- Pharmaceuticals

- Antacids Market

Antacids Market Size, Share, and Growth Forecast, 2025 - 2032

Antacids Market By Formulation (Tablets, Liquids/Suspensions), Active Ingredient (Calcium Carbonate, Magnesium Compounds), Indication (Heartburn, GERD), Distribution Channel (Hospital Pharmacies), and Regional Analysis for 2025 - 2032

Antacids Market Size and Trends Analysis

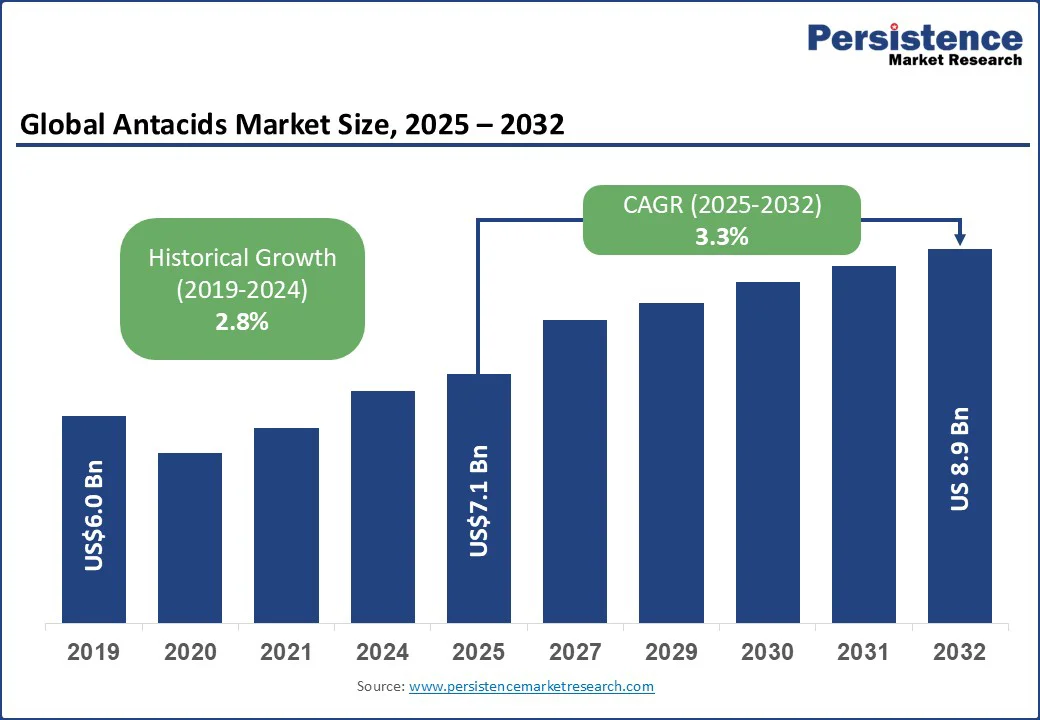

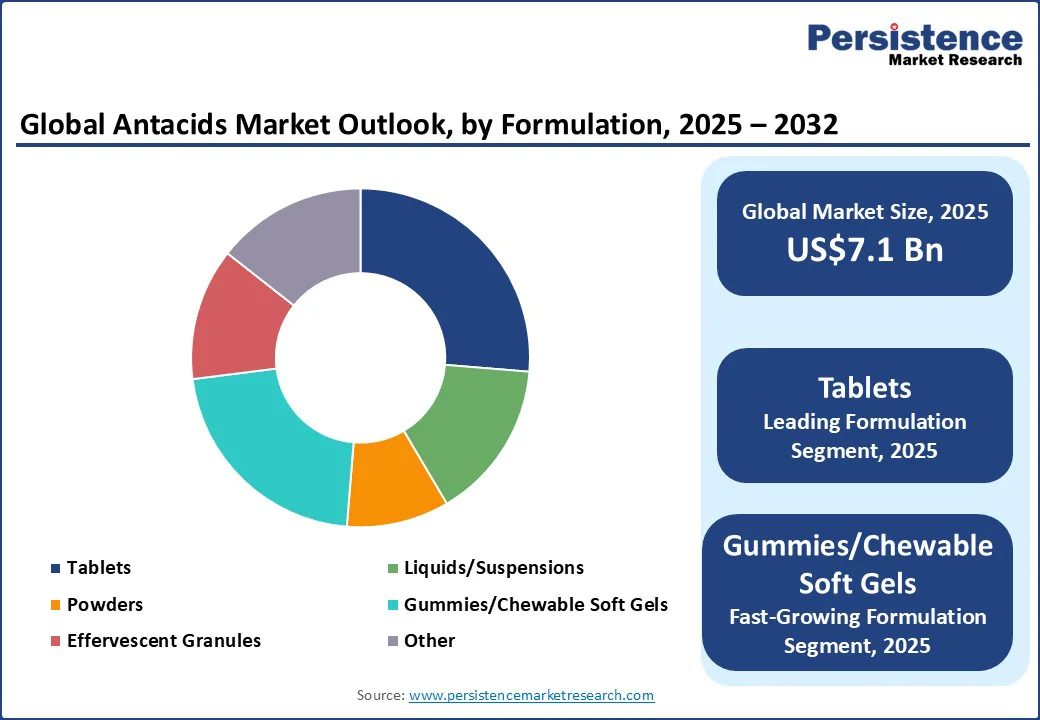

The global antacids market size is likely to be valued at US$7.1 Bn in 2025 and is estimated to reach US$8.9 Bn in 2032, growing at a CAGR of 3.3% during the forecast period 2025-2032, fueled by rising incidence of gastrointestinal disorders, changing dietary habits, and increasing consumer preference for over-the-counter remedies. Leading companies are embracing unique marketing strategies, including product diversification, flavor variations, and direct-to-consumer digital campaigns, to improve brand visibility and engagement.

Key Industry Highlights

- New Product Launch: Akums Drugs & Pharmaceuticals launched an advanced anti-reflux antacid, Sodium Alginate + Potassium Bicarbonate chewable tablet, approved by the Drugs Controller General of India (DCGI). It falls under the category of reflux suppressants.

- Leading Formulation: Tablets are projected to hold approximately 26.3% share in 2025, as they provide convenience, portability, long shelf life, and ease of use.

- Dominant Active Ingredient: Calcium carbonate, approximately 39.7% of the antacids market share in 2025, due to its ability to provide rapid and effective acid neutralization.

- Key Indication: GERD recorded about 50.1% of the market share in 2025, as antacids deliver immediate neutralization of stomach acid, providing fast symptom relief.

