- Automotive

- Aerial Firefighting Market

Aerial Firefighting Market Size, Share, and Growth Forecast, 2026 - 2033

Aerial Firefighting Market by Platform Type (Fixed-Wing Aircraft, Helicopters, Unmanned Aerial Systems (UAS)/Drones, Hybrid/Optionally-Piloted Aircraft), Service Model (Government-Owned & Operated, Government-Contracted Private Operators, On-Demand/Call-When-Needed (CWN) Leasing, OEM Direct Sales, Software/Subscription-Based), Technology (Delivery Systems, Sensors & Imaging Systems, Mission Planning & Command Software, Autonomy Systems, Communication Systems, Fire Retardant Solutions), and Regional Analysis for 2026 - 2033

Aerial Firefighting Market Share and Trends Analysis

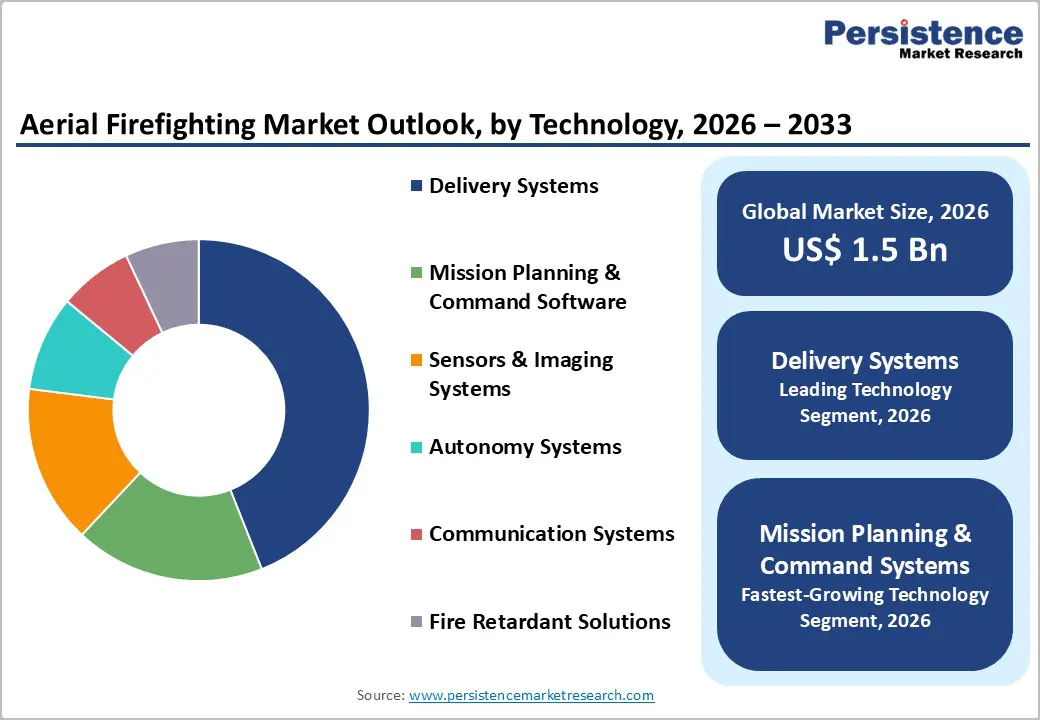

The global aerial firefighting market size is likely to be valued at US$ 1.5 billion in 2026, and is projected to reach US$ 2.4 billion by 2033, growing at a CAGR of 6.9% during the forecast period 2026 - 2033. The market is expanding as wildfire intensity is increasing and suppression budgets are rising across major fire-prone regions. Government data confirm that public expenditure is scaling upward in response to longer and more destructive fire seasons.

The United States Forest Service (USFS) wildfire budget grew from US$ 2.1 billion in 2015 to more than US$ 4.4 billion in 2023, and aviation operations are absorbing a rising proportion of this allocation. Canada, Australia, and Southern European countries are also reporting longer deployment cycles and higher annual fire management outlays. Fire seasons are extending in duration, and agencies are deploying aircraft earlier and retaining them longer. This structural shift is strengthening demand visibility for fixed-wing aircraft, helicopters, and unmanned aerial systems (UAS).

