- Medical Devices

- Whole Slide Imaging Systems Market

Whole Slide Imaging Systems Market Size, Share, and Growth Forecast 2026 - 2033

Whole Slide Imaging Systems Market by Component (Scanners, Services), by Application (Telepathology, Cytopathology, Immunohistochemistry, Hematopathology), by End User (Hospitals, Diagnostic Laboratories, Research Centers), by Regional Analysis, 2026-2033

Whole Slide Imaging Systems Market Size and Trend Analysis

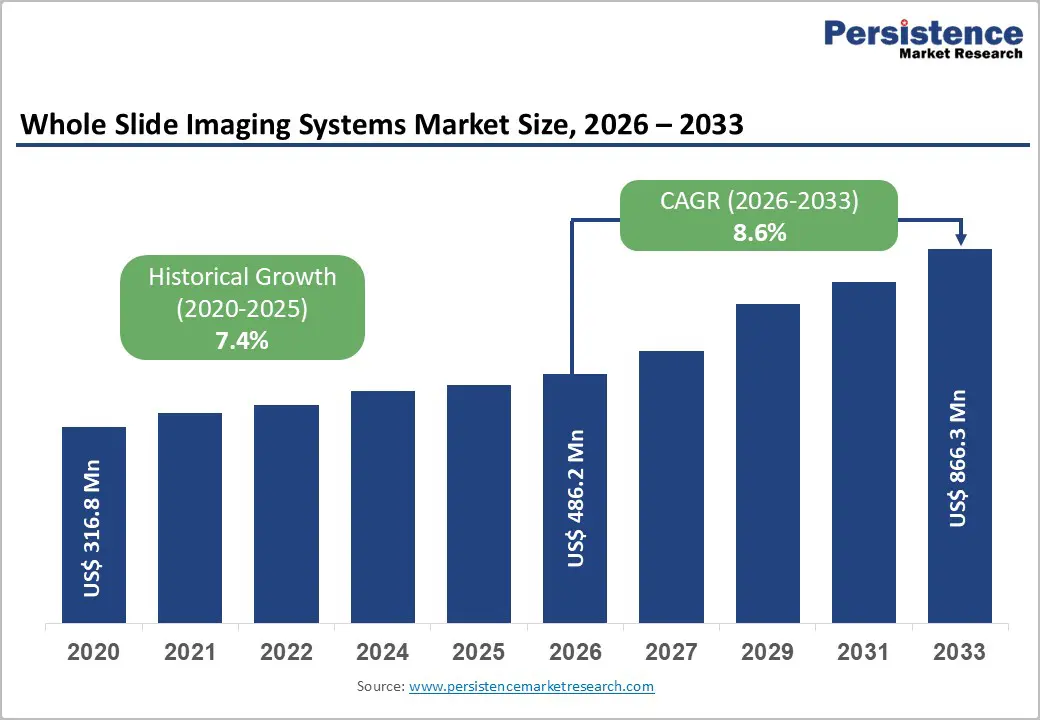

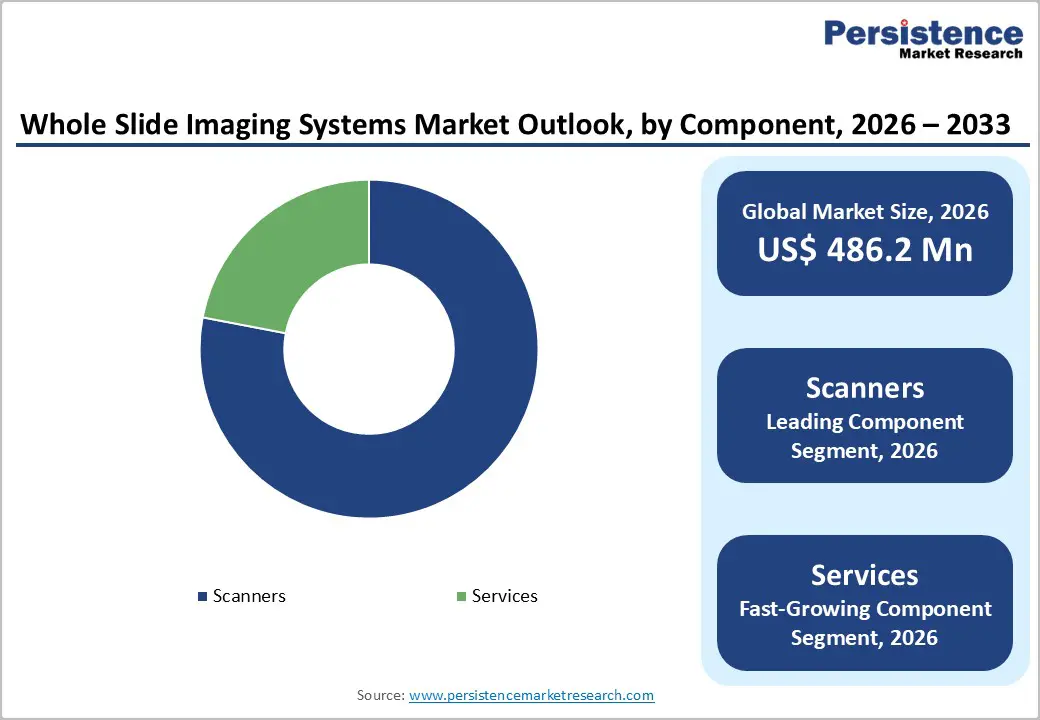

The global whole slide imaging systems market size is expected to be valued at US$ 486.2 million in 2026 and projected to reach US$ 866.3 million by 2033, growing at a CAGR of 8.6% between 2026 and 2033.

Rising demand stems from the need for efficient digital pathology workflows amid increasing cancer cases and pathologist shortages. US Food and Drug Administration (FDA) approvals for primary diagnosis have accelerated adoption, enabling remote consultations and AI integration for faster, accurate diagnostics. Technological advancements in high-throughput scanners further support scalability in high-volume labs.

