- Medical Devices

- Alexandrite Laser Treatment Market

Alexandrite Laser Treatment Market Size, Share, and Growth Forecast 2026 - 2033

Alexandrite Laser Treatment Market by Product (Fixed Spot Size Lasers, Variable/Adjustable Spot Size Lasers), by Indication (Hair Removal, Tattoo Removal, Vascular Lesions, Pigmented Lesions, Others), by End User (Hospitals, Laser Treatment Centers, Specialty Clinics, Ambulatory Surgical Centers), by Regional Analysis, 2026 - 2033

Alexandrite Laser Treatment Market Size and Trends Analysis

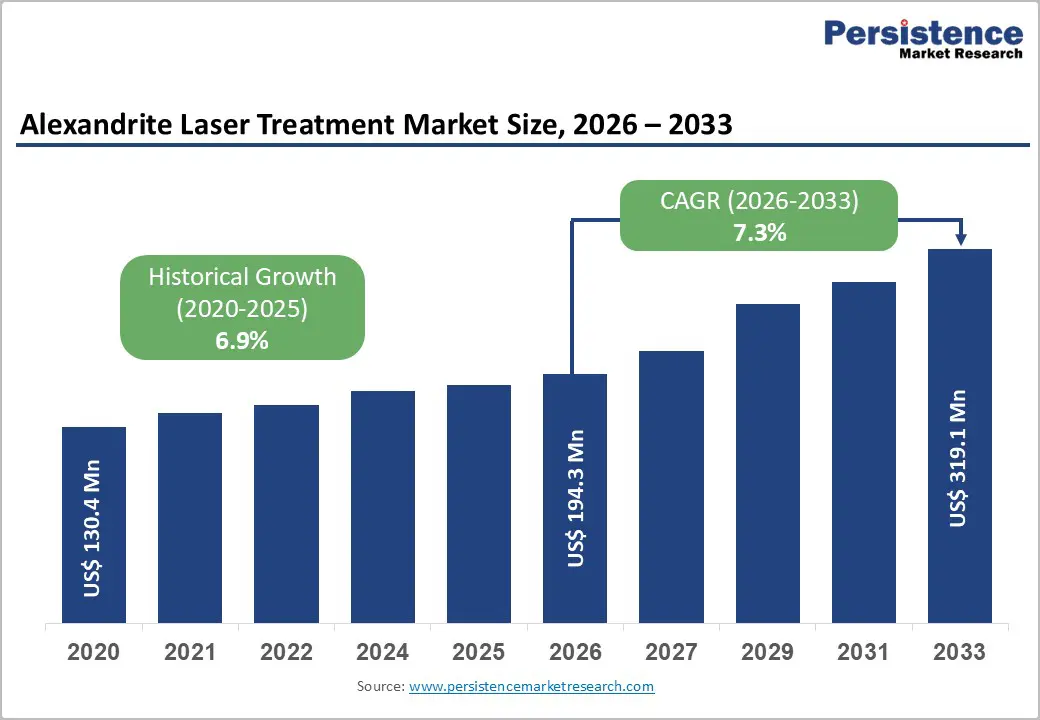

The global Alexandrite Laser Treatment Market size is expected to be valued at US$ 194.3 million in 2026 and projected to reach US$ 319.1 million by 2033, growing at a CAGR of 7.3% between 2026 and 2033.

The market growth is primarily driven by the escalating demand for non-invasive aesthetic and dermatological procedures combined with technological innovations in laser systems. Aging populations worldwide increasingly seek minimally invasive solutions for hair removal, tattoo elimination, and pigmented lesion treatment. Furthermore, the adoption of AI-integrated laser platforms and dual-wavelength technologies that enhance treatment precision across diverse skin types is accelerating market expansion. Regulatory approvals from authoritative bodies like the FDA and endorsements from prestigious organizations such as the American Society for Dermatologic Surgery (ASDS) continue to strengthen consumer confidence and professional adoption rates globally.

