- Medical Devices

- Vitreoretinal Surgery Devices Market

Vitreoretinal Surgery Devices Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Vitreoretinal Surgery Devices Market by Product (Vitreoretinal Packs, Vitrectomy Machines, Vitrectomy Probes, and Others), by Surgery (Posterior Vitreoretinal Surgery, and Anterior Vitreoretinal Surgery) Application (Retinal Detachment, Diabetic Eye Disease, Macular Holes, Vitreous Hemorrhage, and Others) End-user (Hospitals, Ophthalmology Clinics, and Ambulatory Surgery Centers), and Regional Analysis from 2026 to 2033

Vitreoretinal Surgery Devices Market Share and Trends Analysis

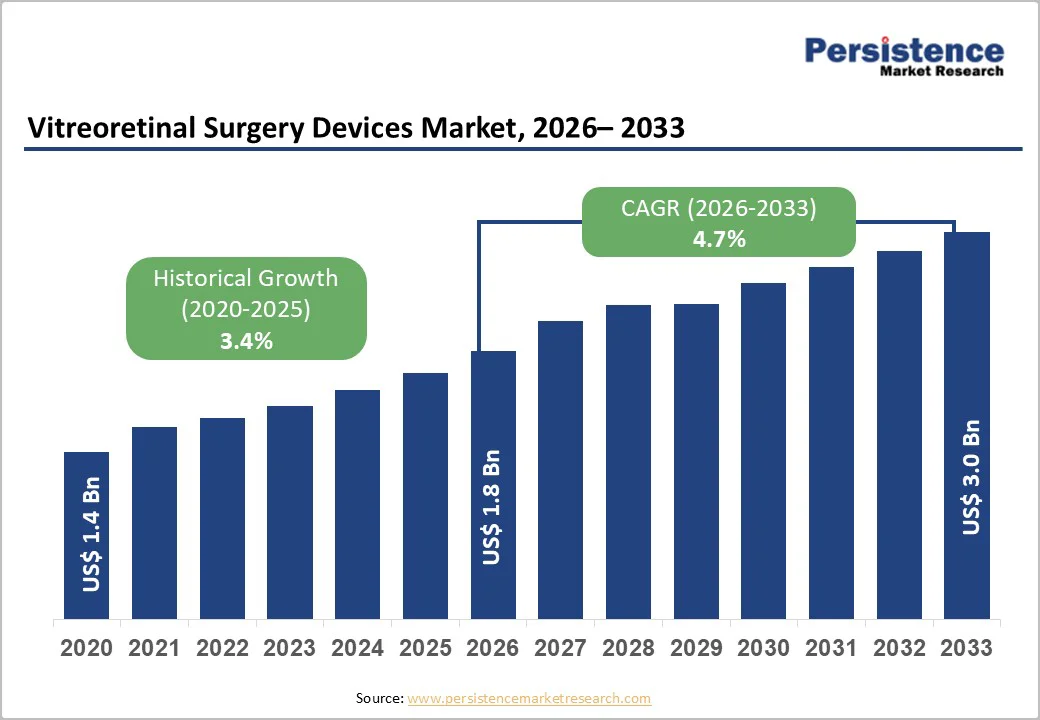

The global vitreoretinal surgery devices market size is estimated to grow from US$ 1.8 billion in 2026 to US$ 3.0 billion by 2033. The market is projected to record a CAGR of 4.7% from 2026 to 2033.

Global demand for vitreoretinal surgery devices is rising rapidly, driven by the increasing prevalence of retinal disorders such as diabetic retinopathy, retinal detachment, macular holes, and age-related macular degeneration. Growing awareness of early diagnosis, rising screening programs, and the global shift toward minimally invasive 25G-27G micro-incision vitrectomy techniques are accelerating market adoption.

