- Sensors & Controls

- Inductive Proximity Sensors Market

Inductive Proximity Sensors Market Size, Share, and Growth Forecast, 2025 - 2032

Inductive Proximity Sensors Market By Housing Type (Cylindrical, Rectangular, Ring-style), Sensing Range (Short-range, Medium-range, Long-range), End-user Industry (Automotive and Transportation), and Regional Analysis for 2025 - 2032

Inductive Proximity Sensors Market Size and Trends Analysis

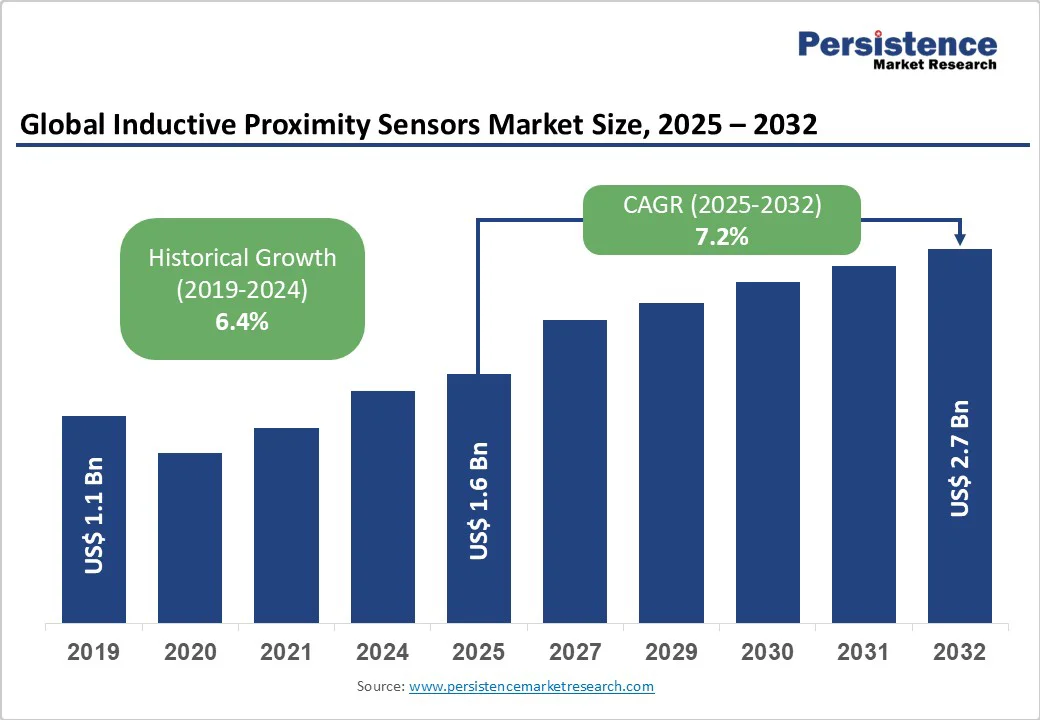

The global inductive proximity sensors market size is likely to be valued at US$1.6 Billion in 2025 and is estimated to reach US$2.7 Billion in 2032, growing at a CAGR of 7.2% during the forecast period 2025-2032. The inductive proximity sensors market growth is being fueled by the increasing adoption of automation, robotics, and digital manufacturing across industries. The automotive industry’s shift toward electric vehicle production is another key catalyst.