Key Market Highlights

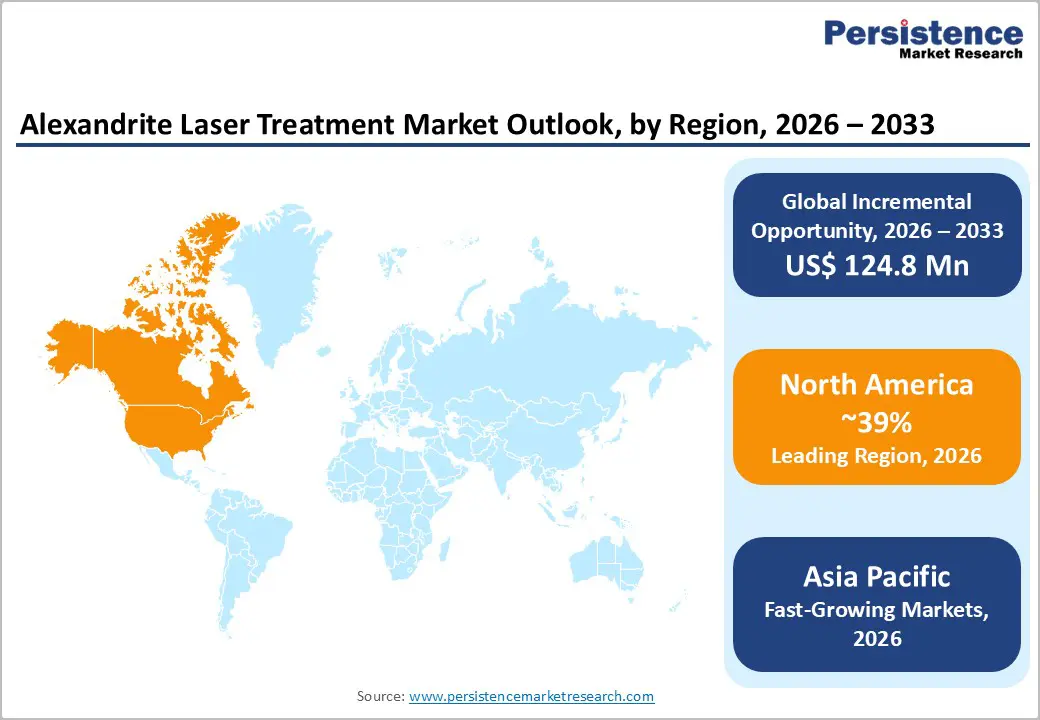

- North America maintains dominant regional positioning with 39% global market share driven by premium healthcare infrastructure, regulatory excellence through FDA approvals, and established aesthetic medicine ecosystems supporting professional adoption and consumer demand.

- Asia Pacific emerges as the fastest-growing region with 14.3% projected CAGR through 2033, driven by healthcare infrastructure expansion in China, India, and ASEAN nations, rising disposable incomes, and medical tourism growth creating incremental demand for advanced dermatological treatments.

