ID: PMRREP13345| 200 Pages | 24 Dec 2025 | Format: PDF, Excel, PPT* | IT and Telecommunication

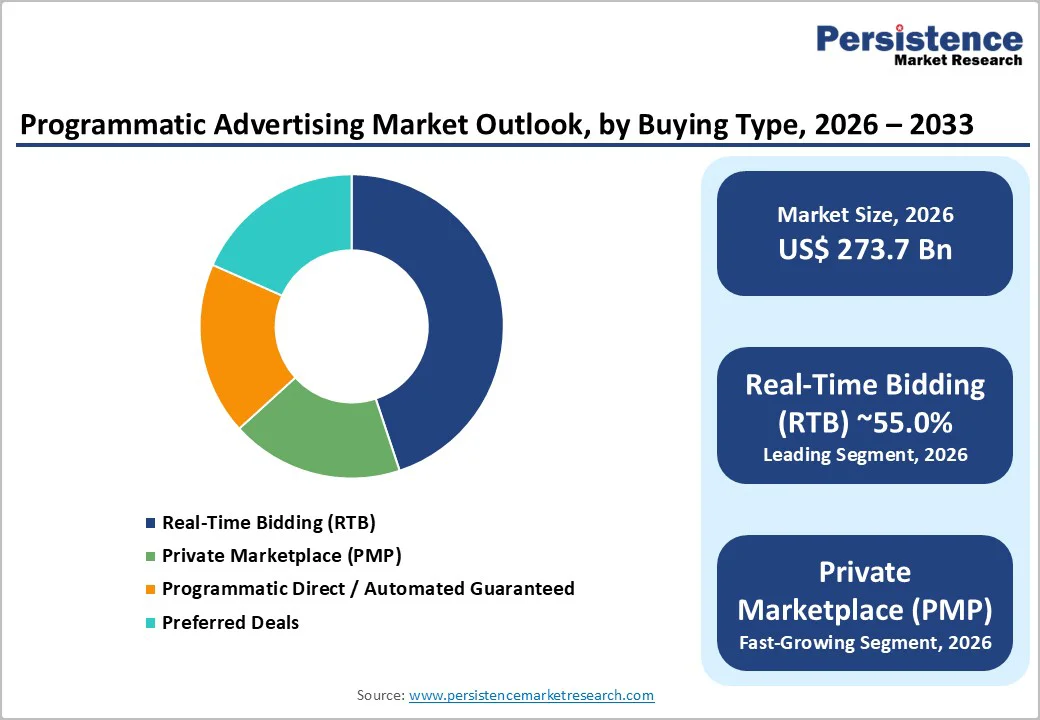

The global programmatic advertising market is projected to reach US$ 975.1 billion by 2033, growing at a CAGR of 19.9% between 2026 and 2033. The market is likely to be valued at US$ 273.7 billion in 2026.

The market continues to consolidate its position as the dominant transaction model for digital advertising, driven by three primary factors: the accelerating adoption of artificial intelligence and machine learning technologies that enhance targeting precision and optimize bidding strategies in real time; the fundamental shift in consumer media consumption toward streaming platforms and connected TV environments, creating new inventory categories and audience segments; and the escalating demand from retailers and enterprises for measurable, performance-driven advertising solutions that deliver transparent return on investment across digital channels.

| Global Market Attributes | Key Insights |

|---|---|

| Programmatic Advertising Market Size (2026E) | US$ 273.7 Bn |

| Market Value Forecast (2033F) | US$ 975.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 19.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 17.7% |

The integration of artificial intelligence and machine learning is a transformative force in the Programmatic Advertising Market, fundamentally reshaping how ad-buying decisions are made. AI-powered systems now process millions of data signals per hour across programmatic platforms, enabling real-time analysis of user behaviour, contextual relevance, and optimal bid pricing without human intervention.

Machine learning algorithms evaluate historical auction data, user engagement patterns, and performance metrics to predict which impressions are most likely to convert, enabling advertisers to allocate budgets to high-value opportunities while minimizing waste. In 2024, more than 790 programmatic platforms integrated machine learning for predictive ad placements and audience behaviour modelling, with over 43% of programmatic campaigns benefiting from AI-optimization. Google reports that AI-powered bidding strategies can reduce cost-per-acquisition by up to 30%, while simultaneously delivering 22% improvements in conversion rates.