Key Industry Highlights

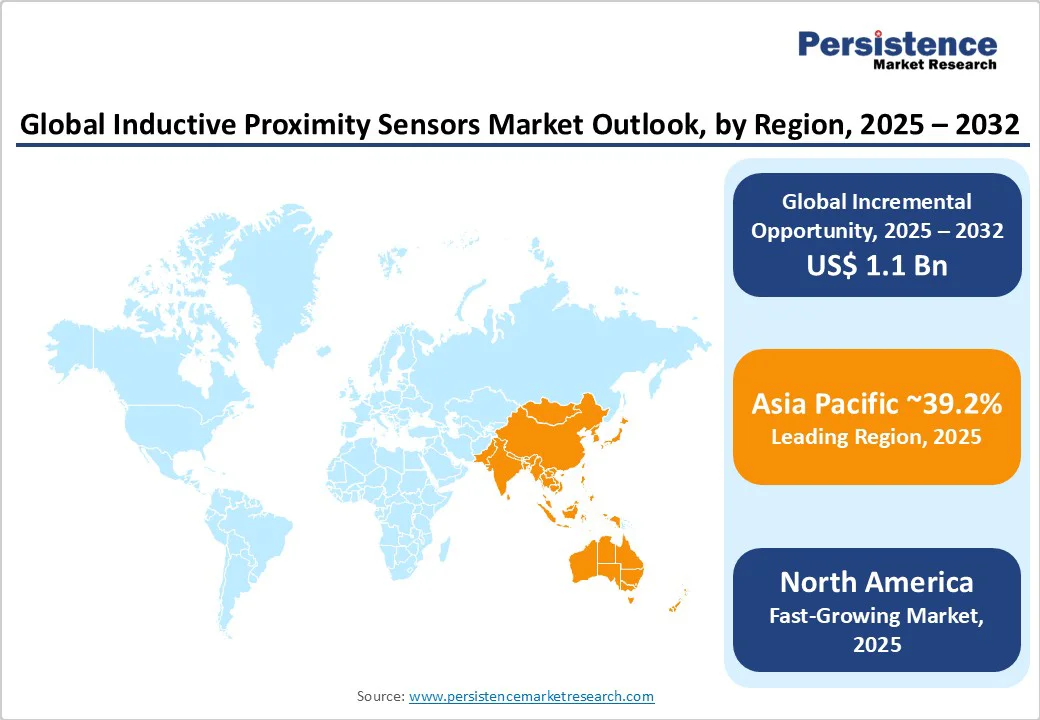

- Leading Region: Asia Pacific, with about 39.2% share in 2025, spurred by government-backed smart factory and industrial digitalization programs.

- Fastest-growing Region: North America, boosted by the ongoing modernization of legacy factories with Industry 4.0 technologies.

- New Product: In October 2025, Melexis launched a dual-input inductive sensor Integrated Circuit (IC). It is designed to read signals from two coil inputs simultaneously, providing high-precision angle and torque measurements for critical vehicle systems.

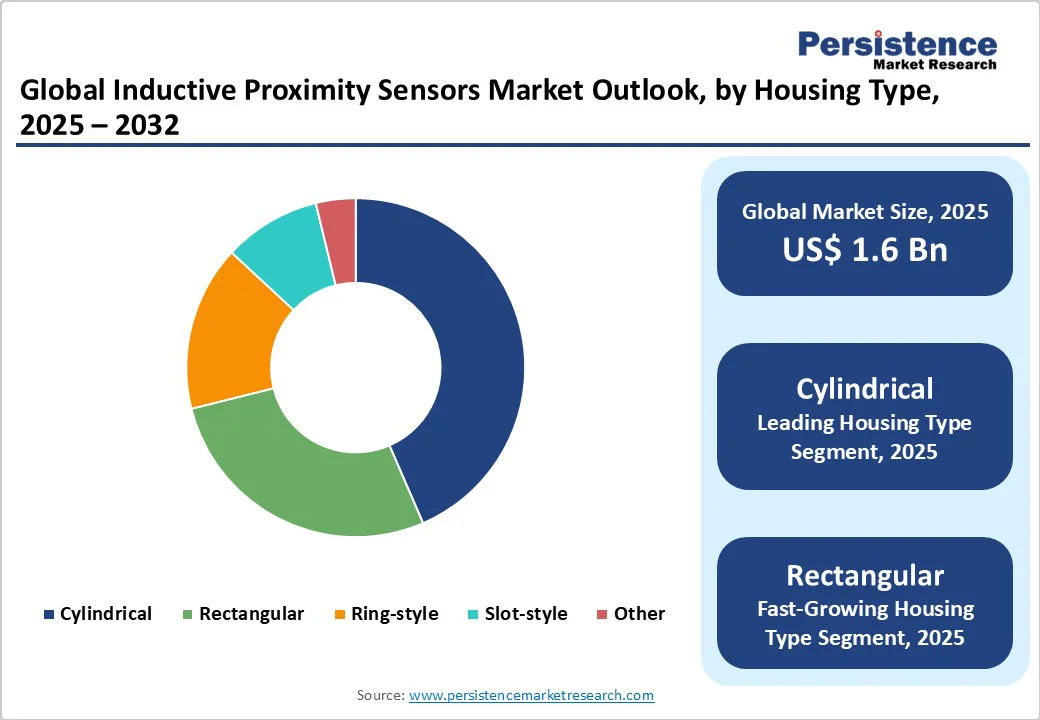

- Leading Housing Type: Cylindrical designs hold nearly 43.5% share in 2025, as they are compatible with diverse mounting options and suited for rugged applications.