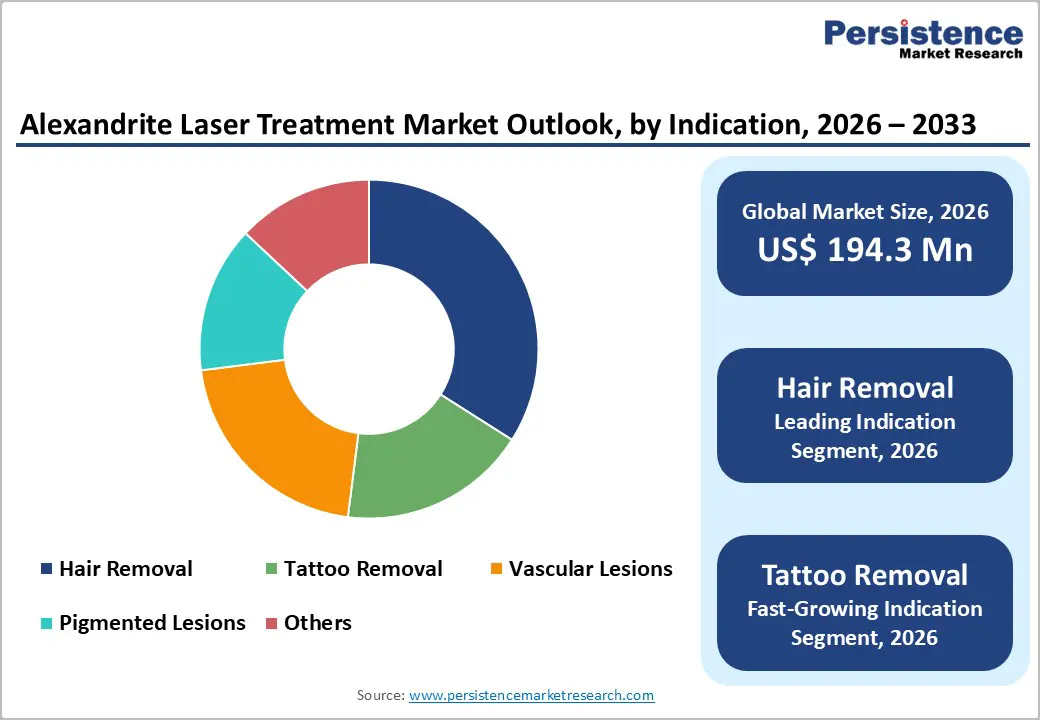

- Hair Removal represents the dominant segment indication with 36% market share in 2025, reflecting proven clinical efficacy of 755nm wavelength targeting melanin in hair follicles, strong physician endorsements, and consumer preference for non-invasive permanent hair reduction solutions.

- Tattoo Removal emerges as the fastest-growing indication segment with projected double-digit CAGR through 2033, driven by superior efficacy for blue and green pigment removal, advancing clinical outcomes exceeding 95% pigment clearance, and changing social attitudes supporting tattoo modification procedures.

- Healthcare infrastructure expansion in Asia Pacific combined with rising aesthetic procedure demand creates substantial growth opportunities for market participants through regional partnerships, localized pricing strategies, and professional training initiatives supporting emerging market development.

| Key Insights | Details |

|---|---|

|

Alexandrite Laser Treatment Market Size (2026E) |

US$ 194.3 million |

|

Market Value Forecast (2033F) |

US$ 319.1 million |

|

Projected Growth CAGR (2026-2033) |

7.3% |

|

Historical Market Growth (2020-2025) |

6.9% |

Market Dynamics

Market Growth Drivers

Rising Consumer Demand for Non-Invasive Aesthetic Procedures

The global cosmetic procedures market is experiencing unprecedented growth, with approximately 70% of consumers actively considering cosmetic treatments according to the 2025 ASDS Consumer Survey on Cosmetic Dermatologic Procedures. Alexandrite laser systems have emerged as the preferred choice for hair removal applications, benefiting from their proven efficacy at the 755 nanometer wavelength and minimal downtime characteristics. The technology's ability to treat diverse skin tones while maintaining safety standards has broadened its addressable market significantly. Additionally, the integration of advanced cooling systems in modern devices has substantially reduced patient discomfort, leading to improved treatment completion rates and higher patient satisfaction levels exceeding 90% across dermatology practices globally.

Technological Advancements and Innovation Ecosystems

Continuous innovation in laser technology represents a fundamental market driver, with manufacturers investing substantially in research and development initiatives. Recent breakthroughs include the integration of AI and automation into Alexandrite laser systems, enabling real-time optimization of treatment parameters based on individual skin type, lesion characteristics, and patient history. Multi-wavelength platforms combining 755 nm Alexandrite with 1064 nm Nd:YAG radiation have expanded clinical applications beyond hair removal to include vascular lesions, pigmented lesions, and complex dermatological conditions. Manufacturers like Candela Corporation, Lumenis Ltd., and Alma Lasers Ltd. have demonstrated commitment to innovation, with recent regulatory approvals confirming the safety and efficacy of next-generation systems. These technological advances have created a competitive differentiation landscape where practitioners increasingly demand sophisticated, multi-functional platforms that can address multiple patient concerns within single integrated systems.

Market Restraints

High Equipment Acquisition and Maintenance Costs

The substantial capital investment required for acquiring Alexandrite laser systems represents a significant market restraint, particularly in developing regions and smaller aesthetic clinics. Entry-level systems typically require capital expenditures ranging from $80,000 to $200,000, while advanced multi-wavelength platforms can exceed $400,000 in acquisition costs. Beyond initial purchase expenses, ongoing operational expenses including maintenance contracts, spare parts, consumables, and annual calibration requirements accumulate substantially over device lifecycles. These financial barriers have created a tiered market structure where only well-established practices and institutional buyers can maintain diverse laser portfolios. Smaller practitioners and emerging markets face consolidation pressures, potentially limiting market fragmentation and innovation diversity across geographic regions.

