- Non-food Packaging

- Aerosol Cans Market

Aerosol Cans Market Size, Share, and Growth Forecast, 2026 - 2033

Aerosol Cans Market By Material (Aluminum, Steel, Others), Product Type (One-Piece, Straight-Wall, Others), Propellant, Application, and Regional Analysis for 2026 - 2033

Aerosol Cans Market Size and Trends Analysis

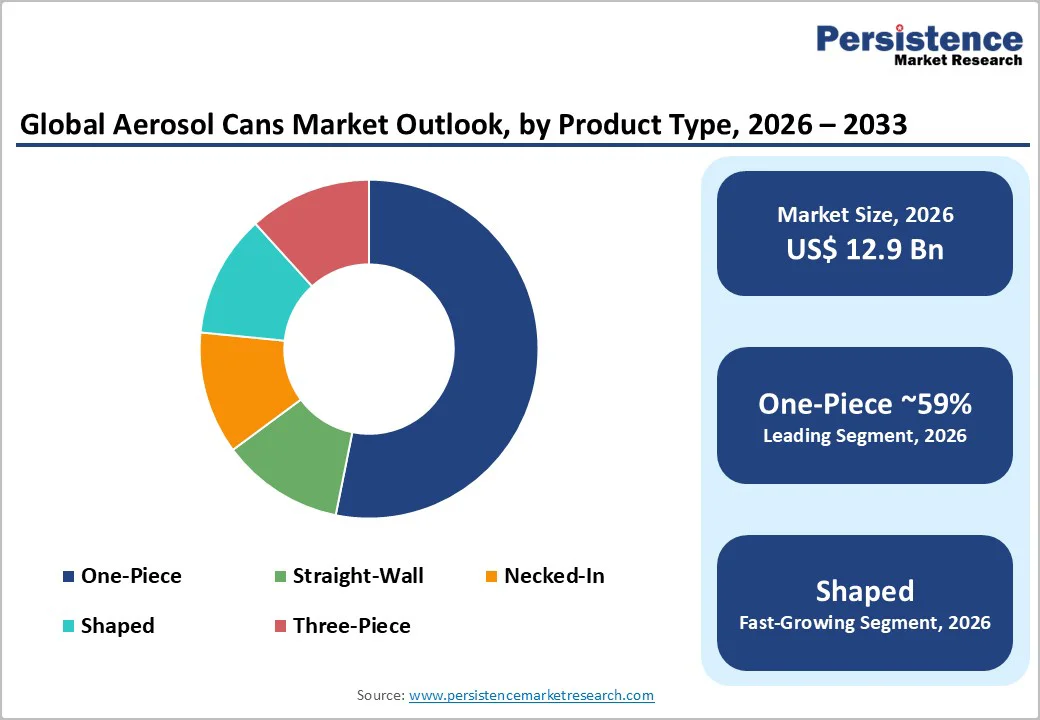

The global aerosol cans market size is likely to be valued at US$12.9 billion in 2026 and is expected to reach US$16.4 billion by 2033, growing at a CAGR of 3.5% during the forecast period from 2026 to 2033, driven by the rising demand in personal-care and household categories, and ongoing innovation in low-VOC propellants and valve technologies.

