- Medical Devices

- Aortic Stent Grafts Market

Aortic Stent Grafts Market Size, Share, and Growth Forecast 2026 - 2033

Aortic Stent Grafts Market by Product Type (Abdominal Aortic Stent Grafts, Thoracic Aortic Stent Grafts, Fenestrated / Branched (Complex) Stent Grafts), by Application (Abdominal Aortic Aneurysm (AAA), Thoracic Aortic Aneurysm (TAA), Aortic Dissection & Trauma), End-user (Hospitals, Specialty Clinics, Ambulatory Surgical Centers, Others), and Regional Analysis, 2026 - 2033

Aortic Stent Grafts Market Share and Trends Analysis

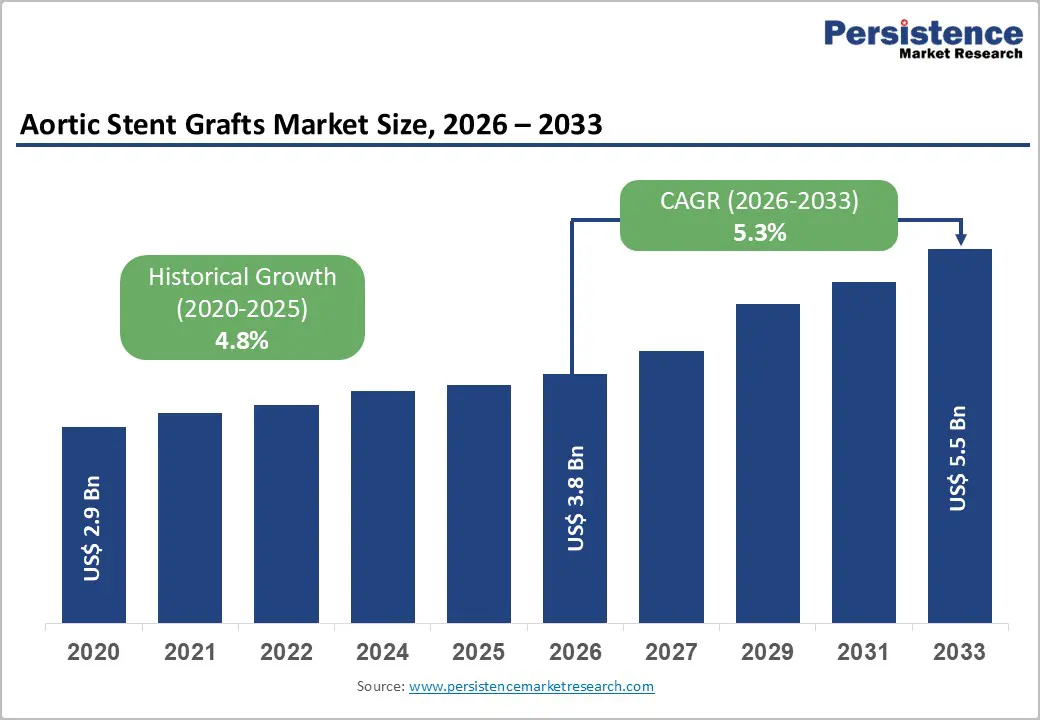

The global aortic stent grafts market size is expected to be valued at US$ 3.8 billion in 2026 and projected to reach US$ 5.5 billion by 2033, growing at a CAGR of 5.3% between 2026 and 2033. This robust growth trajectory is primarily driven by the rapidly aging global population, which exhibits substantially higher prevalence rates of aortic aneurysms requiring endovascular intervention.

The widespread shift toward minimally invasive endovascular aneurysm repair (EVAR) and thoracic endovascular aortic repair (TEVAR) procedures over traditional open surgical repair is accelerating market adoption, as these techniques offer reduced operative mortality (less than 2% compared to 5-10% for open surgery), significantly shorter hospital stays, and faster patient recovery times, making them particularly suitable for elderly and high-risk patient population.