Key Market highlights

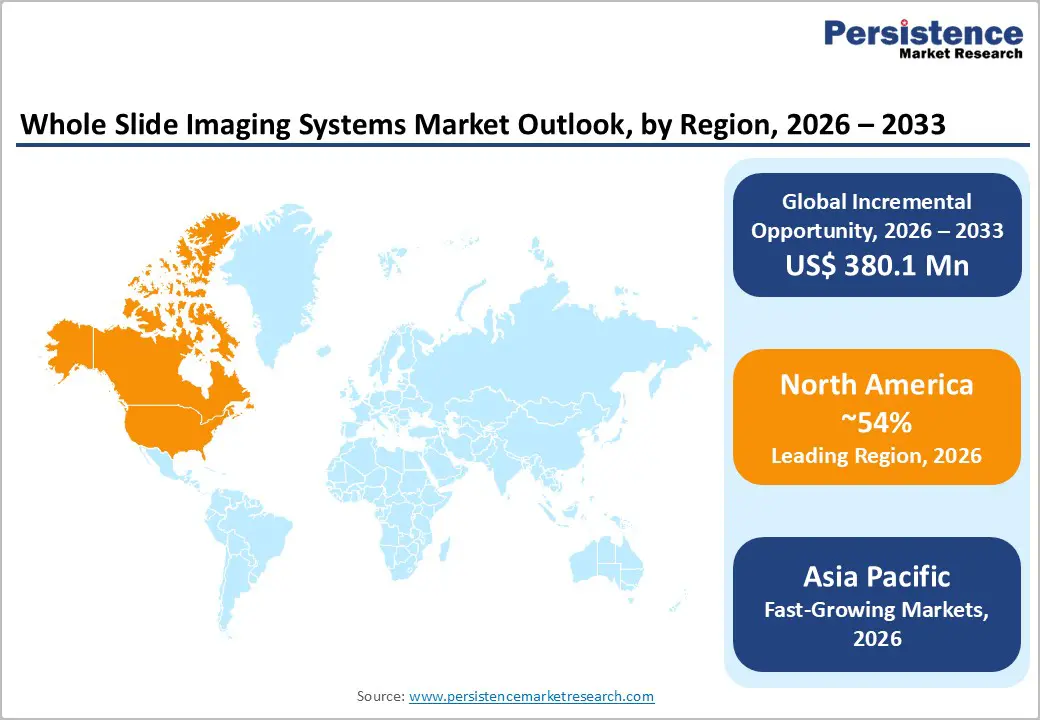

- North America remains the largest region for whole slide imaging systems, driven by advanced healthcare infrastructure, high adoption of digital pathology, strong R&D investments, and supportive regulatory frameworks enabling rapid technology implementation.

- Asia Pacific is expected to grow rapidly, fuelled by increasing cancer prevalence, expanding hospital and laboratory networks, growing investments in healthcare infrastructure, and adoption of digital pathology solutions across China, India, Japan, and Southeast Asia.

- Scanners are projected to hold the largest market share, driven by demand for high-resolution imaging, automation, and digitization of glass slides for clinical and research applications.

- Hospitals and diagnostic laboratories account for the largest value share, providing high-volume slide processing, remote consultations, and efficient workflow management through WSI adoption.

- AI-assisted analysis, digital archiving, and high-throughput imaging platforms offer real-time insights, enabling companies to expand adoption in research centers, pharmaceutical studies, and academic institutions.

| Key Insights | Details |

|---|---|

| Whole Slide Imaging Systems Market Size (2026E) | US$ 486.2 million |

| Market Value Forecast (2033F) | US$ 866.3 million |

| Projected Growth CAGR (2026-2033) | 8.6% |

| Historical Market Growth (2020-2025) | 7.4% |

Market Dynamics

Driver- Advancements in Digital Pathology Integration

Advancements in digital pathology, particularly the integration of whole slide imaging (WSI) with artificial intelligence (AI) and cloud-based platforms, are driving significant growth in the market. Digital pathology solutions enhance diagnostic accuracy, streamline workflow efficiency, and enable pathologists to manage higher caseloads amid global workforce shortages. FDA clearance of systems such as the Philips IntelliSite Pathology Solution in 2017 established regulatory confidence for primary diagnosis, while ongoing AI validation studies report concordance rates exceeding 95% compared to conventional microscopy. High-throughput WSI scanners, capable of processing up to 540 slides per run, reduce turnaround times by up to 30%, particularly in oncology workflows, allowing faster and more efficient patient management in hospitals and diagnostic centers.

The rising global cancer burden further accelerates WSI adoption, as precise, rapid, and reproducible diagnostics become essential for treatment planning. Telepathology applications enable remote consultations, second opinions, and collaborative research across geographies, reducing delays in diagnosis and supporting continuous care during crises such as the COVID-19 pandemic. Academic and research institutions are increasingly adopting WSI for training, teaching, and clinical studies, reinforcing the technology’s utility. Together, these advancements enhance overall clinical efficiency, patient outcomes, and adoption of digital pathology solutions worldwide.

Restraint- High Installation and Maintenance Costs

The high cost of implementing whole slide imaging systems remains a major restraint in the digital pathology market, particularly in developing regions. WSI scanners require significant capital investment, making them inaccessible to many medium-sized laboratories and hospitals. Beyond the initial procurement cost, ongoing expenses for system maintenance, software updates, and consumables add to the financial burden, limiting widespread deployment. Additionally, laboratories must invest in specialized training programs for pathologists and technical staff to effectively utilize these complex platforms, further increasing operational costs.