Governments are institutionalizing higher baseline preparedness levels. Fleet recapitalization initiatives are accelerating, and agencies are integrating drones into reconnaissance and thermal mapping missions to improve operational efficiency. Multilateral coordination frameworks such as the European Union (EU) Civil Protection Mechanism (rescEU) are strengthening shared aerial capacity across borders. Capital deployment is therefore shifting from short-term seasonal leasing toward long-term fleet modernization, technology integration, and performance-based aviation contracts.

Key Industry Highlights

- Dominant Platform Type: Fixed-wing aircraft are expected to account for approximately 52% revenue share in 2026, reflecting their critical role in large-area wildfire suppression and higher payload capacity.

- Fastest-growing Platform Type: Unmanned aerial systems (UAS) are projected to expand at the highest CAGR of around 13% during 2026 - 2033, driven by regulatory easing for beyond visual line-of-sight (BVLOS) operations and cost-efficient reconnaissance deployment.

- Dominant Technology: Delivery systems are anticipated to command nearly 44% of the market revenue in 2026, supported by ongoing aircraft conversion programs and modernization of aging aerial fleets.

- Fastest-growing Technology: Mission systems and software platforms are expected to grow at approximately 11% CAGR through 2033, underpinned by increased adoption of real-time fire mapping and predictive modeling.

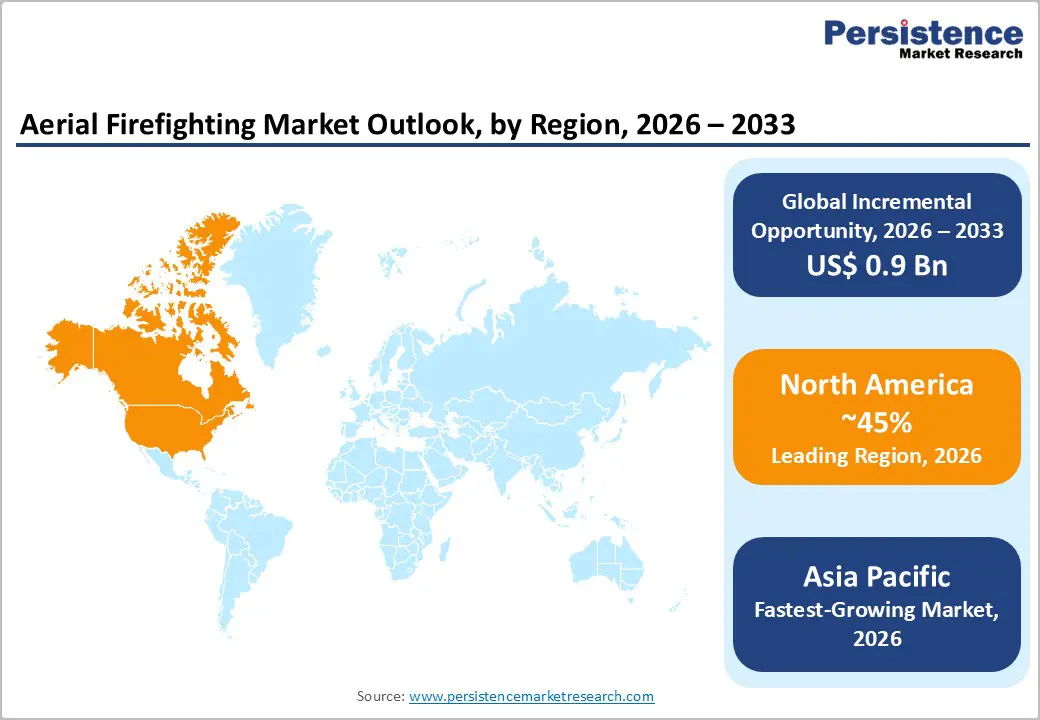

- Regional Leadership: North America is projected to hold roughly 45% market share in 2026, owing to sustained wildfire suppression appropriations and multi-year federal aviation contracts.

- Fastest-growing Market: Asia Pacific is set to register an estimated 2026 - 2033 CAGR of about 8%, supported by rising climate-driven fire exposure and expanding national aerial response budgets.

