- Pharmaceuticals

- Hepatitis C Treatment Market

Hepatitis C Treatment Market Size, Share, and Growth Forecast, 2025 - 2032

Hepatitis C Treatment Market By Treatment Type (Direct-Acting Antivirals, Interferon-Based Therapies, Others), Clinical Indication (Pan-Genotypic, Genotype-Specific, Others), Distribution Channel, and Regional Analysis for 2025 - 2032

Hepatitis C Treatment Market Size and Trends Analysis

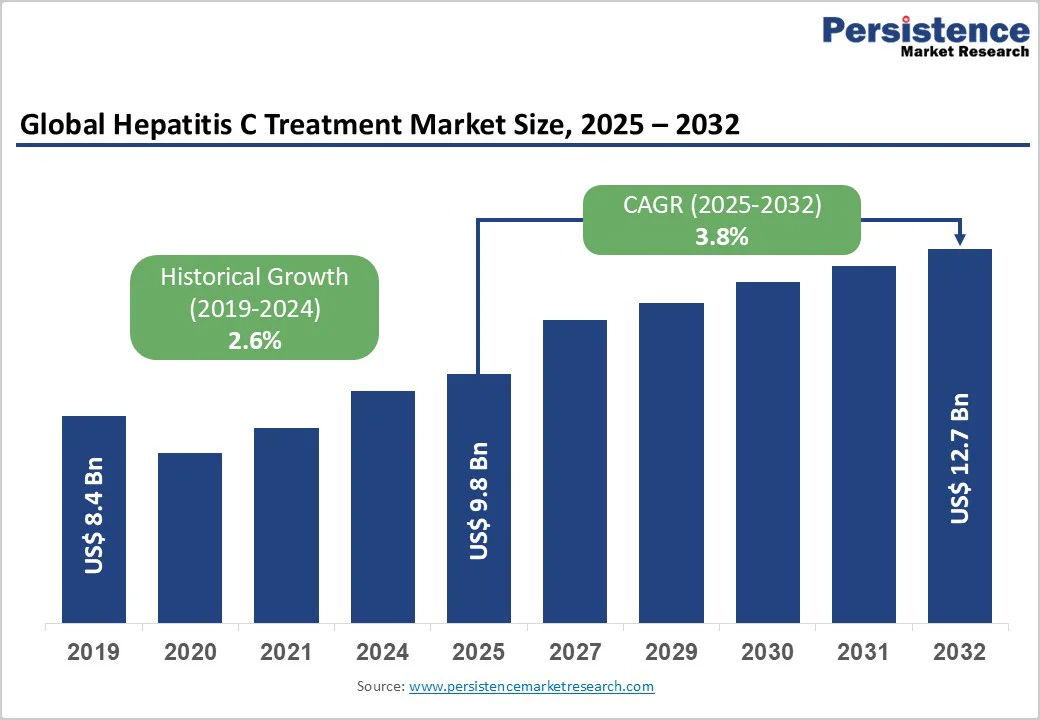

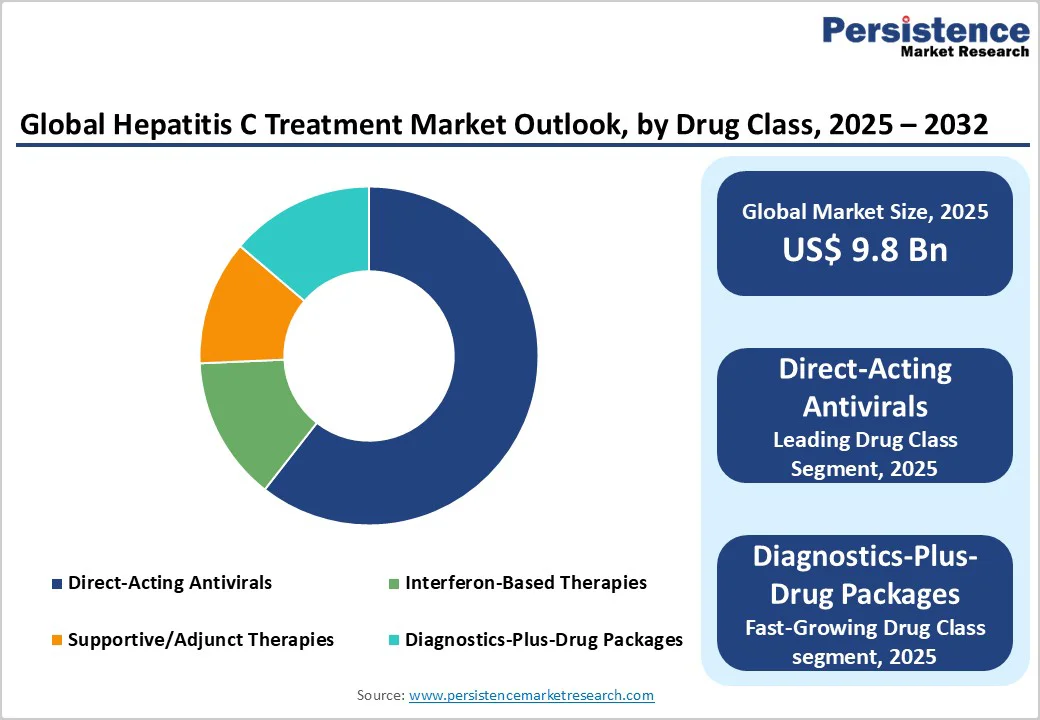

The global hepatitis C treatment market size is likely to be valued at US$9.8 Billion in 2025 and is expected to reach US$12.7 Billion by 2032, growing at a CAGR of 3.8% during the forecast period from 2025 to 2032, driven by the widespread adoption of highly effective direct-acting antivirals (DAAs), many of which offer cure rates above 95% with short 8-12-week regimens.

