- Specialty & Fine Chemicals

- Polyester Polyols Market

Polyester Polyols Market Size, Share, and Growth Forecast, 2025 - 2032

Polyester Polyols Market By Product Type (Aliphatic Polyester Polyols, Aromatic Polyester Polyols), Source (Petroleum-Based, Bio-Based), Application, and Regional Analysis for 2025 - 2032

Polyester Polyols Market Size and Trends Analysis

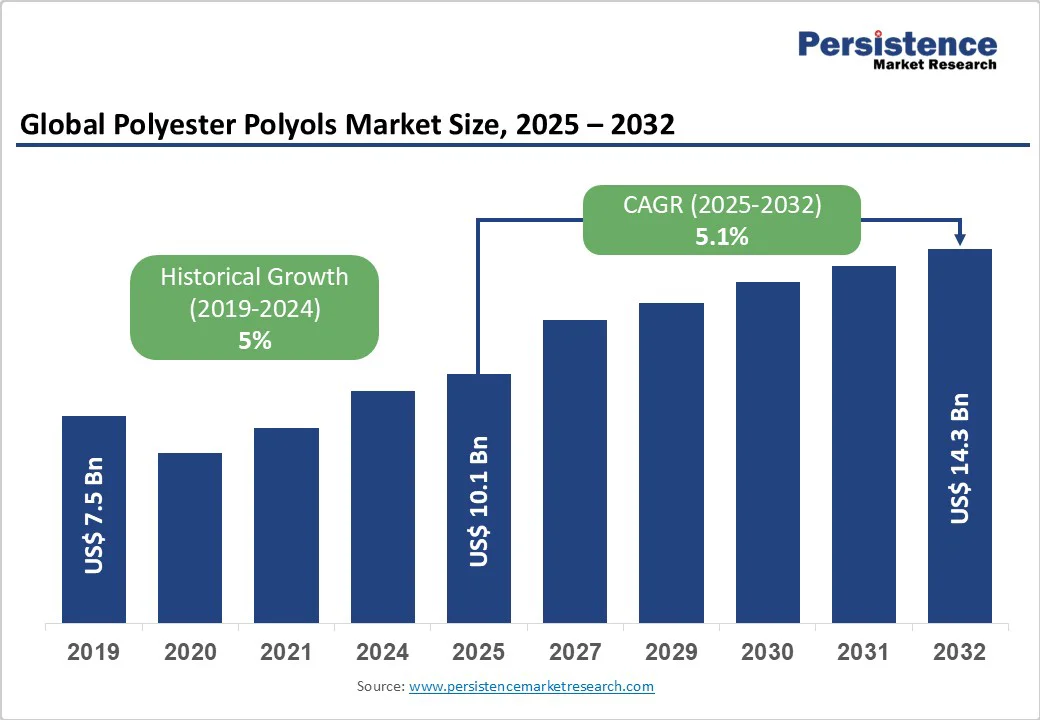

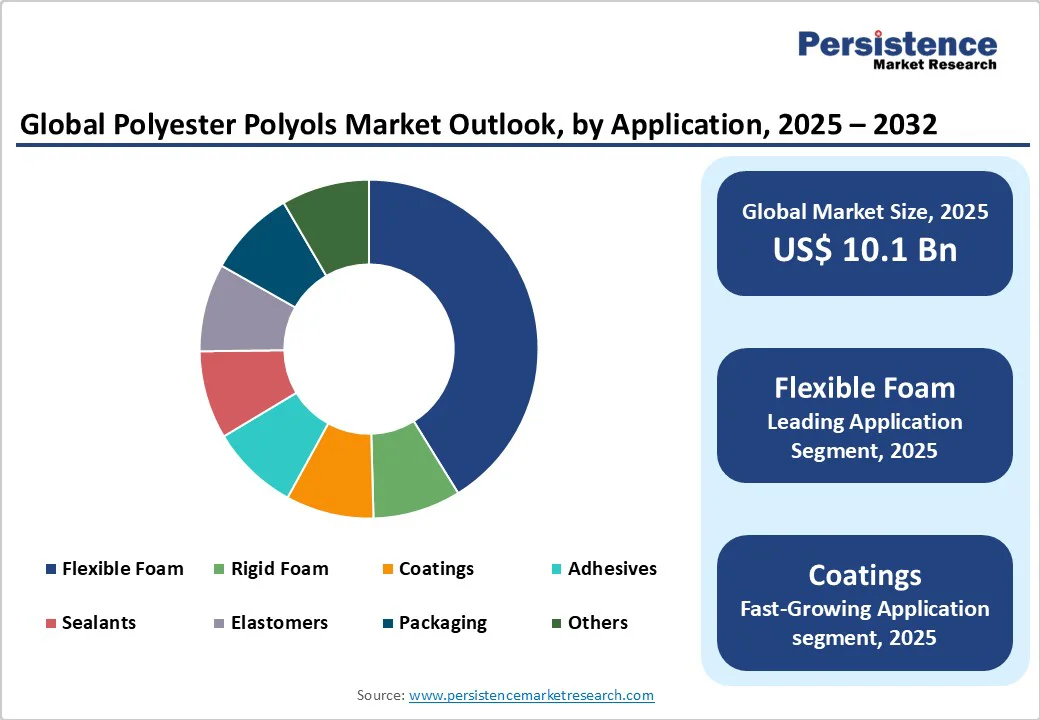

The global polyester polyols market size is likely to be valued at US$10.1 Billion in 2025 and is expected to reach US$14.3 Billion by 2032, growing at a CAGR of 5.1% during the forecast period from 2025 to 2032, driven by increasing consumption of polyester polyols in rigid and flexible polyurethane foams, as well as coatings, adhesives, sealants, and elastomers (CASE) applications. High tensile strength, chemical