- December 2025: IMS New Zealand expanded its Cloudburst Fire Bucket distribution in the United States and Canada through a partnership with Boost Human External Cargo Systems to provide local support and inventory to helicopter firefighting operators.

| Key Insights | Details |

|---|---|

| Aerial Firefighting Market Size (2026E) | US$ 1.5 Bn |

| Market Value Forecast (2033F) | US$ 2.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.5% |

Market Factors - Growth, Barriers, Opportunity Analysis

Escalating Wildfire Expenditure and Climate-Induced Fire Intensity

Wildfire activity is intensifying across continents. The Intergovernmental Panel on Climate Change Sixth Assessment Report (IPCC AR6) confirmed that fire weather conditions are becoming more frequent and severe in North America, Southern Europe, and Australia. The U.S. National Interagency Fire Center (NIFC) is reporting that average annual burned acreage in the United States exceeded 7 million acres between 2015 and 2023, compared with roughly 3 to 4 million acres in the early 2000s. This shift is indicating a structural increase in fire intensity rather than short-term volatility. Federal suppression appropriations are expanding in response to this trend, and budget baselines are rising to reflect recurring fire exposure. Agencies are planning for longer operational periods and higher aircraft utilization rates.

The USFS aviation program budget has more than doubled over the past decade, signaling sustained institutional commitment to aerial suppression capacity. Similarly, EU member states are expanding shared aerial fleets under the rescEU framework to strengthen cross-border response readiness. These verified funding increases are directly elevating demand for fixed-wing airtankers, heavy-lift helicopters, and reconnaissance platforms. Governments are moving away from emergency-only spending models and are adopting multi-year procurement strategies to stabilize fleet availability. This approach is improving revenue predictability for operators, conversion specialists, and maintenance providers. As climate variability is continuing to reshape fire regimes, decision-makers are embedding aviation assets into long-term risk mitigation strategies rather than treating them as seasonal contingencies.

Fleet Modernization and Conversion Programs

National aerial firefighting fleets are undergoing structured renewal. Several countries are retiring aging piston-powered platforms and are transitioning toward turbine-powered and jet-based large airtankers to improve speed, payload capacity, and dispatch reliability. The USFS has been contracting next-generation large airtankers that are delivering higher cruise speeds and increased retardant volume per sortie. In Europe, governments are procuring upgraded amphibious aircraft through coordinated funding mechanisms to enhance rapid water-scooping capability. These modernization initiatives are strengthening operational efficiency and reducing mechanical downtime during peak fire periods. Fleet renewal is therefore becoming a strategic priority rather than a deferred capital decision.

Aircraft conversion economics are reinforcing this transition. Retrofitting a commercial jet or turboprop into a large airtanker generally requires lower capital expenditure than developing a new-build specialized platform, while certification timelines are shorter and deployment cycles are faster. Governments are allocating funding toward conversion programs to expand capacity without incurring extended procurement delays. This approach is increasing demand for specialized retrofit engineering firms, supplemental type certification services, and maintenance, repair, and overhaul (MRO) providers. As more agencies are adopting cost-efficient conversion strategies, recurring inspection, parts replacement, and performance upgrade requirements will have generated sustained aftermarket revenue streams by the end of the forecast period.

Capital Intensity and Seasonal Utilization Risk

Aerial firefighting platforms require substantial capital investment and ongoing operating expenditure. Converting a commercial aircraft into a large airtanker can exceed US$ 30 to US$ 50 million per unit, depending on structural modifications, tank systems, and certification requirements. Heavy-lift helicopters demand specialized maintenance protocols, certified technical crews, and high-cost component overhauls, which are increasing lifecycle expenditure. Seasonal deployment patterns are creating revenue concentration within limited operating windows, particularly in regions where fire seasons are short or highly variable. This utilization imbalance is reducing annual asset productivity and increasing the importance of contract stability. Operators are therefore facing elevated financial exposure when fire intensity declines unexpectedly or when weather conditions reduce flight hours.

To mitigate cash flow volatility, operators are increasingly securing multi-year availability contracts with government agencies. However, call-when-needed agreements are still common in several jurisdictions, and these structures are generating unpredictable revenue inflows. High fixed costs, combined with climate-dependent activation schedules, are constraining smaller and undercapitalized operators from scaling fleets aggressively. Access to financing remains challenging for firms without long-term contractual guarantees. As a result, the market is gradually consolidating around well-capitalized players that can absorb utilization fluctuations. Investors and fleet owners are prioritizing contract-backed expansion strategies and diversified geographic deployment to reduce exposure to regional fire variability.