National elimination programs, expanded screening campaigns, and improvements in treatment eligibility criteria further enlarge the treatable population. In parallel, greater use of generic versions in large public tenders has broadened access in low- and middle-income countries, stabilizing global treatment volumes even as certain high-income markets mature.

Key Industry Highlights

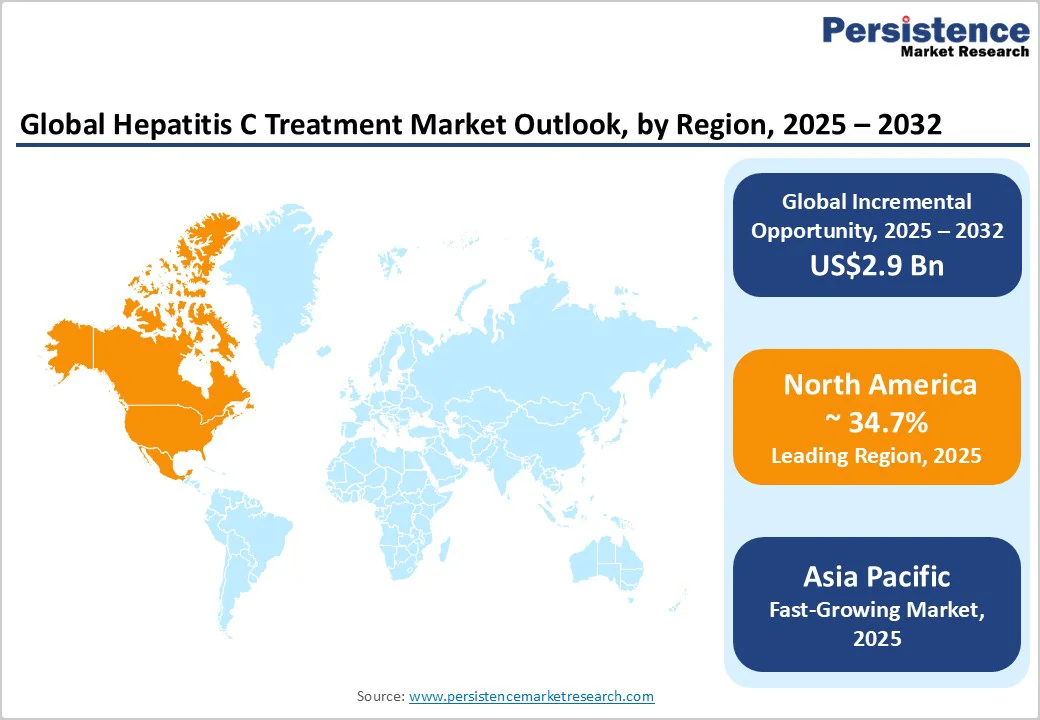

- Leading Region: North America holds around 34.7% of the market, supported by strong reimbursement systems, rapid adoption of pan-genotypic DAAs, and widespread screening programs that sustain steady treatment volumes.

- Fastest-growing Region: Asia Pacific is driven by expanding generic access, national elimination campaigns, and large untreated populations entering accelerated treatment pathways.

