- LED & Lighting (Optoelectronics)

- Architectural LED Products Market

Architectural LED Products Market Size, Share, and Growth Forecast, 2025 - 2032

Architectural LED Products Market By Product Type (LED Linear Fixtures, LED Strip Lights, LED Flood Lights, LED Spotlights, LED Wall Washers, Others), Distribution Channel (Online, Offline), Application, End-user, and Regional Analysis for 2025 - 2032

Architectural LED Products Market Size and Trends Analysis

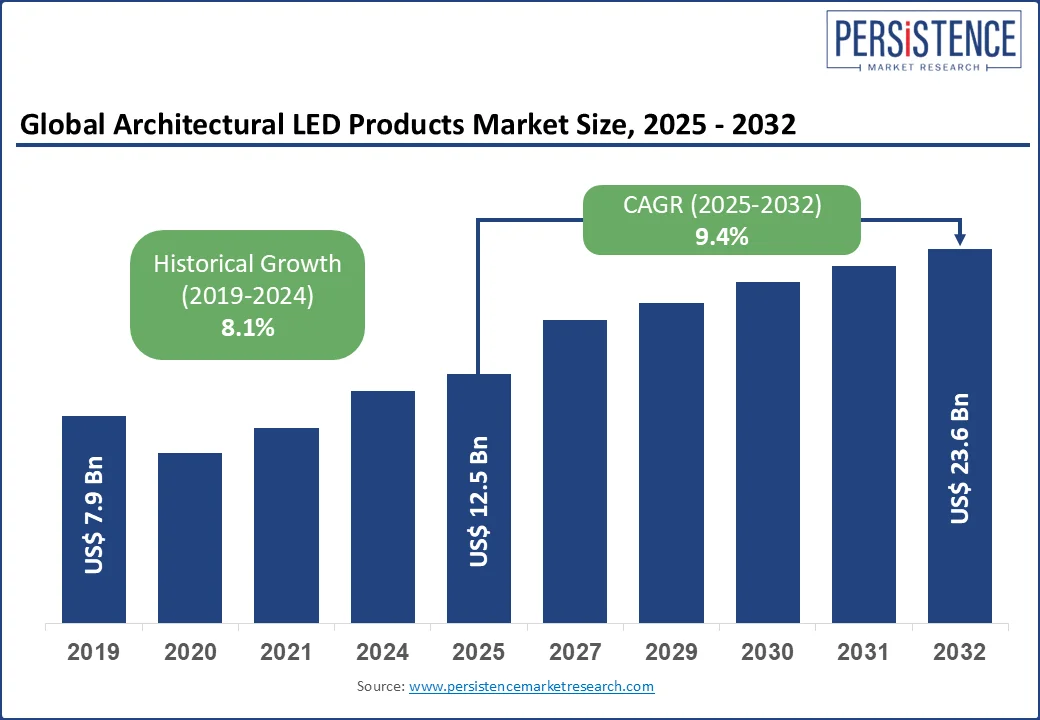

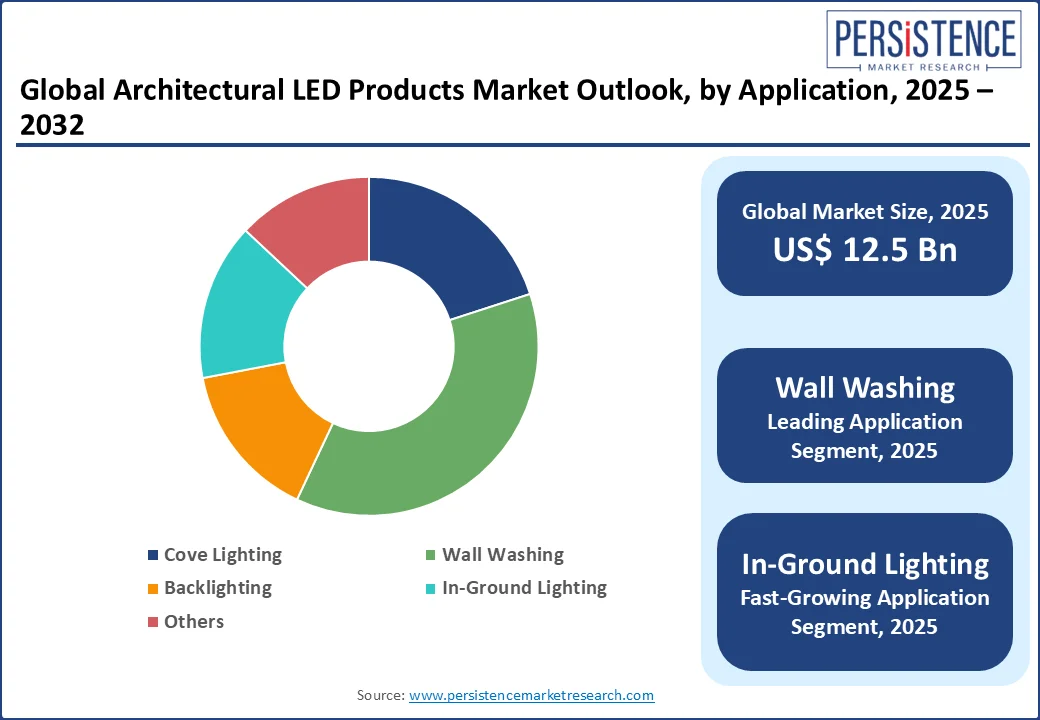