Key Industry Highlights

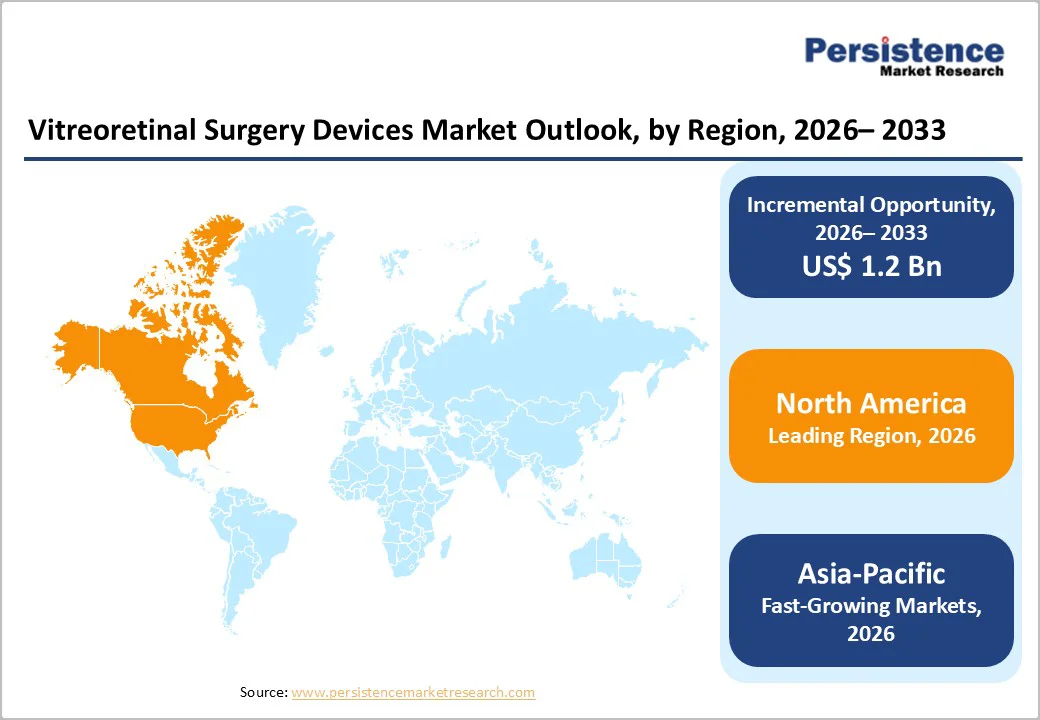

- Leading Region: North America holds the largest share at 44.4%, supported by high surgical volumes, advanced ophthalmic infrastructure, strong adoption of next-generation vitrectomy systems, and rapid integration of OCT-guided and AI-enabled technologies.

- Fastest-Growing Region: Asia Pacific is expanding at the fastest pace, driven by rising diabetic populations, increasing retinal disease burden, higher healthcare spending, and rapid adoption of micro-incision vitrectomy systems across emerging healthcare markets.

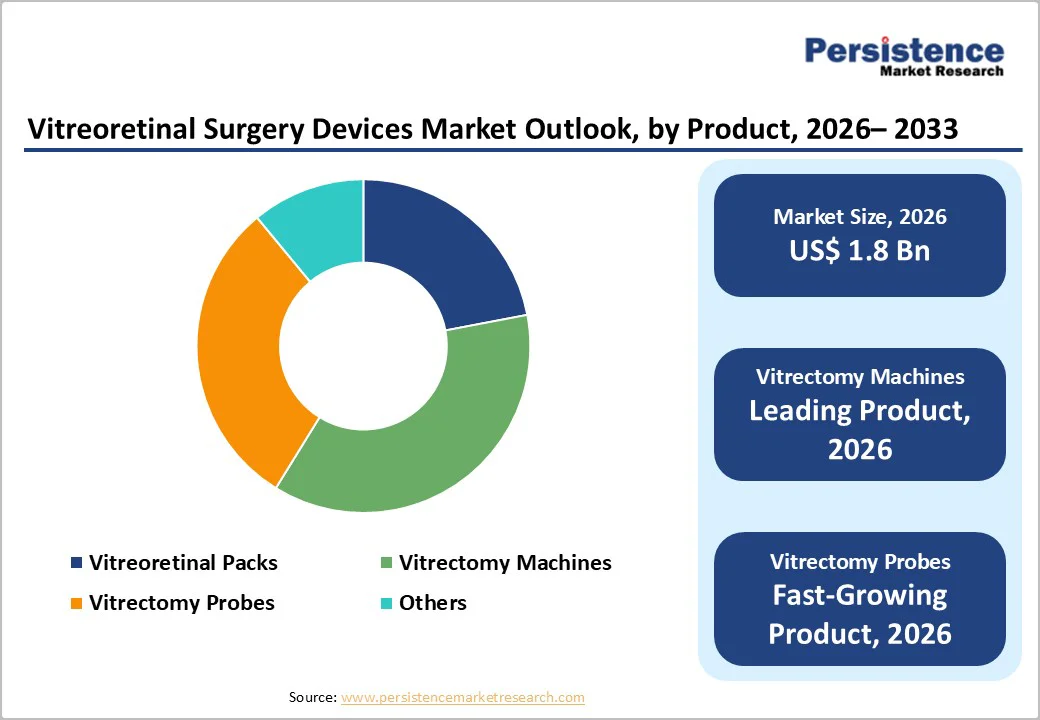

- Leading Product Segment: Vitrectomy machines dominate the market due to their critical role in nearly all vitreoretinal procedures and continuous upgrades in fluidics, cutter control, and visualization integration.

