- Specialty & Fine Chemicals

- Acrylate Oligomer Market

Acrylate Oligomer Market Size, Trends, Share, and Growth Forecast 2026 - 2033

Acrylate Oligomer Market by Product Type (Urethane, Polyester, Silicone, Epoxy, Misc.), by Application (Coatings, Adhesives & Sealants, Printing Inks, Composite Materials, 3D Printing Resins, Electronics Encapsulation, Optical Materials, Others), by Regional Analysis, 2026 - 2033

Acrylate Oligomer Market Size and Trend Analysis

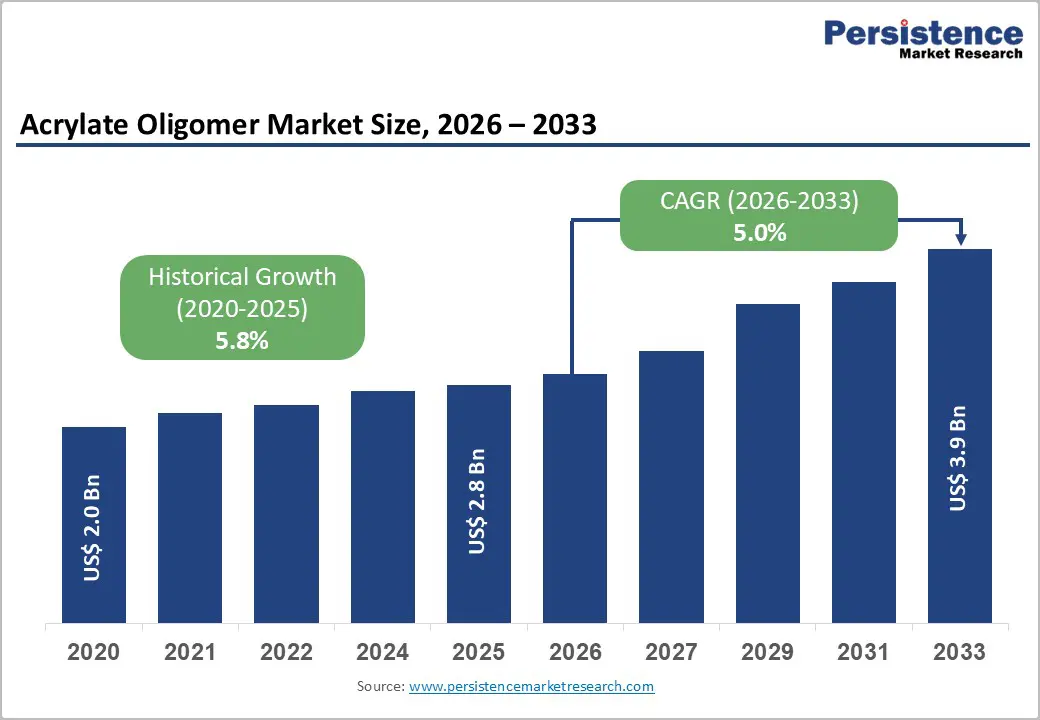

The global acrylate oligomer market size is likely to be valued at US$ 2.8 billion in 2026 and reach US$ 3.9 billion by 2033, growing at a CAGR of 5.0% between 2026 and 2033.

The accelerating transition from conventional solvent-based to energy-efficient, environmentally sustainable UV-curable and electron beam-curable coatings and adhesives is driving robust market expansion. The convergence of stringent environmental regulations, including VOC emission limits, rising consumer demand for low-volatile organic compound formulations, and industrial emphasis on green chemistry principles is compelling manufacturers to adopt acrylate oligomer-based solutions. Major industries such as automotive, aerospace, electronics, packaging, and construction are increasingly deploying acrylate oligomers to achieve superior durability, scratch resistance, and rapid curing capabilities.