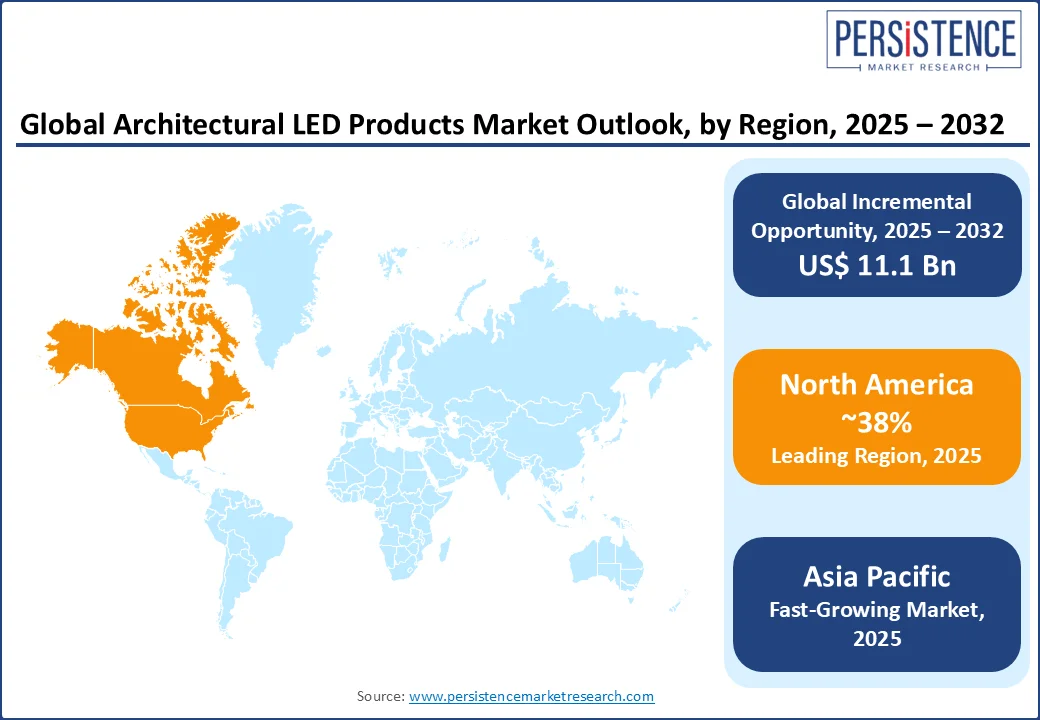

The global architectural LED products market size is likely to be valued at US$ 12.5 Bn in 2025 and is estimated to reach US$ 23.6 Bn in 2032, growing at a CAGR of 9.4% during the forecast period 2025 - 2032. The architectural LED products market is witnessing robust growth driven by the increasing emphasis on energy efficiency and sustainable building solutions. Rising urbanization and smart city initiatives are accelerating the demand for advanced lighting systems that offer both aesthetic appeal and reduced power consumption.