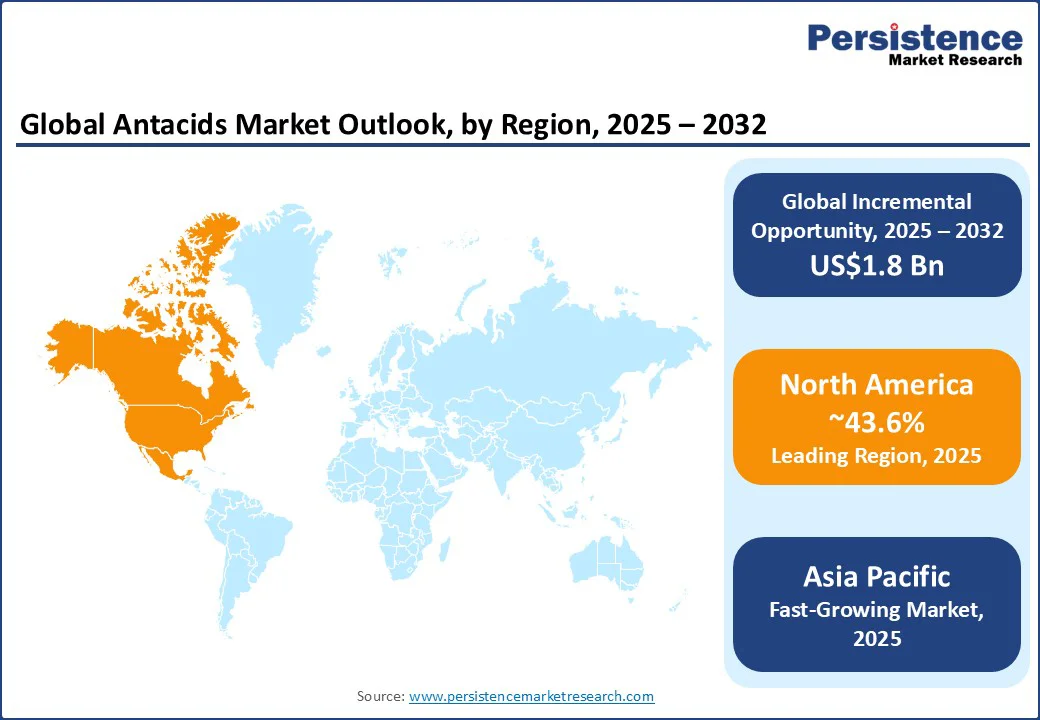

- Leading Region: North America, with about 43.6% share in 2025, due to a large aging population with gastrointestinal disorders.

- Fastest-growing Region: Asia Pacific, with around 5.2% CAGR through 2032, spurred by the expansion of retail pharmacies and increasing healthcare access.

| Key Insights | Details |

|---|---|

|

Antacids Market Size (2025E) |

US$7.1 Bn |

|

Market Value Forecast (2032F) |

US$8.9 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

3.3% |

|

Historical Market Growth (CAGR 2019 to 2024) |

2.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Aging Demographics and Increased Gastrointestinal Disorders

As populations in regions such as Europe and North America continue to age, the prevalence of gastrointestinal issues such as GERD and indigestion is increasing. As per the National Institute of Diabetes and Digestive and Kidney Diseases, digestive diseases affect 60 to 70 million people in the U.S. alone.

Older adults often experience diminished gastric acid secretion, leading to digestive discomfort and increased antacid usage. For instance, in Europe, the aging population has been identified as a key factor driving the demand for antacids, as older individuals are more susceptible to digestive issues.

Sedentary Lifestyles and Dietary Choices

Modern lifestyles characterized by prolonged sitting and poor dietary habits contribute to gastrointestinal problems. High-fat, spicy foods, and irregular eating patterns can exacerbate conditions such as acid reflux. A study revealed that large portions of spicy or greasy foods, sweets, high-fat meals, or drinking too much alcohol or caffeinated drinks can contribute to acid reflux.

Self-medication and Over-the-counter Accessibility

The growing trend of self-medication, facilitated by the easy availability of over-the-counter antacids, empowers consumers to manage mild gastrointestinal symptoms independently. This shift is particularly noticeable in countries such as India, where the OTC market is expanding rapidly, suggesting that consumers are increasingly taking medications on their own.

Safety Concerns Associated with Prolonged Antacid Use

Extended use of antacids can lead to several health complications. For instance, chronic consumption tends to result in acid rebound, where the stomach produces more acid than before, exacerbating symptoms. Additionally, overuse can cause electrolyte imbalances, leading to conditions such as hypercalcemia or low magnesium levels, which can affect heart and muscle function.

Long-term use may also increase the risk of kidney issues and interfere with the absorption of essential nutrients, potentially leading to deficiencies. These safety concerns have prompted healthcare professionals to recommend limiting antacid use and exploring alternative treatments for managing gastrointestinal disorders.

Rising Preference for Proton Pump Inhibitors and H2 Antagonists

The growing adoption of Proton Pump Inhibitors (PPIs) and H2 antagonists is impacting the demand for traditional antacids. PPIs, such as omeprazole and lansoprazole, deliver highly effective and long-lasting relief for conditions such as Gastroesophageal Reflux Disease (GERD) and peptic ulcers.