Key Industry Highlights:

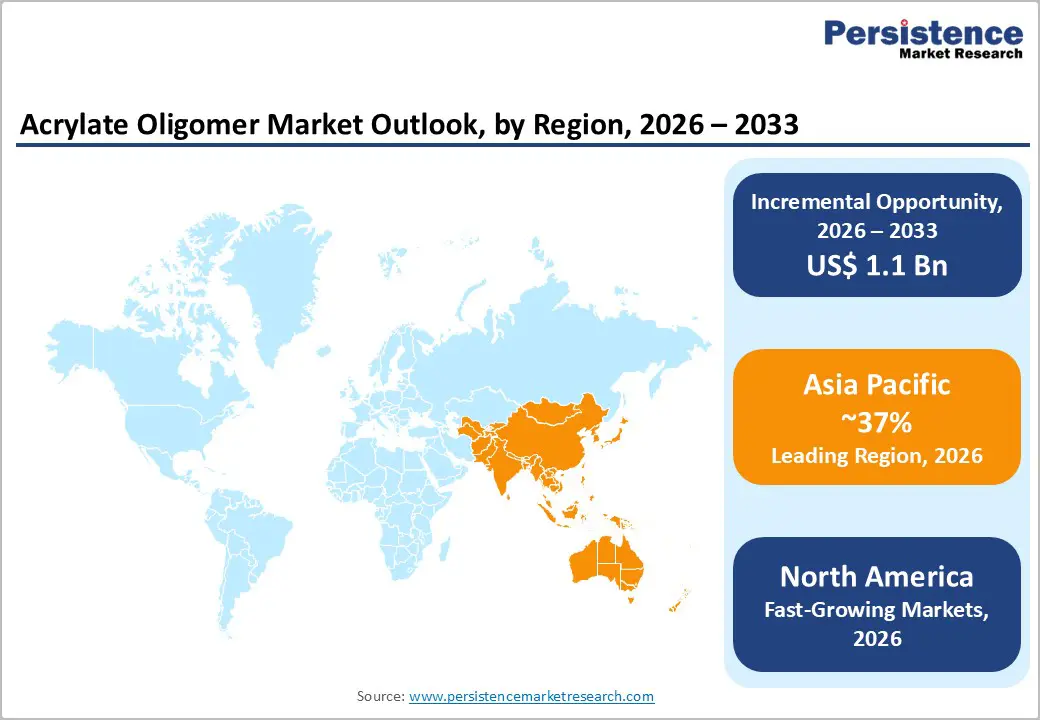

- Leading Region: Asia Pacific commands the largest regional market share of approximately 37% in 2025, driven by rapid industrialization, expanding manufacturing base in China and India, accelerating automotive production, and strong growth in electronics and construction sectors.

- Fastest Growing Region: North America represents the fastest-growing regional market, expanding at approximately 5.2% CAGR through 2033, supported by a robust industrial base, advanced manufacturing capabilities, substantial R&D infrastructure, and accelerating adoption of sustainability-focused UV-curable systems.

- Dominant Segment: Urethane acrylates dominate the product segment, commanding approximately 50% market share in 2025, reflecting exceptional versatility, superior mechanical properties, and outstanding chemical and abrasion resistance enabling deployment across diverse high-performance applications.

- Fastest Growing Segment: Polyester acrylates represent the fastest-growing product category, expanding at approximately 7% CAGR through 2033, driven by superior mechanical performance, cost-effectiveness, and expanding adoption in adhesive and composite applications.

- Key Opportunity: Electronics encapsulation and optical materials represent the fastest-growing application segments, expanding at approximately 9% CAGR through 2033, driven by miniaturization trends in consumer electronics, 5G telecommunications expansion, and advanced optical system development supporting augmented reality and virtual reality applications.