- Investment Plans: Industry and public-sector programs are channeling capital into diagnostics expansion, point-of-care platforms, and integrated digital-plus-clinical care models, enabling faster testing-to-treatment transitions in high-burden regions.

- Dominant Drug Class: Direct-acting antivirals command approximately 66.7% of total market value, reflecting their high cure rates, simplified regimens, and broad adoption across both high-income and middle-income health systems.

- Leading Clinical Indication: Pan-genotypic therapies represent around 64.7% of the global treated population, as they eliminate genotype-specific decision steps and support streamlined procurement and national elimination strategies.

| Key Insights | Details |

|---|---|

| Hepatitis C Treatment Market Size (2025E) | US$9.8 Bn |

| Market Value Forecast (2032F) | US$12.7 Bn |

| Projected Growth (CAGR 2025 to 2032) | 3.8% |

| Historical Market Growth (CAGR 2019 to 2024) | 2.6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Clinical Effectiveness of Daas and Expanded Treatment Guidelines

Direct-acting antivirals transformed Hepatitis C care, delivering sustained virologic response rates above 95% with short, well-tolerated 8-12-week regimens. Pan-genotypic options simplify prescribing, expand eligibility, and support rapid test-and-treat models. Countries adopting broad screening and streamlined initiation have achieved major increases in treatment uptake and programmatic impact.

Global Elimination Targets and Public Procurement Programs

Global viral hepatitis elimination goals have driven countries to scale screening, expand public awareness, and implement coordinated procurement programs. These efforts uncover undiagnosed cases, lower affordability barriers, and generate predictable multi-year demand.

Large tenders and donor-supported purchasing enable stable pricing and incentivize manufacturers to sustain capacity. Nations adopting structured elimination pathways report sharp rises in diagnosis rates, reduced treatment backlogs, and steady long-term treatment volumes supported by aligned policies and health-system planning.

Market Access via Voluntary Licensing and Generic Scale-Up

Voluntary licensing and strong generic manufacturing capacity have greatly expanded access to Hepatitis C therapies. Large-scale production of sofosbuvir-, velpatasvir-, and pibrentasvir-based generics has reduced prices and enabled national programs to treat patients at scale.

These agreements extend reach in low-resource settings and support high-volume, lower-margin models. For suppliers, reduced premium-market pricing is offset by stable, large public-sector procurement, reshaping global revenue distribution across therapy classes.

Barrier Analysis - Shrinking Prevalent Pool and Demand Depletion

As DAAs achieve high cure rates, the number of chronically infected individuals steadily declines, especially in countries with early large-scale adoption. This “depletion effect” reduces the long-term number of new treatment initiations and compresses market growth after initial surges.

Some markets that once recorded high annual treatment volumes now show a year-over-year decline in new starts, pushing suppliers to target underserved regions, develop new formulations, or expand into younger age groups to maintain revenue streams.

Pricing Pressure and Payer Negotiation

Originator therapies face significant pricing pressure from generics and public procurement systems. High initial list prices led to substantial discounting in high-income markets, while competitive public tenders in low- and middle-income markets maintain strict price limits.

These pressures reduce revenue per patient and compress margins even as treatment volumes increase. Manufacturers must balance portfolio strategies, prioritizing markets with stronger reimbursement models and deploying contracting tools to preserve value within increasingly competitive and price-sensitive environments.

Opportunity Analysis - Scaling Diagnostics and Test-And-Treat Programs

Many countries still lack adequate diagnostic coverage for Hepatitis C. Expanding point-of-care testing and integrating simplified test-and-treat models can significantly enlarge the active treatment population. Pilot programs show that reducing the time between diagnosis and therapy initiation improves uptake and allows health systems to treat harder-to-reach groups.

Bundling diagnostics and therapeutics within unified tenders can produce multi-year procurement opportunities, especially in regions aiming for national elimination. Suppliers that provide end-to-end care pathways, including testing technologies, rapid referral mechanisms, and reliable drug supply, stand to benefit the most.

Pediatric and Acute HCV Indications + Shortened Regimens

Recent regulatory expansions allow the treatment of younger pediatric groups and early-stage acute infections. These approvals increase the eligible population and support earlier initiation, which reduces onward transmission and potentially lowers overall disease burden.

Evidence supporting shorter treatment durations, sometimes eight weeks or fewer, reduces costs for health systems and improves adherence. Pediatric programs integrated into maternal and child health platforms can experience steep growth from a low base, making this segment an important future opportunity for both branded and generic suppliers.

