- Medical Devices

- Lithotripsy Devices Market

Lithotripsy Devices Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Lithotripsy Devices Market by Product (Intracorporeal Lithotripsy Device and Extracorporeal Lithotripsy Device), Modality (Standalone Device and Portable Device), Application (Kidney Stones, Ureteral Stones, Bladder Stones, Pancreatic Stones, and Others) End-user (Hospitals, Specialty Clinics, and Ambulatory Surgery Centers), and Regional Analysis from 2026 to 2033

Lithotripsy Devices Market Share and Trends Analysis

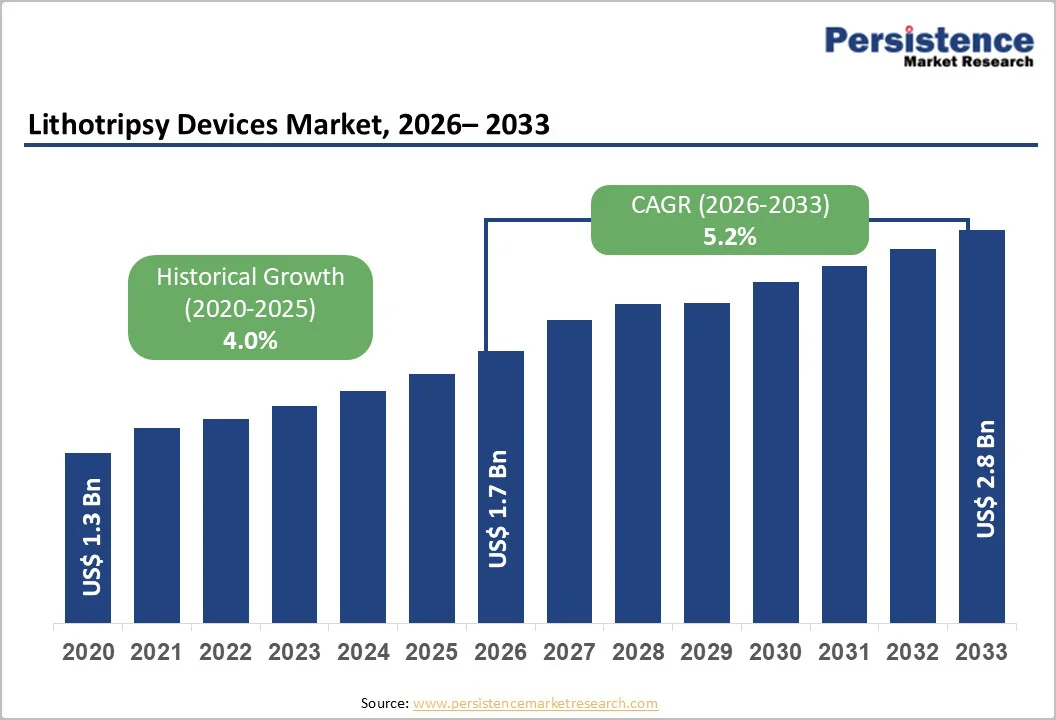

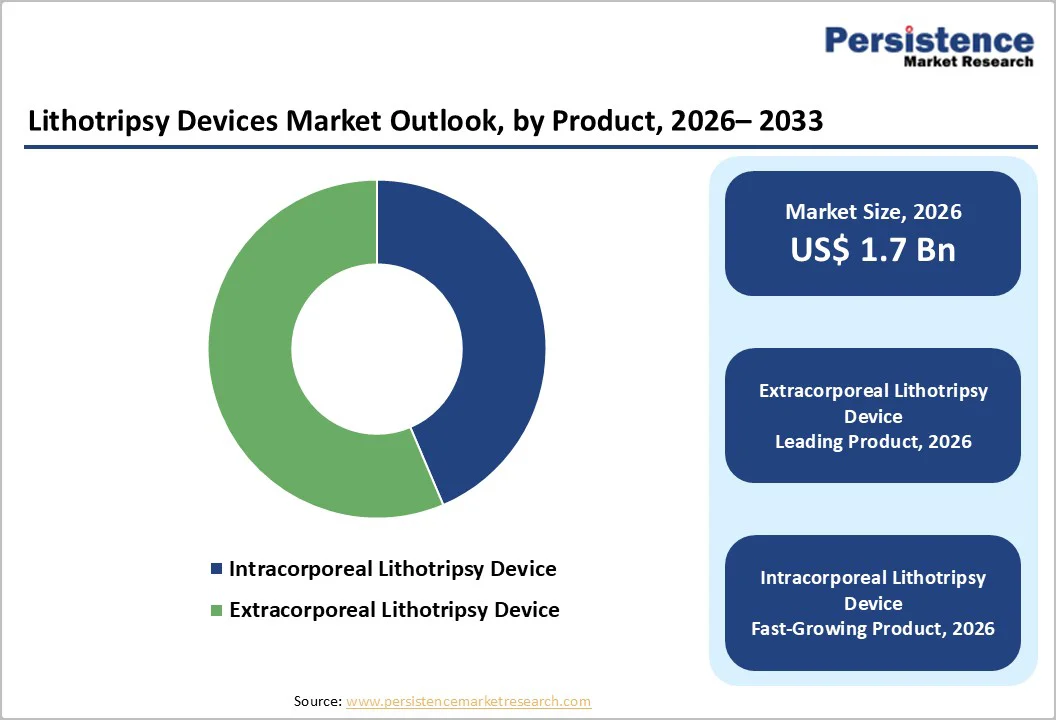

The global lithotripsy devices market size is estimated to grow from US$ 1.7 billion in 2026 to US$ 2.8 billion by 2033. The market is projected to record a CAGR of 5.2% during the forecast period from 2026 to 2033.