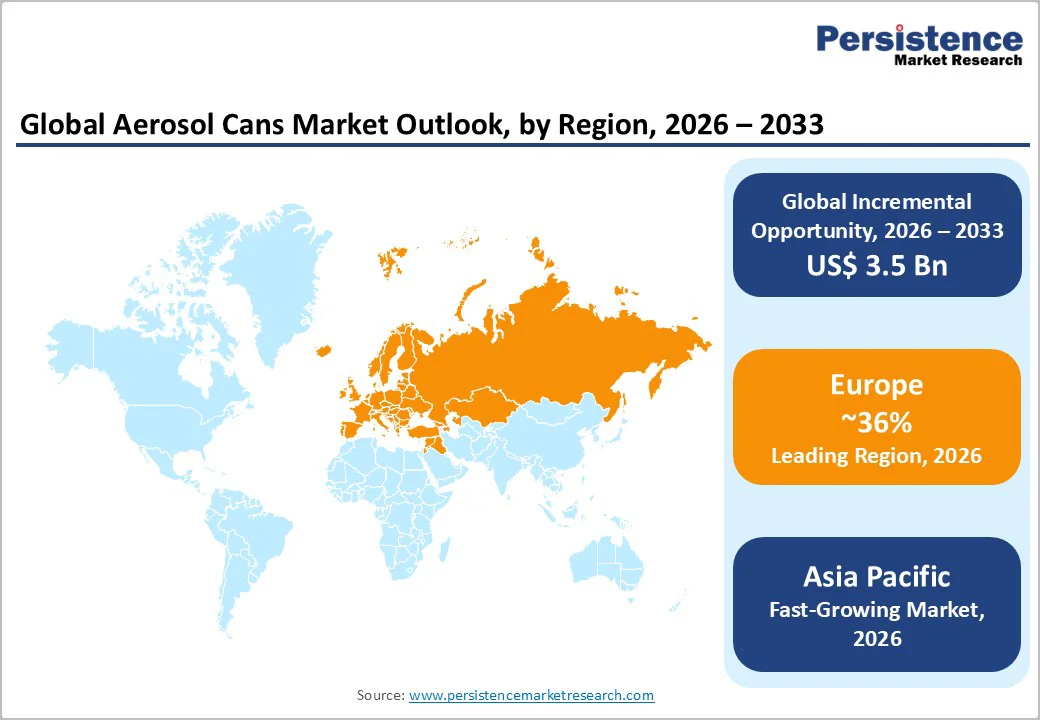

Europe maintains a mature, regulation-led structure, while Asia Pacific posts the fastest growth, supported by manufacturing scale and increasing consumption. Commercial trends include consolidation among metal-packaging suppliers and investments in lightweight and recycled-aluminum technologies.

Key Industry Highlights

- Leading Region: Europe is expected to account for about 36% of the global aluminum pigment demand in 2026, owing to its strong FMCG industry, recycling systems, and widespread use of aluminum aerosol cans.

- Fastest-growing Region: Asia Pacific, driven by rising personal care consumption in China, India, and Southeast Asia, along with large-scale regional manufacturing investments.

- Investment Plans: Major producers are investing in aluminum extrusion capacity, high-recycled-content material integration, and flexible shaping/printing technologies, with multiple global players allocating US$300-500 million annually toward sustainability, modernization, and automation upgrades.

- Leading Application: Personal care is the leading segment with an estimated 50% share of global aerosol can consumption, supported by high-volume demand for deodorants, antiperspirants, hair sprays, body mists, and styling mousses.

- Leading Product Type: One-piece cans, accounting for roughly 59% of global product-format demand due to their compatibility with high-speed filling lines, durability, and premium decoration capabilities.

| Key Insights | Details |

|---|---|

| Market Size (2026E) | US$12.9 Bn |

| Market Value Forecast (2033F) | US$16.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 3.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.9% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Sustainability and Circularity Requirements to Increase Demand for Aluminum

Sustainability mandates across global markets are accelerating the shift toward aluminum aerosol cans due to their infinite recyclability, lighter weight, and strong environmental credentials. Studies consistently highlight aluminum as the leading material by share, supported by regulatory frameworks that encourage high recycled content and lower life-cycle emissions.

Manufacturers are expanding recycled-aluminum capacity, lightweight extrusion lines, and closed-loop sourcing programs to meet these regulatory expectations and to secure premium contracts with consumer-goods companies. Certified low-carbon aluminum cans are achieving higher price realization, strengthening the commercial case for investment.

These developments reinforce aluminum’s position as both the dominant and most strategically favored material type in the aerosol packaging ecosystem.

Rising Demand from Personal Care, Household, and Healthcare Industries

Personal care remains the single largest end-use category for aerosol cans globally, led by deodorants, hair styling products, and cosmetic sprays. The format’s precise dosing, portability, and hygiene advantages help sustain consistent demand. Household products such as air fresheners, disinfectants, cleaners, and insecticides contribute stable volume even when discretionary categories fluctuate.

Healthcare applications, especially topical sprays, antiseptics, and delivery devices, offer counter-cyclical demand and reinforce long-term market resilience. Multiple analyses project mid-single-digit growth across personal care, household, and healthcare segments between 2025 and 2033.

Manufacturers that can ensure valve compatibility, propellant safety, and secure filling capacity continue to benefit from deep partnerships with brand owners in these categories.