| Key Insights | Details |

|---|---|

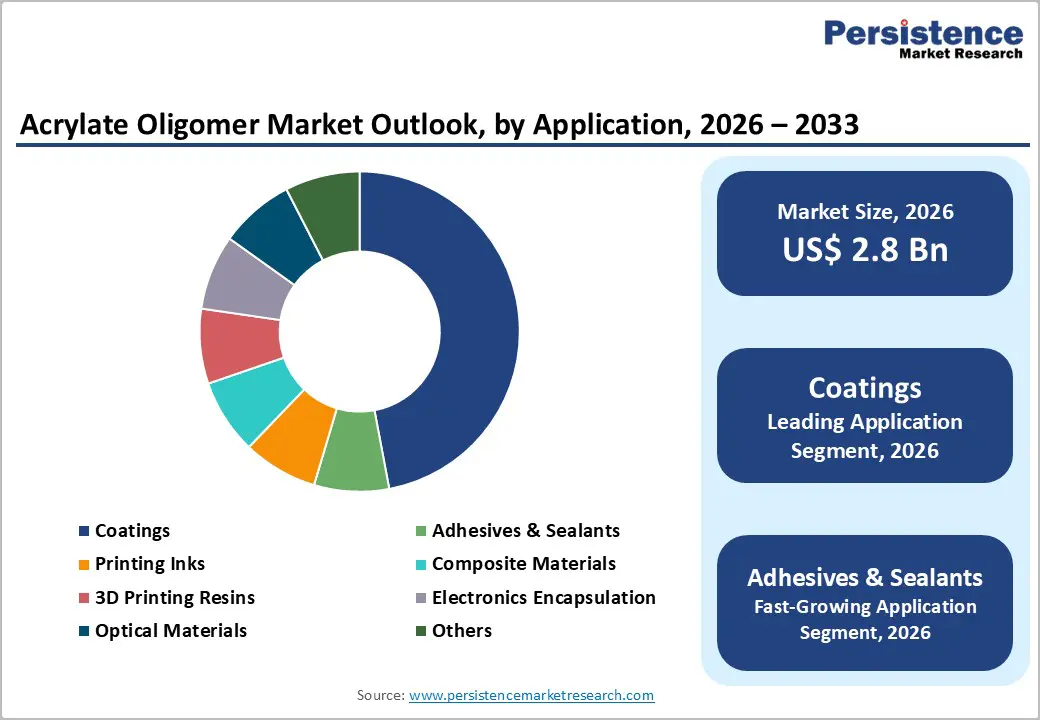

| Acrylate Oligomer Market Size (2026E) | US$ 2.8 billion |

| Market Value Forecast (2033F) | US$ 3.9 billion |

| Projected Growth CAGR (2026 - 2033) | 5.0% |

| Historical Market Growth (2020 - 2025) | 5.8% |

Market Dynamics

Drivers - Rise in Demand for Low-VOC and Eco-Friendly Formulations

The global regulatory environment increasingly mandates reduced volatile organic compound emissions across coatings, adhesives, inks, and industrial formulations, driving accelerated adoption of acrylate oligomer-based solutions. The European Union’s stringent VOC Directive (2004/42/EC) and regulatory harmonization initiatives have established binding limits on solvent emissions, compelling manufacturers to transition from traditional solvent-based systems to advanced UV-curable formulations incorporating acrylate oligomers. Research demonstrates that approximately 25% of new oligomer innovations specifically emphasize eco-friendly acrylate oligomers, reflecting market emphasis on sustainable chemistry.

The convergence of rising environmental consciousness among consumers, corporate sustainability commitments, and government incentives promoting green chemistry has accelerated adoption across diverse applications including furniture finishes, protective films, and industrial coatings. Arkema’s Sartomer specialty acrylate oligomers exemplify industry innovation focused on minimal yellowing, exceptional transparency, and superior durability, enabling vibrant color reproduction in UV-cured applications. Automotive manufacturers, including major German OEMs, are increasingly adopting UV-curable acrylate oligomer-based coatings to enhance vehicle appearance and longevity while maintaining compliance with stringent environmental regulations.

Rapid Expansion of 3D Printing and Additive Manufacturing Applications

The explosive growth of additive manufacturing and 3D printing applications is creating substantial demand for high-performance acrylate oligomers optimized for rapid photopolymerization and superior mechanical properties. 3D printing resin systems incorporating advanced acrylate oligomers enable manufacturers to produce complex, precision components with exceptional mechanical strength, thermal resistance, and dimensional accuracy, supporting industrial applications including aerospace, medical devices, and electronics. Acrylate oligomers deliver the critical building blocks for 3D printing resins, combining flexibility and impact resistance with high-temperature performance capabilities.

The global 3D printing materials market size is valued at US$ 3.1 billion in 2025 and is projected to reach US$ 12.9 billion by 2032, growing at a CAGR of 22.6% between 2025 and 2032, with acrylate oligomer-based resin systems representing the dominant resin category due to superior curing speed, resolution, and post-processing properties. The integration of advanced oligomers enabling precise color reproduction, minimal yellowing, and exceptional surface finish quality supports premium applications including jewelry, dental prosthetics, and architectural models. This convergence of rapid 3D printing market expansion, increasing material performance requirements, and oligomer innovation is driving exceptional growth opportunities in advanced additive manufacturing applications.