Key Industry Highlights:

- Leading Region: North America leads the architectural LED products market, accounting for over approximately 38% of the share, supported by DOE energy efficiency policies, rebates, and regulations driving LED adoption.

- Asia Pacific is the fastest-growing region, due to rapid urbanization, large-scale infrastructure development, and increasing adoption of energy-efficient lighting in commercial and residential projects.

- Wall washing holds around 37% market share in 2025, due to the growing need for uniform, aesthetically pleasing illumination of building facades, enhancing architectural appeal and visibility in commercial and public spaces.

- In-ground lighting is expanding rapidly, fueled by the growing need for durable, discreet, and aesthetically integrated outdoor illumination in urban landscapes, walkways, parks, and architectural facades.

- Technological advancements, such as tunable white and RGBW LED solutions, are enabling dynamic lighting designs, fueling increased adoption in both new construction and renovation projects.

- LEDs consume significantly less power than traditional lighting, making them ideal for sustainable architectural designs and reducing long-term operational costs.

|

Global Market Attribute |

Key Insights |

|

Architectural LED Products Size (2025E) |

US$ 12.5 Bn |

|

Market Value Forecast (2032F) |

US$ 23.6 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

9.4% |

|

Historical Market Growth (CAGR 2019 to 2024) |

8.1% |

Market Dynamics

Driver - Rapid Urbanization and Infrastructure Development

Rapid urbanization and infrastructure development in emerging economies, particularly in regions such as Asia Pacific and Latin America, are significantly driving the market. Growing urban populations are increasing the demand for energy-efficient lighting in public spaces, commercial centers, and residential developments.

For instance, according to the United Nations' World Urbanization Prospects 2024 Report, the urban population in Asia is projected to increase by 1.2 billion people between 2024 and 2050, with India being the major contributor.

This massive urban growth fuels the need for sustainable lighting solutions such as architectural LEDs, as supported by India’s Smart Cities Mission, which, as per the Indian Ministry of Housing and Urban Affairs (2024), has allocated over 48,000 crores (approximately US$ 5.8 Bn) for infrastructure projects, including energy-efficient lighting for public spaces, directly boosting the demand for LED products in urban development.

Restraint - Retrofitting Challenges in Older Structures

Retrofitting older buildings with modern LED systems often requires significant upgrades to outdated wiring, fixtures, and infrastructure, which adds to the complexity and cost. Retrofitting involves rewiring entire buildings to support LED drivers and controls, which may not align with older electrical systems designed for incandescent or fluorescent lighting.

For instance, according to the U.S. General Services Administration (GSA), converting fluorescent luminaires to LED technology may involve bypassing or entirely replacing ballasts with LED-specific drivers.

This process is not only technically complex but also increases labor and material costs, particularly in large or occupied buildings where access to fixtures and wiring may be restricted. These retrofitting requirements make the transition to LED lighting in older structures a resource-intensive task, often discouraging building owners from making the switch despite the long-term energy savings.

Opportunity - Integration of Smart and IoT-enabled Lighting

The integration of advanced sensors and IoT connectivity into architectural LED systems is transforming how lighting is managed in modern infrastructure. These systems enable dynamic control based on user behavior, daylight levels, and occupancy, significantly improving energy efficiency. According to the U.S. Department of Energy, smart lighting solutions can reduce energy consumption by over 30%, making them essential for sustainable building designs.

These systems are flexible and scalable, enabling facility managers to use centralized platforms to diagnose problems, adjust settings, and remotely monitor performance. This helps to improve energy management in public and commercial areas while also extending the life of lighting equipment. IoT-enabled lighting assists designers in creating immersive environments that seamlessly adjust to changing conditions, optimizing both efficiency and experience in architectural applications where lighting serves as both a functional and aesthetic tool.