Advances in Propellants, Valves, and Coatings

Technological advancements in aerosol formulation and hardware are driving value growth across premium and regulated applications. Low-VOC propellants, reduced-leakage valve systems, and enhanced internal coatings support safety compliance and improve product performance. These innovations allow brand owners to meet evolving environmental standards while maintaining or improving efficacy and shelf life.

High-speed automation and next-generation filling systems also raise throughput for producers, reducing operational costs over time. The integration of coating technologies that support vivid printing without hindering recyclability allows manufacturers to serve premium cosmetic and personal-care brands. Collectively, these innovations expand the addressable market, particularly in medical aerosols and specialty applications.

Barrier Analysis - Stricter VOC and Propellant Regulations

Tightening regulations governing volatile organic compounds, propellant blends, and air quality create operational and compliance challenges for aerosol manufacturers. Reformulation to compliant propellants can increase material costs and extend product-development timelines due to testing and validation requirements.

Regulatory transitions in regions such as Europe add low-single-digit percentage points to per-unit costs for certain SKUs, compressing margins in commodity segments. These pressures can also delay product launches until reformulations pass certification, slowing rollout across highly regulated markets.

Raw-Material Volatility and Supply Chain Concentration

Aluminum, steel, and propellant feedstocks such as hydrocarbons and DME remain exposed to energy price fluctuations and regional supply disruptions. Aerosol can manufacturing relies on a concentrated supplier base for specialized components like valves and high-grade metal coils, resulting in periodic bottlenecks.

When capacity is tight, lead times extend, and spot prices rise for urgent orders. During historical volatility cycles, producers experienced short-term margin pressure and sometimes lost production days due to mismatched supply, increasing reliance on inventory buffers, and contingency sourcing.

Opportunity Analysis - Lightweight and 100% Recycled-Aluminum Cans

Companies that scale ultra-light and 100% recycled-content aluminum aerosol cans are positioned to capture accelerated growth tied to corporate sustainability commitments. Newer production technologies enable reduced-gauge metal usage without compromising structural integrity.

Market potential is substantial: if premium personal-care brands raise adoption of recycled-aluminum formats by 10-15%, the incremental opportunity could reach several hundred million dollars globally by 2030. Realizing this requires investment in scrap recovery, traceable chain-of-custody systems, and advanced extrusion technologies that support consistent quality and regulatory compliance.

Growth through Localization in Emerging Markets

Asia Pacific, particularly China, India, and Southeast Asia, presents strong opportunities through localized production and joint-venture expansion. Rising middle-class consumption of personal-care products drives steady volume increases, while proximity to customers reduces shipping costs and enhances service reliability.

Success depends on competitive labor structures, access to recycled feedstock, and the ability to align with evolving regional regulatory standards for propellant safety and VOC limits.

Category-wise Analysis

Application Insights

Personal care is expected to be the largest and most influential segment with an estimated 50% of market share in 2026. High-volume products such as deodorants, antiperspirants, hair sprays, mousse formulations, and body mists rely heavily on aerosol dispensing for precision application and consumer convenience.

Global brands such as Unilever, L’Oreal, and Procter & Gamble maintain extensive aerosol portfolios, supported by innovations in natural propellants, low-VOC formulations, and decorative aluminum finishes that elevate shelf appeal.

Growth is also linked to rising grooming awareness in emerging economies and the premiumization trend in cosmetics. Demand remains stable across both mass-market and professional salon channels, strengthening personal care’s position as the leading revenue-contributing segment.

Healthcare aerosols are anticipated to expand rapidly in 2026, driven by growing consumer and institutional adoption of topical anesthetics, antiseptic sprays, wound-care formulations, and metered-dose pharmaceutical devices.

Demographic factors such as aging populations, rising chronic skin conditions, and greater emphasis on at-home care support this momentum. Innovations in barrier-pack technology and sterile filling lines are enabling wider use of aerosols for pain-relief sprays, dermatology treatments, and inhalation-support products.

Companies such as AptarGroup and LINDAL Group are investing in precision valve systems tailored for medical applications. Healthcare’s stringent quality requirements also accelerate the shift toward aluminum and hybrid materials due to their compliance with safety and sterility standards, positioning this segment as the fastest-growing within the industry.