Market Opportunities

Explosive Growth in Tattoo Removal Applications

Tattoo removal represents one of the fastest-growing segments within the Alexandrite laser market, with significantly higher growth rates compared to traditional hair removal applications. The 755 nm wavelength of Alexandrite lasers demonstrates superior efficacy specifically for removing blue and green tattoo pigments, colors that represent approximately 40-50% of professional tattoo ink compositions. Contemporary tattoo removal procedures now achieve greater than 95% pigment removal within 8-9 treatment sessions, substantially improving over historical outcomes achieved with earlier laser generations. The global tattoo removal market is projected to experience double-digit CAGR growth driven by increasing social acceptance of tattoo modification, advancing career requirements, and lifestyle changes. Market participants can capitalize on this opportunity through strategic positioning in the tattoo removal vertical, specialized staff training, and targeted marketing initiatives emphasizing clinical efficacy and aesthetic outcomes.

Rapid Healthcare Infrastructure Expansion in Emerging Markets

Asia Pacific markets, particularly China, India, and ASEAN nations, present compelling growth opportunities driven by rapidly expanding healthcare infrastructure and rising disposable incomes. China demonstrates 10.2% annual laser sector growth reflecting both public hospital upgrades and accelerating consumer demand for aesthetic procedures. India's healthcare sector expansion, combined with the country's substantial medical tourism industry, is creating incremental demand for advanced dermatological equipment and services. ASEAN nations, including Thailand, Vietnam, and Philippines are attracting international medical tourism, driving investment in premium aesthetic facilities requiring state-of-the-art Alexandrite laser systems. Manufacturers can leverage emerging market opportunities through partnerships with regional distributors, localized pricing strategies, and capacity-building initiatives supporting professional training in underserved geographic regions. The region's projected 14.3% CAGR in medical laser adoption through 2033 positions Asia Pacific as the fastest-growing geographic market segment.

Category-wise Insights

Product Analysis

Fixed Spot Size Lasers currently maintain dominance within the Alexandrite laser product category, commanding approximately 64% market share in 2025. These systems deliver consistent energy distribution through standardized spot sizes, providing predictable treatment outcomes and simplified operator training requirements. Fixed spot size configurations enable precise control over treatment depth and energy absorption patterns, making them particularly suitable for standardized clinical protocols in hospitals and specialty clinics. The segment's leadership reflects the established clinical evidence supporting fixed-wavelength systems and their proven safety profile across diverse patient populations. However, the segment faces competitive pressure from emerging variable spot size technologies that offer enhanced flexibility and customization capabilities for treating complex anatomical areas.

Indication Analysis

Hair Removal has established itself as the dominant indication segment, capturing 36% market share in 2025 and representing the most significant revenue generator for market participants. The indication's market leadership reflects the substantial consumer preference for non-invasive hair removal solutions compared to traditional methods like waxing, threading, and chemical depilation. Alexandrite lasers at 755 nanometers represent the optimal wavelength for hair removal applications, offering superior melanin absorption and deeper tissue penetration while minimizing epidermal damage. The segment benefits from strong clinical evidence demonstrating permanent hair reduction through selective targeting of melanin-containing hair follicles, creating durable competitive advantages for Alexandrite technology versus alternative laser platforms. Healthcare professional endorsements from the American Society for Dermatologic Surgery and patient satisfaction rates exceeding 90% continue to drive sustained demand across all geographic markets.

End User Analysis

Hospitals represent the leading end-user segment for Alexandrite laser systems, capturing the largest market share in 2025. Hospital settings provide institutional frameworks supporting complex patient management, qualified medical supervision, and comprehensive treatment protocols aligned with regulatory requirements. The institutional buyer segment demonstrates elevated purchasing power and commitment to capital equipment investments, driving sustained device replacement cycles and technology upgrades. Hospital-based dermatology departments benefit from cross-functional collaborations with other specialties, enabling diversified treatment applications beyond standalone aesthetic uses. The segment's leadership reflects hospitals' positioning as primary treatment destinations for complex dermatological conditions, particularly those requiring physician-level supervision and integrated post-operative care protocols unavailable in standalone aesthetic clinics.