- Fastest-Growing Product Segment: Vitrectomy probes are expanding the fastest owing to increasing use of 25G-27G high-speed, single-use probes and growing preference for minimally invasive retinal surgeries.

- Leading Surgery Segment: Posterior vitreoretinal surgery leads globally because most high-volume procedures, such as retinal detachment repair, diabetic vitrectomy, macular hole surgery, and epiretinal membrane removal are performed in the posterior segment.

- Fastest-Growing Surgery Segment: Anterior vitreoretinal surgery is scaling rapidly as surgeons increasingly address complex anterior segment complications, trauma cases, and device-related issues using minimally invasive approaches.

| Key Insights | Details |

|---|---|

| Vitreoretinal Surgery Devices Market Size (2026E) | US$ 1.8 Bn |

| Market Value Forecast (2033F) | US$ 3.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.4% |

Market Dynamics

Driver - Rising Retinal Disease Burden and Advancements in Minimally Invasive Vitreoretinal Technologies

The global rise in retinal disorders, particularly diabetic retinopathy, age-related macular degeneration (AMD), retinal detachment, and macular holes, is significantly increasing the demand for vitreoretinal surgeries and driving the market growth.

For instance, according to Ocular Therapeutix, Inc., more than 410 million people worldwide are affected by retinal diseases, highlighting the growing demand for advanced vitreoretinal procedures and device adoption across hospitals and specialty ophthalmic centers.

Expanding diabetic populations, longer life expectancy, and growing screening programs are leading to earlier detection and higher surgical intervention rates. As more patients present with vision-threatening complications, procedure volumes continue to rise across hospitals, ophthalmic clinics, and ambulatory surgical centers.

Rapid innovation in minimally invasive vitrectomy platforms, including 25G-27G micro-incision systems, ultra-high-speed cutters, advanced fluidics control, and intraoperative OCT-based visualization, is transforming surgical outcomes.

These technologies allow precise tissue handling, reduced trauma, shorter operating times, and faster patient recovery. Improved device reliability and expanded surgical indications, ranging from complex diabetic vitrectomies to delicate macular procedures, are accelerating adoption worldwide.

Restraints - High Cost Barriers, Reimbursement Gaps, and Shortage of Skilled Vitreoretinal Surgeons

The high capital costs of next-generation vitrectomy platforms, imaging systems, and single-use disposables significantly constrain the adoption of advanced vitreoretinal surgery devices. Smaller hospitals and outpatient centers, particularly in developing regions, often face budget constraints that limit their ability to adopt new technology.

Additionally, reimbursement variability across countries with inconsistent coverage for retinal procedures and consumables creates financial uncertainty for providers, reducing investment incentives and slowing technology penetration.

Moreover, the shortage of trained vitreoretinal surgeons is due to the fact that the specialty requires extensive fellowship training and advanced surgical skill. Many regions, especially low- and middle-income markets, lack structured vitreoretinal training programs, leading to slower adoption of modern surgical systems.

This skills gap restricts the number of procedures performed, delays patient access to sight-saving surgery, and ultimately hinders broader market expansion despite growing clinical need.

Opportunity - Emerging Digital Technologies and Next-Generation Surgical Innovations

The growing integration of AI-driven retinal screening, tele-ophthalmology platforms, and automated referral systems is enabling earlier detection of diabetic retinopathy, macular disorders, and other vision-threatening conditions.

These technologies improve patient triage, expand access in underserved regions, and drive higher volumes of timely surgical referrals. As healthcare systems adopt remote diagnostics and cloud-based imaging analytics, demand for vitreoretinal procedures is expected to rise, strengthening long-term device utilization and propelling market growth.

Furthermore, manufacturers are introducing smaller-gauge, single-use instruments, micro-incision procedure kits, robotic-assisted systems, and advanced intraoperative OCT guidance. These innovations enhance surgical precision, shorten operating times, and improve overall clinical outcomes, making them particularly appealing to high-end ophthalmic centers.

Robotic and imaging-enhanced platforms further strengthen performance differentiation, and together these advancements are driving broader technology adoption and creating growth opportunities across both developed and emerging regions.