Category-wise Analysis

Drug Class Insights

Direct-acting antivirals dominate with a market share of 66.7%, due to their high cure rates, favorable safety profiles, and strong endorsement in treatment guidelines. They capture the bulk of global revenue as they are used widely in both high-income and middle-income settings. In wealthier markets, branded versions retain a strong share due to their clinical reputation and streamlined reimbursement.

In lower-income regions, generics supply the same molecules at significantly lower prices, enabling large public programs to treat high volumes. The segment benefits from ongoing preference for pan-genotypic combinations, which simplify both clinical decision-making and national procurement processes. DAAs remain central to elimination strategies, ensuring steady demand even in maturing markets.

Bundled diagnostics-plus-drug packages represent the fastest-growing segment, driven by large-scale adoption in low-resource regions. As voluntary licensing expands and manufacturing efficiency improves, prices continue to fall, encouraging countries to adopt high-volume testing and treatment campaigns.

Bundled procurement, where suppliers combine drugs with testing tools, training, or software, is gaining traction as it reduces time-to-treatment and helps governments execute simplified care pathways. Growth rates in this segment exceed those of branded therapies due to larger untreated populations and strong donor or government-backed procurement mechanisms.

Genotype Insights

Pan-genotypic regimens lead the market, holding a share of 64.7% as they treat all major Hepatitis C genotypes with a single combination, eliminating the need for genotype testing in many settings. This greatly simplifies procurement and care delivery. Countries pursuing elimination targets favor pan-genotypic therapies to streamline logistics and minimize diagnostic complexity.

These regimens often command higher pricing in high-income markets due to their convenience and robust clinical evidence. The ability to treat diverse populations with one product makes pan-genotypic options the backbone of national treatment guidelines and a consistently high-value segment.

The market for acute Hepatitis C treatment is expanding rapidly due to new approvals and increasing detection efforts. Acute infection treatment supports early intervention and may prevent further transmission, creating a strong case for integrating rapid diagnosis with immediate therapeutic initiation.

Recent regulatory updates enabling the use of short-course pan-genotypic regimens in acute cases have accelerated adoption across several regions. As screening programs broaden and high-risk groups undergo more frequent testing, the number of identified acute cases is rising, strengthening demand for streamlined, fast-acting therapies.

Regional Insights

North America Hepatitis C Treatment Market Trends - Digital Access & State-Led Elimination Drives

North America remains the largest regional Hepatitis C market, holding an estimated 34.7% share, driven by strong uptake of branded direct-acting antivirals (DAAs), broad insurance coverage, and early adoption of curative therapies. The U.S. market operates within a complex multi-payer environment that includes commercial insurers, Medicare, Medicaid, and federal programs.

While most payers list modern DAAs on formularies, prior authorization rules, fibrosis criteria, and state-level restrictions continue to shape treatment initiation patterns. Screening initiatives targeting older adults, high-risk groups, and underserved communities help sustain treatment volumes by continuously identifying new candidates for therapy.

Regional growth is reinforced by updated clinical guidelines, expanded pediatric indications, and ongoing efforts to decentralize diagnostics through community clinics, pharmacies, and telehealth channels.

Several U.S. states have launched elimination strategies that temporarily boost treatment starts and create opportunities for companies offering integrated testing-to-treatment solutions. The investment landscape has shifted toward digital health, remote monitoring, and care-coordination platforms rather than new DAA development, given the highly effective nature of existing regimens.

Recent regional developments include state-funded elimination pilots bundling diagnostics and therapeutics, expansion of simplified treatment pathways, collaborations deploying rapid screening tools, and health-system adoption of digital adherence platforms. Partnerships between pharmacy chains and telehealth providers now further improve access through same-day testing and prescribing.

Europe Hepatitis C Treatment Market Trends - Centralized Procurement & Community-Based Screening

Europe is the second-largest Hepatitis C market, supported by strong public health systems, comprehensive reimbursement policies, and coordinated national elimination strategies. Major Western European countries, including Germany, the U.K., France, Italy, and Spain, maintain high treatment penetration through structured procurement and uniform clinical guidelines.

Although therapy prices are lower than in the U.S., they remain sufficient to support a competitive branded segment and ongoing supplier participation. Centralized price negotiations and national treatment protocols further streamline access and ensure consistency across regions.

The U.K.’s national elimination pathways, France’s and Spain’s targeted programs for high-risk groups, and Italy’s structured public-sector purchasing all contribute to steady progress toward elimination goals.