Key Industry Highlights:

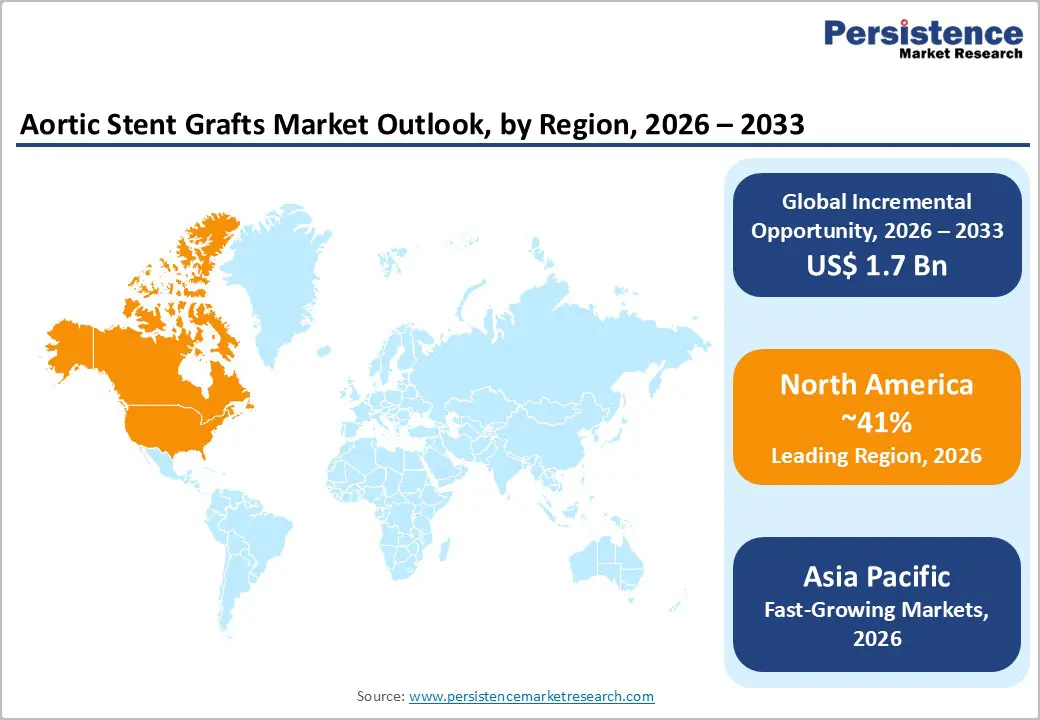

- Leading Region: North America dominates the aortic stent grafts market with approximately 41% share in 2025, driven by advanced healthcare infrastructure, comprehensive reimbursement frameworks, established screening programs mandating ultrasound examination for men aged 65-75 years with smoking history, and rapid adoption of innovative technologies, including complex fenestrated and branched devices for challenging anatomies.

- Fastest Growing Region: Asia Pacific emerges as the fastest-growing regional market with projected compound annual growth rates exceeding 9% through 2033, fueled by rapidly aging populations, expanding healthcare investments in China, India, and Japan, government pricing reforms improving procedure affordability, and growing networks of specialized aortic centers establishing endovascular capabilities previously concentrated in Western markets.

