies, out-of-pocket expenses further restrict patient access to advanced treatments. Healthcare systems in emerging economies also face budget constraints, limiting the inclusion of high-cost biologics in public formularies. Even in developed markets, payer scrutiny and cost-containment measures can delay therapy initiation or restrict eligibility to severe cases only.

Advancements in Oral Small Molecules and Topical Biologics

Advancements in oral small molecules and topical biologics are reshaping the treatment landscape for autoimmune skin diseases by offering more targeted, convenient, and patient-friendly therapeutic options. Oral small molecules, such as selective immune pathway inhibitors, are designed to precisely regulate intracellular signaling involved in inflammation. Their oral administration improves patient compliance compared to injectable therapies, while flexible dosing allows physicians to tailor treatment intensity based on disease severity and patient response. These agents also benefit from simpler manufacturing processes than biologics, supporting broader accessibility over time.

Progress in topical biologics has opened new possibilities for localized treatment with reduced systemic exposure. Innovations in formulation science and drug-delivery technologies have enabled large, complex biologic molecules to penetrate the skin barrier more effectively. This allows targeted action directly at inflamed skin sites, minimizing systemic side effects and lowering the risk of immunosuppression. Topical biologics are particularly promising for mild-to-moderate disease and for patients who are unsuitable for systemic therapies.

Category-wise Analysis

Disease Types Insights

Psoriasis is anticipated to dominate, accounting for approximately 45% of the revenue share in 2026, driven by its high global prevalence and lifelong, relapsing nature, which necessitate continuous disease management. The condition often progresses to moderate or severe stages, increasing reliance on advanced therapies. Psoriasis has the widest range of approved biologics targeting specific inflammatory pathways, enabling effective long-term control. Strong clinical outcomes, broad physician familiarity, and sustained patient demand continue to reinforce psoriasis’s leading market position.

Cosentyx is a monoclonal antibody that targets the IL-17A cytokine, a key driver of inflammation in plaque psoriasis. It has been approved in more than 50 countries for moderate-to-severe plaque psoriasis and is also indicated for psoriatic arthritis and ankylosing spondylitis, making it a versatile choice for patients with immune-mediated conditions.

Atopic dermatitis is likely to be the fastest-growing segment in 2026, supported by rapid therapeutic innovation and changing patient demographics. The condition is increasingly diagnosed across both children and adults, with pediatric cases showing notable growth due to improved awareness and earlier clinical intervention. Traditional treatments often provide limited long-term control, creating demand for advanced therapies. Recent approvals of targeted biologics and novel immunomodulators have significantly improved disease management by addressing underlying inflammatory pathways.

Expanded treatment options, favorable clinical outcomes, and growing acceptance of early biologic use are collectively accelerating market growth for atopic dermatitis therapies. EBGLYSS™ (lebrikizumab-lbkz) from Eli Lilly and Company, which the FDA approved in September 2024 for adults and children aged 12 years and older with moderate-to-severe atopic dermatitis. This approval introduces an additional targeted biologic option, broadening the treatment landscape and reinforcing the rapid expansion of therapy choices in this segment.

Therapy Types Insights

Biologics are expected to lead the market, holding over 50% revenue share in 2026, primarily due to their superior performance in moderate-to-severe cases. These therapies are designed to selectively target specific immune pathways responsible for chronic inflammation, resulting in more consistent disease control and longer remission periods compared to conventional treatments. Their proven clinical effectiveness, favorable safety profiles with long-term use, and strong physician confidence have supported widespread adoption. Skyrizi® (risankizumab) from AbbVie Inc.

Skyrizi is a targeted biologic approved for moderate-to-severe plaque psoriasis that has demonstrated very high skin clearance rates in clinical studies, with around 75% of patients achieving 90% improvement (PASI 90) within 16 weeks, and sustained responses over time. Its precision targeting of the IL-23 pathway contributes to strong efficacy and patient outcomes, helping drive its widespread adoption in moderate-to-severe disease.