Regulatory Certification and Airframe Constraints

Aircraft conversion initiatives are operating within strict aviation regulatory frameworks. Programs must secure certification from authorities such as the Federal Aviation Administration (FAA), the European Union Aviation Safety Agency (EASA), and Transport Canada. Approval processes are becoming more rigorous as regulators are conducting detailed structural assessments, flight performance evaluations, and system safety analyses. These reviews are extending certification timelines and are increasing engineering documentation requirements. As a result, new entrants are facing longer time-to-market cycles and higher compliance costs. Project delays are affecting revenue realization and are requiring stronger working capital planning.

The supply of suitable donor aircraft is also tightening. Commercial aviation recovery following the COVID-19 downturn has reduced the availability of parked or retired airframes that are appropriate for modification. Airlines are returning aircraft to service or extending fleet utilization periods, limiting the pool of conversion candidates. This constraint is reducing retrofit capacity and is lengthening procurement lead times for government agencies. Supply limitations are also increasing acquisition prices for eligible aircraft, which is raising overall program costs. Operators and engineering firms are therefore competing more aggressively for viable platforms, and near-term bottlenecks are constraining rapid fleet expansion.

Integration of UAS into Suppression Ecosystems

Government agencies are increasingly integrating unmanned aerial systems into wildfire response operations. Fire authorities are deploying drones for high-resolution mapping, thermal imaging, hotspot detection, and night reconnaissance missions that are difficult or costly for crewed aircraft to perform. The FAA is expanding BVLOS pilot programs, which is enabling broader operational deployment across federal and state jurisdictions. On the other side of the Atlantic, the EASA is advancing regulatory frameworks to support safe drone integration within controlled airspace. These regulatory developments are reducing operational constraints and are encouraging structured procurement of UAS platforms by public agencies.

The UAS segment, as a part of the aerial firefighting market landscape, is expected to exceed US$ 350 to US$ 400 million by 2033 as governments continue prioritizing cost-efficient reconnaissance and rapid deployment capabilities. Lower acquisition costs, reduced fuel consumption, and minimal crew requirements are improving lifecycle economics. Operators integrating drones into conventional fleets are decreasing dependency on high-cost flight hours and are improving operational margins. This convergence of regulatory progress, cost efficiency, and operational flexibility is positioning UAS as a core component of future aerial suppression ecosystems.

Firefighting Program Implementation in Emerging Economies

Governments in Latin America and parts of Southeast Asia are formalizing structured wildfire suppression budgets in response to escalating fire incidents. Brazil and Chile are expanding aerial suppression contracts following severe wildfire seasons that have affected urban interfaces and agricultural zones. Member states of the ASEAN are strengthening cross-border fire management coordination to address transboundary haze and peatland fires. Public agencies are allocating dedicated aviation funding rather than relying solely on emergency response mechanisms. These policy shifts are institutionalizing aerial firefighting capacity within national disaster management frameworks and are increasing demand for fixed-wing aircraft, helicopters, and support services.

Relative to North America and Europe, these regions remain underpenetrated in terms of installed aerial fleet capacity and structured aviation contracts. Based on modeled expenditure announcements, fleet procurement plans, and regional fire exposure trends, these markets could generate incremental value in several hundred millions in cumulative revenue expansion by 2033. Early market entry is enabling operators to secure multi-year concession-style agreements that provide predictable utilization rates. Governments are prioritizing partners that offer integrated fleet management, training, and maintenance support. Investors who establish operational presence during this institutionalization phase are positioning themselves to capture long-term contract pipelines and regional scaling advantages.

Category-Wise Analysis

Platform Type Insights

Fixed-wing aircraft are expected to remain the leading platform in 2026, accounting for approximately 52% of the aerial firefighting market revenue shre. These aircraft are continuing to anchor large-area wildfire suppression strategies due to their high retardant payload capacity and extended operational range. Fleet disclosures from the USFS and the European Union Civil Protection Mechanism (rescEU) are confirming that large airtankers and amphibious water-scooping aircraft are forming the backbone of sustained fire response operations. Governments are prioritizing jet-powered next-generation large airtankers to improve cruise speed, sortie frequency, and drop precision. Capital allocation is increasingly targeting modernization programs that enhance operational readiness and reduce mechanical downtime during peak deployment cycles.