Global demand for lithotripsy devices is rapidly increasing due to the rising prevalence of kidney stones and peripheral artery disease (PAD), coupled with the growing preference for minimally invasive treatment options. The expansion of outpatient and ambulatory care, increasing surgical volumes, and adoption of advanced intravascular and extracorporeal lithotripsy technologies are key contributors.

Technological innovations, including smart, integrated, and combination devices, real-time imaging guidance, and catheter miniaturization, are enhancing procedural efficiency, safety, and patient outcomes. Additionally, expanding insurance coverage, investments in digital health integration, and rising awareness of non-surgical interventions further drive market growth.

Key Industry Highlights:

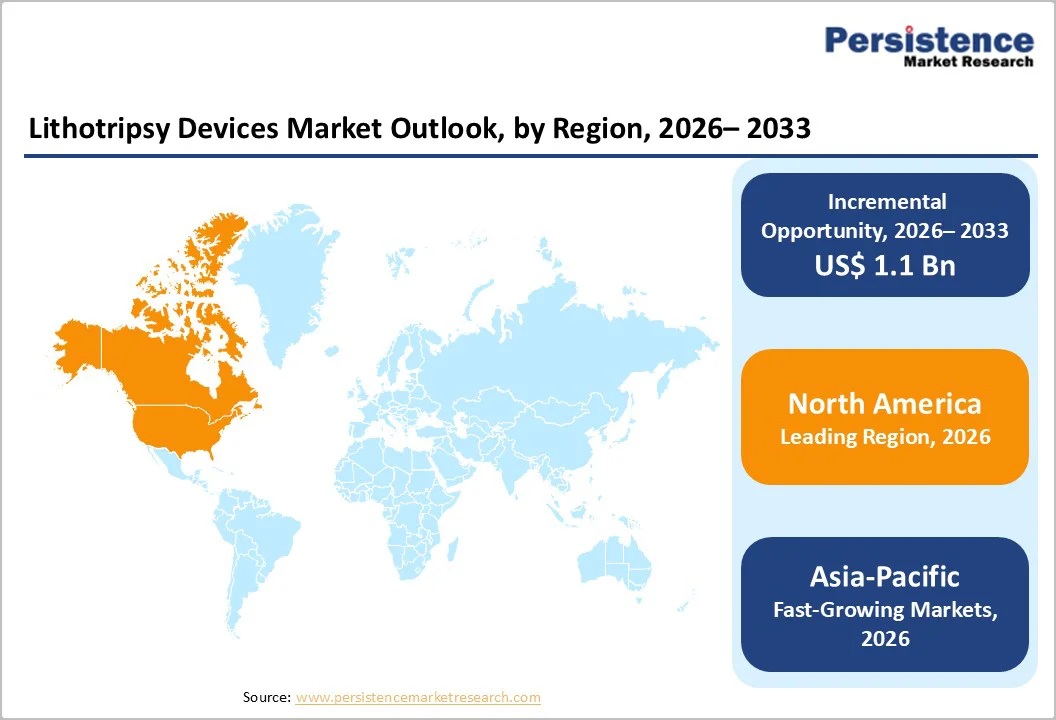

- Leading Region: North America dominates the global lithotripsy devices market with a 43.4% share, supported by high kidney stone prevalence, advanced healthcare infrastructure, strong adoption of IVL and extracorporeal lithotripsy systems, and favorable reimbursement policies.

