- Biotechnology

- Lateral Flow Assay Market

Lateral Flow Assay Market Trends, Size, Share, and Growth Forecast, 2025 - 2032

Lateral Flow Assay Market by Product Type (LFA Readers, LFA Kits), Application (Sexually Transmitted Diseases, Infectious Diseases, Diabetes, Pregnancy and Fertility Testing, Drug of Abuse Testing), Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Supermarkets/Hypermarkets, E-Commerce), and Regional Analysis for 2025 - 2032

Lateral Flow Assay Market Size and Trends Analysis

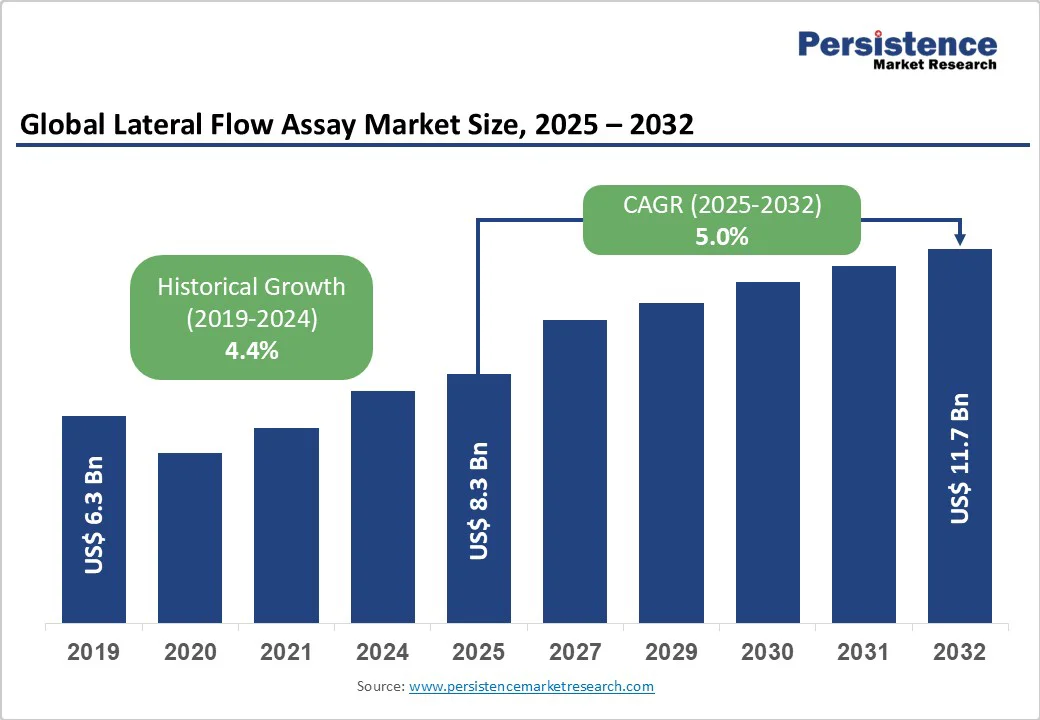

The global lateral flow assay market size is likely to be valued at US$8.3 billion in 2025, growing to US$11.7 billion by 2032 at a CAGR of 5.0% during the forecast period from 2025 to 2032.

The lateral flow assay industry is experiencing robust growth driven by the increasing prevalence of infectious and chronic diseases, rising demand for rapid point-of-care diagnostics, and advancements in lateral flow technologies.

