- Medical Devices

- Airway Catheters Market

Airway Catheters Market Size, Share, and Growth Forecast, 2025 - 2032

Airway Catheters Market By Product (Endotracheal Catheters, Tracheostomy Catheters, Nasopharyngeal Catheters, Oropharyngeal Catheters, Suction Catheters), Material, Usage, by End-user, and Regional Analysis from 2025 - 2032

Airway Catheters Market Size and Trends Analysis

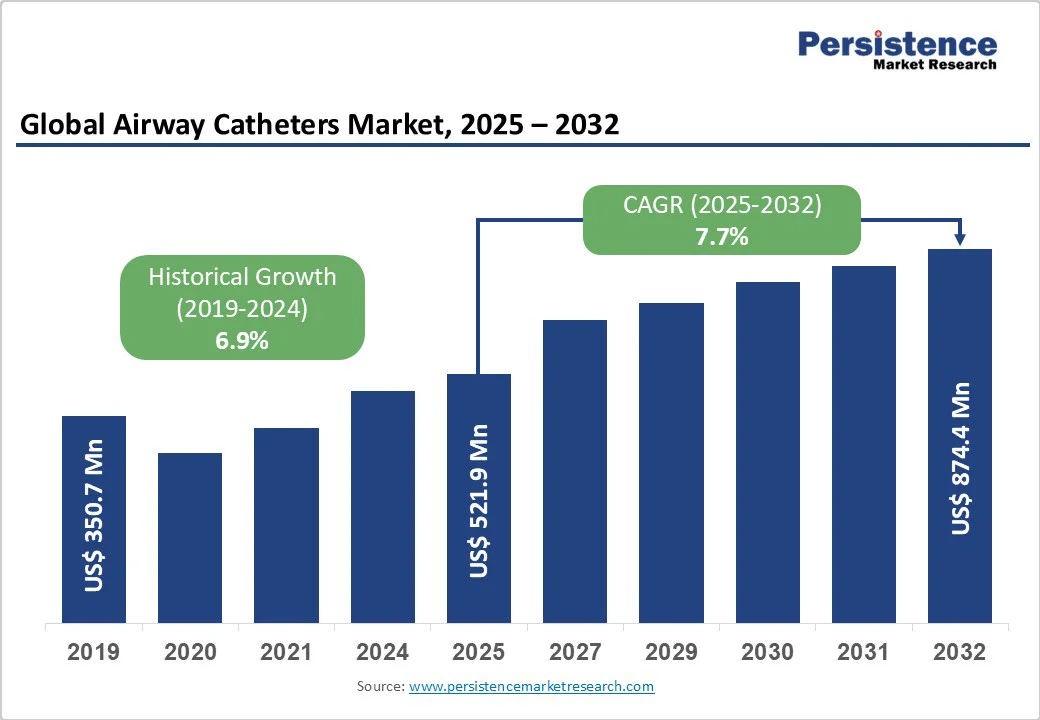

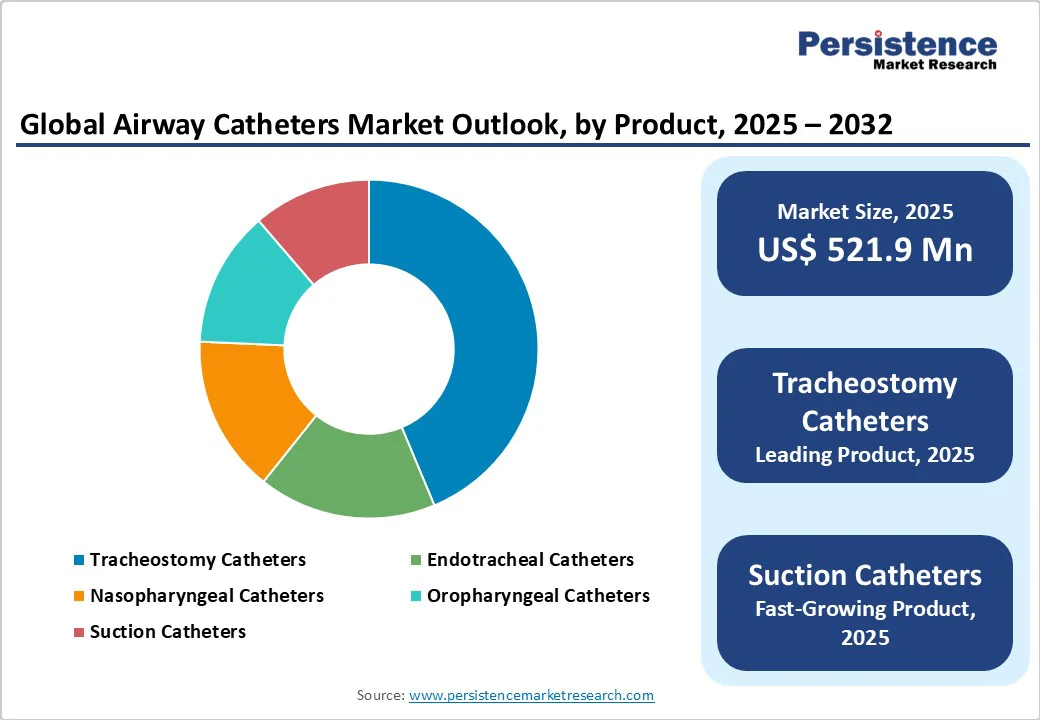

The global airway catheters market size is likely to be valued at US$521.9 Million in 2025. It is expected to reach US$874.4 Million by 2032, growing at a CAGR of 7.7% during the forecast period from 2025 to 2032, driven by increasing demand in hospitals, surgical