- Metals & Minerals

- Metallurgical Coke Market

Metallurgical Coke Market Size, Share, and Growth Forecast for 2024 - 2031

Metallurgical Coke Market by Product Type (Blast Furnace, Foundry, Technical), Ash Content (Low Ash Content, High Ash Content), End Use (Iron and Steel Production, Non-ferrous Metal Casting, Chemical Industry), and Regional Analysis from 2024 to 2031

Metallurgical Coke Market Size and Share Analysis

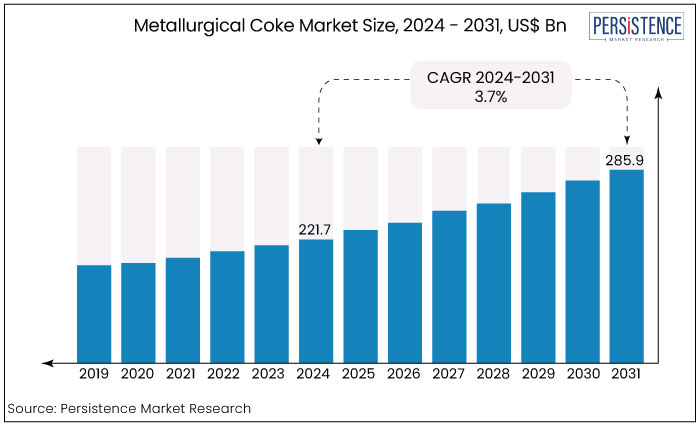

The metallurgical coke market is estimated to increase from US$ 221.7 Bn in 2024 to US$ 285.9 Bn by 2031. The market is projected to record a CAGR of 3.7% during the forecast period from 2024 to 2031. Booming iron and steel industry as well as rapid industrialization is anticipated to create fresh growth prospects worldwide.

As per the India Brand Equity Foundation (IBEF), the consumption of finished steel in the country stood at 138.5 MT in FY24 and 119.17 MT in FY23. In FY25, the country’s domestic steel demand is projected to surge by 9 to 10%. With rising production and consumption of iron and steel in emerging markets, thermal and metallurgical coal is set to witness high sales.

Key Highlights of the Market

- Sales of metallurgical coke or met coke are set to rely on the global steel industry, with high demand from construction, automotive, and infrastructure sectors.

- Coke producers are integrating Artificial Intelligence (AI), Internet of Things (IoT), and advanced desulfurization processes to improve quality and production efficiency.

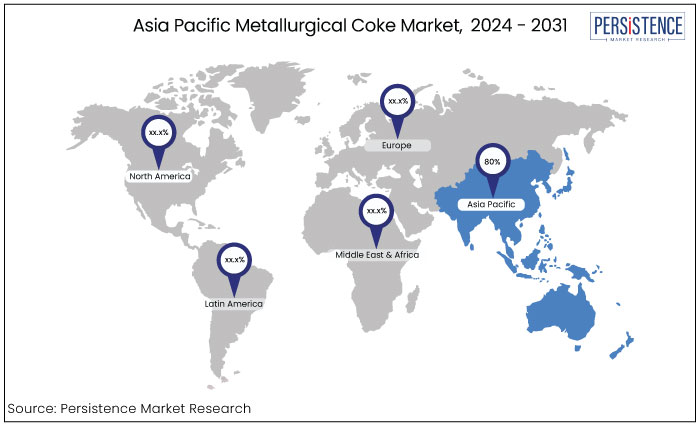

- Asia Pacific is projected to account for a share of 80% in 2024 as India is enhancing domestic coke production to reduce import dependence.

- By end use, the iron and steel production segment is anticipated to dominate with a share of 60% in 2024 owing to rising production in emerging countries.

- Waste heat recovery systems and by-product recycling are being adopted worldwide to improve sustainability and operational efficiency.

- Collaborations between coke producers and steel manufacturers are allowing for the development of long-term supply chains.

