- Medical Devices

- Hepatitis C Virus Testing Market

Hepatitis C Virus Testing Market Size, Share, and Growth Forecast 2026 - 2033

Hepatitis C Virus Testing Market by Test Type (HCV Antibody Testing, HCV Viral Load Testing, HCV Genotyping Testing), by Technique (Immunoassay-based Hepatitis C Virus Testing, Polymerase Chain Reaction-based (PCR) Hepatitis C Virus Testing, Others), End-user (Hospitals, Diagnostic Centers, Blood Donation Centers, Others), and Regional Analysis, 2026 - 2033

Hepatitis C Virus Testing Market Size and Trend Analysis

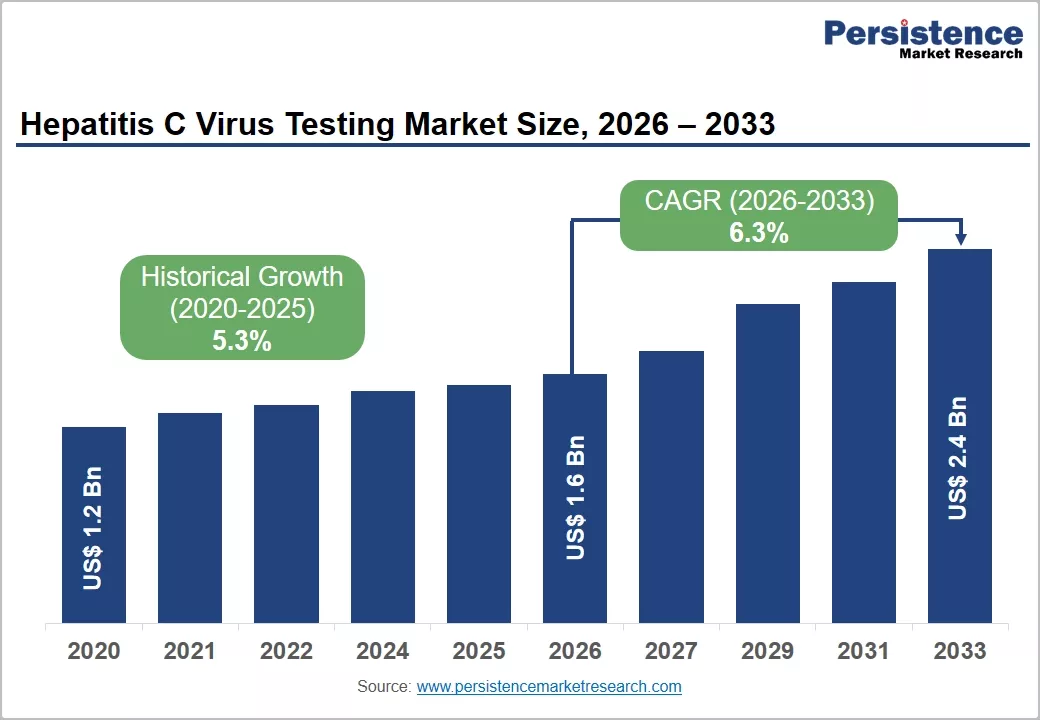

The global hepatitis C virus testing market size is expected to be valued at US$ 1.6 billion in 2026 and projected to reach US$ 2.4 billion by 2033, growing at a CAGR of 6.3% between 2026 and 2033. This steady growth is driven by the World Health Organization (WHO)'s global HCV elimination target of reducing new infections by 80% and HCV-related deaths by 65% by 2030, which is compelling governments and health systems worldwide to dramatically scale up HCV screening, diagnosis, and treatment linkage programs.

The WHO estimates that approximately 50 million people currently live with chronic HCV infection globally with the vast majority unaware of their status creating an enormous undiagnosed population that systematic public health screening initiatives, advancing point-of-care diagnostics from manufacturers including Abbott, Roche Diagnostics, and OraSure Technologies, and expanding health insurance coverage in emerging economies are collectively mobilizing into a large, growing addressable testing volume base throughout the forecast period.