The programmatic advertising market is experiencing accelerated adoption of AI-driven sentiment analysis tools that reduce ad fatigue by 27% through dynamic creative frequency adjustment. These technological advancements enable advertisers to execute campaigns across 2.7 devices per user on average, improving message sequencing and personalization effectiveness while enhancing overall campaign margins and ROI predictability.

The fundamental transformation in how audiences consume video content has created unprecedented demand for programmatic solutions designed specifically for streaming environments. Connected TV (CTV) has transitioned from a nascent channel to become television's growth engine, with streaming now accounting for 43.8% of all US TV viewing time as of March 2025, up 10 percentage points over two years. CTV ad spending is projected to exceed $40 billion globally by 2028, representing 10 times faster growth than linear television advertising.

The Programmatic Advertising Market has responded by developing specialised tools and supply-side platforms that enable programmatic buying across CTV inventory, with CTV programmatic tools expanding to 180 new platforms in 2024, enabling audience extension to connected TVs across 64 countries. Advertisers have documented that CTV generates 10 times more conversions than linear TV despite using just 60% of the media budget, making it an increasingly central component of performance marketing strategies.

By 2030, CTV is projected to account for more than 40% of global ad spending, surpassing the combined share of broadcast and cable television. This shift is being amplified by the adoption of ad-supported video-on-demand (AVOD) models, where 72.4% of US TV viewing time is now ad-supported, with streaming comprising 42.4% of that total. The Programmatic Advertising Market's expansion into CTV has enabled advertisers to deploy closed-loop measurement systems linking impressions directly to retail transactions, creating a superior performance accountability framework compared to traditional broadcast television.

The accelerating penetration of digital commerce, mobile connectivity, and internet infrastructure across the Asia Pacific and other emerging markets has fueled unprecedented growth in digital advertising budgets. Global e-commerce is projected to surpass $6.86 trillion in 2025, with 2.77 billion online shoppers representing 33% of the world's population. India's e-commerce market, valued at US$ 125 billion in 2024, is expanding at a 15% CAGR and is projected to reach US$ 345 billion by 2030, creating substantial demand for programmatic solutions.

The Programmatic Advertising Market is benefiting from the rapid expansion of digital payment infrastructure, with digital wallets and UPI transactions facilitating 20 billion transactions worth US$ 288.65 billion in August 2025 alone in India. Programmatic buying now accounts for 78% of digital impressions in the BFSI sector and 88% of all digital ad impressions globally, reflecting complete ecosystem penetration.

In 2024, over 2.3 trillion programmatic ad impressions were recorded across display, video, mobile, and social channels, with mobile ads comprising over 63% of total programmatic impressions. The Programmatic Advertising Market continues to capture a disproportionate share of incremental advertising budgets, with programmatic channels accounting for 96.8% of new display ad dollars in 2025.

Regulatory frameworks, including the General Data Protection Regulation (GDPR) in Europe and the California Consumer Privacy Act (CCPA) in the United States, along with emerging state-level privacy legislation, have created substantial compliance burdens that constrain the effectiveness of programmatic advertising.

Approximately 88% of advertisers anticipate that privacy regulations will moderate or significantly alter their programmatic targeting strategies, particularly regarding personalised ad delivery. The absence of a federal data privacy framework in the United States has created jurisdictional fragmentation, requiring advertisers to simultaneously comply with multiple state-level standards that impose inconsistent requirements for data collection, consent management, and user privacy protection. These regulatory constraints have necessitated fundamental shifts in data architecture, with advertisers redirecting budgets toward first-party data collection and customer data platforms (CDPs) rather than third-party data marketplaces, increasing operational complexity and infrastructure costs.

The recognised need for greater transparency and efficiency within programmatic supply chains has catalysed a market-wide shift toward supply path optimisation (SPO) and direct programmatic partnerships that bypass unnecessary intermediaries. Supply path optimisation enables demand-side platforms to identify the most efficient routes to publisher inventory by limiting bid requests to preferred sellers and eliminating unauthorised resellers engaged in fraud. By consolidating connections with high-quality supply partners and reducing supply chain hops from five or more to two or three, advertisers can simultaneously achieve cost reductions, improve ad quality assurance, and reduce fraud exposure.