- In terms of product type, blast furnace coke is set to lead with a share of 45% in 2024 amid rising demand from large-scale production facilities.

|

Market Attributes |

Key Insights |

|

Metallurgical Coke Market Size (2024E) |

US$ 221.7 Bn |

|

Projected Market Value (2031F) |

US$ 285.9 Bn |

|

Global Market Growth Rate (CAGR 2024 to 2031) |

3.7% |

|

Historical Market Growth Rate (CAGR 2019 to 2023) |

2.8% |

Asia Pacific Metallurgical Coke Market Leads as Construction Activities Skyrocket

|

Region |

Market Share in 2024 |

|

Asia Pacific |

80% |

Asia Pacific is anticipated to lead with a market share of around 80% in 2024. It is attributed to rising investments by iron and steel companies for the development of new products. India is set to account for a sizeable portion of the global market in terms of volume and value. This is due to its status as the second-largest steel-producing country in the world.

The production of crude and finished steel, according to the India Brand Equity Foundation (IBEF), was 71.56 MT and 68.17 MT, respectively, from April to October 2022. The affordability of labor and domestic accessibility of raw materials like iron ore have been the main drivers of growth in the country’s steel industry.

Robust economic reforms, rising per capita income, and increasing infrastructure projects are a few prominent factors bolstering demand for steel in the country. High-strength steel is also projected to be used due to its superior tensile strength and stiffness in the building and construction sector.

In August 2023, NMDC Limited, a government-owned iron mining enterprise in India, announced the initiation of operations at its blast furnaces in Chhattisgarh. It is the country’s second-largest blast furnace, which is anticipated to yield 9,500 tons of molten metal daily. It is an environmentally sustainable and energy-efficient blast furnace technology for steel production.

China, on the other hand, is estimated to hold a significant share of the global market in 2031. It is set to be one of the key crude steel-producing countries globally. Development of new steel manufacturing plants and increasing automotive production are projected to drive metallurgical coke demand in China.

Blast Furnace Coke Dominates due to Need for Low Production Cost and Energy

|

Category |

Market Share in 2024 |

|

Product Type- Blast Furnace Coke |

45% |

Based on product type, the market is divided into blast furnace, foundry, and technical coke. Out of these, the blast furnace coke segment dominates the market. This is attributed to the rising use of metallurgical charcoal as an essential feedstock in blast furnace coke.

Anthracite has a history of usage in blast furnaces for smelting iron. However, it lacked the pore space of metallurgical coke that eventually replaced the material. The latter is layered into a blast furnace using the pulverized coal injection system to convert iron ore into metallic iron.

Due to its various advantages, including suitability for large-scale continuous production and continuous feeding and tapping, blast furnace coke holds a significant share of the market. It also requires a relatively low production cost, has high efficiency, and consumes less power, which is likely to increase demand.

Iron and Steel Production Companies to Push Demand for Met Coke

|

Category |

Market Value Share 2024 |

|

End Use- Iron and Steel Production |

60% |

Based on end use, the market is classified into iron and steel production, non-ferrous metal casting, and chemical industry. Among these, the iron and steel production segment dominates the market.

The iron and steel industry consists of foundries, sintering plants, and blast furnaces. These require a significant amount of metallurgical coke to convert iron ore to iron. Coke is commonly used to make iron, which is a key component of steel and accounts for 70% of all steel production.

The production of iron requires the use of metallurgical coke. It contributes to both the heat and carbon required for the blast furnace to process heated metal and chemically reduce the iron load. Coking coal, also known as metallurgical coal, is a crucial component in the process of manufacturing steel, which is set to propel demand.

Metallurgical Coke Market Introduction and Trend Analysis

Metallurgical coke or met coke is an essential material used for the production of steel and crude iron. It is generally used in steel and iron industry processes such as sinter plants, blast furnaces, and foundries to convert iron ore to iron. Metallurgical coke demand is significantly dependent on the steel and iron industry.