Key Industry Highlights:

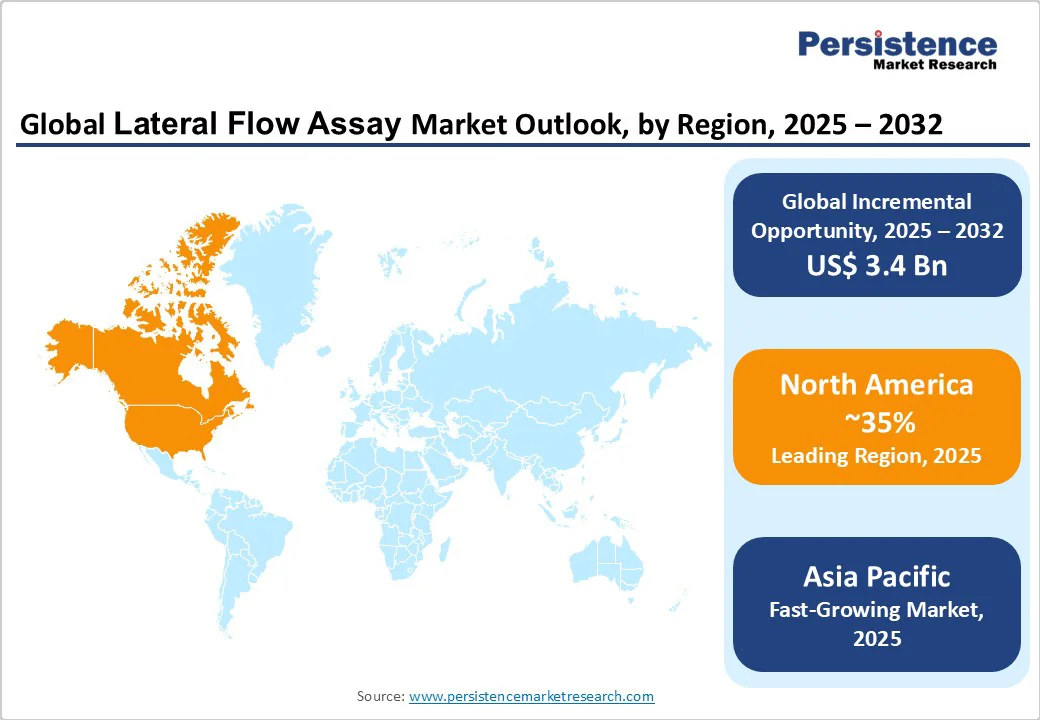

- Leading Region: North America, commanding a 35% market share in 2025, driven by advanced healthcare infrastructure, high adoption of point-of-care testing, and strong R&D in the U.S.

- Fastest-growing Region: Asia Pacific, fueled by rising disease burdens, expanding healthcare access, and investments in affordable diagnostics in countries like China and India.

- Dominant Product Type: LFA Kits, holding approximately 70% of the market share, due to their simplicity, portability, and widespread use in rapid testing.

- Leading Application: Infectious Diseases, accounting for over 40% of market revenue, driven by demand for quick pathogen detection in outbreaks.

- Leading Distribution Channel: Hospital Pharmacies, contributing nearly 50% of market revenue, owing to their role in clinical dispensing and patient education.

- Key Market Driver: Global diabetes prevalence, affecting 589 million adults in 2024, boosting the need for at-home glucose monitoring via lateral flow assays.

- Growth Opportunity: Advancements in digital LFA readers, enabling quantitative results and integration with telemedicine.

| Key Insights | Details |

|---|---|

| Lateral Flow Assay Market Size (2025E) | US$8.3 Bn |

| Market Value Forecast (2032F) | US$11.7 Bn |

| Projected Growth (CAGR 2025 to 2032) | 5.0% |

| Historical Market Growth (CAGR 2019 to 2024) | 4.4% |

Market Dynamics

Driver - Rising prevalence of infectious and chronic diseases and demand for rapid diagnostics

The increasing prevalence of infectious and chronic diseases globally is a primary driver of the lateral flow assay market. World Health Organization, infectious diseases such as tuberculosis affected 8.2 million people with new diagnoses in 2025, while diabetes impacts 589 million adults worldwide, projected to rise to 853 million by 2050.