resistance, and thermal stability are driving material adoption across automotive, construction, and electronics sectors.The global polyester polyols market size is likely to be valued at US$10.1 Billion in 2025 and is expected to reach US$14.3 Billion by 2032, growing at a CAGR of 5.1% during the forecast period from 2025 to 2032, driven by increasing consumption of polyester polyols in rigid and flexible polyurethane foams, as well as coatings, adhesives, sealants, and elastomers (CASE) applications. High tensile strength, chemical resistance, and thermal stability are driving material adoption across automotive, construction, and electronics sectors.

Key Industry Highlights

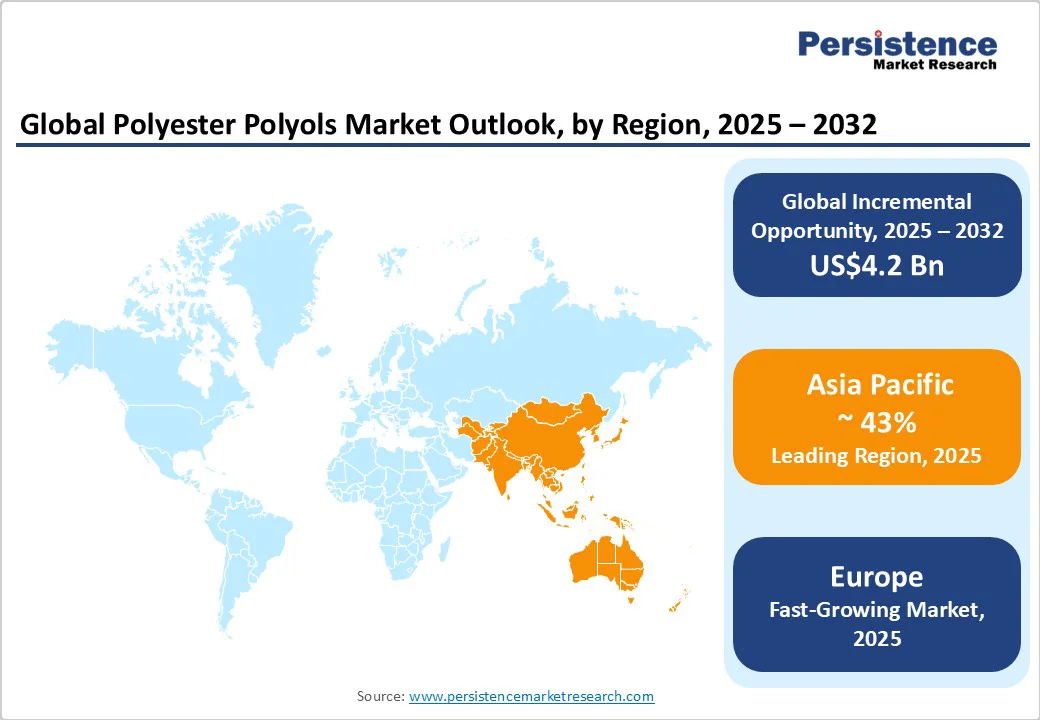

- Leading Region: Asia Pacific accounts for 43% of global market revenue, driven by China, India, Japan, and ASEAN industrial growth.