- Dominant Sensing Range: Medium-range devices, approximately 46.3% of the inductive proximity sensors market share in 2025, since they provide an optimal balance between detection distance and accuracy for metal-based operations.

- Key End-user Industry: Industrial machinery and robotics recorded about 37.8% share in 2025, as sensors enable real-time performance monitoring.

| Key Insights | Details |

|---|---|

|

Inductive Proximity Sensors Market Size (2025E) |

US$1.6 Bn |

|

Market Value Forecast (2032F) |

US$2.7 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

7.2% |

|

Historical Market Growth (CAGR 2019 to 2024) |

6.4% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Integration of Smart Sensors in Industry 4.0 Automation

The ongoing expansion of Industry 4.0 across manufacturing hubs is pushing companies to deploy inductive proximity sensors for real-time monitoring and predictive maintenance. These sensors enable precise object detection and machine feedback, essential for automated assembly and robotics.

For example, in 2024, Siemens and Schneider Electric upgraded their automation systems with IO-Link-enabled inductive sensors to improve connectivity and diagnostics in industrial setups. The surging use of smart factories in Europe and Asia Pacific, supported by government-led digital transformation programs, continues to create high demand for novel and data-capable inductive sensors that improve efficiency and reduce downtime.

Expanding Automotive Manufacturing Embracing Sensor-based Precision

Automotive manufacturers are extensively integrating inductive proximity sensors into vehicle assembly and inspection processes to improve accuracy and safety. These sensors are used in robotic welding, engine assembly, and position monitoring applications.

In 2024, Bosch and Continental expanded their use of inductive sensors to improve automation in EV component production lines. The ongoing rise in electric vehicle manufacturing and the shift toward contactless sensing for harsh environments have made inductive sensors indispensable in automotive automation systems worldwide.

Barrier Analysis - Shorter Detection Range Compared to Optical Sensors

One of the key challenges for inductive proximity sensors is their limited sensing distance, which restricts their use to close-range metal detection. Unlike photoelectric sensors that can detect objects from several meters away, inductive sensors typically operate within a few millimeters to centimeters. This limitation becomes necessary in applications requiring long-range object recognition, such as packaging or logistics automation.

Several factories are now combining inductive and optical sensors to balance precision and coverage. However, in scenarios demanding greater flexibility and non-metal object detection, photoelectric and capacitive sensors continue to replace inductive models.

Intense Cost Competition from Asia Pacific-based Manufacturers

The increasing presence of low-cost Asia Pacific-based suppliers, particularly from China and South Korea, has created intense pricing pressure in the field of inductive sensors. These manufacturers deliver sensors with basic functionality at significantly lower prices, challenging established Europe- and U.S.-based brands.

Various premium sensor companies face shrinking margins and are compelled to differentiate through unique features such as IO-Link connectivity or improved housing durability. While this competition broadens market access for small-scale industries, it also augments commoditization, making it difficult for global players to sustain high-end pricing strategies.

Opportunity Analysis - Integration into Smart Farming Equipment

The adoption of inductive proximity sensors in agricultural machinery is surging as farming becomes more data-driven and automated. These sensors are being integrated into seeders, tillers, and harvesting machines to measure metal component positions and ensure precise depth control during planting or soil preparation.

For instance, in 2024, John Deere began broadening the use of inductive sensors in its precision agriculture equipment to improve field efficiency and reduce mechanical wear. Their durability against dust, vibration, and moisture makes them ideal for rugged outdoor operations, supporting the broad shift toward smart farming technologies.