Key Market Highlights

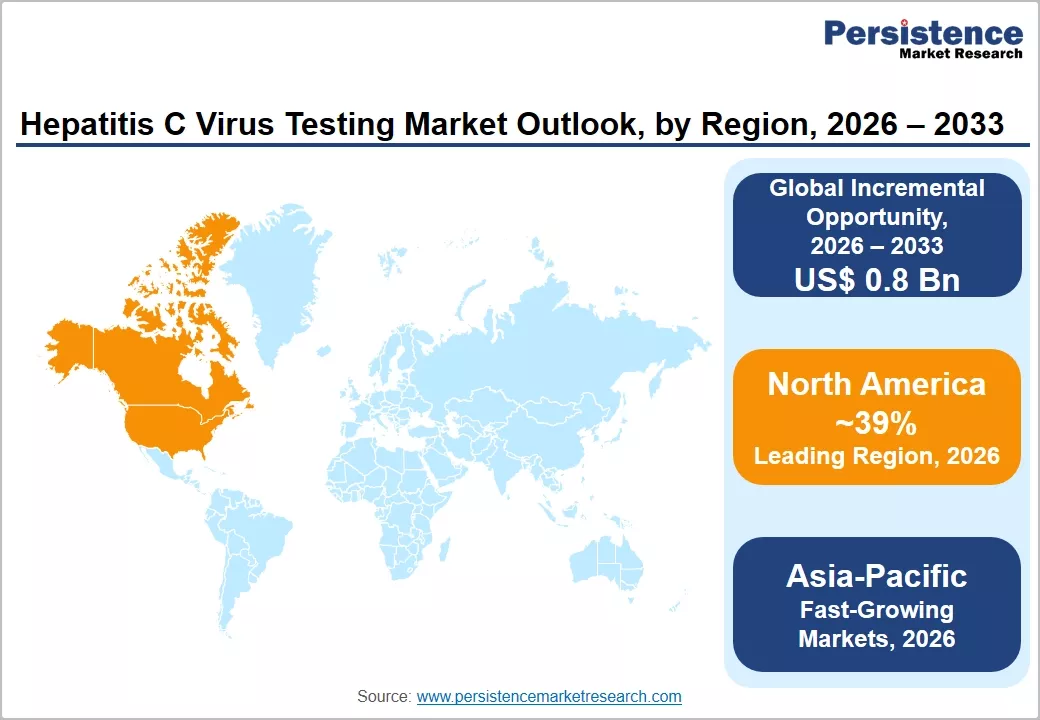

- North America leads the global HCV Testing market with approximately 39% revenue share in 2026, anchored by the CDC/USPSTF Grade B universal adult HCV screening recommendation mandating insurance coverage under the ACA, and HHS national elimination program infrastructure expanding community and primary care testing access.

- Asia Pacific is the fastest-growing HCV testing market, driven by China's 10 million chronically infected individuals, India's NVHCP national screening program deploying rapid antibody tests at district hospitals, and WHO-supported elimination roadmaps accelerating HCV diagnostic investment across ASEAN markets.