- Fastest-Growing Region: Europe, led by the sustainability-driven adoption of bio-based and low-VOC polyols.

- Investment Plans: Significant expansions in Asia Pacific and North America, including bio-based and specialty polyol plants by BASF, Huntsman, and Covestro.

- Dominant Product Type: Aliphatic polyester polyols hold the largest market share at 58% of revenue due to superior UV stability and high-performance coatings applications.

- Leading Application: Flexible foam consumes over 49% of total polyester polyol volumes, with rigid foams used in insulation and flexible foams in furniture and automotive interiors.

| Key Insights | Details |

|---|---|

|

Polyester Polyols Market Size (2025E) |

US$10.1 Bn |

|

Market Value Forecast (2032F) |

US$14.3 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

5.1% |

|

Historical Market Growth (CAGR 2019 to 2024) |

5% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising Construction and Insulation Demand

Growing awareness of energy conservation and new building codes are spurring demand for polyurethane insulation panels made with polyester polyols. Government-led programs focused on retrofitting and energy-efficient housing are significantly increasing the need for high-performance insulation materials. The construction industry’s shift toward sustainable and lightweight materials directly supports growth in rigid polyurethane foams. This trend contributes to stable, long-term demand for polyester polyols used in thermal insulation, roofing, and panel applications.

Automotive Lightweighting and Interior Comfort

Automotive manufacturers are increasingly substituting heavier materials with polyurethane-based components to reduce overall vehicle weight and improve fuel efficiency. Polyester polyols, valued for their mechanical durability and superior heat resistance, are vital in producing seat cushions, headrests, sound insulation, and coatings. The global transition to electric vehicles further boosts demand for lightweight insulation materials that support battery performance and safety. Expanding EV production and stringent emissions regulations are key growth multipliers across major automotive economies.

Technological Shift toward Bio-Based Feedstocks

Advances in bio-refining and polymer chemistry are introducing new bio-based diols and glycols, enabling the production of sustainable polyester polyols. Companies are investing heavily in renewable raw materials such as bio-MEG and bio-MPG, which align with corporate sustainability goals and emerging environmental legislation. This transition opens premium opportunities in food-grade packaging and consumer goods where eco-certification drives purchasing decisions. As bio-based polyols reach commercial scale, cost competitiveness improves, and regulatory compliance strengthens their long-term viability.

Barrier Analysis - Feedstock Price Volatility

Volatile petrochemical feedstock prices continue to pressure polyester polyol producers. The industry’s dependence on raw materials such as diacids and glycols, which are derived from crude oil, results in fluctuating production costs. Periods of high crude oil prices have historically compressed margins and delayed planned capacity expansions. Feedstock volatility poses a consistent risk to profitability, particularly for producers without backward integration or long-term raw-material contracts.

Competitive Pressure from Polyether Polyols

Polyether polyols maintain a dominant position in many polyurethane applications due to lower cost and wider supply availability. This competitive pressure constrains polyester polyols in price-sensitive end uses such as flexible foams. While polyester polyols outperform in mechanical strength and heat resistance, market substitution toward polyether or recycled alternatives is common when performance requirements are moderate. To sustain competitiveness, polyester polyol producers must focus on differentiation through quality, specialty formulations, and technical service.

Growth of Bio-Based and Circular Polyols

Global sustainability policies and consumer preference shifts are creating a substantial growth window for bio-based polyester polyols. Manufacturers adopting renewable glycols and integrating recycling technologies can target high-margin applications in packaging, construction, and coatings. The opportunity for certified bio or recycled polyester polyols is estimated at an additional US$1.5–2.5 Billion by 2032. Producers that invest early in certification and traceable supply chains stand to secure long-term offtake contracts from major industrial users.

Expansion in CASE Applications

Polyester polyols’ superior performance characteristics make them ideal for coatings, adhesives, sealants, and elastomers. Demand for high-durability coatings in electronics, industrial machinery, and automotive components continues to rise. This segment is growing faster than the overall market and is expected to account for nearly one-fourth of global polyester polyol revenues by 2032. High resistance to chemicals, UV radiation, and abrasion enhances product value, encouraging formulators to shift toward polyester-based systems.