Smaller institutions and regional diagnostic centers often struggle to justify these high expenditures due to limited budgets and lower patient throughput. Even when infrastructure and technical expertise are available, the need for continuous calibration, data storage solutions, and integration with existing laboratory information systems increases total cost of ownership. These financial barriers slow adoption rates, particularly in regions with constrained healthcare spending, delaying the benefits of digital pathology despite its proven advantages in efficiency, accuracy, and workflow optimization. As a result, high installation and maintenance costs remain a significant challenge for market growth globally.

Opportunity- AI-Driven Image Analysis and Research Applications

AI-driven image analysis and digital pathology applications in research represent a significant growth opportunity for the market. Research centers and pharmaceutical companies increasingly adopt WSI for drug discovery, biomarker identification, and clinical trial validation, which demands high-volume, reproducible, and digitally archived pathology images. Digital pathology solutions streamline image analysis workflows, support large-scale data handling, and enable precise quantification of histopathological features, driving greater efficiency in research operations. Products such as Hamamatsu Photonics’ NanoZoomer S540MD enable high-throughput scanning, meeting the growing needs of pharmaceutical and academic institutions conducting complex clinical trials.

Moreover, the digital archiving of pathology slides enhances long-term data accessibility for retrospective studies, training, and cross-institutional collaboration. AI algorithms can detect subtle morphological patterns, support predictive modeling, and reduce inter-observer variability, improving reliability and consistency in research outcomes. As more research organizations integrate WSI and AI into drug development pipelines, the adoption of advanced digital pathology solutions is expected to rise, creating new revenue streams for vendors. This trend offers a dual benefit: accelerating scientific discovery while expanding the market for AI-enabled digital pathology platforms in both clinical and research settings.

Category-wise Insights

Component Analysis

Scanners are a critical component in whole slide imaging (WSI) systems, driving significant demand due to their role in converting traditional glass slides into high-resolution digital images. As the primary input device in the digital pathology workflow, scanners enable remote access, secure storage, and computational analysis of pathology specimens. Their ability to produce precise, reproducible, and detailed images is essential for clinical diagnosis, telepathology consultations, research applications, and regulatory compliance.

The growing adoption of digital pathology across hospitals, diagnostic laboratories, and research centers has intensified the need for advanced scanners. Healthcare facilities are transitioning from conventional microscopy to digital imaging to enhance diagnostic accuracy, reduce turnaround times, and improve workflow efficiency. Innovations in scanner technology, including ultra-high resolution, rapid scanning speeds, automation features, and integration with AI-powered analysis platforms, are further fueling demand. These improvements allow pathologists to handle larger caseloads, support multi-site collaborations, and facilitate training or teaching applications. As hospitals and laboratories increasingly prioritize quality, efficiency, and remote accessibility, scanner sales continue to rise, solidifying their role as a cornerstone of the WSI market.

End User Analysis

Hospitals are a major end-user segment for whole slide imaging systems, leveraging WSI to improve diagnostic precision, workflow efficiency, and patient management. High patient volumes and complex disease profiles, especially in oncology, necessitate rapid and reliable digital pathology solutions. WSI enables pathologists to access high-resolution slides remotely, share cases for second opinions, and streamline multidisciplinary consultations, which is crucial for timely treatment decisions.

Large hospitals and academic medical centers increasingly integrate WSI into routine diagnostics, particularly for cancer, infectious disease, and histopathology workflows. Investments in high-throughput scanners and automated imaging systems help manage growing workloads while addressing pathologist shortages. Hospitals also adopt WSI for telepathology, training, and teaching, enhancing clinical outcomes and operational efficiency. The focus on digital transformation, precision medicine, and AI integration drives ongoing WSI adoption, making hospitals a leading and fast-growing segment in the market.

Regional Insights

North America Whole Slide Imaging Systems Market Trends and Insights

North America is the largest and most mature market for whole slide imaging (WSI) systems, driven primarily by the U.S. The region benefits from advanced healthcare infrastructure, a high concentration of research and diagnostic laboratories, and a strong regulatory framework that supports the adoption of innovative medical technologies. Rising cancer prevalence and growing demand for precision medicine have increased the need for efficient and accurate pathology solutions. Hospitals, diagnostic laboratories, and academic centers are increasingly deploying WSI systems to enhance diagnostic workflows, support telepathology consultations, and improve case turnaround times.