The programmatic advertising market is experiencing structural transformation as advertisers systematically audit and simplify their supply paths, leading to better ROI predictability and improved measurement accuracy. Publishers are concurrently enhancing supply-side optimisation by auditing their ads.txt and sellers.json files to verify partner authorisation and eliminate unnecessary technology intermediaries.

The convergence of direct programmatic buying with private marketplaces has become a core market opportunity, with over 91% of total US programmatic display ad spending projected to flow toward private marketplaces (PMPs) and programmatic direct in 2025, compared with minimal growth on open exchanges. Private marketplace spending is expected to grow nearly 13% in 2025, substantially outpacing open exchange growth.

The programmatic advertising market's structural shift toward PMPs and direct buying has created opportunities for specialised technology platforms, independent agencies, and mid-market advertisers seeking equitable access to premium streaming inventory. In December 2025, the partnership between Untapped Growth and FreeWheel exemplifies this opportunity, providing indie and mid-sized advertisers with transparent pricing and direct access to high-quality CTV audiences previously limited to major advertisers, while simultaneously diversifying publisher demand sources and creating a more inclusive programmatic ecosystem.

The fragmented landscape of programmatic buying, selling, and attribution systems has created substantial inefficiencies and workflow impediments that specialised technology platforms are systematically addressing. The programmatic advertising industry is experiencing standardisation of AI workflows through collaborative initiatives such as the October 20, 2025, launch of the Ad Context Protocol (AdCP) by over 20 companies, including Yahoo, PubMatic, Scope3, and Triton Digital.

AdCP standardises how AI-driven media agents execute buying and selling across fragmented publisher landscapes, enabling advertisers direct access to inventory and publishers to offer products efficiently while simplifying, optimising, and increasing transparency in programmatic buying. Agentic advertising represents a substantial market opportunity, with AI agents now capable of executing real-time campaign analysis, mid-flight optimisation, and strategic bidding decisions without human intervention. The Programmatic Advertising Market continues to expand AI agent capabilities, enabling algorithms to manage audience targeting through first-party CRM data, geo-targeting, demographic filters, and intent-based segments.

This technological standardisation reduces operational friction, enables faster campaign deployment, and facilitates adoption by smaller advertisers and publishers previously excluded from sophisticated programmatic systems.

The leading segment is Real-Time Bidding (RTB), which is expected to command a dominant 55.0% share in 2026. RTB's leadership is driven by its efficiency, allowing advertisers to bid on ad impressions in real-time auctions, which enables precise targeting and cost-effective media buying at scale across the open web.

The fastest-growing segment is the Private Marketplace (PMP). PMPs offer a more controlled, invitation-only auction environment where premium publishers make their inventory available to a select group of advertisers. This model provides greater transparency and brand safety than open RTB auctions, which is increasingly appealing to brands concerned about the quality of their ad placements. The growth of PMPs reflects a market trend toward prioritising quality and control alongside the scale offered by programmatic execution.

Display Ads are the leading segment, projected to hold a market share of 32.0% in 2026. Their prevalence is due to their versatility, cost-effectiveness, and broad reach across websites and apps. Display ads serve as a foundational format for many digital campaigns, from brand awareness to direct response, making them a staple in programmatic advertising strategies.

The fastest-growing segment is Video Ads (In-stream & Out-stream). The surge in video consumption, particularly on mobile devices and Connected TV (CTV), is fueling the demand for programmatic video advertising. Advertisers are increasingly allocating budgets to video to leverage its high engagement rates and storytelling capabilities. As programmatic technologies for CTV and OTT mature, through partnerships like Xumo and PubMatic, the ability to target and measure video ad campaigns with precision is accelerating the growth of this format.

The Retail & E-Commerce sector is the leading segment, accounting for an estimated 24.0% of the market in 2026. This dominance is propelled by the massive and continuous growth of online shopping, which is projected to involve 2.86 billion shoppers in 2026. Retailers heavily rely on programmatic advertising to drive traffic, retarget customers, and boost sales in a competitive digital landscape.