Product Type Insights

One-piece cans are anticipated to remain the leading product type, estimated to hold 59% of market share in 2026, due to their ability to withstand higher internal pressures, uniform wall construction, and compatibility with high-speed continuous extrusion lines. These cans are widely preferred in personal care, cosmetics, and premium household aerosols, where consistent spray quality, durability, and superior decoration options are essential.

Global manufacturers such as Ball Corporation, CCL Container, and Tubex promote their one-piece and necked-in formats as central to their performance and sustainability portfolios.

The seamless construction offers advantages in lightweighting, advanced shaping, and decorative printing, making one-piece cans the flagship choice for deodorants, hair sprays, and body mists. Their operational efficiency in filling plants and strong recyclability profile further reinforce their position as the dominant product type in high-volume consumer categories.

Shaped cans are anticipated to witness the fastest growth, due to rising demand for brand differentiation, premium aesthetics, and limited-edition promotional packaging. These formats allow brands to create unique profiles, oval, contoured, ergonomic, or sculpted shapes that visually distinguish products on shelves. Premium fragrance body sprays, seasonal launches, and luxury cosmetic aerosols increasingly use shaped cans to elevate brand identity.

Companies such as LINDAL Group, Crown Holdings, and Trivium Packaging have expanded investments in flexible forming technologies, digital printing, and short-run customization, enabling specialty formats without compromising recyclability.

Shaped cans also appeal to marketing teams seeking enhanced tactile features, embossing, and metallized finishes. Growth is supported by advancements in tooling systems and quick-change manufacturing setups that reduce downtime and cost barriers, making specialty designs more accessible to mid-size brands and private-label producers.

Regional Insights

North America Aerosol Cans Market Trends - Premium Personal-Care Demand, Recycling Expansion, and Low-VOC Packaging Innovation

North America remains a high-value market for aerosol cans, driven by strong per-capita consumption of personal-care and household products and supported by a well-established packaging ecosystem. While Europe leads in global market value, North America follows closely due to its extensive manufacturing capacity, particularly in the U.S., where multiple aluminum extrusion lines, component plants, and advanced filling facilities form a mature supply chain.

Brands increasingly rely on domestic and near-shore suppliers to ensure consistency, reduce logistics costs, and meet regulatory requirements shaped by federal and state air-quality standards.

These regulations influence propellant use and formulation strategies, benefiting suppliers that offer low-VOC-compliant systems. Market growth is reinforced by rising premiumization in personal-care aerosols, strong sustainability commitments calling for higher recycled-aluminum content, and expanding demand for topical healthcare aerosols.

Manufacturers are upgrading coating, printing, and valve technologies while investing in automation and recycling infrastructure. Ongoing capacity rationalization, targeted expansions, and strategic acquisitions continue to reshape the competitive landscape.

Sustainability-led improvements, such as increased use of recycled aluminum, advanced decoration technologies, and energy-efficient filling operations, are becoming central to maintaining long-term competitiveness in the North American aerosol can market.

Europe Aerosol Cans Market Trends - Regulation-Driven Circular Packaging Leadership and Premium Aesthetic Manufacturing

Europe is anticipated to lead the global aerosol cans market, accounting for 36% of the market share in 2026, due to stringent environmental regulations, mature consumption patterns, and high demand for premium personal-care aerosols.

Per-unit prices tend to be higher than in other regions due to detailed finishing requirements and strong consumer expectations for aesthetic quality. European production centers benefit from efficient recycling systems, which improve aluminum sourcing and reduce supply risk. Germany, the U.K., France, and Spain represent key markets.

Germany and the U.K. host considerable automotive and industrial aerosol production, while France and Spain anchor premium personal-care and cosmetic packaging. These countries maintain strong regulatory alignment under EU packaging and emissions directives. Recyclability, verified recycled content, and VOC compliance are major considerations shaping design and production decisions.

Growth in Europe is driven by regulatory pressure for circular packaging, increasing adoption of recycled aluminum, and brands’ willingness to invest in premium packaging for competitive differentiation. Manufacturers gain an advantage when they can document low-carbon material sourcing and provide decorative finishes that satisfy both brand and regulatory expectations.

Compliance investments can be costly but offer significant differentiation benefits. Investment trends point toward expanded aluminum-extrusion capacity, improvements in energy efficiency, and rapid adoption of next-generation coatings and low-VOC technologies. Recent developments across the region include facility upgrades focused on recycled aluminum, carbon-reduction roadmaps, and modernization of high-speed production lines.