Additionally, the presence of leading manufacturers and technology providers in the region promotes continuous innovation in scanner resolution, throughput, and digital slide management. Government and private funding for research and development, along with increasing collaboration between healthcare institutions and technology providers, further drive market growth. Adoption is also supported by the integration of WSI systems into clinical trials, education, and training programs. These factors collectively make North America a dominant and highly strategic market for whole slide imaging systems.

Asia Pacific Whole Slide Imaging Systems Market Trends and Insights

The Asia Pacific whole slide imaging systems market is emerging as the fastest-growing region, fueled by rising healthcare investments and increasing demand for advanced diagnostic solutions. Countries such as China, India, Japan, and South Korea are witnessing rapid expansion of hospitals, diagnostic laboratories, and research centers, leading to greater adoption of WSI systems. The growing prevalence of cancer and other chronic diseases in the region has increased the need for accurate pathology diagnosis and workflow optimization. Additionally, governments in several countries are promoting healthcare modernization, improving laboratory infrastructure, and supporting digital pathology initiatives, which further drive market penetration.

Regional growth is also supported by increasing collaborations between local distributors and global technology providers, facilitating access to high-resolution scanners and imaging platforms. Academic and research institutions are integrating WSI systems for education, clinical trials, and biomarker research, enhancing the demand for digital pathology solutions. The affordability of labor and expanding middle-class populations in developing countries contribute to the adoption of cost-effective WSI platforms. Collectively, these trends position the Asia Pacific region as a high-growth opportunity for whole slide imaging system vendors over the forecast period.

Competitive Landscape

Market Structure Analysis

The whole slide imaging (WSI) systems market is highly competitive and moderately consolidated, dominated by several large global players. Companies are actively pursuing mergers, acquisitions, and strategic partnerships to expand product portfolios, enhance technological capabilities, and increase market share. Investments in research and development focus on high-throughput scanners, AI integration, and automation to meet growing clinical and research demands. Pharmaceutical and biotech firms are significant contributors, adopting WSI for drug discovery, biomarker studies, and clinical trial pathology. Continuous innovation, regulatory compliance, and expansion into emerging markets shape the competitive landscape, driving growth and encouraging new entrants in this evolving industry.?

Key Market Developments

- In May 2024, Indica Labs received FDA 510(k) clearance for HALO AP Dx, supporting primary diagnosis of FFPE surgical slides scanned with Hamamatsu’s NanoZoomer S360MD scanner.

- In April 2024, Standard BioTools launched new solutions for the Hyperion XTi Imaging System, enhancing automation and flexibility in Imaging Mass Cytometry to accelerate discoveries in human health research.

Companies Covered in Whole Slide Imaging Systems Market

- Perkin Elmer Inc

- Inspirata Inc.

- Koninklijke Philips NV

- Spectra AB

- Ventana Medical Systems Inc

- Leica Biosystems Nussloch GmbH (Danaher Corporation)

- Olympus Corporation

- ZEISS International

- Hamamatsu Photonics KK

- ISTECH Ltd

- Others

Frequently Asked Questions

The global market is expected to reach US$ 486.2 million in 2026.

Integration of AI and cloud-based platforms, rising cancer incidence, telepathology adoption, and high-throughput WSI improving diagnostic accuracy and workflow efficiency.

North America leads with 54% share in 2025, supported by regulatory clearances and infrastructure.

AI-driven image analysis and digital pathology for research, drug discovery, and biomarker studies offer significant growth potential in clinical and pharma sectors.

Perkin Elmer Inc, Inspirata Inc., Koninklijke Philips NV, and Spectra AB are among the top players in the maarket.