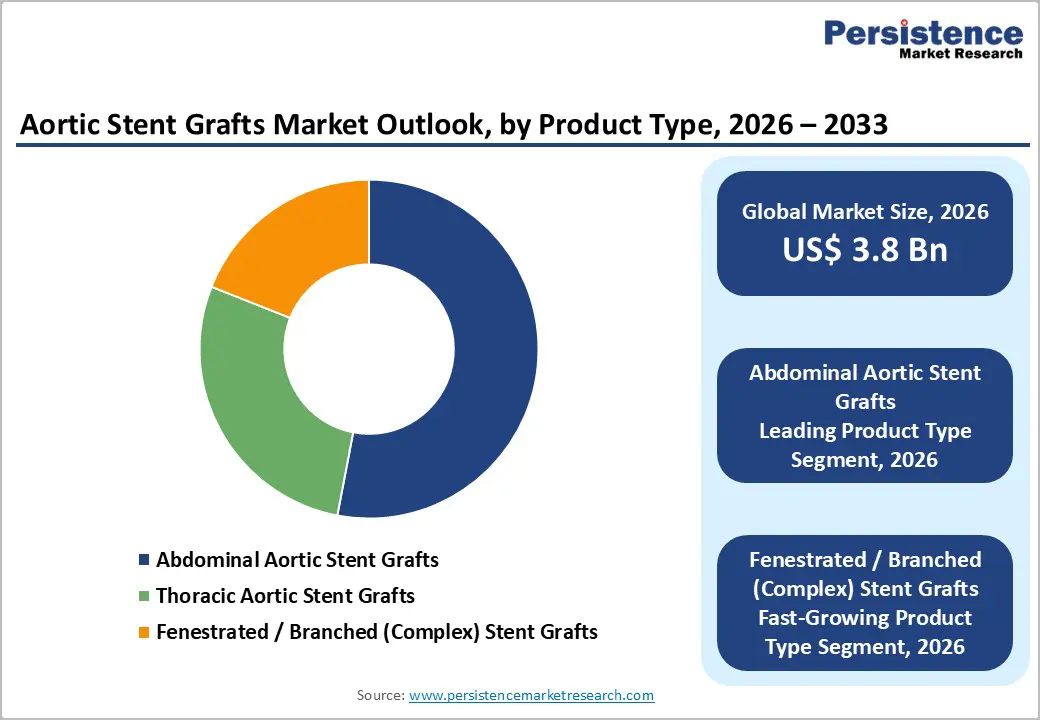

- Dominant Applications: Abdominal aortic stent grafts command approximately 53% product type market share in 2025, supported by substantially higher disease prevalence (infrarenal AAA representing 85% of all aortic aneurysms), robust clinical evidence from decade-long registries demonstrating 42% reduction in aneurysm-related mortality, widespread screening programs, and mature treatment algorithms with technical success rates exceeding 90% even in elderly populations.

| Key Insights | Details |

|---|---|

| Aortic Stent Grafts Market Size (2026E) | US$ 3.8 Bn |

| Market Value Forecast (2033F) | US$ 5.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.8% |

Market Dynamics

Driver - Increasing Geriatric Population and Rising Prevalence of Aortic Aneurysms

The global demographic shift toward an aging population is the primary driver of aortic stent graft market expansion, as abdominal aortic aneurysm (AAA) predominantly affects individuals aged 65 years and older, with prevalence rates ranging from 4.0% to 7.6% in men, according to screening data from major clinical trials. According to the Centers for Disease Control and Prevention (CDC), aortic aneurysms or aortic dissections were responsible for 9,904 deaths in 2019 in the United States alone, with approximately 59% of these fatalities attributed specifically to aortic aneurysm complications.

The aging demographic is further compounded by lifestyle-related risk factors, including hypertension, hyperlipidemia, smoking, obesity, and diabetes, which collectively weaken arterial walls and accelerate aneurysm formation. In 2021, the CDC reported that 38.4 million people (11.6% of the US population) had diabetes, a condition that significantly heightens vascular complications and increases surgical risk, thereby making minimally invasive stent grafts the preferred intervention modality. The mortality rate from ruptured abdominal aortic aneurysm exceeds 80%, creating urgent clinical imperatives for early detection through screening programs and prophylactic endovascular repair before rupture occurs.

Technological Advancements and Regulatory Approvals Expanding Treatment Options

Continuous innovation in stent graft design, delivery systems, and biocompatible materials is substantially expanding the treatable patient population and driving market growth through improved clinical outcomes. In October 2025, Medtronic plc achieved a landmark regulatory milestone by receiving U.S. Food and Drug Administration (FDA) labeling approval for its Endurant stent graft system, becoming the first and only company to remove the ruptured abdominal aortic aneurysm (rAAA) treatment warning from its device instructions, thereby aligning regulatory labeling with real-world endovascular practices. The Endurant system, supported by the ENGAGE 10-year global registry, which demonstrates consistently high rates of sac regression and low aneurysm-related mortality, has been used to treat more than 500,000 patients worldwide over the past decade. The development of fenestrated and branched stent grafts has revolutionized the treatment of complex anatomies, enabling endovascular repair of juxtarenal, suprarenal, and thoracoabdominal aneurysms that previously required high-risk open surgery. Multicenter clinical studies report technical success rates exceeding 97% and 30-day mortality rates below 5%.