This dual burden creates a substantial demand for accessible and rapid testing solutions. Lateral flow assays provide results in 15-30 minutes with over 90% accuracy for diseases such as COVID-19 and STIs, making them ideal for point-of-care settings where lab access is limited.

For instance, kits from companies like Abbott have shown 95% sensitivity in detecting HIV, enabling early intervention and reducing transmission by up to 70% in clinical studies. Additionally, the post-pandemic surge in home testing, coupled with investments in global health initiatives totaling US$10 Bn in 2025, has accelerated adoption.

The demand for affordable diagnostics in low-resource areas, supported by WHO's push for universal health coverage, continues to propel the market forward, particularly in regions with high disease incidence, such as the Asia Pacific and North America.

Restraint - Limitations in Sensitivity and Regulatory Hurdles

The limitations in sensitivity and specificity of lateral flow assays, along with stringent regulatory requirements, pose a significant restraint on market growth. While convenient, these assays can yield false negatives in low-concentration scenarios, with sensitivity rates as low as 70% for certain biomarkers, necessitating the use of confirmatory laboratory tests.

Development involves rigorous validation, with costs exceeding US$20 Mn per kit due to clinical trials and quality controls. Regulatory bodies, such as the U.S. FDA and EMA, demand extensive data on accuracy and stability, which can extend timelines to 2-4 years.

For example, approvals for multiplex assays by Roche have faced delays due to variability issues, resulting in increased costs of 25%. Smaller firms struggle against giants such as Thermo Fisher Scientific, which limits innovation in emerging markets where affordability is crucial.

Opportunity - Advancements in Digital Integration and Multiplex Capabilities

Advancements in digital readers and multiplex assays present significant growth opportunities for the lateral flow assay market. Digital LFA readers provide quantitative data via smartphone connectivity, improving accuracy to 98% and enabling remote monitoring.

These innovations align with the growth of telemedicine, as multiplex kits simultaneously detect multiple analytes for comprehensive screening. For instance, companies such as Siemens Healthineers are investing in AI-enhanced readers, with trials showing an 85% reduction in diagnostic errors.

Modular designs cut development costs by 30%, and integration with wearables boosts compliance. As global point-of-care demand surges, projected at US$50 billion by 2030-these opportunities are expected to drive expansion in high-tech regions such as North America and Europe.

Category-wise Analysis

Product Type Insights

LFA Kits are expected to dominate and account for approximately a 70% share in 2025. Their dominance is driven by ease of use, low cost, and portability, making them staples in home and field testing for infectious diseases.

LFA Readers are the fastest-growing segment, fueled by demand for precise, quantifiable results. Their integration with apps supports chronic disease management, with rapid adoption in clinical settings across innovative markets.