Screening integration with sexual health services and substance-use treatment increases diagnosis rates and expands the eligible treatment population. While the European Medicines Agency provides centralized approval for therapies, national health technology assessments determine reimbursement timing and final pricing, influencing adoption speeds.

Competitive tenders and multi-year procurement agreements encourage manufacturers to offer value-based pricing across branded and generic options.

Recent developments include regional screening campaigns for migrant populations, expanded prison-based treatment programs in Italy and Spain, and cross-country procurement collaborations to improve affordability. Several countries have piloted community pharmacy-based treatment initiation, while the U.K. and Nordic markets have adopted digital outcome-tracking platforms to strengthen monitoring and refine elimination strategies.

Asia Pacific Hepatitis C Treatment Market Trends - High-Burden Growth & Generic Manufacturing Strength

Asia Pacific has the world’s highest Hepatitis C disease burden, supported by strong generic manufacturing capacity and wide variation in healthcare access across economies. The region encompasses major markets such as China, India, and Japan, alongside emerging Southeast Asian countries. Asia Pacific contributes the largest global increase in treatment volume, driven by a substantial untreated population and rapidly expanding national screening programs.

India plays a pivotal role as a global hub for generic DAA production, supplying domestic public health initiatives and exporting to numerous international markets. Large-scale procurement continues to sustain high treatment volumes, while improvements in state-level screening and linkage-to-care systems strengthen domestic uptake.

In China, expanded insurance coverage, updated reimbursement policies, and broader access to branded therapies, especially in urban hospitals, have accelerated treatment initiations, with government programs increasingly extending access into rural areas.

Growth across the region is further supported by competitive pricing enabled by local manufacturing, rising public health investment, and multi-country collaboration to negotiate affordable procurement terms. Innovation activity has expanded around decentralized diagnostics, mobile screening units, and digital platforms designed to track adherence and follow-up testing.

Recent developments include nationwide screening campaigns in China, new low-cost DAA manufacturing capacity in India, and government-funded treatment programs in countries such as Indonesia and Vietnam aimed at rapidly scaling access.

Competitive Landscape

The global Hepatitis C treatment market is moderately concentrated in branded therapies and highly fragmented in generics. Originator companies dominate high-income markets with premium DAAs, while Indian and other generic manufacturers supply large-scale public tenders. Market positioning relies on IP rights, manufacturing capacity, geographic reach, and integrated diagnostic-therapeutic offerings.

High-income regions drive revenue, whereas low-income countries account for most treatment volume. Key strategies include voluntary licensing, competitive tendering, bundled diagnostics-and-treatment solutions, and lifecycle management via new indications or shorter regimens, supported by cost efficiency, diagnostic partnerships, and robust supply chains for multi-year public contracts.

Key Industry Development

- In June 2025, the U.S. FDA approved an expanded indication for Mavyret (glecaprevir/pibrentasvir), making it the first and only 8-week oral DAA therapy for treating acute Hepatitis C virus infection in adults and pediatric patients aged 3 years and older.

- In June 2025, the FDA granted MAVYRET Breakthrough Therapy Designation for acute HCV, underscoring its potential to simplify test-and-treat strategies by treating patients immediately at diagnosis.

Companies Covered in Hepatitis C Treatment Market

- Gilead Sciences

- AbbVie

- Merck & Co.

- Bristol-Myers Squibb

- Cipla

- Mylan

- Dr. Reddy’s Laboratories

- Zydus Lifesciences

- Hetero Healthcare

- Natco Pharma

- Roche

- Pfizer

- Johnson & Johnson

- Novartis

- Teva Pharmaceutical Industries

- Apotex

- Sun Pharmaceutical Industries

- Lupin

- Glenmark Pharmaceuticals

- Aurobindo Pharma

Frequently Asked Questions

The global hepatitis C treatment market is estimated at US$9.8 Billion in 2025.

By 2032, the market is expected to reach US$12.7 Billion.

Key trends include the dominance of direct-acting antivirals (DAAs), rapid scale-up of pan-genotypic therapies, expansion of generic treatment programs in low-resource regions, and rising demand for bundled diagnostics-plus-treatment packages.

Direct-acting antivirals (DAAs) lead the market, accounting for the majority of global treatment value, while pan-genotypic regimens dominate clinical usage due to simplified care pathways.

The hepatitis C treatment market is projected to grow at a CAGR of 3.8% between 2025 and 2032.

Major companies with strong treatment portfolios include Gilead Sciences, AbbVie, Bristol-Myers Squibb, Merck & Co., and Cipla.