- Fastest-Growing Region: Asia Pacific is the fastest-growing market, driven by increasing kidney stone incidence, expanding access to outpatient care, rapid healthcare digitization, and growing adoption of portable and catheter-based lithotripsy devices.

- Leading Product Segment: Extracorporeal lithotripsy devices lead the product category due to advanced precision, non-invasive application, high safety, and widespread use in kidney stone treatment.

- Fastest-Growing Product Segment: Intravascular lithotripsy (IVL) devices are the fastest-growing segment, fueled by affordability, minimally invasive procedure benefits, and rising adoption in PAD management.

- Leading Application Segment: Kidney stones dominate the application segment, attributed to high prevalence, cost-effective treatment over surgical options, and compatibility with hospital and outpatient protocols.

- Fastest-Growing Application Segment: Ureteral stones are the fastest-growing category due to the rising prevalence of ureteral calculi, increasing preference for minimally invasive treatments, enhanced safety and precision of modern lithotripsy devices, and growing demand for outpatient and home-care procedures.

| Key Insights | Details |

|---|---|

| Lithotripsy Devices Market Size (2026E) | US$ 1.7 Bn |

| Market Value Forecast (2033F) | US$2.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.0% |

Market Dynamics

Driver - Rising Nephrolithiasis Burden Coupled with Advancements in Lithotripsy Technology

The global rise in nephrolithiasis incidence, driven by ageing populations, obesity, dehydration, and dietary habits, continues to increase patient volumes and recurrent stone cases.

For instance, according to the National Kidney Foundation, reported that kidney stones lead to over 500,000 emergency room visits every year in the U.S., and roughly one in ten individuals will experience a stone at some point in their lifetime.

This rising disease burden is pushing hospitals and ambulatory centers to adopt faster, minimally invasive stone-management techniques that reduce hospital stay and procedure time, supporting long-term demand for lithotripsy systems.

Technology upgrades such as compact, portable extracorporeal shock wave lithotripsy (ESWL) units, enhanced shock-wave targeting, high-resolution ultrasound/fluoroscopy guidance, and energy-efficient generators are making lithotripsy safer, more precise, and more accessible.

These advancements are expanding adoption in smaller centers, improving treatment accuracy, lowering complications, and strengthening the overall value proposition for both providers and patients.

Restraints - Cost, Clinical, and Competitive Constraints Limiting Wider Adoption

High upfront capital costs for lithotripsy systems, combined with variable reimbursement and notable per-procedure expenses, continue to restrict adoption, particularly for smaller hospitals and ambulatory centers. These financial barriers make it difficult for facilities to justify investment, especially in regions with tighter budgets or inconsistent insurance coverage.

Moreover, lithotripsy faces inherent clinical limitations, such as reduced effectiveness for large, hard, or lower-pole stones and contraindications in certain patient groups. Furthermore, the market faces strong competitive pressure from ureteroscopy and percutaneous nephrolithotomy, which offer higher stone-free rates for complex cases, as well as from improved medical expulsive therapies that reduce the need for device-based intervention.

Opportunity - Smart Imaging Integration and Affordable Portable Devices

Advances in AI-driven imaging, real-time stone tracking, and automated targeting are set to transform treatment precision and workflow efficiency. The integration of intelligent guidance systems with lithotripsy platforms is improving shock-wave accuracy, reducing retreatment rates, and enabling more consistent outcomes.

Additionally, hybrid therapy approaches combining ESWL with laser or ultrasound modalities are opening new pathways for treating complex stones with fewer complications.

Furthermore, the development of portable, compact, and lower-cost lithotripsy units is widening access among ambulatory surgical centers (ASCs) and smaller healthcare facilities. These cost-efficient devices reduce infrastructure needs, support higher procedure throughput, and make advanced stone management feasible in resource-constrained settings, ultimately expanding market penetration in both mature and emerging regions.