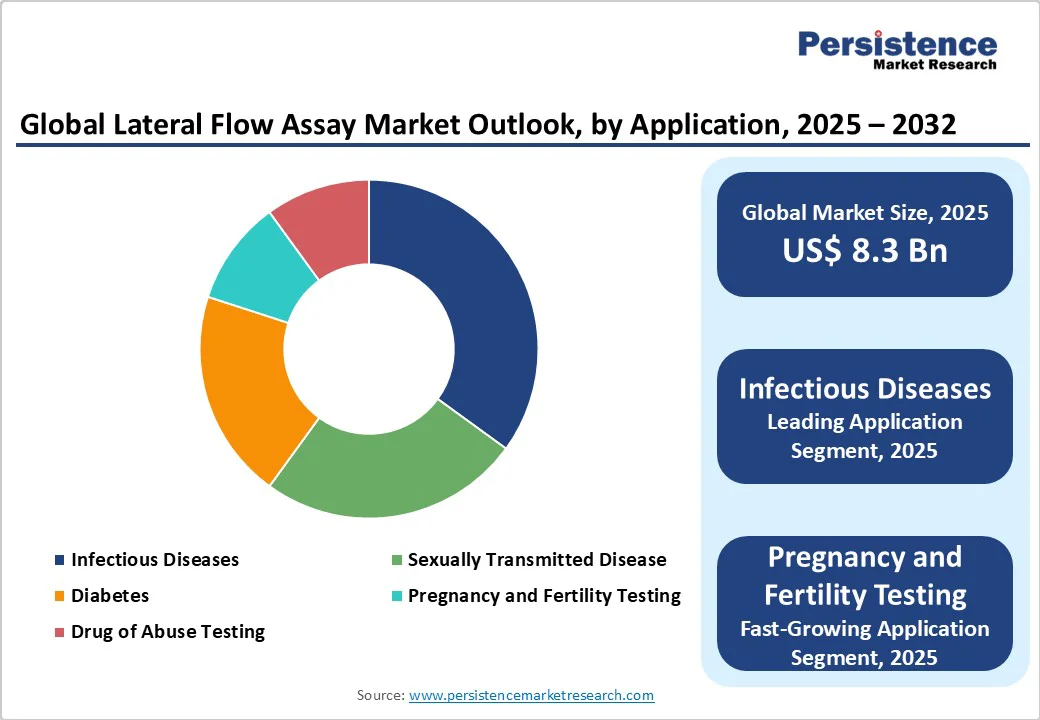

Application Insights

Infectious diseases are likely to lead with over 40% share in 2025, driven by their vital role in managing global health crises. Rapid testing for infections such as COVID-19 enables early detection, containment, and effective public health responses. Continuous innovation in point-of-care diagnostics strengthens surveillance, ensuring timely intervention and control of emerging infectious threats worldwide.

Pregnancy and fertility testing is the fastest-growing segment, fueled by increasing awareness of reproductive health and the rising adoption of home-use diagnostic kits. Convenient, accurate, and affordable options empower women to monitor fertility and detect pregnancy early, while digital integration and smartphone-based readers enhance result accuracy and accessibility, supporting proactive health management.

Distribution Channel Insights

Hospital pharmacies are likely to account for nearly 50% share in 2025, driven by their trusted role in dispensing prescription-based diagnostic tests. Their integration within healthcare settings ensures professional oversight, accurate guidance, and patient safety. Strong collaborations with clinicians and diagnostic suppliers further reinforce their reliability and accessibility in managing complex and chronic disease testing.

E-commerce is the fastest-growing segment in diagnostics, driven by the convenience of online purchasing and the rise of direct-to-consumer models. Digital platforms enable 20% annual growth, especially in urban regions with strong internet connectivity. This trend enhances accessibility, allowing consumers to easily order and receive diagnostic kits at home for faster, private testing.

Regional Insights

North America Lateral Flow Assay Market Trends

North America accounts for 35% market share in 2025, driven by its advanced healthcare and diagnostics infrastructure, combined with a high prevalence of chronic diseases, particularly diabetes, which affects approximately 38 million individuals.

This widespread disease burden creates a substantial demand for accurate, rapid, and reliable diagnostic testing, positioning the U.S. as a key market globally. The country benefits from a robust research and development ecosystem, with significant investments from both private and public sectors in developing innovative diagnostic tools, including point-of-care and high-throughput laboratory solutions.

Regulatory support further strengthens the market, as the FDA offers fast-track approvals for rapid diagnostic tests, ensuring timely access to critical technologies. Additionally, the integration of telemedicine and digital health platforms has expanded access to diagnostics, allowing remote patient monitoring, real-time results, and improved chronic disease management. Healthcare providers increasingly leverage these innovations to enhance patient outcomes, reduce hospital visits, and streamline clinical workflows.

Europe Lateral Flow Assay Market Trends

Europe holds about 25% market share, supported by unified EU regulations and collaborative health initiatives, which provide a stable framework for innovation, safety, and cross-border healthcare delivery. Leading countries such as Germany, France, and the U.K. are major contributors to growth, collectively investing over €5 Bn in diagnostics in 2025. Germany’s focus on precision engineering enhances the production of high-quality diagnostic kits, enabling rapid responses during infectious disease outbreaks and strengthening its position as a leader in technology.