centers, and intensive care units for procedures requiring effective airway management. The rising awareness of hospital-acquired infections (HAIs), patient safety, and ventilation efficiency is fueling the adoption of advanced airway catheters.

Key Industry Highlights

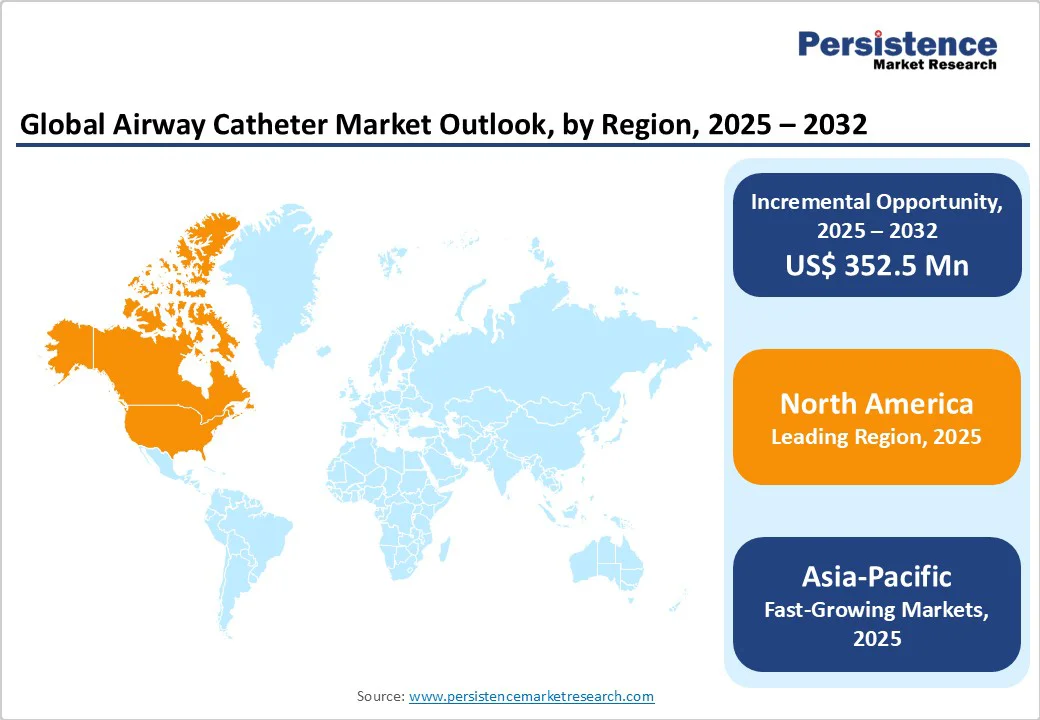

- Leading Region: North America leads globally with 35.5% of the market share, supported by advanced healthcare infrastructure, high ICU and surgical volumes, and the presence of major medical device manufacturers.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region, driven by expanding healthcare facilities, rising awareness of infection prevention, and increasing investments in critical care and surgical procedures.