Restraints - High Procedural Costs and Reimbursement Challenges

The substantial financial burden associated with aortic stent graft devices and endovascular procedures represents a significant market restraint, particularly in price-sensitive and emerging healthcare markets. The cost of advanced stent graft systems can range from 50,000 to 120,000 RMB (approximately $7,000 to $17,000) per device in markets such as China, with hospital markups historically reaching 140% before recent regulatory interventions by the National Healthcare Security Administration mandated price reductions of approximately 40%. In the United States, the Centers for Medicare & Medicaid Services (CMS) reimburses EVAR procedures under the Outpatient Prospective Payment System (OPPS) at approximately $15,000 per case, which may not fully cover institutional costs for complex procedures requiring custom-made fenestrated or branched devices. The economic burden extends beyond initial device costs to encompass advanced imaging guidance, specialized hybrid operating room infrastructure, and extended surveillance requirements for detecting late complications such as endoleaks, stent migration, or device structural failure. These cumulative costs create accessibility barriers in resource-limited settings and contribute to disparities in treatment availability across different geographic regions and healthcare systems.

Risk of Device-Related Complications and Need for Reintervention

Post-procedural complications inherent to endovascular stent graft technology, including endoleaks, device migration, and late graft failure, represent significant clinical challenges that may dampen market enthusiasm among certain physician populations. Type I and Type III endoleaks, occurring in 7.8% to 10.8% of cases in recent multicenter thoracic endovascular aortic repair studies, require secondary interventions to prevent aneurysm rupture, thereby increasing overall treatment costs and patient burden. Registry data indicate that reintervention rates following EVAR can reach 10% during a 2-year follow-up period, with some patients requiring conversion to open surgical repair when endovascular salvage fails. The risk of retrograde aortic dissection, while rare, carries mortality rates up to 37.1% and remains a feared complication, particularly associated with thoracic endovascular procedures in the aortic arch. Additionally, late branch endograft failure, particularly in renal arteries after fenestrated repairs, necessitates continued surveillance protocols that entail ongoing healthcare resource utilization. These device-related limitations, combined with the necessity for specialized vascular surgery expertise that may be unavailable in many medical centers, constrain broader market penetration and slow adoption rates in certain geographic regions.

Opportunity - Expansion of Fenestrated and Branched Stent Graft Technology for Complex Anatomies

The fenestrated and branched (complex) stent graft segment is the fastest-growing product category and presents substantial untapped market opportunities for manufacturers and healthcare providers, as these advanced devices enable endovascular treatment of approximately 20-30% of patients with aortic aneurysms who previously required high-risk open surgery due to unfavorable anatomy. Clinical evidence from multicenter registries demonstrates that custom-designed fenestrated and branched devices achieve technical success rates of 98.3% and 98.7%, respectively, with 30-day mortality rates of 3.8% and 5.4%, representing significant improvements over historical open repair outcomes in a comparable high-risk population.

In October 2024, the FDA approved W. L. Gore & Associates' Excluder Thoracoabdominal Branch Endoprosthesis (TAMBE), the first FDA-approved stent graft designed for minimally invasive repair of complex thoracoabdominal aortic aneurysms, with the device offering patients shorter recovery times, reduced hospital stays, and lower complication rates compared to traditional open surgery. As physician training programs expand and more centers develop expertise in complex endovascular techniques, the addressable patient population for these premium-priced devices will grow substantially, creating significant revenue opportunities for innovative device manufacturers.