Category-wise Analysis

By Product Insights

The extracorporeal lithotripsy devices segment is projected to dominate the global lithotripsy devices market in 2026, accounting for a revenue share of 56.4%. The segment’s strong performance is primarily driven by its non-invasive nature, shorter recovery time, and widespread adoption for kidney and ureteral stones.

Increasing preference for outpatient ESWL procedures, along with advancements in shock-wave targeting and imaging integration, further supports its leading position across both developed and emerging healthcare settings. Additionally, growing patient preference for minimally invasive treatments and rising hospital investments in upgraded ESWL platforms continue to strengthen segment demand. Expanding utilization in high-volume stone management centers.

By Modality Insights

The standalone device segment is projected to dominate the global lithotripsy devices market in 2026, accounting for a revenue share of 54.7%.

This is driven by their higher energy output, integrated imaging capabilities, and superior efficiency in managing a wide range of stone types, enabling clinicians to achieve high stone-free rates in a single session. Their robust design, longer operational lifespan, and compatibility with advanced targeting technologies make them the preferred choice for high-volume hospitals and specialized urology centers.

Additionally, the rising demand for comprehensive stone-management infrastructure, along with the need for reliable, continuous operation during peak patient loads, further supports strong adoption of standalone systems. Healthcare facilities in developed markets are increasingly allocating capital budgets toward system upgrades, imaging-linked platforms, and replacement of aging ESWL units.

By End-user Insights

The hospitals segment is projected to dominate the global lithotripsy devices market in 2026, accounting for a revenue share 56.9%. This is driven by their strong infrastructure, availability of advanced imaging systems, and higher patient inflow for complex kidney, ureteral, and bladder stone procedures. Hospitals also manage a greater proportion of emergency and high-risk cases, making them primary adopters of high-precision lithotripsy platforms.

Furthermore, hospitals benefit from larger capital budgets, enabling investment in standalone ESWL systems, hybrid technologies, and integrated urology suites. The presence of skilled urologists, multidisciplinary care teams, and post-procedure monitoring capabilities further strengthens their preference among patients.

Region-wise Insights

North America Lithotripsy Devices Market Trends

The North America market is expected to dominate globally with a value share of 43.4% in 2026, with the U.S. leading the region due to its highly developed healthcare ecosystem, strong technological readiness, and widespread availability of advanced imaging and surgical infrastructure.

The country records one of the highest incidences of kidney stones worldwide, driven by dietary patterns, obesity prevalence, and climatic factors that increase dehydration risk. This consistently large patient pool sustains high procedural volumes across hospitals and ambulatory surgery centers, strengthening demand for both extracorporeal and intracorporeal lithotripsy systems.

Furthermore, favorable reimbursement mechanisms and insurance coverage for minimally invasive stone-management procedures encourage healthcare providers to invest in next-generation lithotripsy platforms.

Early adoption of AI-integrated imaging, real-time stone-tracking systems, and high-precision energy sources such as high-power lasers accelerates the modernization of urology departments across the region. The presence of leading manufacturers, strong R&D pipelines, and frequent replacement cycles for aging ESWL units also contribute to sustained market growth.

Europe Lithotripsy Devices Market Trends

Europe is expected to achieve a steady growth, driven by the rising prevalence of kidney and ureteral stones, especially among ageing populations and individuals with lifestyle-related risk factors such as obesity and metabolic disorders.

Strong adoption of minimally invasive urology procedures, supported by well-structured healthcare systems and widespread access to advanced diagnostic imaging, continues to fuel consistent demand for both extracorporeal and intracorporeal lithotripsy devices across the region.

Moreover, increasing investments by public hospitals in modern ESWL platforms, expanding availability of laser-based intracorporeal systems, and the shift toward outpatient day-care procedures are contributing to sustained market expansion. Favorable reimbursement frameworks in several Western European countries and government initiatives aimed at upgrading surgical infrastructure further support market growth.

Asia Pacific Lithotripsy Devices Market Trends

The Asia Pacific market is expected to register a relatively higher CAGR of around 7.8% between 2026 and 2033, fueled by the rapidly growing burden of kidney stones across major countries such as India, China, Japan, and Southeast Asia.