The fastest-growing segment is Media & Entertainment. This sector is increasingly adopting programmatic strategies to promote content, acquire subscribers for streaming services, and engage audiences across a fragmented media landscape. The proliferation of streaming platforms and digital content has created a heightened need for data-driven, automated advertising to reach viewers efficiently. As consumers spend more time on digital platforms, media and entertainment companies are investing heavily in programmatic advertising to capture their attention.

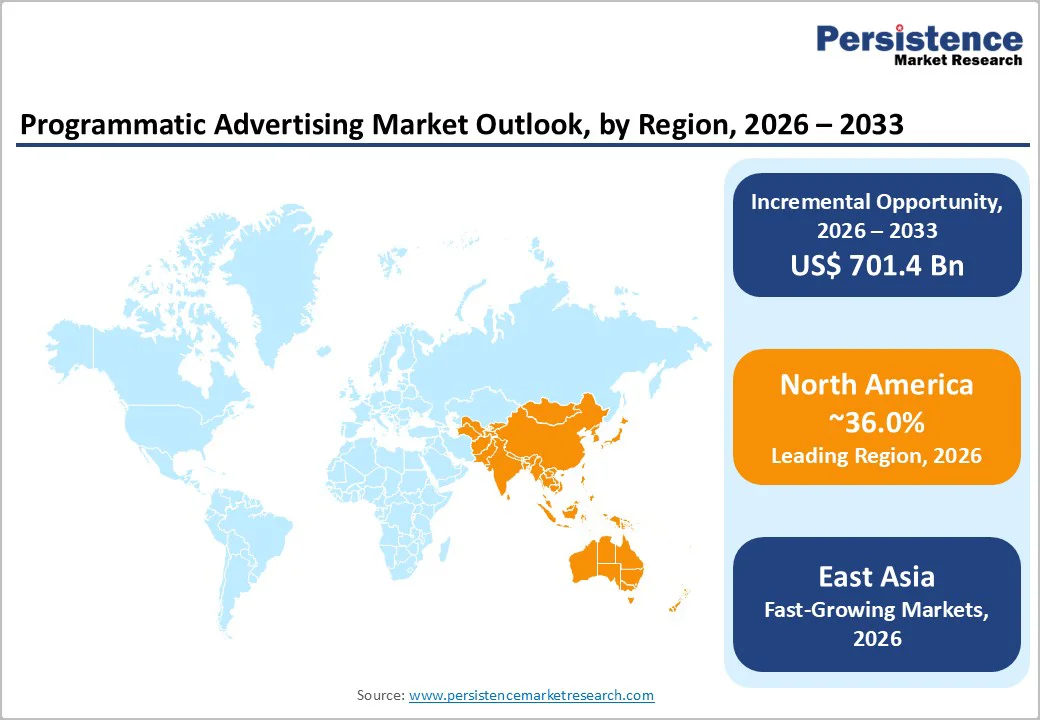

North America represents 36% of the global programmatic advertising market, maintaining the largest absolute market share despite a gradually declining percentage contribution as Asia Pacific markets experience accelerated growth. The United States dominates global programmatic ad spend, accounting for over 52% of global programmatic transactions in 2024, reflecting the region's advanced digital infrastructure, sophisticated advertiser capabilities, and mature programmatic platform ecosystem.

Regulatory developments have substantively influenced North America's programmatic market trajectory, with privacy legislation, including CCPA and the absence of federal data privacy frameworks, creating compliance complexity that has incentivized first-party data strategies and contextual advertising adoption. Advertisers in North America have systematically redirected budgets toward direct publisher relationships and private marketplaces, with over 91% of U.S. programmatic display ad spending projected to flow toward PMPs and programmatic direct in 2025.

Strategic investments and platform consolidation continue to characterize the competitive landscape, with major technology firms including Google, Amazon, Adobe, and Microsoft maintaining dominant market positions. The region has also witnessed the emergence of specialised providers targeting mid-market advertisers and independent agencies, such as the December 3, 2025, partnership between Untapped Growth and FreeWheel, which democratized access to premium CTV opportunities for smaller advertisers. North America's programmatic market continues to lead in technological innovation, AI integration, and development of cross-channel attribution and measurement solutions supporting advertiser ROI optimisation.