Growing Adoption of Ambulatory Surgical Centers and Outpatient EVAR Procedures

The accelerating shift of endovascular aneurysm repair procedures from traditional inpatient hospital settings to ambulatory surgical centers (ASCs) represents a transformative market opportunity, driven by cost-containment pressures, improved device profiles that enable same-day discharge, and patient preferences for less-disruptive treatment experiences. Ambulatory surgical centers are experiencing the fastest growth among end-user segments, with projections indicating a compound annual growth rate of 12.5%, as device miniaturization and streamlined procedural protocols enable safer outpatient treatments for appropriately selected patients with straightforward anatomies and low surgical risk profiles. In July 2023, Adventist HealthCare opened a new Ambulatory Surgery Center offering multi-specialty outpatient care, including minimally invasive procedures for vascular conditions such as aortic aneurysms, demonstrating the expanding infrastructure supporting this care model transition. The economic advantages of ASC-based EVAR are substantial, with procedural costs typically 30-40% lower than hospital-based interventions due to reduced facility fees, shorter procedure times, and elimination of overnight stays. The growing acceptance of EVAR and fenestrated EVAR procedures in outpatient settings, facilitated by advances in local anesthesia techniques, percutaneous vascular closure devices, and enhanced recovery protocols, is democratizing access to endovascular repair while simultaneously creating market opportunities for ASC operators, device manufacturers offering lower-profile delivery systems, and healthcare systems seeking to optimize cardiovascular service line efficiency and profitability.

Category-wise Analysis

Product Type Insights

Abdominal aortic stent grafts dominate the product category, accounting for approximately 53% of the market in 2025, driven by the substantially higher prevalence of abdominal aortic aneurysms relative to thoracic or thoracoabdominal pathologies. The clinical evidence supporting abdominal EVAR is exceptionally robust, with landmark randomized controlled trials demonstrating 42% reduction in aneurysm-related mortality over 13 years of follow-up and a number needed to screen of 305 men to prevent one AAA death according to systematic reviews. Leading devices in this segment include Medtronic's Endurant family, which achieved first-in-industry FDA labeling for ruptured AAA treatment in 2025, and W. L. Gore & Associates' Excluder AAA Device Family, both supported by decade-long registry data demonstrating high rates of sac regression and low aneurysm-related mortality.

The technical success rate for abdominal EVAR exceeds 90% even in the octogenarian population, with contemporary 30-day mortality rates of 2.28% in elderly patients, substantially lower than the 5-10% mortality associated with open surgical repair. The segment's market leadership is further reinforced by widespread screening programs, particularly the U.S. Preventive Services Task Force recommendation for one-time ultrasound screening in men aged 65-75 years with a history of smoking, which generates approximately 1.5 million annual screening examinations and 60,000 EVAR procedures in the United States alone.

Application Insights

Abdominal aortic aneurysm (AAA) treatment constitutes the leading application segment, capturing 65% share in 2025, reflecting both disease epidemiology and the maturity of endovascular treatment protocols for infrarenal aortic pathology. AAA predominantly affects men over 65 years of age, with additional risk stratification based on smoking history (current and former smokers exhibiting 4-8 fold increased risk), family history (first-degree relatives facing 2-3 fold elevated risk), and comorbid conditions including hypertension, hyperlipidemia, and chronic obstructive pulmonary disease. Current clinical practice guidelines from the Society for Vascular Surgery recommend elective repair when the AAA diameter reaches 5.5 cm in males and 5.0 cm in females, or when rapid expansion exceeding 1.0 cm per year is documented, criteria that balance rupture risk against procedural complications. The segment's dominance is underpinned by the fact that 80% of intact AAA repairs in the United States are now performed with EVAR, according to nationwide trend analyses, reflecting the procedure's advantages of reduced hemodynamic changes, decreased blood transfusion requirements, shorter intensive care and hospital stays, and favorable cost-to-outcome ratios. While thoracic aortic aneurysm treatment and aortic dissection management currently represent smaller application segments, they exhibit faster growth trajectories as technological innovations in low-profile delivery systems, enhanced imaging guidance, and specialized graft configurations improve treatment feasibility for these anatomically complex and clinically challenging conditions.