Category-wise Analysis

Product Type Insights

Aliphatic polyester polyols are anticipated to hold a dominant market share, accounting for approximately 58% of the total revenue in 2025. Their strong UV resistance, weatherability, and non-yellowing properties make them the preferred choice for exterior architectural coatings, industrial paints, and automotive finishes. For example, aliphatic polyols are extensively used in premium automotive topcoats, where long-term color stability and resistance to environmental degradation are critical. In construction, aliphatic polyester polyols are used in high-performance flooring and exterior coatings requiring durability and chemical resistance. Their long-term reliability enables manufacturers to command premium pricing and sustain strong margins.

Aromatic polyester polyols are forecast to be the fastest-growing segment, driven by cost efficiency and mechanical strength in applications such as flexible and rigid foams, adhesives, and sealants. For instance, aromatic polyols are increasingly used in furniture foams for mattresses and upholstered seating due to their superior load-bearing properties and elasticity. Rapid capacity expansions in China, Taiwan, and India are enhancing the availability of these grades to regional markets. Industrial adhesives and protective coatings in the electronics and packaging sectors are increasingly using aromatic polyols for their superior tensile strength and chemical resistance. Rising construction and furniture demand in emerging economies further positions aromatic polyester polyols as a high-volume growth opportunity through 2032.

Application Insights

Flexible foams constitute the largest application segment, consuming over 49% of total polyester polyol volumes. Flexible foams are found in mattresses, furniture cushions, and automotive seating, where comfort, resilience, and durability are key performance factors. For example, flexible foam cores in automotive seating help reduce weight without compromising comfort. The steady growth of the construction, furniture, and automotive sectors, particularly in North America and Asia Pacific, ensures sustained baseline demand and predictable volume growth for foam applications.

Coatings are projected to be the fastest-growing segment of the polyester polyols market. Growth is driven by rising demand for high-performance, chemically resistant, and low-VOC coatings across automotive, industrial, and electronics sectors. For example, in automotive interiors, polyester-based coatings enhance scratch resistance and durability on dashboards and panels. In industrial machinery, protective coatings prevent corrosion and thermal degradation, while in electronics, specialty coatings protect sensitive components from moisture and heat.

Regional Insights

Asia Pacific Polyester Polyols Market Trends - Industrial Scale and Renewable Push Cement Global Leadership

Asia Pacific is the largest regional market, accounting for nearly 43% of global polyester polyol revenue in 2025. The region is both the leading producer and consumer, with China and India driving demand through rapid industrialization, construction, and growth in the automotive and furniture sectors. The expansion of rigid polyurethane foams in insulation panels for cold storage, residential construction, and refrigeration is a primary factor behind volume growth.

Japan and South Korea focus on high-performance specialty polyols for electronics, automotive coatings, and industrial adhesives. For example, Japan’s Mitsui Chemicals and LG Chem in South Korea are investing in advanced aromatic and aliphatic polyols tailored for electronics packaging and premium automotive interior applications. ASEAN countries leverage cost-competitive production and growing domestic demand, making them attractive hubs for new capacity.

Asia Pacific remains the key growth hub for polyester polyols, supported by green manufacturing incentives and major expansions like Huntsman’s Taiwan plant and BASF’s Shanghai complex. Cost advantages, manufacturing scale, and rising demand from construction and automotive sectors, alongside renewable feedstock investments, reinforce the region’s leadership through 2032.

Europe Asia Pacific Polyester Polyols Market Trends - Circular Economy and Bio-Based Polyols Lead Sustainable Shift

Europe serves as a leader in sustainability-driven chemical innovation. Germany remains the dominant producer, leveraging its advanced chemical infrastructure and industrial manufacturing base. Other key countries, the U.K., France, and Spain, show strong growth in construction and coatings applications, particularly in low-VOC architectural paints and high-performance industrial coatings.

Regulatory frameworks, including the European Green Deal, REACH regulations, and Packaging Waste Directives, are accelerating the adoption of bio-based and recycled polyester polyols. Companies such as Covestro and UPM Biochemicals are expanding bio-based polyol production in Germany and Finland to meet growing demand. For instance, UPM Biochemicals’ large-scale bio-MEG plant in Leuna is supplying renewable glycols for polyurethane production across the EU, supporting both coatings and rigid foam applications. Europe’s growth is also fueled by circular economy initiatives.