- Leading Product Category: Tracheostomy catheters dominate the market with a 43.7% market share, due to their role in long-term airway management and the reduced risk of laryngeal injury during prolonged ventilation.

- Fastest-Growing Product Category: Suction catheters are gaining traction, driven by the need for efficient airway clearance in ventilated patients and innovations that reduce infection risk and improve patient safety.

- Leading Material Segment: Polyvinyl chloride (PVC) catheters lead the market, favored for flexibility, biocompatibility, and cost-effectiveness.

- Fastest-Growing Material Segment: Silicone and advanced biocompatible polymers are gaining popularity due to their comfort, durability, and reduced tissue irritation.

- ICU care, emergency care, surgical intubation, and home ventilation create strong growth opportunities for market players.

- Investments focus on sensor-enabled, antimicrobial-coated, and single-use catheters to enhance patient safety, reduce infections, and improve clinical efficiency.

| Key Insights | Details |

|---|---|

|

Airway Catheters Market Size (2025E) |

US$521.9 Mn |

|

Market Value Forecast (2032F) |

US$874.4 Mn |

|

Projected Growth (CAGR 2025 to 2032) |

7.7% |

|

Historical Market Growth (CAGR 2019 to 2024) |

6.9% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Advancements in Technology and Rising Prevalence of Respiratory Disorders

Technological innovations have enhanced airway catheters with greater flexibility, durability, and biocompatibility. Advanced features such as cuff pressure monitoring, subglottic suction ports, and antimicrobial coatings improve safety, reduce infection risks, and enhance patient comfort. These advancements are driving market growth.

The escalating prevalence of respiratory disorders, including chronic obstructive pulmonary disease (COPD), asthma, and respiratory infections, is a key driver propelling the expansion of the market. With an aging population and the continued adoption of unhealthy lifestyles, the burden of respiratory diseases is on the rise globally. For instance, the Australian Institute of Health and Welfare reported that in 2023, chronic obstructive pulmonary disease (COPD) represented 3.6% of the overall disease burden and accounted for half of the total burden from respiratory conditions.

Patients suffering from these conditions often require airway intervention to maintain adequate oxygenation and ventilation, particularly during exacerbations or critical illness. Consequently, there is a growing demand for airway catheters across various healthcare settings, including hospitals, clinics, and emergency departments.

Regulatory Challenges and Compliance Hurdles

The airway catheters market faces significant challenges due to stringent regulatory requirements and compliance hurdles imposed by regulatory bodies worldwide. The approval process for new airway catheter designs and materials involves rigorous testing and clinical trials to ensure safety, efficacy, and adherence to quality standards. Delays in obtaining regulatory approvals can prolong the time to market for innovative products, hindering market growth and limiting manufacturers' ability to meet evolving healthcare needs promptly.

Frequent changes in regulatory guidelines and compliance standards add complexity and uncertainty to the product development and commercialization process, increasing costs and resource requirements for companies operating in the market. As a result, many manufacturers may face difficulties navigating the regulatory landscape, leading to delays in product launches and market entry.

Expansion of Home Healthcare Services and Growing Adoption of Single-Use and Antimicrobial Catheters

The expanding scope of home healthcare services presents a significant opportunity for the market to grow and thrive. As healthcare delivery models evolve, there is a growing trend toward providing medical care in the comfort of patients' homes, especially for those with chronic respiratory conditions requiring long-term airway management. Home-based ventilation and airway clearance therapies are becoming increasingly prevalent, boosted by factors such as the desire for patient-centered care and cost-effectiveness.