Small molecule drugs are estimated to be the fastest-growing segment, fueled by their ease of oral administration and broadening clinical use. Unlike injectable therapies, oral small molecules offer greater convenience, improving patient adherence and acceptance, particularly for long-term disease management. Ongoing research has expanded their indications across multiple inflammatory skin conditions, increasing their clinical relevance. Their rapid onset of action, flexible dosing, and suitability for both moderate and severe cases continue to accelerate adoption and support strong growth within this segment.

Apremilast, an oral phosphodiesterase-4 (PDE4) inhibitor developed by Amgen and Celgene/Bristol-Myers Squibb. Apremilast (brand name Otezla) is approved by the U.S. FDA for adults with plaque psoriasis, offering an orally administered option that modulates inflammatory pathways and reduces key cytokines involved in disease activity. Its oral convenience improves patient adherence compared with injectable therapies and supports broader use in moderate psoriasis and psoriatic arthritis.

End-user Insights

Hospitals are expected to account for nearly 45% of revenue in 2026, driven by the demand for infusion-based biologic therapies. Biologics often require intravenous administration under controlled medical supervision to ensure safety, monitor potential adverse reactions, and maintain accurate dosing. Hospitals provide the necessary infrastructure, trained personnel, and monitoring capabilities, making them the preferred setting for such treatments. The rising adoption of advanced biologics, combined with patients’ preference for supervised administration, reinforces hospitals’ leading role in delivering effective care.

For example, Remicade, approved for plaque psoriasis and psoriatic arthritis, must be administered via intravenous infusion in a controlled clinical environment, unlike self-administered injections. This process requires careful dosing, continuous monitoring, and trained medical oversight, which drives patients to hospital facilities rather than outpatient or home-based care.

Specialty clinics are projected to be the fastest-growing segment, supported by the increasing demand for personalized dermatology care and a shift toward outpatient services. These clinics provide tailored treatment plans, focused monitoring, and patient education, improving adherence and clinical outcomes. Outpatient visits offer greater convenience, reduce hospital dependency, lower healthcare costs, and enhance access for patients managing chronic conditions.

The availability of advanced therapies is further expanding the role of specialty clinics in delivering effective, patient-centered dermatologic care. For instance, the Autoimmune Skin Disease and Atopic Dermatitis Programs at Brigham and Women’s Hospital in the U.S. offer disease-specific, personalized management for patients with psoriasis and atopic dermatitis, integrating advanced treatments outside traditional hospital settings.

Regional Insights

North America Autoimmune Skin Diseases Treatment Market Trends

North America is projected to hold approximately 40% of the market share in 2026, with the U.S. leading due to the highest biologic penetration, extensive clinical trial activity, and strong global market presence. The region’s leadership is supported by advanced healthcare infrastructure, high patient awareness, and substantial investments in research and development. Early adoption of innovative therapies, including biologic agents and targeted small molecules, is driving treatment for conditions such as psoriasis and atopic dermatitis. High diagnosis rates, comprehensive insurance coverage, and supportive reimbursement policies further facilitate access to these advanced treatments, fueling market growth.

Biologics and JAK inhibitors are major growth drivers as clinicians increasingly adopt precision immunomodulation for moderate-to-severe disease, supported by ongoing clinical trials and regulatory approvals. Additional trends include the expansion of outpatient specialty dermatology services, growing use of teledermatology and digital health platforms for disease monitoring, and a stronger focus on personalized care models.

Europe Autoimmune Skin Diseases Treatment Market Trends

Europe’s market growth is supported by strong reimbursement policies and advanced dermatology expertise in countries such as Germany, France, and the U.K. Fast-track approvals by the European Medicines Agency (EMA) facilitate the timely launch of new therapies. Biologics remain the largest therapeutic class, particularly for conditions such as psoriasis and atopic dermatitis, driving regional revenue through expanded indications and wider clinician adoption. Their use is increasingly complemented by targeted small molecules, including PDE4 and JAK inhibitors, which provide alternative mechanisms of action and greater convenience for managing moderate-to-severe disease.