Category-wise Analysis

By Product, Vitrectomy Machines Dominate Globally Due to Their Central Role in All Vitreoretinal Surgical Procedures

The vitrectomy machines segment is projected to dominate the global vitreoretinal surgery devices market in 2026, accounting for 36.8% of revenue. The segment’s strong performance is driven primarily by the essential role these systems play as the core platform for vitreoretinal surgical procedures, including retinal detachment repair, diabetic vitrectomy, macular hole treatment, and vitreous hemorrhage management.

Modern vitrectomy consoles integrate advanced fluidics, dual-pneumatic cutters, high-speed probe control, and real-time intraoperative OCT, enabling greater precision, stability, and safety, making them indispensable in both routine and complex surgeries. The growing prevalence of diabetic retinopathy and macular disorders supports rising procedure volumes.

Additionally, favorable reimbursement, continuous product innovation by leading players, and the expansion of ambulatory surgical centers adopting compact consoles boost the market growth.

By Application, Retinal Detachment Leads the Market Globally Due to Its High Surgical Incidence and Urgent Treatment Requirement

The retinal detachment segment is projected to dominate the global vitreoretinal surgery devices market in 2026, accounting for a revenue share of 41.5%, driven by its high clinical urgency, rising global incidence, and the critical need for immediate surgical intervention to prevent permanent vision loss.

Rhegmatogenous, tractional, and complex detachments are rising worldwide, driven by aging populations, high myopia prevalence, ocular trauma, and complications associated with diabetic retinopathy.

These cases require advanced vitrectomy machines, high-speed cutters, fluidics control systems, endoillumination, perfluorocarbon liquids, and retinal tamponade agents, significantly boosting device utilization. Hospitals and specialized ophthalmic centers continue to report growing surgical volumes, supported by enhanced imaging techniques and early disease detection.

By End-user, Hospitals Dominate Globally Due to Their Advanced Infrastructure and High Volume of Complex Retinal Procedures

The hospitals segment is projected to dominate the global vitreoretinal surgery devices market in 2026, accounting for a revenue share 52.7%. This is driven by their advanced clinical infrastructure, broad procedural capacity, and strong adoption of next-generation vitrectomy technologies.

Hospitals perform the majority of complex retinal interventions, including retinal detachment repair, diabetic vitrectomy, macular hole surgery, and epiretinal membrane removal, which require high-precision instruments, intraoperative OCT, hybrid illumination systems, and premium vitrectomy consoles.

Their ability to manage high-risk patients, provide multidisciplinary care, and handle surgical complications further solidifies their leadership. Tertiary care and specialty ophthalmic hospitals also benefit from greater capital budgets, allowing faster procurement of 25G-27G micro-incision systems, high-speed cutters, advanced fluidics platforms, and visualization upgrades.

Strong reimbursement coverage for hospital-based procedures, combined with rising inpatient and day-care retinal surgeries, continues to boost market growth.

Region-wise Insights

North America Vitreoretinal Surgery Devices Market Trends

The North America market is expected to dominate globally with a value share of 44.4% in the 2026, with the U.S. leading the region due to its strong clinical infrastructure, high surgical volumes, and rapid adoption of next-generation retinal technologies.

The region has one of the highest diagnosed rates of diabetic retinopathy, retinal detachment, and age-related macular degeneration, supported by extensive screening programs and a large aging population. This drives sustained demand for advanced vitrectomy systems, dual-blade cutters, hybrid illumination platforms, and intraoperative OCT-guided visualization.

The region also benefits from the presence of leading manufacturers, including Alcon, Bausch + Lomb, ZEISS, and DORC, as well as frequent FDA approvals and early availability of technologically advanced platforms. Strong reimbursement coverage for retinal procedures, combined with the expansion of ambulatory surgical centers specializing in ophthalmology, further boosts device utilization.

Europe Vitreoretinal Surgery Devices Market Trends

The Europe market is expected to grow steadily, driven by the region’s strong healthcare infrastructure, increasing burden of age-related retinal disorders, and rapid adoption of advanced micro-incision vitrectomy systems.

Countries such as Germany, the U.K., France, Italy, and Spain are witnessing a rising prevalence of diabetic retinopathy, macular degeneration, retinal detachment, and epiretinal membrane disorders, supported by expanding diabetic and geriatric populations. This is increasing the number of vitreoretinal procedures performed annually across specialized ophthalmic centers.