Rising urbanization, dietary changes, dehydration due to hot climates, and increasing rates of obesity and diabetes are contributing to a sharp rise in stone-forming populations. This growing patient base is creating strong demand for both extracorporeal and intracorporeal lithotripsy systems across hospitals, specialty clinics, and newly expanding ambulatory surgery centers.

Additionally, improving healthcare infrastructure, rising government investments in urology departments, and greater availability of advanced imaging modalities such as ultrasound and CT are supporting higher adoption of precision lithotripsy solutions.

Increasing penetration of private hospitals and medical tourism, particularly in India, Thailand, and Malaysia, is further accelerating equipment procurement. The introduction of portable and lower-cost lithotripsy devices tailored for resource-constrained settings is also expanding accessibility.

Competitive Landscape

The global lithotripsy devices market is highly competitive, with major players such as Siemens Healthineers AG, Dornier MedTech., Boston Scientific Corporation, STORZ MEDICAL AG, ?nceler Medikal Ltd., and DirexGroup leveraging extensive product portfolios, advanced ESWL and intracorporeal lithotripsy technologies, and well-established international distribution networks.

Companies are increasingly prioritizing innovation in compact, portable, and digitally enhanced lithotripsy systems designed to improve treatment precision, reduce procedure time, and support both hospital and ambulatory surgical center workflows.

Market participants are actively investing in next-generation platforms that integrate AI-driven imaging, real-time stone tracking, automated targeting, and hybrid energy systems to enhance clinical outcomes and expand the treatable stone spectrum.

Strategic initiatives include mergers and acquisitions aimed at strengthening technological capabilities, partnerships with urology centers for clinical validation, and expansion into fast-growing regions such as the Asia Pacific and the Middle East.

Key Industry Developments:

- In September 2025, Johnson & Johnson launched its Shockwave Javelin Peripheral IVL Catheter in Europe. The new intravascular lithotripsy system uses a single emitter placed near the catheter tip to improve calcium modification in severely narrowed vessels. With safety and performance similar to earlier Shockwave IVL devices, the launch strengthens the company’s leading PAD treatment portfolio.

- In October 2025, the FDA granted Breakthrough Device Designation to Avvio Medical’s Avvio enhanced lithotripsy system (ELS), a minimally invasive platform for treating ureteral stones. The device is currently being evaluated in a pivotal IDE study. The designation supports accelerated FDA review and closer regulatory guidance, recognizing the system’s potential to improve treatment safety and effectiveness. Avvio plans to submit a de novo application for device clearance in early 2026.

- In March 2025, Shockwave Medical, Inc., a subsidiary of Johnson & Johnson MedTech and a global leader in circulatory restoration, announced the U.S. launch of its Shockwave Javelin Peripheral IVL Catheter. This innovative intravascular lithotripsy (IVL) device is designed to modify calcium and navigate highly narrowed vessels in patients with peripheral artery disease (PAD).

- In November 2024, Philips announced the enrollment of the first U.S. patient in its THOR IDE clinical trial. The study will evaluate an innovative combined laser atherectomy and intravascular lithotripsy (IVL) catheter, which integrates two key treatments for peripheral artery disease (PAD) into a single device.

Companies Covered in Lithotripsy Devices Market

- Siemens Healthineers AG

- Dornier MedTech.

- Boston Scientific Corporation

- STORZ MEDICAL AG

- İnceler Medikal Ltd.

- DirexGroup

- Johnson & Johnson

- Focal One

- GEMSS HEALTHCARE Co., Ltd

- Olympus Corporation

- Cook Group

- EMS (Electro Medical Systems)

- Allengers

- Potent Medical

- Others

Frequently Asked Questions

The global lithotripsy devices market is projected to be valued at US$ 1.7 Bn in 2026.

Rising prevalence of kidney stones and peripheral artery disease, along with growing adoption of minimally invasive and advanced intravascular lithotripsy technologies are driving the global lithotripsy devices market.

The global lithotripsy devices market is poised to witness a CAGR of 5.2% between 2026 and 2033.

Development of next-generation intravascular and renal lithotripsy technologies, and expansion into emerging markets with rising prevalence of kidney stones and peripheral artery disease are creating opportunities in the market.

Siemens Healthineers AG, Dornier MedTech., Boston Scientific Corporation, STORZ MEDICAL AG, İnceler Medikal Ltd., and DirexGroup are some of the key players in the lithotripsy devices market.