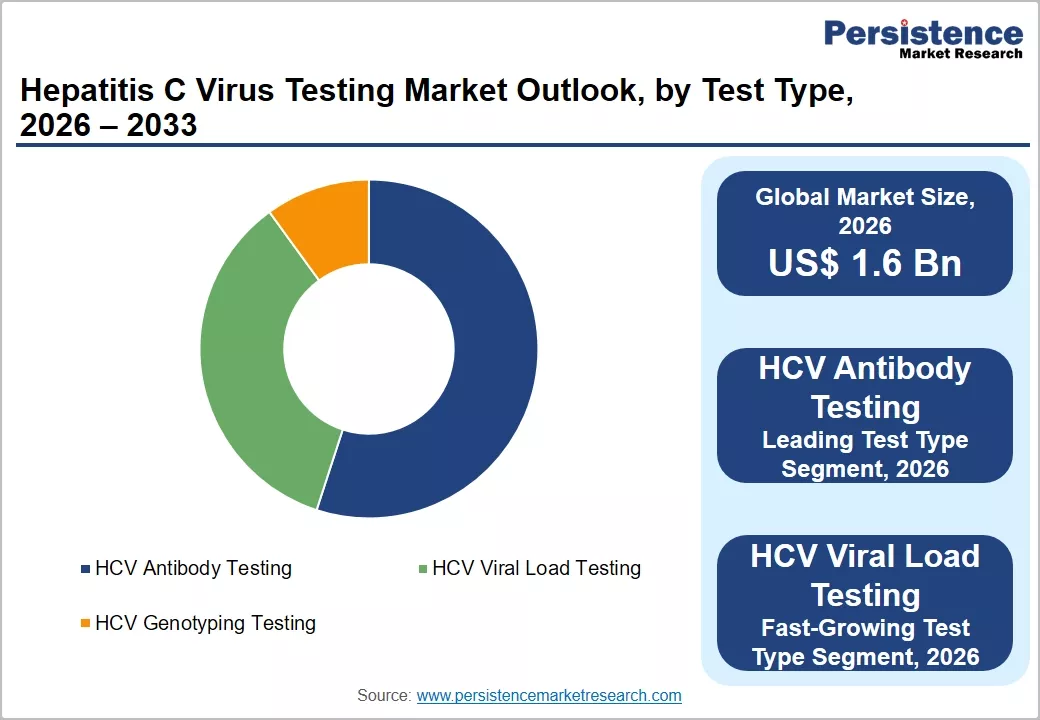

- HCV Antibody Testing dominates the test type category with approximately 55% market share in 2025, anchored by USPSTF, WHO, and ECDC universal screening algorithm mandates requiring antibody tests as the first-line diagnostic step for all adults in target populations across major high-income national screening programs.

- HCV Viral Load Testing is the fastest-growing test type segment through 2033, driven by the global scale-up of DAA therapy achieving 95%+ cure rates with 9.4 million people initiated on treatment globally (WHO 2022), each generating three to five viral load test events across baseline, monitoring, and SVR12/SVR24 assessment milestones.

- Point-of-care HCV RNA testing combining antibody screening and viremia confirmation in a single visit represents the most transformative commercial opportunity, addressing the critical HCV linkage-to-care gap in LMIC and community settings, endorsed by UNITAID and Médecins Sans Frontières for large-scale public health deployment.

Market Dynamics

Drivers - WHO 2030 Hepatitis C Elimination Goals Driving Unprecedented National Screening Program Expansion

The World Health Organization's Global Health Sector Strategy on Viral Hepatitis 2016–2021 and its successor frameworks targeting HCV elimination by 2030 have created a binding global policy mandate that is directly translating into expanded national HCV testing programs across both high-income and emerging market countries. The WHO estimates that only 21% of the 50 million people living with HCV had been diagnosed as of 2022, highlighting a massive unmet testing gap that elimination programs must close.

The U.S. Department of Health and Human Services (HHS) launched its National Viral Hepatitis Action Plan, recommending universal HCV screening for all adults aged 18 to 79 under CDC guidelines updated in 2020. Similar universal screening recommendations have been adopted across EU member states under the European Centre for Disease Prevention and Control (ECDC) hepatitis action framework, directly expanding the addressable testing population and generating sustained volume growth for HCV diagnostics manufacturers.

Restraints - Stigma and Testing Awareness Gaps Suppressing HCV Screening Uptake in High-Risk Populations

Despite expanded universal screening recommendations, HCV-associated stigma linked to the virus's historical association with intravenous drug use remains a persistent barrier suppressing testing uptake among the highest-prevalence populations. The CDC estimates that people who inject drugs (PWID) account for approximately 60% of new HCV infections in the United States, yet this population demonstrates the lowest healthcare engagement rates. Studies published in the Lancet Infectious Diseases document that fear of stigmatization, criminalization of drug use in many jurisdictions, and distrust of healthcare systems substantially reduce voluntary HCV testing among PWID, limiting the effectiveness of universal screening policies in reaching the populations where HCV burden and unmet testing need are greatest.

Opportunities - HCV Viral Load Testing: Fastest-Growing Segment Driven by Treatment Expansion and SVR Monitoring Protocols

HCV Viral Load Testing (quantitative HCV RNA assays) represents the fastest-growing test type segment in the HCV testing market, propelled by the global scale-up of DAA therapy programs that mandate RNA quantification at multiple treatment milestones. Confirmatory HCV RNA testing at diagnosis, baseline viral load assessment pre-treatment, and post-treatment SVR12 and SVR24 assessment for all treated patients generate a cascading test volume expansion as more patients enter DAA therapy.