Rising Use of Non-contact Sensing for Extreme Industrial Settings

Industries such as oil and gas, mining, and marine are now turning toward inductive proximity sensors for reliable position sensing in challenging environments. These sensors operate efficiently under exposure to oil, heat, and high pressure, where optical or mechanical sensors often fail.

For example, offshore drilling systems and metal processing units now rely on sealed, corrosion-resistant inductive sensors to monitor equipment movement without physical contact. This ability to perform consistently in harsh or contaminated conditions presents new opportunities for manufacturers developing superior, high-temperature, and stainless-steel-encased sensor variants.

Category-wise Analysis

Housing Type Insights

Cylindrical designs are poised to capture around 43.5% of the share in 2025, supported by their ease of installation, compatibility with threaded mounting, and adaptability to different machine designs. Their uniform shape allows quick replacement during maintenance without modifying existing setups. Manufacturers such as Pepperl+Fuchs and ifm continue to introduce stainless-steel cylindrical sensors with IP69K protection for use in washdown and metal-cutting environments, strengthening their dominance in legacy and new automation systems.

Rectangular inductive sensors are gaining impetus because they deliver better surface mounting flexibility in space-constrained environments. Their flat profile enables installation on conveyor belts, packaging systems, and assembly lines where cylindrical sensors cannot fit. For example, Balluff recently extended its compact rectangular inductive series for robotic end-effectors, helping optimize limited mounting space without sacrificing sensing accuracy.

Sensing Range Insights

Medium-range devices dominate with approximately 46.3% of the share in 2025, as they provide a balance between detection distance and precision for most industrial applications. They work efficiently in metal detection within 5 to 15 mm, suitable for assembly lines, CNC machines, and robotic fixtures. These sensors minimize false triggering while maintaining stable performance, making them ideal for repetitive operations in manufacturing and automotive plants.

The demand for long-range sensors is increasing as factories adopt automation for large metal components and heavy machinery. Extended-range variants, some providing up to 40 mm detection, reduce the requirement for exact alignment and allow safe installation at a distance from moving parts. In 2024, Omron introduced its E2E NEXT long-range models, which drastically extend sensing distance without sacrificing precision, addressing industrial demands for superior operational flexibility and safety.

End-user Industry Insights

Industrial machinery and robotics dominate with nearly 37.8% of the share in 2025, since inductive sensors are essential for detecting metal parts, guiding robotic movement, and ensuring machine safety. They provide non-contact position feedback essential in welding robots, material handling arms, and automated presses. As robotic deployments increase in automotive and electronics sectors, manufacturers are integrating inductive sensors for cycle-time optimization and error prevention in high-speed operations.

In the energy and utilities sector, inductive sensors are important for detecting valve positions, monitoring turbine components, and managing equipment in high-temperature or high-vibration environments. Their resistance to oil, dust, and electromagnetic interference makes them more reliable than optical or mechanical alternatives. Power generation plants and wind turbine systems increasingly use corrosion-resistant inductive sensors to ensure continuous operation and minimize maintenance downtime in harsh outdoor and offshore conditions.

Regional Insights

Asia Pacific Inductive Proximity Sensors Market Trends

Asia Pacific is estimated to account for a share of approximately 39.2% in 2025, backed by the ongoing expansion of industrial automation and robotics. China dominates both production and consumption in this market. The country not only manufactures a large share of global inductive sensors but also integrates them across its expanding EV and electronics industries. Japan and South Korea continue to favor high-end, precision-based sensors, supported by leading players, including Omron and Keyence. These countries focus on miniaturized and intelligent sensors with IO-Link and diagnostic functions to meet unique robotics and semiconductor production requirements.

India and Southeast Asia are emerging as promising markets, where rising investments in smart factories and ‘Make in India’ initiatives are encouraging local sensor manufacturing and adoption. Several regional companies are providing affordable alternatives to global brands, catering to small and mid-sized manufacturers seeking cost-efficient automation solutions. However, Asia Pacific still faces challenges such as price sensitivity, limited technical support in rural industrial areas, and competition from low-cost China-based suppliers.