Rising awareness of hospital-acquired infections (HAIs) and stricter infection control regulations are fueling the transition toward single-use and antimicrobial-coated airway catheters. Reusable catheters pose a higher risk of cross-contamination, prompting healthcare facilities to adopt disposable alternatives that ensure sterility and patient safety. The integration of antimicrobial coatings, such as silver ions or chlorhexidine, helps prevent bacterial colonization and biofilm formation. This boosts the use of airway catheters in ICUs, surgical units, and emergency departments, where infection prevention remains a top clinical priority.

Category-wise Analysis

Product Insights

The tracheostomy catheters segment is projected to lead the market with 43.7% in 2025. The segment’s strong performance is primarily driven by its role in long-term airway management for patients requiring extended mechanical ventilation or experiencing chronic respiratory failure due to conditions such as COPD, neuromuscular disorders, or severe trauma.

Tracheostomy catheters offer a more stable and comfortable airway compared to endotracheal tubes, reducing the risk of vocal cord damage, ventilator-associated pneumonia (VAP), and other airway complications. Technological advancements such as cuffed, fenestrated, and antimicrobial-coated tracheostomy tubes are improving patient safety and infection control outcomes.

Material Insights

The polyvinyl chloride (PVC) segment is expected to dominate the market in 2025, with a revenue share of 57.4%. The widespread adoption of PVC catheters is primarily due to the material’s cost-effectiveness, flexibility, and excellent biocompatibility, which make it suitable for a diverse range of clinical applications across critical care, surgical, and emergency settings. PVC’s versatility allows manufacturers to produce both single-use and reusable catheters efficiently, meeting the high-volume demands of hospitals, specialty clinics, and ambulatory surgical centers.

PVC can be easily modified or combined with antimicrobial coatings and other enhancements to reduce infection risks, improve patient safety, and extend device usability. These properties, coupled with its ability to maintain structural integrity under mechanical stress, make PVC the material of choice for healthcare providers.

Usage Insights

The disposable catheters segment is projected to hold 63.1% of the market share in 2025. This is due to the rising awareness of hospital-acquired infections (HAIs) and the implementation of strict infection control protocols across healthcare settings. Disposable catheters help minimize the risk of cross-contamination between patients, making them the preferred choice in critical care environments such as intensive care units (ICUs), operating rooms, emergency departments, and surgical units.

Single-use catheters offer advantages in terms of convenience, time efficiency, and regulatory compliance, as they eliminate the need for sterilization procedures and reduce the burden on hospital staff. The increasing adoption of antimicrobial coatings, sensor-enabled monitoring, and advanced ergonomic designs in single-use devices further enhances patient safety and procedural efficiency.

End-user Insights

The hospitals segment is projected to hold 55.8% of the market share in 2025. Hospitals represent the primary setting for airway catheter usage due to high patient volumes, complex surgical procedures, and extensive intensive care unit (ICU) requirements, all of which demand reliable airway management solutions such as airway catheters. The adoption of advanced technologies, including antimicrobial-coated, single-use, and sensor-enabled catheters, is particularly prominent in hospital settings, as these devices help reduce the risk of hospital-acquired infections (HAIs) and enhance patient safety.

Hospitals are increasingly investing in state-of-the-art critical care infrastructure and operating room technologies, further driving the demand for airway catheters that offer precise monitoring and improved procedural efficiency.

Regional Insights

North America Airway Catheters Market Trends

The North American market is expected to dominate globally with a value share of 35.5% in 2025, with the U.S. leading the region. This dominance is due to several factors, such as high prevalence of respiratory disorders, well-established healthcare infrastructure, and widespread adoption of advanced airway management technologies. For instance, according to the American Lung Association, over 25 million people in the U.S. are living with asthma, of which around 5 to 10% experience severe forms that require intensive airway management and hospitalization. Chronic obstructive pulmonary disease (COPD) also represents a major contributor to the country’s respiratory health burden.

The region also benefits from the strong presence of leading medical device manufacturers, which drives continuous innovation in airway catheter design, such as sensor-integrated, antimicrobial-coated, and single-use catheters. There is a growing demand for minimally invasive devices that enhance patient safety and reduce the risk of ventilator-associated infections.