Restraints - Volatility in Raw Material Costs and Supply Chain Disruptions

Acrylate oligomer production depends on sophisticated petrochemical feedstocks, including acrylic acid derivatives, polyols, and specialty monomers, whose prices exhibit substantial volatility responding to crude oil price fluctuations and geopolitical disruptions. The global energy crisis and supply chain disruptions experienced since 2021 have created sustained uncertainty regarding raw material availability and pricing, particularly for critical building block compounds. Manufacturers face ongoing challenges managing input cost variations while maintaining competitive pricing, particularly in price-sensitive applications, including standard industrial coatings and adhesives.

Supply chain vulnerabilities associated with concentrated production of critical monomers in specific geographic regions create manufacturing and sourcing risks. The semiconductor shortage and chemical industry capacity constraints experienced through 2023 created significant production bottlenecks affecting oligomer manufacturers’ ability to fulfill growing demand. These challenges require manufacturers to pursue strategic sourcing initiatives, vertical integration, and hedging strategies to mitigate raw material cost exposure and supply availability risks.

Complex Regulatory Compliance Requirements and Environmental Restrictions

The increasingly stringent global regulatory landscape governing chemical substances, waste management, and environmental protection creates substantial compliance complexity and operational costs for acrylate oligomer manufacturers. REACH regulations in the European Union, China’s comprehensive chemical regulations, and emerging regulatory frameworks in developing markets impose rigorous testing, documentation, and substance restriction requirements.

Compliance with evolving regulations including VOC restrictions, water-based system mandates in specific applications, and emerging restrictions on specific chemical structures requires substantial research and development investments and regulatory expertise. The uncertainty surrounding future regulatory developments, particularly regarding polymer restrictions and microplastic concerns, creates hesitation among manufacturers regarding long-term investment decisions. Manufacturers must navigate divergent regulatory requirements across multiple jurisdictions, creating operational complexity and increased compliance costs.

Opportunity - Accelerating Adoption in Automotive and Electric Vehicle Manufacturing

Exceptional market opportunities exist in automotive applications, particularly electric vehicle manufacturing, where acrylate oligomer-based UV-curable coatings and adhesives are enabling enhanced performance, sustainability, and manufacturing efficiency. Electric vehicle production is expanding at approximately 20-25% annually globally, creating substantial demand for high-performance materials including specialized coatings and adhesives incorporating advanced acrylate oligomers. UV-curable coatings incorporating acrylate oligomers deliver superior mechanical properties, enhanced scratch resistance, and rapid curing characteristics enabling accelerated vehicle production timelines.

The integration of advanced encapsulation materials for battery systems and electronic components using acrylate oligomer-based resins is driving emerging high-value applications. German automotive manufacturers are increasingly adopting UV-curable acrylate oligomer-based coatings to enhance vehicle appearance, durability, and environmental compliance. The automotive segment represents the fastest-growing end-use application, projected to expand at approximately 8% CAGR through 2033.

The convergence of accelerating EV production volumes, stringent environmental regulations in transportation, and material performance requirements is creating compelling opportunities for acrylate oligomer manufacturers capable of developing specialized automotive formulations.

Expansion of Electronics Encapsulation and Optical Material Applications

Significant opportunities exist in electronics encapsulation and optical material applications, representing the fastest-growing segment at approximately 9% CAGR through 2033, driven by miniaturization trends in consumer electronics and demand for high-performance optical systems. Advanced acrylate oligomer resins enable precise encapsulation of complex electronic assemblies including 5G telecommunications equipment, high-speed data transmission systems, and advanced display technologies.

The mini-LED and micro-LED market is expanding at approximately 17% CAGR, driven by adoption in premium smartphones, tablets, and automotive dashboards, creating substantial demand for encapsulant materials with ultra-low viscosity, exceptional moisture resistance, and optical clarity.