North America Inductive Proximity Sensors Market Trends

In North America, the demand for inductive proximity sensors is rising steadily, propelled by the modernization of manufacturing and the shift toward smart factories. Automotive, aerospace, packaging, and metalworking industries are increasingly replacing mechanical limit switches with inductive sensors to improve precision and reliability. The region’s focus on Industry 4.0 and automation upgrades is pushing companies to adopt sensors that support real-time diagnostics and digital connectivity.

For example, several U.S.-based manufacturers are adopting IO-Link-enabled sensors to monitor equipment health and reduce unplanned downtime. Leading companies such as Rockwell Automation, Honeywell, and Turck continue to dominate the regional market. They provide rugged and long-life sensor solutions suited for harsh industrial environments. Most manufacturers prioritize sensor reliability and certification, as equipment downtime and safety compliance are key concerns. Products meeting UL and CSA standards are preferred, specifically in sectors such as automotive assembly and heavy machinery.

Europe Inductive Proximity Sensors Market Trends

Europe’s market is influenced by its mature manufacturing base, heavy regulation, and push toward smart or sustainable factories. Germany, France, Italy, and the U.K. are leading adopters, with sensors widely used in automotive production lines, robotics, packaging, and aerospace manufacturing. Europe’s strict industrial and safety standards, including CE and RoHS compliance, have encouraged the use of high-quality and durable sensors capable of performing reliably in harsh conditions.

Germany-based manufacturers, including SICK, ifm, and Pepperl+Fuchs, continue to lead Europe with unique sensors that deliver diagnostic capabilities and support predictive maintenance. The ongoing Industry 4.0 movement in Europe has further created high demand for smart sensors with digital communication interfaces such as IO-Link. These sensors enable continuous monitoring and data sharing, allowing manufacturers to optimize machine performance and reduce downtime.

Competitive Landscape

The global inductive proximity sensors market is dominated by global automation leaders such as Omron, Keyence, Pepperl+Fuchs, SICK, Balluff, Rockwell Automation, and Honeywell. These companies focus on innovation and quality, targeting high-end applications in automotive, industrial automation, and robotics. They maintain an edge by delivering sensors with unique features such as IO-Link connectivity, improved durability, and self-diagnostic capabilities. Small-scale companies from China, Japan, and South Korea compete on cost and cater to local OEMs that prioritize affordability over novel functionality.

Business Strategies

Most established companies in the inductive proximity sensors market are now competing beyond hardware by integrating predictive maintenance tools and Industry 4.0 compatibility into their ranges. This shift toward smart sensing solutions allows manufacturers to differentiate through software and service value rather than just physical performance. The market has seen fewer mergers and acquisitions in recent years, as leading firms prefer to strengthen their presence through technological upgrades rather than consolidation.

Key Industry Developments

- In April 2025, Triad introduced SICK’s novel SIG300 Universal IO-Link Master. It is a powerful solution designed to revolutionize how individuals connect, control, and optimize production.

- In March 2025, Omron Corporation invested US$150 Million to broaden its Kusatsu factory in Japan. The expansion included new Application-Specific Integrated Circuit (ASIC) lines and automated test cells.

Companies Covered in Inductive Proximity Sensors Market

- Rockwell Automation, Inc.

- Pepperl+Fuchs SE

- Eaton Corporation plc

- Panasonic Holdings Corporation (Panasonic Industry Co., Ltd.)

- SICK AG

- Delta Electronics, Inc.

- Omron Corporation

- Datalogic S.p.A.

- Autonics Corporation

- Riko Optoelectronics Technology Co., Ltd.

- Hans Turck GmbH & Co. KG

- Fargo Controls, Inc.

- Honeywell International Inc.

- Keyence Corporation

- Euchner GmbH + Co. KG

- K.A. Schmersal GmbH & Co. KG

- Balluff GmbH

- Banner Engineering Corp.

- IFM Electronic GmbH

- Baumer Holding AG

Frequently Asked Questions

The inductive proximity sensors market is projected to reach US$1.6 Billion in 2025.

Expanding use in EV manufacturing and rising focus on predictive maintenance are the key market drivers.

The inductive proximity sensors market is poised to witness a CAGR of 7.2% from 2025 to 2032.

Integration of self-diagnostic capabilities and development of extended-range variants are the key market opportunities.

Rockwell Automation, Inc., Pepperl+Fuchs SE, and Eaton Corporation plc are a few key market players.