Architectural LED Products Market Key Trend

Personalized Lighting Solutions Transforming Architectural Spaces

Architectural LED lighting is evolving from basic illumination to a dynamic design element that enhances spatial aesthetics. Designers now prioritize solutions that not only serve a functional purpose but also help set moods, emphasize architectural details, and align with design themes. This has driven the demand for lighting products that offer customizable features such as varied color temperatures, dimmable brightness, and modular designs.

For instance, Zumtobel’s TECTON II continuous-row lighting system was developed in collaboration with the Italian design studio, Pininfarina. It combines an elegant, minimalistic design with high flexibility, offering 15 poles and multiple circuits to adapt to diverse applications, from offices to industrial settings. This system allows seamless integration into various architectural environments while providing personalized lighting solutions that meet both functional and design needs.

Category-wise Analysis

Product Type Insights

Based on product type, the market is segmented into LED linear fixtures, LED strip lights, LED flood lights, LED spotlights, LED wall washers, and others. Among these, LED linear fixtures dominate due to their versatile design adaptability, enabling seamless integration into modern architectural aesthetics with customizable shapes, lengths, and mounting options. They are becoming popular due to their low maintenance requirements, energy efficiency, and ability to blend in with walls, ceilings, and furniture. The demand for LED linear fixtures in upscale residential and commercial spaces is driven by the need for intelligent lighting controls such as dimming and color tuning, along with design trends favoring open office layouts and modern retail spaces requiring uniform task lighting.

LED strip lights are also witnessing significant growth due to their slim profile and ease of installation, which allows designers and architects to use them creatively across a wide range of applications. Advancements in smart, color-changing, and dimmable options further drive their adoption, making them the preferred choice for modern, energy-efficient designs.

Application Insights

Based on applications, the market is segmented into cove lighting, wall washing, backlighting, in-ground lighting, and others. Among these, wall washing dominates the market with an estimated share of approximately 37% in 2025 due to its ability to uniformly illuminate vertical surfaces, enhancing textures, colors, and spatial openness. It is widely used in galleries, retail stores, offices, and modern homes to highlight architectural details and artwork. The technique supports minimalist design trends while offering energy efficiency through LED technology.

In-ground lighting is emerging as the fastest-growing application, driven by increasing demand for sleek, discreet lighting solutions in urban landscapes, public parks, driveways, and commercial exteriors. It enhances architectural appeal while ensuring safety and durability in high-traffic areas.

Regional Insights

North America Architectural LED Products Market Trends

North America continues to lead the architectural LED products market, accounting for over 38% of market share, driven by strong adoption across commercial, residential, and public infrastructure segments. The U.S. government’s focus on energy efficiency through initiatives such as ENERGY STAR and rebate programs has significantly accelerated the demand. A key regulatory move came in April 2024 when the Department of Energy (DOE) finalized energy efficiency standards for general service lamps, effective from July 2028, raising minimum efficacy from 45 to over 120 lumens per watt. This is expected to save U.S. households US$ 1.6 Bn annually and reduce 70 million metric tons of CO2 emissions over 30 years.

This regulatory shift aligns with the broader need for sustainable and energy-saving solutions, as LEDs are projected to constitute 84% of all lighting installations by 2035, equivalent to saving 569 TWh annually, or the output of 92 large power plants. In Canada, the phase-out of mercury-based HID lamps by December 2028 promotes mercury-free LED adoption in new infrastructure. Provincial programs such as takeCHARGE have provided additional support. For instance, its Energy Savers Kit initiative distributed 2,547 kits containing 7,641 LED bulbs, generating over 2,104 MWh in annual energy savings.