East Asia is a critical region in the global programmatic advertising market, projected to hold a 28% share. The region's growth is powered by its massive and rapidly growing digital population and the dominance of mobile-first economies. China leads the world with 904.6 million online shoppers, creating an enormous addressable audience for programmatic campaigns. The Asia Pacific (APAC) region is expected to capture 80% of the B2B e-commerce market share by 2026, a trend that will fuel significant investment in programmatic B2B advertising.

Countries such as India are experiencing explosive e-commerce growth, with the market valued at US$ 125 billion in 2024 and projected to reach US$ 345 billion by 2030, driven by rising internet penetration in tier-II and tier-III cities. Government initiatives such as India's Open Network for Digital Commerce (ONDC) are further expanding the digital commerce infrastructure, creating fertile ground for programmatic advertising. The preference for virtual sales models is also high, with over 90% of B2B companies in the region having shifted to this approach since 2020, solidifying the need for automated and data-driven advertising solutions.

Europe is a substantial market for programmatic advertising, accounting for an estimated 24% of the global share. The region is characterised by a diverse collection of mature and emerging digital markets. The UK, Germany, and France are among the top advertising spenders, with high levels of digital adoption. The market's growth is supported by a strong e-commerce sector and increasing investment in programmatic channels, particularly video and CTV.

The defining characteristic of the European market is its stringent regulatory environment, led by the General Data Protection Regulation (GDPR). This has forced the industry to innovate in privacy-centric advertising solutions, such as contextual targeting and data clean rooms. Strategic partnerships are also shaping the market, such as the collaboration between Advertima and One Tech Group in June 2025 to enable audience-based programmatic advertising in Swiss in-store retail media networks. This move highlights a trend toward bringing programmatic precision to physical environments, creating a more integrated omnichannel advertising ecosystem across the region.

The global programmatic advertising market is moderately consolidated with oligopolistic characteristics, where a handful of large players dominate ad spend and technological innovation, while a long tail of smaller platforms serves niche or regional segments.

Alphabet Inc. (Google LLC), Meta, Amazon.com, Inc., Adobe, The Trade Desk, Magnite, and PubMatic are among the leading companies, leveraging their scale, first-party data, and omnichannel capabilities to offer highly targeted and efficient ad solutions. These players control a significant portion of inventory across display, video, CTV, and mobile channels, creating high entry barriers for new competitors.

Specialised platforms such as Index Exchange, Criteo, and NextRoll cater to specific formats or regional markets, contributing to a fragmented fringe. The market is driven by innovations in AI, audience targeting, and cross-channel integration, while privacy regulations and cookieless environments favour firms with strong data capabilities.

The landscape combines a concentrated core of dominant players with a diverse set of smaller, agile competitors, reflecting both consolidation and ongoing fragmentation in niche segments.

The global Programmatic Advertising Market is projected to be valued at US$273.7 Bn in 2026.

The display Ads segment is expected to account for approximately 32.0% of the global Programmatic Advertising Market by Ad Format in 2026.

The market is expected to witness a CAGR of 19.9% from 2026 to 2033.

The Programmatic Advertising Market growth is driven by AI and machine learning integration for real-time targeting, rapid adoption of Connected TV (CTV) and streaming platforms, expansion of digital ad budgets in emerging markets and e-commerce, mobile and multi-channel consumption, and high penetration of programmatic buying across industries.

Key market opportunities in the Programmatic Advertising Market include supply path optimisation, direct programmatic partnerships, growth of private marketplaces (PMPs), equitable access to premium CTV inventory for mid-market advertisers, and standardization of AI-driven workflows with agentic advertising for real-time optimization.

The key players in the Programmatic Advertising market include Alphabet Inc. (Google LLC), Meta, Amazon.com, Inc., Microsoft, The Trade Desk, and Adobe.

| Report Attribute | Details |

|---|---|

| Forecast Period | 2026 to 2033 |

| Historical Data Available for | 2020 to 2025 |

| Market Analysis | USD Million for Value |

| Region Covered |

|

| Key Companies Covered |

|

| Report Coverage |

|

By Buying Type

By Ad Format

By End-user

By Region

Delivery Timelines

For more information on this report and its delivery timelines please get in touch with our sales team.

About Author