These medications work by reducing stomach acid production, providing more sustained symptom control compared to antacids. As a result, patients and healthcare providers are increasingly favoring PPIs and H2 antagonists over antacids, leading to a shift in treatment preferences and affecting the antacids market.

Developments in Formulation and Delivery Technologies

Recent developments in antacid formulations are improving their efficacy and patient compliance. For instance, Gastro-Retentive Drug Delivery Systems (GRDDS) such as floating tablets have been developed to prolong the residence time of antacids in the stomach, allowing for sustained acid neutralization. These systems utilize materials such as guar gum and xanthan gum to create a buoyant matrix that remains afloat in gastric fluids, thereby refining therapeutic outcomes.

Controlled-release antacid tablets have also been formulated using a combination of gel-forming agents and water-insoluble lipids, providing prolonged relief from acid reflux and reducing the frequency of dosing. Such developments cater to the high demand for effective and convenient antacid therapies.

Increased Healthcare Spending in Developing Markets

The rising healthcare expenditures in emerging economies present a new opportunity for the market. As disposable incomes increase and access to healthcare improves, there is a rising demand for over-the-counter medications, including antacids. Countries such as India and China are witnessing a surge in healthcare investments.

This trend is leading to better availability and affordability of antacid products. This trend is expected to boost market growth, as consumers in these regions become proactive about managing gastrointestinal health and seek accessible treatment options.

Expansion of Retail and Online Distribution Channels

The proliferation of retail pharmacies and the growth of digital commerce are transforming the accessibility of antacids. In regions such as North America, retail pharmacies accounted for a significant share of antacid sales, and this trend is expected to continue with a projected CAGR of 3.1% from 2025 to 2032.

The rise of e-commerce platforms further allows consumers to purchase antacids conveniently from home, broadening the market reach and catering to the increasing preference for online shopping. This dual-channel distribution approach improves product availability and consumer choice, augmenting market expansion.

Category-wise Analysis

Formulation Insights

Tablets are projected to account for around 26.3% of the market share in 2025, owing to their convenience and portability. They are easy to carry, require no preparation, and have a long shelf life, making them ideal for on-the-go relief from heartburn and indigestion. While liquid forms may act faster, tablets are often preferred for their ease of use and longer shelf stability.

Gummies and chewable tablets are gaining popularity due to their palatable taste and ease of consumption. These formats are specifically appealing to children and individuals who dislike swallowing pills. For instance, TUMS Chewy Bites provide heartburn relief in a berry-flavored chewable form, improving user compliance.

Active Ingredient Insights

Calcium carbonate is expected to hold approximately 39.7% of the market share in 2025, backed by its potent acid-neutralizing capacity. It effectively neutralizes stomach acid, providing rapid relief from heartburn and indigestion. Additionally, it delivers the benefit of calcium supplementation, which is advantageous for individuals with low calcium intake. Products such as TUMS and Rolaids utilize calcium carbonate for its dual action, thereby neutralizing acid and supplementing calcium levels.

Alginate-based antacids are seeing a considerable growth due to their unique mechanism of action. When alginate comes into contact with stomach acid, it forms a gel-like barrier that floats on top of the stomach contents, preventing acid reflux into the esophagus. This property provides effective relief from GERD symptoms.

Indication Insights

GERD is poised to account for about 50.1% of the market share in 2025 as it involves frequent acid reflux, causing irritation of the esophagus. Antacids provide rapid neutralization of stomach acid, delivering quick symptom relief and reducing discomfort caused by regurgitated acid.

Heartburn, a burning sensation in the chest or throat, results from the backflow of stomach acid and is often an early symptom of GERD. Antacids are highly effective in neutralizing this excess acid, providing fast relief from the discomfort. Products such as Maalox and Rolaids are commonly used for occasional heartburn, making them a preferred first-line remedy for consumers who experience sporadic symptoms.

Regional Insights

North America Antacids Market Trends

In 2025, North America is estimated to record approximately 43.6% of the market share. It is driven by an aging population, increased prevalence of gastrointestinal disorders, and a preference for over-the-counter medications. The U.S. market is characterized by a diverse range of products, including chewable tablets, liquids, and effervescent formulations.