The porous carbon material’s quality, strength, porosity, and chemical composition are crucial for effective and superior steel manufacturing. It is an essential component in the steel industry, greatly aiding the creation of diverse steel used in buildings, automobile manufacturing, and infrastructure development.

Several companies are increasingly integrating AI and IoT technologies to monitor and maintain the quality of metallurgical coke. They are also optimizing its strength, porosity, and chemical composition in real time. This strategy is set to help coke producers ensure the consistent quality required for blast furnace operations.

Historical Growth and Course Ahead

From 2019 to 2023, the global market expanded at a CAGR of 2.8%. Rapid expansion of the steel industry and rising innovations in coke-producing technologies bolstered low ash metallurgical coke demand during this period.

A significant decline in global steel production in 2022 compared to 2021, however, resulted in a sluggish growth rate during the historical period. According to the World Steel Association, global crude steel production witnessed a decrease of around 3.7% from January to November 2022 compared to the same period in 2021. This decline was attributed to factors such as high inflation, rising interest rates, and increasing energy costs worldwide.

A significant increase in new infrastructure projects and mild recovery of the real estate sector in several emerging economies are anticipated to create new prospects in future. Government-led initiatives for economic diversification are also projected to bolster growth.

Countries such as China, India, and Brazil are set to witness substantial growth in their construction sector. It is owing to the increasing construction of office buildings, shopping centers, and light rail corridors. Surging use of metallurgical coke in various fields, such as iron and steel processing and glass manufacturing is further anticipated to boost demand.

Market Growth Drivers

Rising Demand for Steel from Automakers to Propel Metallurgical Coke Production

Steel is one of the key raw materials in the automotive industry, accounting for about 60% of the weight of an average automobile. On average, about 900 kgs of steel is used per vehicle. According to the World Steel Association, the automotive industry accounts for around 10% to 12% of global steel consumption.

Steel is widely used in the manufacturing of vehicle body structures, drive trains, cast iron for engine blocks, suspensions, fuel tanks, steering, braking systems, and various other components. According to the European Automobile Manufacturers' Association, nearly 50 million passenger cars were manufactured globally over the first three quarters of 2022. It showed a growth of around 9% compared to the same nine-month period in 2021.

Significant increase in the production and sales of passenger cars, light commercial vehicles, and heavy commercial vehicles, is set to accelerate steel demand across the globe. Several companies are anticipated to come up with unique steel components to increase sales from automakers. For instance,

- In 2024, Luxembourg-based ArcelorMittal, one of the most prominent steel producers, developed Advanced High-Strength Steel (AHSS) tailored for the automotive industry. It helps reduce vehicle weight while maintaining safety, which is critical for fuel efficiency and electric vehicles.

Investments in Infrastructure Development Activities to Bolster Demand

The correlation between urbanization, construction projects, infrastructure development, and demand for metallurgical coke is substantial. These sectors predominantly depend on steel, which relies on metallurgical coke for its manufacturing.

There is a concurrent growth in the demand for steel. It is anticipated to push steel production across mills to satisfy the growing demand with the rise of urbanization and construction projects. Metallurgical coke is essential in the steelmaking process, especially in the blast furnace method. Hence, its demand correlates directly with the steel industry's production levels. Consequently, an increased demand for steel necessitates a greater quantity of metallurgical coke for its production.

The construction sector is a primary consumer of steel. It is an essential element which is integral to the structural framework of buildings and the reinforcing of concrete. Key construction endeavors like skyscrapers, bridges, and stadiums, necessitate considerable amounts of steel.

Infrastructure development initiatives heavily depend on steel for ensuring high strength and durability. These include transportation networks such as highways, railways, and airports as well as energy generation and distribution systems like power plants and grids. Also, investments by governments to develop public facilities such as schools, hospitals, and water treatment plants are anticipated to create a high demand.