Markets such as Germany, France, the U.K., and Italy lead in biologic adoption due to comprehensive reimbursement frameworks and high patient awareness. The increasing prevalence of psoriasis is driving greater demand for treatment and promoting earlier intervention with systemic, targeted therapies. Improvements in diagnostics and digital health technologies, such as AI-assisted tools, are supporting earlier detection and more personalized care. Despite these advances, challenges persist, including high treatment costs, inconsistent national reimbursement policies, and lengthy approval processes that can slow patient access to new therapies.

Asia Pacific Autoimmune Skin Diseases Treatment Market Trends

Asia Pacific is the fastest-growing region, led by China and India, with rising diagnosis rates and improving healthcare infrastructure. Local biosimilar development reduces costs. The prevalence of conditions such as psoriasis and atopic dermatitis is gradually increasing due to urbanization, changing lifestyles, and environmental factors. Growing patient awareness and early diagnosis initiatives are fueling demand for effective systemic treatments, including biologics and oral small molecules. Compared to Western markets, adoption of biologics is still emerging but is accelerating as local regulatory approvals increase and healthcare reimbursement programs expand.

Oral small molecules are gaining traction in the region due to their ease of administration, especially in outpatient and specialty clinic settings. Rising investment by global pharmaceutical companies, coupled with local manufacturing initiatives, is improving accessibility and reducing costs. Key markets such as Japan, China, South Korea, and Australia are leading adoption due to well-developed healthcare systems and higher disposable incomes, while emerging economies such as India and Southeast Asia are witnessing gradual uptake driven by awareness campaigns and patient support programs.

Competitive Landscape

The global autoimmune skin diseases treatment market is highly competitive, due to the presence of numerous established pharmaceutical and biotechnology companies, including AbbVie Inc., Amgen Inc., Eli Lilly and Company, Johnson & Johnson Services, Inc., Novartis AG, Pfizer Inc., and Biogen Inc. Competition is primarily driven by the development and commercialization of biologics, targeted small molecules, and combination therapies for conditions such as psoriasis and atopic dermatitis.

Companies are heavily investing in research and development to expand indications, enhance efficacy, and reduce side effects, creating a dynamic therapeutic landscape. Patent expirations, biosimilar introductions, and strategic collaborations further intensify market rivalry. Mergers and acquisitions are also common, as companies aim to strengthen product portfolios and expand geographic reach. This competitive environment promotes continuous innovation, pricing strategies, and patient support programs, benefiting clinicians and patients while shaping the market’s long-term growth trajectory.

Key Industry Developments

- In April 2025, Amgen announced a US$900?million expansion of its New Albany, Ohio, biomanufacturing facility. The investment aims to boost production capacity for both pipeline and commercial biologics, potentially supporting treatments in autoimmune dermatology. This expansion strengthens Amgen’s manufacturing network to meet growing global demand for innovative therapies.

- In January 2025, AbbVie completed its ~US$200?million acquisition of Nimble Therapeutics, gaining its lead oral peptide IL-23 receptor inhibitor for psoriasis and inflammatory bowel disease, along with Nimble’s proprietary peptide drug discovery platform to advance targeted autoimmune disease therapies.

Companies Covered in Autoimmune Skin Diseases Treatment Market

- AbbVie Inc.

- Amgen Inc.

- Eli Lilly and Company

- Johnson & Johnson Services, Inc.

- Novartis AG

- Pfizer Inc.

- Biogen Inc.

- Sanofi S.A.

- Merck & Co., Inc.

- GlaxoSmithKline plc

- UCB S.A.

- Horizon Therapeutics plc

Frequently Asked Questions

The global autoimmune skin diseases treatment market is projected to reach US$11.5 billion in 2026.

The rising prevalence of psoriasis and atopic dermatitis, and demand for targeted biologics, are the key drivers.

The autoimmune skin diseases treatment market is poised to witness a CAGR of 14.5% from 2026 to 2033.

Advancements in oral small molecules and topical biologics are the key opportunities.

AbbVie Inc., Eli Lilly and Company, Johnson & Johnson Services, Inc., Novartis AG, and Amgen Inc. are the key players.