Regional Insights

North America Alexandrite Laser Treatment Market Trends and Insights

North America dominates the global Alexandrite laser market, commanding 39% market share in 2025 and generating the highest absolute market revenues globally. The region's market leadership reflects the presence of premium healthcare infrastructure, elevated consumer spending on aesthetic procedures, and advanced innovation ecosystems concentrated primarily in the United States. The U.S. market demonstrates particular strength driven by established aesthetic medicine practices, board-certified dermatologists, and medical spas competing vigorously for market share through service differentiation and technology investments.

Physician involvement in laser procedures remains substantially higher in North America compared to other regions, with 60% of procedures performed by board-certified dermatologists according to 2024 ASDS practice surveys. The region demonstrates the most stringent regulatory compliance requirements through FDA approval processes and 21 CFR Part 878 device classifications, ensuring advanced safety standards and clinical efficacy validation. Recent market developments include Ideal Image's April 2025 deployment of Candela's GentleMax Pro Plus featuring dual-wavelength technology promising faster treatment times and enhanced patient comfort. The region's maturity creates opportunities for premium positioning and advanced feature differentiation, while competitive saturation in major metropolitan markets pressures pricing and service margins.

Asia Pacific Alexandrite Laser Treatment Market Trends and Insights

Asia Pacific represents the fastest-growing geographic region, with projected growth CAGR of 14.3% substantially exceeding global market growth rates through 2033. The region's expansion reflects demographic shifts toward aging populations, rising disposable incomes, and accelerating healthcare infrastructure development across China, Japan, India, and ASEAN nations. China demonstrates particularly robust growth momentum with 10.2% annual laser sector expansion driven by government-sponsored hospital modernization initiatives and surging consumer demand for aesthetic services among affluent middle-class populations.

India's medical tourism ecosystem, combined with expanding domestic aesthetic medicine markets, creates incremental demand for advanced dermatological equipment including Alexandrite laser systems. The country's healthcare sector growth and professional training expansion support the emergence of specialized aesthetic clinics equipped with premium laser technologies. ASEAN nations including Thailand and Philippines leverage medical tourism advantages to attract international patients, requiring investment in advanced treatment technologies and international-standard facilities. Manufacturing advantages in the region, including lower labor costs and established medical device supply chains, support potential localization of device production and service infrastructure. However, regulatory fragmentation and infrastructure inconsistencies across regional markets require customized market entry strategies and partnerships with local distributors.

Competitive Landscape

The competitive landscape of the Alexandrite Laser Treatment market is moderately concentrated, with a handful of established players holding most of the global share through broad portfolios and strong clinic partnerships. Competition focuses on technological innovation, clinical support services, geographic reach, and after-sales networks rather than solely on price. Companies vie to offer advanced, multi-application systems that improve treatment precision and safety, while regional and emerging vendors seek niche opportunities with cost-effective or specialized solutions.

Key Market Developments

- In April 2025, Lumenis Be. Ltd., a leading energy-based medical device company, unveiled the latest edition of its dual-wavelength laser hair removal solution, SPLENDOR X™. The new edition built upon the proven benefits of BLEND X® and patented square-fiber technologies, while incorporating a redesigned, user-centric interface and enhanced digital capabilities.

Companies Covered in Alexandrite Laser Treatment Market

- Candela Corporation

- Cynosure Inc.

- Lumenis Ltd.

- Alma Lasers Ltd.

- Quanta System S.p.A.

- Asclepion Laser Technologies GmbH

- Fotona d.o.o.

- Cutera Inc.

- Syneron Medical Ltd.

- Sciton Inc.

- Solta Medical Inc.

- Venus Concept Ltd.

Frequently Asked Questions

The global Alexandrite Laser Treatment Market is expected to reach US$ 194.3 million in 2026.

The market is fundamentally driven by escalating consumer demand for non-invasive aesthetic procedures, with approximately 70% of consumers actively considering cosmetic treatments according to recent ASDS surveys.

North America dominates the global market with 39% market share in 2025, driven by premium healthcare infrastructure, elevated consumer spending on aesthetic procedures, and established innovation ecosystems concentrated primarily in the United States.

Tattoo removal represents the most compelling market opportunity, emerging as the fastest-growing indication segment with projected double-digit CAGR substantially exceeding hair removal growth rates.

Candela Corporation, Cynosure Inc., Lumenis Ltd., Alma Lasers Ltd., etc.