Europe’s strong regulatory environment, including CE-certified surgical innovations, promotes faster market penetration of next-generation vitrectomy consoles, dual-pneumatic cutters, enhanced fluidics systems, and OCT-integrated visualization platforms. Growing emphasis on minimally invasive procedures, improved surgical outcomes, and surgeon-friendly ergonomics is further accelerating device replacement cycles.

Asia Pacific Vitreoretinal Surgery Devices Market Trends

Asia Pacific is expected to register a relatively higher CAGR of around 6.3% between 2026 and 2033, driven by demographic, technological, and healthcare infrastructure developments across the region.

A rapidly growing elderly population, particularly in China, Japan, South Korea, and India, is contributing to a higher incidence of diabetic retinopathy, retinal detachment, macular holes, and age-related macular degeneration conditions that require surgical intervention.

The expansion of national screening programs for diabetes and ophthalmic disorders is further enabling earlier disease detection, increasing surgical volumes.

Improved access to advanced retinal surgical systems, increased adoption of micro-incision vitrectomy technologies (25G-27G), and the growing penetration of ambulatory surgical centers are driving market growth. Medical tourism in India, Thailand, and Singapore is also driving high-complexity ophthalmic procedures at comparatively lower costs.

Competitive Landscape

The global vitreoretinal surgery devices market is highly competitive, led by companies such as Alcon, Inc., Dutch Ophthalmic Research Center International B.V., Bausch & Lomb Incorporated, Geuder AG, and ZEISS supported by broad surgical portfolios, strong ophthalmic distribution networks, and continuous innovation in minimally invasive retinal surgery platforms.

Market players are focusing on 27G-29G micro-incision vitrectomy systems, high-speed cutters, and advanced intraoperative OCT-guided visualization technologies to improve precision, reduce surgical trauma, and accelerate patient recovery.

Manufacturers are also moving toward AI-backed surgical visualization, pneumatic and dual-blade cutter upgrades, and integrated fluidics control systems to strengthen clinical outcomes and differentiate device performance during complex retinal procedures.

Additionally, companies are investing in portable vitrectomy consoles, endoillumination upgrades (LED/laser-based), single-use instrument kits, and surgeon-friendly ergonomics to expand access across ambulatory surgical centers and emerging markets.

Key Industry Developments:

- In September 2025, BVI, a global ophthalmic device leader, announced the European launch of Virtuoso®, its next-generation phaco-vitrectomy surgical platform. Designed as a dual-function system for both cataract and vitreoretinal procedures, Virtuoso® integrates advanced technologies to enhance surgical efficiency, precision, and workflow.

- In September 2025, Oertli introduced the OS 4 Up, its next-generation surgical platform designed for both cataract and vitreoretinal procedures. Developed and manufactured in Switzerland, the OS 4 Up focuses on enhancing precision, control, and workflow efficiency for surgeons and operating-room teams.

- In April 2025, Alcon announced the launch of the UNITY® Vitreoretinal Cataract System (VCS) and UNITY® Cataract System (CS), a new dual-configuration surgical platform designed to enhance efficiency in both vitreoretinal and cataract procedures. The platform offers a combined console (VCS) and a standalone cataract system (CS), integrating several first-to-market technologies such as UNITY 4D Phaco, HYPERVIT® 30K, and the UNITY Intelligent Fluidics system.

Companies Covered in Vitreoretinal Surgery Devices Market

- Alcon, Inc.

- Dutch Ophthalmic Research Center International B.V.

- Bausch & Lomb Incorporated

- Geuder AG

- ZEISS

- Hooya Corporation

- Lumibird Medical

- Elektromedizin GmbH

- Medical Instrument Development Laboratories, Inc.

- Iscon Surgicals Ltd.

- HASA OPTIX SRL

- Microtrack Surgicals

- Others

Frequently Asked Questions

The global vitreoretinal surgery devices market is projected to be valued at US$ 1.8 Bn in 2026.

Rising retinal disease prevalence, advancements in minimally invasive vitrectomy technologies, expanding surgical infrastructure, and increasing early diagnosis and treatment rates are driving the global vitreoretinal surgery devices market.

The global vitreoretinal surgery devices market is poised to witness a CAGR of 4.7% between 2026 and 2033.

AI-enabled screening, growth of minimally invasive vitrectomy systems, rising adoption of single-use instruments, and expanding access to advanced retinal care in emerging markets are creating opportunities in the market.

Alcon, Inc., Dutch Ophthalmic Research Center International B.V., Bausch & Lomb Incorporated, Geuder AG, and ZEISS are some of the key players in the vitreoretinal surgery devices market.