Apple’s adoption of mini-LED backlighting in iPad Pro and MacBook Pro exemplifies premium applications demanding specialized encapsulant materials preventing delamination under prolonged heat exposure. Optical materials incorporating advanced acrylate oligomers are enabling next-generation applications in augmented reality, virtual reality, and advanced imaging systems.

The convergence of miniaturization trends in consumer electronics, rising demand for high-speed data infrastructure, and optical system innovations creates substantial value for oligomer manufacturers capable of developing specialized formulations addressing specific application requirements including ultra-low viscosity, wavelength transparency, and thermal stability.

Category-wise Analysis

Product Type Insights

Urethane acrylates dominate the acrylate oligomer market, commanding approximately 50% market share in 2025, reflecting exceptional versatility, superior mechanical properties, flexibility, and outstanding chemical and abrasion resistance characteristics. Urethane acrylates deliver the optimal balance of performance attributes, enabling their deployment across diverse applications including high-performance coatings, adhesives, and industrial inks where superior durability is essential.

The aliphatic urethane acrylates segment represents approximately 36% of UV-curable urethane acrylate oligomer market share, driven by superior UV stability and outdoor durability performance enabling extended service life in exterior applications.

Application Insights

Coatings represent the dominant application segment, commanding approximately 45% market share in 2025, driven by escalating demand for UV-curable coatings in wood finishes, protective films, automotive, and industrial applications. The wood and paper coatings segment within the UV-curable resin category demonstrates exceptional growth at approximately 10.1% CAGR, driven by superior adhesion, rapid curing times, and high surface hardness characteristics essential for premium finish applications.

However, adhesives and sealants emerge as the fastest-growing application category, expanding at approximately 8% CAGR through 2033, driven by demand for high-strength pressure-sensitive adhesives, structural adhesives, and advanced sealants in automotive, construction, medical, and aerospace applications.

Regional Insights

North America Acrylate Oligomer Market Trends and Insights

North America maintains strong market position, valued at approximately US$ 900 million in 2025 and projected to reach approximately US$ 1,500 million by 2033. The United States dominates North American market supported by robust industrial base, advanced manufacturing capabilities, and substantial research and development infrastructure. The region benefits from substantial venture capital investment and innovation ecosystems supporting continuous advancement in acrylate oligomer formulation and application development.

North American enterprises prioritize sustainability and environmental compliance, driving accelerated adoption of low-VOC and eco-friendly acrylate oligomer formulations. The convergence of stringent EPA regulations, rising consumer demand for environmentally responsible products, and corporate sustainability commitments is compelling manufacturers to transition to advanced UV-curable systems incorporating specialized acrylate oligomers.

The 3D printing market in North America is expanding exceptionally rapidly, with manufacturers increasingly adopting acrylate oligomer-based resin systems for industrial applications including aerospace components, medical devices, and advanced prototyping. The region’s concentration of automotive manufacturing, advanced electronics production, and aerospace industries creates substantial demand for high-performance acrylate oligomers enabling superior product performance and environmental compliance.

Europe Acrylate Oligomer Market Trends and Insights

Europe represents about a one-fifth share of global acrylate oligomer, driven by stringent environmental regulations, strong sustainability emphasis, and robust demand across automotive, packaging, and industrial applications. Germany, France, and the United Kingdom lead European adoption, with substantial emphasis on low-VOC coatings, advanced adhesive technologies, and sustainable formulation development. The EU Green Deal and Circular Economy Action Plan initiatives are compelling manufacturers to adopt eco-friendly, recyclable polymer materials, driving accelerated acrylate oligomer adoption across coatings and adhesive applications.

European automotive manufacturers including major German OEMs are increasingly transitioning to UV-curable acrylate oligomer-based coatings to enhance vehicle appearance and longevity while maintaining stringent environmental compliance. The UK market demonstrates persistent growth driven by packaging, electronics, and automotive industry expansion, with companies implementing alternatives to solvent-based products to comply with evolving environmental regulations.

Regulatory harmonization across EU member states is creating unified requirements supporting consistent adoption of advanced acrylate oligomer formulations across the region. Evonik Industries AG strategic restructuring emphasizing specialty chemicals including polyester acrylate oligomers demonstrates industry commitment to focusing on high-performance materials addressing evolving market demands.