Unmanned aerial systems are poised to emerge as the fastest-growing platform type between 2026 and 2033, expanding at an estimated CAGR of 13%. Agencies are accelerating drone deployment for thermal imaging, hotspot identification, perimeter mapping, and night reconnaissance missions. Lower cost per flight hour and reduced crew requirements are strengthening lifecycle economics relative to conventional aircraft. Regulatory advancements, including an increasing number of BVLOS approvals by aviation authorities, are enabling broader operational integration. Incident command structures are increasingly incorporating UAS data streams into decision-making workflows, and this integration is driving structured procurement budgets for drone platforms and associated software systems.

Technology Insights

Delivery systems are forecasted to remain the dominant technology, commanding approximately 44% of the aerial firefighting market share in 2026. Tank assemblies, pressurized drop mechanisms, and modular retrofit kits are constituting the core hardware investment within aircraft conversion programs. Installation engineering, structural modification, and certification costs are representing a substantial share of overall project expenditure. Governments are prioritizing system upgrades to improve drop accuracy, retardant dispersion control, and sortie efficiency. Fleet modernization initiatives across North America and Europe are sustaining steady demand for advanced delivery configurations, particularly for next-generation large airtankers and amphibious platforms. As agencies are upgrading legacy fleets, retrofit engineering is continuing to generate consistent capital allocation.

Mission systems and software platforms are projected to be the fastest-growing technology segment between 2026 and 2033, registering an estimated 2026-2033 CAGR of 11%. Real-time fire perimeter mapping, predictive spread modeling, and coordinated dispatch optimization tools are gaining operational importance. Governments are embedding data analytics into incident command structures to enhance situational awareness and resource allocation efficiency. Integration of geospatial intelligence with aircraft telemetry is improving drop planning precision and reducing redundant flight activity. Software providers are increasingly offering subscription-based deployment models, which are generating recurring revenue streams and improving long-term margin stability for technology vendors.

Regional Insights

North America Aerial Firefighting Market Trends

North America is projected to account for approximately 45% of the aerial firefighting market value in 2026, maintaining its position as the largest regional market. The United States and Canada are operating the most extensive installed fleet base of fixed-wing airtankers, heavy-lift helicopters, and support aircraft. The USFS is expanding multi-year aviation contracts to stabilize fleet availability and improve operational readiness. Provincial governments in Canada are increasing aviation budget allocations to address longer fire seasons and higher suppression complexity. These structured funding mechanisms are strengthening demand visibility for operators and maintenance providers.

The regional market is projected to showcase a CAGR of nearly 6% during the 2026-2033 forecast period. Climate-driven fire intensity is continuing to elevate suppression expenditure baselines across western North America. Agencies are extending deployment periods and increasing average annual flight hours per aircraft. Investment is concentrating on fleet modernization, conversion upgrades, and enhanced mission coordination systems. Stable public funding structures and mature procurement frameworks are reinforcing predictable revenue streams, positioning North America as a steady but moderately growing market within the global landscape.

Europe Aerial Firefighting Market Trends

Europe is projected to account for approximately 28% of the global market for aerial firefighting technologies and solutions in 2026, positioning it as the second-largest regional market. Southern European countries are experiencing longer and more severe fire seasons, particularly in Mediterranean climate zones. The European Commission (EC) is expanding shared aerial capacity under the rescEU framework to strengthen collective response capability across member states. France, Italy, and Spain are modernizing amphibious aircraft fleets to improve rapid water-scooping operations and cross-border deployment readiness. These coordinated procurement initiatives are enhancing fleet resilience and operational interoperability within the region.

The Europe market is projected to grow at an estimated CAGR of roughly 6.5% from 2026 to 2033. Regulatory harmonization across the EU is improving procurement efficiency and accelerating aircraft acquisition timelines. Governments are allocating multi-year funding to stabilize aerial readiness and reduce dependence on ad hoc leasing. Increased collaboration under joint civil protection mechanisms is optimizing fleet utilization across borders. As climate variability continues to intensify wildfire exposure in Southern Europe, structured investment in aviation assets and modernization programs is sustaining above-average regional growth.

Asia Pacific Aerial Firefighting Market Trends

Asia Pacific is projected to account for an estimated 17% of the aerial firefighting market revenue in 2026. The region is expanding its aviation-based wildfire response capacity in line with rising climate exposure and infrastructure risk. Australia is maintaining one of the highest per-capita aerial suppression budgets globally, supported by structured federal and state funding frameworks. Indonesia and other Southeast Asian countries are strengthening peatland fire response programs to address recurring transboundary haze events. Governments are formalizing procurement strategies and are integrating aerial assets into national disaster management systems.