Retail pharmacies play a major role in distribution, holding a substantial share of the market. In addition, the rise of digital commerce has made antacids more accessible, allowing consumers to purchase these products online with ease. Key players are focusing on innovation to develop safe and highly effective antacid formulations.

Asia Pacific Antacids Market Trends

Asia Pacific will likely exhibit a considerable CAGR of nearly 5.2% through 2032. China, India, and Japan are witnessing a surge in antacid consumption due to lifestyle changes, dietary habits, and increased stress levels. For example, in India, the market is projected to rise at a CAGR of 9.3% during the forecast period, attributed to the expansion of retail pharmacies and e-commerce platforms.

However, the market faces challenges such as regulatory scrutiny and quality control issues. In 2024, India's drug regulator identified over 50 drugs, including popular antacids such as Pan-D and Pantocid, as substandard or counterfeit, highlighting the need for stronger quality control measures.

Europe Antacids Market Trends

In Europe, market growth is spurred by a diverse range of products, including chewable tablets, liquids, and effervescent formulations. Retail pharmacies play a key role in distribution, holding a considerable share of the market. Additionally, the rise of digital commerce has made antacids more accessible, allowing consumers to purchase these products online with ease.

Despite the availability of alternative treatments such as Proton Pump Inhibitors (PPIs) and H2 antagonists, antacids remain a popular choice for quick relief from heartburn and acid reflux. However, there is an increasing awareness of the potential side effects associated with long-term antacid use, such as electrolyte imbalances and kidney issues, leading to a shift toward balanced treatment approaches.

Competitive Landscape

The global antacids market is characterized by intense competition among established pharmaceutical companies and emerging regional players. Key global players such as GlaxoSmithKline, Abbott Laboratories, Pfizer, and Sun Pharmaceuticals dominate the market through a combination of strong brand portfolios, extensive distribution networks, and constant investments in research and development. These companies focus on product development, strategic marketing, and expanding their presence in both developed and emerging markets to maintain their competitive advantage.

Business Strategies

Innovation remains central, with companies investing in research to introduce new active ingredients and formulations that deliver improved efficacy and convenience. Cost leadership is pursued by optimizing production and supply chain operations to reduce expenses. Market expansion is facilitated by identifying and entering new geographic areas, mainly in Asia Pacific, where demand for over-the-counter medications is increasing.

Key Industry Developments

- In August 2025, Mankind Pharma launched a marketing campaign for its Gas-O-Fast antacid brand focused on local solutions for digestive issues. The new campaign proudly positions the product as the Asli Indian Solution.

- In July 2025, Abbott introduced Digene Insta On The Go, a ready-to-use and water-free antacid solution to provide quick relief from heartburn, acidity, and indigestion. The product provides relief in just two seconds and is aimed at people looking for convenience while managing gastrointestinal discomfort.

Companies Covered in Antacids Market

- Bayer AG

- Johnson & Johnson (Kenvue)

- Haleon Plc

- WellSpring Pharmaceutical Corporation

- Sanofi S.A.

- Sun Pharmaceutical Industries Ltd.

- CVS Health Corporation

- Advance Pharmaceutical Inc.

- Takeda Pharmaceutical Company Ltd.

- Reckitt Benckiser Group Plc

- Safetec Of America Inc.

- Dr. Reddy's Laboratories Ltd.

- Perrigo Company Plc

- Procter & Gamble Co.

Frequently Asked Questions

The antacids market is projected to reach US$7.1 Bn in 2025.

The rising prevalence of GERD and the increasing preference for over-the-counter gastrointestinal remedies are the key market drivers.

The antacids market is poised to witness a CAGR of 3.3% from 2025 to 2032.

The increasing adoption of chewable gummies and the expansion of e-commerce channels are the key market opportunities.

Bayer AG, Johnson & Johnson (Kenvue), and Haleon Plc are a few key market players in the antacids market.