Polyol manufacturers are partnering with recycling firms to develop closed-loop systems, turning PET and other polymer waste into feedstock for polyester polyols. Even with moderate volume growth, the focus on high-performance, compliant materials ensures strong value gains. Emerging opportunities include green construction materials, sustainable automotive interior components, and specialty CASE applications, particularly in Germany and France.

North America Asia Pacific Polyester Polyols Market Trends - EV Growth and Green Building Codes Drive Polyol Innovation

North America is primarily supported by stringent energy-efficiency and building codes, which increase the adoption of rigid polyurethane foams in insulation panels, roofing systems, and refrigeration applications. Renovation activity in both commercial and residential sectors, coupled with urbanization, fuels consistent demand. The automotive sector is another significant driver. Lightweighting initiatives and the rapid expansion of electric vehicle (EV) production are encouraging the use of high-performance polyurethane foams and coatings in seats, interiors, and battery casings.

For example, manufacturers such as Dow and BASF are supplying specialty polyester polyols for EV battery insulation and automotive adhesives, reflecting the sector’s technological focus. North America’s innovation ecosystem is strengthened by extensive R&D investment from chemical majors.

Companies are developing low-VOC, recyclable, and bio-based polyols in response to environmental regulations enforced by agencies, including the EPA and DOE. Recent developments include BASF’s expansion of its U.S. polyol plant in Geismar, Louisiana, aimed at producing bio-based polyols for sustainable coatings and foam applications. These efforts enhance compliance with emerging sustainability standards while enabling premium product offerings.

Competitive Landscape

The global polyester polyols market is moderately fragmented, characterized by a mix of global chemical corporations and specialized regional producers. Leading multinationals such as BASF, Dow, Covestro, Huntsman, and Evonik collectively command a significant portion of global revenue. Smaller players and regional formulators serve niche applications in coatings and adhesives. The market is more consolidated in North America and Europe, where integration across feedstock and downstream polyurethane systems is high. Competition increasingly centers on sustainability credentials, supply security, and technological differentiation.

Market leaders are focusing on vertical integration, sustainability initiatives, and innovation in specialty formulations. Strategic themes include expanding bio-based production, enhancing regional manufacturing footprints, and developing customized polyols for high-value CASE applications. Collaboration with renewable feedstock suppliers and investment in low-carbon processes are becoming central competitive differentiators.

Key Industry Developments

- In August 2025, Algenesis Labs introduced Soleic®, a novel polyester aromatic polyurethane technology that meets the performance demands of traditional polyurethane applications while addressing environmental challenges. The polyester polyols used in Soleic® are USDA BioPreferred certified at 100% biocontent, made from renewable, plant-based raw materials that do not compete with food sources or contribute to deforestation.

- In October 2025, Reju, a startup based near Frankfurt, Germany, announced the construction of a chemical recycling plant aimed at transforming used polyester garments into high-quality polyester polyols. This innovative process, supported by Technip Energies, utilizes a proprietary catalyst to depolymerize polyester into pure monomers, enabling the creation of new polyester without quality degradation.

Companies Covered in Polyester Polyols Market

- BASF SE

- Covestro AG

- Dow Inc.

- Huntsman Corporation

- Mitsui Chemicals, Inc.

- LG Chem Ltd.

- Bayer MaterialScience AG

- Shell Chemicals

- Wanhua Chemical Group Co., Ltd.

- Sinopec Shanghai Petrochemical Co., Ltd.

- Kumho P&B Chemicals, Inc.

- Mitsubishi Chemical Corporation

- Evonik Industries AG

- Arkema S.A.

- Ashland Global Holdings, Inc.

- Allnex Austria GmbH

- UPM-Kymmene Corporation

- Trinseo S.A.

- Celanese Corporation

- Lonza Group AG

Frequently Asked Questions

The polyester polyols market size was valued at US$10.1 Billion in 2025.

The polyester polyols market is projected to reach US$14.3 Billion by 2032, reflecting steady growth in industrial, automotive, and construction applications.

Key trends are increasing adoption of bio-based and low-VOC polyols due to environmental regulations and the rising demand from flexible and rigid foams, coatings, and automotive interiors.

By product type, aliphatic polyester polyols hold the largest market share of 58% in 2025.

The polyester polyols market is projected to grow at a CAGR of 5.1% from 2025 to 2032, driven by urbanization, industrial growth, and sustainability-focused product adoption.

Major companies include BASF SE, Covestro AG, Dow Inc., Huntsman Corporation, and Mitsui Chemicals.