France emphasizes reproductive health, particularly fertility testing, driven by approximately 4 million annual pregnancies, which fuels demand for advanced prenatal and genetic diagnostics. On the other hand, the U.K. is expected to show an upward trend, with 15% market growth in 2025, driven by the National Health Service’s adoption of digital readers for the management of sexually transmitted infections (STIs). This integration of digital technologies increases accessibility, accuracy, and patient engagement, particularly in the post-Brexit healthcare landscape.

Asia Pacific Lateral Flow Assay Market Trends

Asia Pacific commands around a 25% share and is the fastest-growing region, driven by high population density and the prevalence of disease hotspots, particularly in countries like China and India. In China, the market is expanding rapidly, supported by investments of approximately US$15 Bn in health technology aimed at improving disease detection and management. A key focus is diabetes, affecting around 200 Mn individuals, where affordable diagnostic kits and point-of-care solutions are enabling widespread testing, early detection, and better disease control.

The Chinese government and private sector are also leveraging digital health platforms and telemedicine to reach underserved populations, enhancing access to timely diagnostics across urban and rural regions. In India, growth is fueled by nationwide healthcare initiatives, such as the Ayushman Bharat program, which subsidizes healthcare services and promotes preventive care. The program, combined with the expansion of e-commerce distribution channels, facilitates access to diagnostic tools, including STI screening kits, particularly in rural and semi-urban areas where healthcare infrastructure is limited.

Competitive Landscape

The global lateral flow assay market is characterized by intense competition, driven by both established diagnostic giants and agile innovative startups. In North America and Europe, major players like Abbott and Roche maintain market dominance through continuous technological advancements, such as high-sensitivity detection and integration with digital platforms.

Meanwhile, the Asia-Pacific region sees strong participation from local companies offering cost-effective solutions, catering to large populations, and emerging healthcare needs. Market competition is further intensified by the growing emphasis on multiplex assays, which allow simultaneous detection of multiple targets, and digital innovations that enhance result accuracy and connectivity.

Key Developments:

- In July 2025, VolitionRx Limited announced a lateral flow test that can quantify nucleosomes in whole venous blood in minutes. This technology, part of the SUMMIT program, could enable the rapid detection of immune disruptions in settings such as emergency rooms or intensive care.

- In May 2025, Researchers published a paper on a centrifugation-assisted LFA platform that improves sensitivity by regulating capillary flow. As proof of concept, they detected human chorionic gonadotropin (hCG) and hemoglobin (Hb) with greater sensitivity than commercial LFA tests.

Companies Covered in Lateral Flow Assay Market

- Thermo Fisher Scientific

- Roche

- Abbott

- Becton Dickinson

- PerkinElmer

- Siemens Healthineers

- QIAGEN

- bioMérieux

- Bio-Rad

- Maternova

- Quidel

- Healgen Scientific

- Meridian Bioscience

- Abcam

- Access Bio

- Humasis

- DIALUNOX

- Detekt Biomedical

- Others

Frequently Asked Questions

The global Lateral Flow Assay Market is projected to reach US$ 8.3 Bn in 2025, driven by surging demand for rapid diagnostics amid rising infectious and chronic diseases.

The market is driven by global health challenges like 8.2 million new TB cases and 589 million diabetes patients in 2024, necessitating quick, affordable point-of-care testing solutions.

The market is poised to witness a CAGR of 5.0% from 2025 to 2032, supported by tech advancements in digital readers and multiplex kits for enhanced accuracy.

Advancements in digital integration and multiplex capabilities offer key opportunities, enabling quantitative, multi-analyte testing for telemedicine and personalized health monitoring.

Thermo Fisher Scientific, Roche, Abbott, Becton Dickinson, and Siemens Healthineers are key players, leading through innovations in rapid test kits and reader technologies.