Asia Pacific Architectural LED Products Market Trends

The Asia Pacific region is witnessing the fastest growth in the adoption of architectural LED solutions, propelled by government-led infrastructure development, urbanization, and rising demand for energy-efficient lighting. In India, the landscape has transformed significantly through programs such as UJALA and the Street Lighting National Programme, which have distributed around 368 million LED bulbs and tube lights by June 2023. These initiatives underline the growing need for cost-effective, sustainable lighting in large-scale public and residential settings.

In Japan, the LED sector is advancing through IoT-enabled lighting adoption in public spaces and commercial establishments, driven by energy-efficiency goals and support from the government and smart city projects. This reflects the growing need for intelligent, low-emission lighting integrated with digital infrastructure. Southeast Asian nations are accelerating LED deployment, supported by urban development and foreign investments. For example, Pattaya City upgraded 4,000 streetlights to LEDs to improve safety and reduce energy consumption.

Europe Architectural LED Products Market Trends

The architectural LED products market in Europe is growing steadily, driven by the region’s commitment to smart and green urban infrastructure, strict energy efficiency regulations, and long-term sustainability goals. The European Union (EU) has outlined ambitious initiatives, including the European Green Deal and the Energy Efficiency Directive, which target a 55% reduction in greenhouse gas emissions by 2030 and encourage the phase-out of outdated, high-consumption lighting systems. These policies have spurred widespread adoption of LED-based architectural lighting across public spaces, historical landmarks, and modern urban developments.

Several countries are at the forefront, integrating LED solutions into smart city frameworks, municipal buildings, and heritage sites through national programs and local council efforts. For example, in Spain, the city of Córdoba has launched an ambitious public lighting overhaul, the municipal government approved plans to replace 9,000 high-consumption streetlights with energy-efficient LEDs by the end of its current term, representing 40% LED penetration in public lighting and saving both CO2 emissions and utility costs.

Competitive Landscape

The global architectural LED products market is highly competitive, with diversification into different product forms to cater to varied consumer preferences. Manufacturers are prioritizing innovation and sustainability to strengthen their market position.

Companies such as Signify, Cree Lighting, and Acuity Brands are investing in R&D to develop technologies such as tunable white LEDs, OLEDs, and IoT- and AI-enabled smart controls. These innovations support energy-efficient, customizable lighting for smart cities and human-centric applications. Strategic partnerships and acquisitions, such as Significs' joint venture with Dixon Technologies in India in March 2025 to produce cost-effective LED solutions, are also key strategies for expanding geographic reach and enhancing product portfolios.

Key Industry Developments

- In September 2024, iGuzzini introduced its Trick and EM/360 lighting solutions, focusing on emotional impact and interaction in architectural design. These products leverage dynamic light effects to enhance spatial experiences, catering to modern architectural trends that prioritize ambiance and user engagement.

- In August 2024, AiSPIRE/WAC Lighting launched the VENTRIX Modular Lighting System, a customizable architectural LED platform designed for high-end commercial and residential applications.

Companies Covered in Architectural LED Products Market

- Signify N.V. (Philips Lighting)

- OSRAM GmbH

- Cree Lighting

- Acuity Brands, Inc.

- Zumtobel Group AG

- GE Lighting (under Savant Systems, Inc.)

- Hubbell Incorporated

- Eaton Corporation (Cooper Industries LLC)

- Samsung Electronics Co., Ltd.

- Seoul Semiconductor Co., Ltd.

- Delta Light NV

- Technical Consumer Products, Inc. (TCP)

Frequently Asked Questions

The architectural LED products market is projected to be valued at US$ 12.5 Bn in 2025.

The growing demand for energy-efficient lighting solutions that enhance aesthetic appeal and reduce operational costs drives the need for architectural LED products.

The architectural LED products market is poised to witness a CAGR of 9.4% from 2025 to 2032.

The integration of smart lighting with AI and IoT, along with the rising adoption of human-centric lighting (HCL), presents significant growth opportunities in the architectural LED products market.

Signify N.V. (Philips Lighting), OSRAM GmbH, Cree Lighting, Acuity Brands, Inc., Zumtobel Group AG, and Hubbell Incorporated are among the leading key players.