The WHO reported that global HCV treatment initiation increased to 9.4 million people by 2022, with each patient generating three to five viral load test events. Leading platforms including Roche's cobas HCV for use on the cobas 6800/8800 Systems and Abbott's RealTime HCV Viral Load assay dominate institutional viral load testing, and next-generation digital PCR platforms from Thermo Fisher and QIAGEN are creating additional high-sensitivity quantification options that command premium pricing in confirmatory diagnostic settings.

Category-wise Analysis

Test Type Insights

HCV antibody testing leads the HCV testing market by test type, commanding approximately 55% of global revenues in 2026. HCV antibody tests serve as the foundational first-line screening tool in all HCV testing algorithms recommended by WHO, CDC, and ECDC, detecting IgG antibodies produced in response to HCV infection in the majority of exposed individuals.

The broad deployment of fourth-generation enzyme immunoassays (EIAs) and chemiluminescent immunoassay (CLIA) platforms by Abbott (ARCHITECT anti-HCV), Roche (Elecsys anti-HCV II), and Siemens Healthineers (ADVIA Centaur HCV) across high-throughput hospital and blood bank laboratory settings generates the highest aggregate test volume of any HCV diagnostic category. Universal screening recommendations targeting all adults encompassing hundreds of millions of individuals annually across North America and Europe anchor antibody testing as the sustained market volume leader throughout the forecast period.

Technique Insights

Immunoassay-based hepatitis C virus testing leads the technique segmentation, representing approximately 62% of global HCV test market revenues in 2026. Immunoassays encompassing enzyme-linked immunosorbent assays (ELISA), chemiluminescent immunoassays (CLIA), and rapid immunochromatographic assays constitute the dominant technical approach for first-line HCV antibody screening due to their high sensitivity, scalability on automated laboratory platforms, low per-test cost, and established performance data within regulatory-approved testing algorithms.

Major automated immunoassay platforms from Abbott (ARCHITECT), Roche (cobas e 801), Siemens Healthineers (ADVIA Centaur XPT), and bioMérieux (VIDAS) process thousands of HCV antibody samples per hour with regulatory-cleared performance specifications, making immunoassay the default technique for high-volume screening environments including hospital laboratories, blood donation centers, and national population screening programs.

Regional Insights

North America Hepatitis C Virus Testing Market Trends and Insights

North America dominates the HCV testing market due to high diagnosis rates, strong screening infrastructure, and widespread molecular testing adoption. The region benefits from national elimination strategies, especially in the United States, where the CDC estimates over 2.4 million people live with chronic HCV. Large-scale screening recommendations for adults aged 18–79 and integration of HCV testing in primary care drive consistent demand. High adoption of PCR-based viral load testing further strengthens market dominance. The regional market is expected to reach US$ 600 Mn by 2026, supported by advanced diagnostic infrastructure and reimbursement coverage.

U.S. Hepatitis C Virus Testing Market Trends and Insights

The United States is the primary contributor, driven by CDC-recommended universal HCV screening and strong insurance coverage for diagnostics. The U.S. has one of the highest diagnosed patient pools in developed markets, with rising testing in emergency departments and primary care settings. Blood donation screening is mandatory nationwide, supporting consistent antibody and RNA testing volumes. The market is expected to reach US$ 450 Mn by 2026, driven by increasing uptake of reflex RNA testing and expansion of point-of-care molecular diagnostics across hospitals and urgent care centers.

Canada Hepatitis C Virus Testing Market Trends and Insights

Canada is witnessing faster growth due to provincial hepatitis elimination programs and expanding access to diagnostic services in remote populations. The Public Health Agency of Canada reports ongoing efforts to reduce undiagnosed HCV cases through targeted screening in high-risk groups. Indigenous population-focused healthcare initiatives and expansion of laboratory networks are increasing testing penetration. The country is expected to grow at a CAGR of 6.9%, supported by improved molecular diagnostic access and integration of HCV screening into routine healthcare checkups.