Europe Airway Catheters Market Trends

The European market is projected to experience steady growth, supported by advancements in healthcare infrastructure and the increasing adoption of innovative airway management technologies. Growing awareness of hospital-acquired infections (HAIs) is driving demand for single-use and antimicrobial-coated catheters, particularly in ICUs, surgical units, and emergency care settings, where airway catheters are frequently used for intubation and ventilation.

Contaminated or reused airway catheters can serve as potential sources of infection, making infection-resistant and disposable options essential for patient safety. For instance, according to the European Center for Disease Prevention and Control (ECDC), around 4.3 million patients in hospitals across Europe acquire at least one healthcare-associated infection (HAI) each year during their hospital stay. Favorable government initiatives and healthcare policies are also promoting the modernization of critical care facilities and encouraging investment in advanced medical devices.

Asia and Pacific Airway Catheters Market Trends

The Asia Pacific market is expected to register a relatively higher CAGR of around 10.0% between 2025 and 2032, driven by the growing prevalence of respiratory disorders, increasing demand for advanced airway management devices, and expanding healthcare infrastructure across the region. Rapid urbanization, rising awareness of infection control, and an increasing number of hospitals and critical care units are fueling the adoption of single-use, antimicrobial, and technologically advanced catheters.

Countries such as India, China, and Japan are benefiting from growing government initiatives supporting the MedTech industry, which are enhancing manufacturing capabilities and facilitating the adoption of advanced medical devices such as airway catheters. For example, in May 2025, Invest India reported that the Indian MedTech market has been growing steadily at around 15% annually over the past three years and is projected to capture 10–12% of the global market share within the next 25 years, highlighting the region’s significant growth potential. Ongoing investments by governments and private players in healthcare modernization, coupled with the presence of emerging medical device manufacturers, are further supporting market expansion.

Competitive Landscape

The global airway catheters market is highly competitive, with major players such as Medtronic, Teleflex Incorporated, Convatec, and Cook dominating the market through a combination of product innovation, strategic partnerships, mergers and acquisitions, and geographic expansion.

These companies are continuously investing in research and development to introduce technologically advanced catheters, including sensor-enabled, antimicrobial-coated, and single-use devices, to enhance patient safety and procedural efficiency. They also leverage strong distribution networks and regulatory expertise to maintain market leadership and expand their presence in emerging regions, thereby strengthening their competitive position globally.

Key Industry Developments

- In January 2025, Ambu announced the launch of its new video laryngoscopy solution Ambu SureSight Connect, which is fully integrated with the company’s advanced digital visualization systems, Ambu aView 2 Advance and Ambu aBox 2. This next-generation solution is designed to enable efficient and precise intubation in both routine and difficult airway procedures across operating rooms (ORs) and intensive care units (ICUs).

- In November 2024, Asahi Kasei Medical Co., Ltd. launched TrachFlush in Japan, an endotracheal tube cuff inflator developed by AW Technologies Aps. The device automatically inflates and deflates the tube cuff to prevent secretion buildup and reduce ventilator-associated pneumonia (VAP), enhancing airway hygiene and patient safety during mechanical ventilation.

Companies Covered in Airway Catheters Market

- Medtronic

- Teleflex Incorporated

- Convatec

- Cook

- Boston Scientific Corporation

- BD

- Intersurgical Ltd.

- Suzhou Sunmed Co., Ltd.

- ICU Medical, Inc.

- ANGIPLAST PRIVATE LIMITED

- Sterimed Group

- Ivor Shaw T/A Pennine Healthcare

- Medilivescare Manufacturing Pvt. Ltd.

- Narang Medical Limited

- VBM Medizintechnik GmbH

- Ambu A/S

Frequently Asked Questions

The airway catheters market is projected to be valued at US$521.9 Million in 2025.

The rising prevalence of respiratory diseases and increasing demand for advanced airway management solutions are driving market growth.

The airway catheters market is poised to witness a CAGR of 7.7% between 2025 and 2032.

Development of smart, sensor-enabled, and antimicrobial catheters and the growing adoption of single-use devices are creating significant opportunities.

Medtronic, Teleflex Incorporated, Convatec, Cook, and Boston Scientific Corporation are the key players in the airway catheters market.