The regional market is projected to grow at approximately 8.2% CAGR between 2026 and 2033, making it the fastest-growing market for aerial firefighting. Investment is increasing in aircraft leasing, fleet modernization, and cross-border coordination mechanisms. Infrastructure protection, including power transmission networks, transport corridors, and urban peripheries, is driving expanded aerial readiness. ASEAN cooperation frameworks are supporting joint monitoring and rapid deployment initiatives. As fire intensity is continuing to affect economic assets and public health, governments across Asia Pacific are scaling aviation budgets and strengthening long-term suppression capabilities.

Competitive Landscape

The global aerial firefighting market structure demonstrates moderate concentration, with the top five operators accounting for approximately 35-40% of total revenues, based on disclosed fleet sizes and publicly reported contract values. Leading companies such as Conair Group Inc., Coulson Aviation (USA) Inc., Erickson Incorporated, Neptune Aviation Services, Inc., and 10 Tanker Air Carrier, LLC are operating diversified fleets that include large airtankers, amphibious aircraft, and heavy-lift helicopters. These firms are securing multi-year government contracts that are stabilizing revenue streams and supporting capital-intensive fleet modernization programs. Scale advantages are enabling them to optimize aircraft utilization across geographies and extend deployment windows.

Smaller regional operators are concentrating on specialized helicopter services and localized suppression missions, where operational flexibility and proximity to fire-prone zones are creating competitive differentiation. Entry barriers remain high due to stringent aviation certification requirements, significant upfront capital investment, and the need for experienced flight crews and maintenance personnel. Regulatory approvals from authorities such as the FAA and the EASA are requiring rigorous compliance processes. These structural constraints are limiting new market entrants and reinforcing the competitive position of established operators with proven safety records and contract portfolios.

Key Industry Developments

- In February 2026, Swiss research institutions École Polytechnique Fédérale de Lausanne (EPFL) and Swiss Federal Laboratories for Materials Science and Technology (Empa) unveiled a new FireDrone, an aerial system designed to operate safely in extreme heat conditions up to 200 °C that are too dangerous for humans and conventional unmanned aerial vehicles (UAVs). The FireDrone is engineered to support emergency services by transmitting real-time infrared thermal imagery from complex and hazardous environments such as burning buildings, tunnels, and underground structures.

- In February 2026, at the 2026 Singapore Airshow, Commercial Aircraft Corporation of China (COMAC) secured its first commercial order for the C909 firefighting aircraft, consisting of three firm orders and three options for the jet-based fire suppression variant. The C909 firefighting model had received approval from the Civil Aviation Administration of China (CAAC) in December 2025, enabling operational deployment of the special-mission platform.

- In December 2025, Coulson Aviation USA launched a Boeing 767 Very Large Airtanker (VLAT) program aimed at replacing aging MD-11 and DC-10 fire suppression aircraft that are nearing retirement, offering greater payload capacity, improved fuel efficiency, and more sustainable long-term supportability compared with legacy platforms. Engineering work and systems integration planning for the 767 VLAT, which will feature an expanded retardant delivery system and complement Coulson’s existing large airtanker fleet, are already underway.

Companies Covered in Aerial Firefighting Market

- Conair Group Inc.

- Coulson Aviation (USA) Inc.

- Erickson Incorporated

- Neptune Aviation Services, Inc.

- 10 Tanker Air Carrier, LLC

- Bridger Aerospace Group Holdings, Inc.

- Air Spray Ltd.

- Dauntless Air, Inc.

- Aero-Flite, Inc.

- Babcock International Group PLC

- Viking Air Limited

- Textron Inc.

- Lockheed Martin Corporation

- Airbus SE

Frequently Asked Questions

The global aerial firefighting market is projected to reach US$ 1.5 billion in 2026.

Prolonging of the duration of fire seasons and strengthening of multilateral coordination frameworks such as the rescEU are driving the market.

The market is poised to witness a CAGR of 6.9% from 2026 to 2033.

Acceleration of fleet recapitalization initiatives and integration of drones into reconnaissance and thermal mapping missions to improve operational efficiency are key market opportunities.

Conair Group Inc., Coulson Aviation (USA) Inc., Erickson Incorporated, and Neptune Aviation Services are some of the key players in the market.