Asia Pacific Aerosol Cans Market Trends - Fast-Growth Consumer Expansion, Manufacturing Scale-Up, and Emerging Sustainability Adoption

Asia Pacific is likely to be the world’s fastest-growing aerosol cans market in 2026, due to rapid urbanization, expanding middle-class consumption, and rising penetration of personal-care products. China is the largest market in the region with strong domestic manufacturing and a growing consumer base for cosmetics and household aerosols. Japan maintains a high-value segment focused on technical and medical aerosols requiring stringent process controls.

India and Southeast Asia present major growth opportunities as retail penetration accelerates and personal-care consumption rises. Local and global manufacturers increasingly establish greenfield plants and joint ventures to serve domestic brands more effectively.

The region’s manufacturing strengths, cost competitiveness, growing technical capabilities, and proximity to major consumer markets contribute to ongoing capacity expansion. Key growth drivers include rising disposable incomes, expanding distribution networks, and the increasing popularity of aerosol-based beauty and hygiene products.

E-commerce growth enables niche brands to introduce aerosol SKUs, further diversifying demand. In parallel, adoption of premium packaging, specialty finishes, and sustainable materials is gaining traction as regional consumers adopt global beauty standards. Regulatory frameworks in Asia Pacific vary widely.

Some markets are strengthening VOC and propellant rules, while others maintain more flexible standards. This creates staggered demand for low-VOC technologies and presents opportunities for suppliers that can move early in markets expected to tighten regulations. Recycling infrastructure across the region is uneven, influencing the pace at which recycled aluminum can be integrated into supply chains.

Competitive Landscape

The global aerosol cans market is characterized by a blend of large integrated manufacturers and regional converters. Market concentration is moderate: a small group of multinational metal-packaging companies controls substantial global capacity, particularly in aluminum extrusion and advanced decorative finishes.

Numerous regional players support local demand through flexible production and specialty capabilities. Competitive differentiation hinges on sustainability credentials, recycled-content readiness, decoration technologies, geographic footprint, and validated low-VOC systems. Consolidation, targeted acquisitions, and optimization of production footprints continue as companies pursue scale, margin stability, and technological leadership.

Dominant strategies include sustainability leadership through recycled aluminum, expansion into premium decorative finishes, and regional production to reduce freight costs. Technical differentiation through advanced valves, compliant propellants, and validated low-VOC filling systems strengthens supplier positioning across regulated and premium segments.

Key Industry Developments

- In June 2024, Sonoco Products Company (NYSE: SON), a global leader in sustainable packaging, announced an agreement to acquire Eviosys, Europe’s largest manufacturer of food cans, ends, and closures, from KPS Capital Partners for approximately US$3.9 billion.

- In July 2024, Colep Packaging strengthened its position in the aerosol packaging sector by acquiring the remaining 60% stake in ALM, SL, completing full ownership of the Spanish aluminum aerosol manufacturer.

Companies Covered in Aerosol Cans Market

- Ball Corporation

- Crown Holdings

- Trivium Packaging

- CCL Container

- LINDAL Group

- AptarGroup

- Mauser Packaging Solutions

- Ardagh Group

- Colep Packaging

- Shanghai Sunhome Industrial

- Tubex Group

- Exal Corporation

- Bharat Containers

- Perfektup Ambalaj

- Nampak

- Montebello Packaging

- BWAY Corporation

- Euro Asia Packaging

- Alltub Group

- Toyo Seikan Group

Frequently Asked Questions

The global aerosol cans market size is estimated to reach US$12.9 billion in 2026.

By 2033, the aerosol cans market is projected to reach US$16.4 billion.

Major trends include the shift toward high-recycled-content aluminum cans, growth in shaped and specialty formats, expansion of healthcare aerosols, adoption of low-carbon packaging, and investment in advanced printing and decorative finishes.

Aluminum-based one-piece aerosol cans represent the leading segment due to their recyclability, compatibility with high-speed production lines, and strong penetration in personal care and cosmetics.

The aerosol cans market is expected to grow at a CAGR of 3.5% between 2026 and 2033.

Leading companies include Ball Corporation, Crown Holdings, Trivium Packaging, CCL Container, and LINDAL Group.