Regional Insights

North America Aortic Stent Grafts Market Trends and Insights

North America holds the largest regional market share at approximately 41% in 2025, underpinned by its advanced healthcare infrastructure, robust reimbursement frameworks, high disease awareness, and well-established aortic aneurysm screening programs. The United States leads regional growth, supported by Society for Vascular Surgery (SVS) clinical practice guidelines mandating ultrasound screening for men aged 65-75 years with a smoking history, generating approximately 1.5 million annual screening examinations that facilitate early aneurysm detection and prophylactic intervention before rupture risk escalates. The Centers for Medicare & Medicaid Services (CMS) provides comprehensive reimbursement coverage for both screening and therapeutic interventions under the Outpatient Prospective Payment System, with typical reimbursement of approximately $15,000 per EVAR case, supporting procedure accessibility across a diverse patient population.

Asia Pacific Aortic Stent Grafts Market Trends and Insights

Asia-Pacific emerges as the fastest-growing regional market, projected to expand at a compound annual growth rate (CAGR) exceeding 9% by 2033, driven by rapidly aging populations in developed economies, expanding healthcare infrastructure in emerging markets, increasing disease awareness, and growing adoption of minimally invasive treatment paradigms. China is the largest and most dynamic market in the region, where government healthcare reforms are dramatically improving access to procedures. Japan exhibits the most mature market profile in Asia-Pacific, characterized by advanced adoption of healthcare technology, comprehensive national health insurance coverage, sophisticated medical device regulatory frameworks, and high standards for clinical evidence generation. Japanese medical societies encourage the development of "region-ready" graft designs utilizing domestically manufactured nitinol and polyester fabrics to reduce geopolitical supply chain vulnerabilities. India presents an enormous growth opportunity, with an expanding middle class, rising healthcare expenditure, a growing cardiovascular disease burden, and government initiatives, including the potential implementation of national aneurysm screening programs similar to those established in Western markets.

Competitive Landscape

The aortic stent grafts market is highly competitive and moderately consolidated, dominated by a few global players with strong clinical portfolios and extensive regulatory approvals, alongside several regional and emerging manufacturers. Competition centers on device durability, delivery-system flexibility, imaging compatibility, and the ability to treat complex anatomies through customized or off-the-shelf solutions. Continuous product innovation, clinical trial expansion, and next-generation graft designs are key differentiators. Strategic initiatives, including mergers, acquisitions, geographic expansion, and partnerships with hospitals, support market positioning.

Key Developments:

- Medtronic plc announced that it had received U.S. Food and Drug Administration (FDA) labeling approval for its Endurant stent graft system, adding clinical evidence for ruptured abdominal aortic aneurysm (rAAA) treatment and removing the previous rAAA warning from the system’s Instructions for Use (IFU). This regulatory update made Medtronic the first and only company to eliminate the rAAA warning from its stent graft IFU, aligning the device’s labeling with real-world clinical practice and physician training to support confident decision-making in emergency settings.

Companies Covered in Aortic Stent Grafts Market

- Medtronic plc

- W. L. Gore & Associates

- Cook Medical

- Terumo Corporation

- Endologix

- Lombard Medical

- MicroPort Scientific

- Cordis

- Becton, Dickinson and Company

- Jotec

- Lifetech Scientific

- Artivion

- Others

Frequently Asked Questions

The global aortic stent grafts market is expected to be valued at US$ 3.8 billion in 2026.

Primary demand drivers include the rapidly expanding geriatric population (with AAA prevalence of 4.0-7.6% in men over 65 years), superior clinical outcomes of endovascular repair compared to open surgery (procedural mortality below 2% versus 5-10%), continuous technological innovations including fenestrated and branched devices expanding treatable patient populations, landmark regulatory approvals such as Medtronic's 2025 FDA clearance for ruptured AAA treatment, and established screening programs facilitating early aneurysm detection before rupture occurs.

North America dominates the global aortic stent grafts market with approximately 41% market share in 2025, supported by advanced healthcare infrastructure, comprehensive Medicare and commercial insurance reimbursement, Society for Vascular Surgery guidelines mandating screening for men aged 65-75 years with smoking history (generating 1.5 million annual examinations), rapid adoption of innovative technologies, and extensive networks of specialized aortic centers delivering complex endovascular procedures.

The increasing incidence of abdominal and thoracic aortic aneurysms, especially in aging populations, is driving demand for stent graft interventions.

Medtronic plc, W. L. Gore & Associates, Cook Medical, and Terumo Corporation.