Market Restraining Factors

Fluctuations in Steel Prices May Negatively Affect Uses of Metallurgical Coke

As metallurgical coke is a fundamental raw material in steel manufacturing, especially in blast furnace processes, fluctuations in steel demand directly affect coke consumption. In an ever-developing economy, steel mills can increase production to satisfy the rising demand for commodities, thereby enhancing demand for metallurgical coke. During an economic downturn, steel output diminishes, resulting in a reduced need for coke.

Economic recessions can induce uncertainty and volatility in terms of the metallurgical coke market revenue. The volatility of steel demand, shaped by global economic factors, complicates production planning and inventory management for coke manufacturers. This condition can sometimes be augmented by the high fixed costs and capital-intensive characteristics of coke production. It will likely hinder growth in the global market.

Key Market Opportunities

Increasing Coal Tar Production to Make Aromatic Compounds Creates Opportunities

The chemical industry's increasing focus on coal tar manufacturing is set to propel the global metallurgical coke market growth during the forecast period. As coal tar is widely utilized to make aromatic compounds, it has significant economic significance for the chemical industry. For instance,

- In 2023, Tokyo-based Nippon Steel increased its production and processing of coal tar. It capitalized on rising demand from the chemical industry for raw materials used to manufacture aromatic compounds and carbon-based products.

Improvements in coke-making technologies have further reinforced the demand for metallurgical coke. Heat recovery coke manufacturing technology is becoming increasingly important in developed countries like the U.S. and the U.K.

Several developing nations have also observed the significant market potential of simple designs and ease of use. As a result, the total carbon footprint of the procedures used to produce metallurgical coke has significantly reduced.

Growing need for low operating and maintenance costs is a key factor driving the development of new products. In future years, blast furnaces used by manufacturers of metallurgical coke are anticipated to receive increased attention. It is likely to enable them to focus more on performance, thereby augmenting market growth.

Competitive Landscape for the Metallurgical Coke Market

The global metallurgical coke market is one of the fastest-growing industries. It comprises several key players holding a significant market share. These players are mainly investing in enhancing product quality by implementing new technologies to improve the strength of coke. They also focus on the techniques for producing high-strength coke using coal with small inert ingredient content.

Key players are constantly investing in extending their sales network and acquiring small and regional players. They are also strategically forming long-term contracts with dealers and suppliers. These contracts are not just about stability in revenue generation but also about creating opportunities for growth. These demonstrate the focus of leading players on both stability and expansion.

Recent Industry Developments

- In November 2023, Glencore plc, based in Switzerland, announced an agreement to acquire a 77% stake in Teck Resources’ steel-making coal subsidiary, Elk Valley Resources, which amounts to US$ 6.93 Bn.

- In November 2023, Warrior Met Coal Inc., based in the U.S., allocated US$ 127.8 Mn in the fourth quarter of 2023 to its Blue Creek Growth project, resulting in a total investment of US$ 319.1 Mn for 2023.

Companies Covered in Metallurgical Coke Market

- OKK Koksovny, A.S.

- SunCoke Energy Inc.

- Ennore Coke Limited

- Hickman, Williams and Company

- MECHEL PAO

- China Risun Coal Chemicals Group Limited

- YILCOQUE S.A.S.

- Sino Hua-An International Berhad

- China Shenhua Energy Company Limited

- ArcelorMittal

- Drummond Company, Inc.

- Jiangsu Surun High Carbon Co., Ltd.

- Nippon Steel and Sumitomo Metal

- Haldia Coke

- Baosteel Group

- Shanxi Sunlight Coking Group Company Ltd.

- Taiyuan Coal Gasification (Group) Co. Ltd.

- Shanxi Lubao Coking Group Co. Ltd.

Frequently Asked Questions

The market is estimated to be valued at US$ 285.9 Bn by 2031.

The market is estimated to exhibit a CAGR of 3.7% over the forecast period.

OKK Koksovny, A.S., SunCoke Energy Inc., and Ennore Coke Limited are a few manufacturers.

Coal is the primary raw material for making metallurgical coke.

It is mainly used for steel and coke production.