Asia Pacific Acrylate Oligomer Market Trends and Insights

Asia Pacific dominates global acrylate oligomer market, commanding approximately 37% market share in 2025, driven by rapid industrialization, expanding manufacturing base, and accelerating adoption across automotive, electronics, and construction sectors. China represents the largest Asia Pacific market with expanding manufacturing base supporting industrial coatings, adhesives, and specialty applications. China oligomer market is expanding at approximately 5.8% CAGR, driven by rapid economic growth, expanding automotive production, rising construction activities, and accelerating electronics manufacturing.

India’s rapidly urbanizing economy, strong growth in construction, automotive, and packaging industries, combined with government initiatives promoting sustainable development and infrastructure investments, is driving substantial acrylate oligomer demand expansion. Japan’s sophisticated technology base and emphasis on advanced materials, coupled with the region’s concentration of electronics and automotive manufacturing, support continued strong demand.

ASEAN nations including Vietnam, Thailand, and Indonesia are experiencing accelerating industrialization and manufacturing expansion, creating emerging opportunities for acrylate oligomer suppliers. The region’s manufacturing advantages, cost-effective production capabilities, and expanding domestic demand create compelling growth opportunities for manufacturers capable of scaling production and meeting regional requirements.

Competitive Landscape

The acrylate oligomer market reflects a moderately consolidated competitive landscape, with a small group of established specialty chemical producers holding substantial share while regional manufacturers and formulation specialists compete in niche segments. Market structure is shaped by high capital requirements, technology-intensive production processes, and the need for global distribution capabilities, creating barriers to entry and reinforcing incumbent advantage. Competitive strategies increasingly emphasize development of eco-friendly, low-VOC and UV-curable chemistries aligned with tightening regulatory frameworks and rising sustainability expectations across end-use industries.

Leading suppliers are expanding manufacturing capacity, pursuing backward integration to secure raw material availability, and strengthening application-specific technical support capabilities to deepen customer relationships. Partnerships with 3D printing system manufacturers, electronics component suppliers, and automotive coating formulators are accelerating technology adoption and enabling differentiated product positioning. Consolidation continues as established companies acquire smaller formulation innovators to expand product portfolios, enhance performance attributes, and access high-growth regional markets.

Key Market Developments

- May 2024: Arkema showcased sustainable acrylate oligomer innovations for UV/LED/EB curing at RadTech 2024, including bio-based SARBIO® acrylate oligomers (up to 88% bio-content), new difunctional oligomers for 3D printing, and "Inherently Reactive" urethane acrylate oligomers with low migration and extractables.

- December 2025: Hesheng Chemical has launched a new Waterborne Epoxy Silane Oligomer. This product combines epoxy resin adhesion with silane oligomer weather resistance, delivering superior waterproof and anti-corrosion performance, low VOC content for environmental benefits, and easy application in coatings for construction, automobiles, and ships.

- April 2025: hubergroup Chemicals showcase groundbreaking bio-based oligomers at RadTech 2025. These innovative products offer sustainable alternatives for industrial UV coatings, delivering high performance while reducing environmental impact through renewable raw materials and low VOC formulations.

Companies Covered in Acrylate Oligomer Market

- Arkema SA

- BASF SE

- Covestro AG

- Royal DSM

- Hitachi Chemical Company Ltd.

- Nippon Gohsei

- Lambson Limited

- Allnex Group

- Jiangsu Sanmu Group Corporation

- Miwon Specialty Chemical Co. Ltd.

- Toagosei Co. Ltd.

- IGM Resins B.V.

- Alberdingk Boley GmbH

- Evonik Industries AG

- Mitsubishi Chemical Group

- DIC Corporation

- Showa Denko Materials

- Shin-Etsu Chemical Co., Ltd.

Frequently Asked Questions

The global Acrylate Oligomer Market is expected to reach around US$ 2.8 billion in 2026.

Demand is driven primarily by stringent VOC regulations, growing eco-friendly formulation adoption, and increasing use in advanced manufacturing and 3D printing applications.

The Asia Pacific region is expected to maintain the largest market share throughout the forecast period.

Key opportunities lie in EV manufacturing, UV-curable coatings, electronic encapsulation, and optical material applications.

Leading market participants include BASF SE, Arkema SA, Covestro AG, Allnex Group, Royal DSM, etc.