Europe Hepatitis C Virus Testing Market Trends and Insights

Europe remains a major HCV testing market due to strong universal healthcare systems, government-led elimination programs, and standardized diagnostic guidelines across EU member states. The European Centre for Disease Prevention and Control (ECDC) estimates around 3.9 million people living with chronic HCV in Europe. National screening campaigns and blood safety regulations support stable demand for both antibody and PCR-based testing. The regional market is expected to reach US$ 400 Mn by 2026, with a steady adoption of molecular diagnostics and increasing focus on elimination targets set by WHO.

Germany Hepatitis C Virus Testing Market Trends and Insights

Germany leads the European market due to advanced healthcare infrastructure, high diagnostic penetration, and strong insurance reimbursement policies. Routine screening in hospitals and specialty clinics is widely implemented. The Robert Koch Institute supports systematic surveillance and testing programs, contributing to early detection rates. Germany has a well-established laboratory network enabling high-volume immunoassay and PCR testing. The market is expected to reach US$ 150 Mn by 2026, driven by increasing adoption of reflex RNA testing and integration of HCV screening into chronic disease management programs.

Italy Hepatitis C Virus Testing Market Trends and Insights

Italy is among the fastest-growing markets due to government-led hepatitis elimination initiatives and historical HCV burden in older populations. The Italian Ministry of Health has implemented nationwide screening programs targeting individuals born between 1969 and 1989. Expansion of hospital-based molecular diagnostics and increasing awareness campaigns are improving detection rates. The country is expected to grow at a CAGR of 5.8%, supported by scaling up of universal screening programs and increased access to antiviral treatment-linked testing pathways.

Asia Pacific Hepatitis C Virus Testing Market Trends and Insights

Asia-Pacific is the fastest-growing region due to its large undiagnosed population, improving healthcare infrastructure, and rising adoption of molecular diagnostics. WHO estimates that Asia accounts for a significant proportion of global HCV burden, particularly in China, India, and Southeast Asia. Increasing government screening initiatives and expansion of laboratory networks are driving demand for both antibody and RNA testing. The region is expected to grow rapidly with a CAGR of 7.4%, higher than the global average of 6.3%, making it the key growth engine.

China Hepatitis C Virus Testing Market Trends and Insights

China leads the Asia Pacific HCV testing market due to large population size and national infectious disease screening programs. The Chinese CDC has expanded hepatitis surveillance and blood donor screening nationwide, significantly increasing diagnostic volumes. Hospital modernization and expansion of PCR laboratories have improved access to viral load testing. China is expected to reach US$ 200 Mn by 2026, driven by increasing integration of HCV screening into routine health check-ups and growing awareness of antiviral treatment availability under national health reforms.

India Hepatitis C Virus Testing Market Trends and Insights

India is the fastest-growing market in the region due to government initiatives such as the National Viral Hepatitis Control Program (NVHCP), which promotes free or low-cost testing in public healthcare facilities. Increasing awareness, expansion of diagnostic labs in tier-2 and tier-3 cities, and rising adoption of point-of-care antibody tests are driving growth. The country is expected to grow at a CAGR of 8.2%, supported by scaling molecular diagnostics infrastructure and increasing treatment linkage after diagnosis.

Competitive Landscape

The global Hepatitis C Virus Testing market is moderately consolidated, with Roche Diagnostics, Abbott Laboratories, and Siemens Healthineers commanding the dominant share of high-throughput automated immunoassay and molecular HCV testing revenues through their established instrument installed bases in hospital and blood bank laboratory settings.

Key competitive differentiators include WHO prequalification for LMIC use, FDA 510(k) clearance breadth across test types, and integrated testing menu on multiplex infectious disease platforms. OraSure Technologies leads the POC segment through its FDA-cleared OraQuick platform. Competitive strategies increasingly encompass combination antibody/RNA reflex testing workflows, digital health laboratory connectivity, and LMIC access pricing programs. bioMérieux, Grifols, and Fujirebio compete effectively in specialized blood screening and molecular confirmation segments.

Key Developments:

- May 2026: AbbVie announced that the Committee for Medicinal Products for Human Use (CHMP) of the European Medicines Agency had issued a positive opinion recommending approval of MAVIRET® (glecaprevir/pibrentasvir) for the treatment of acute hepatitis C virus (HCV) infection.

- May 2026: Abbott Laboratories expanded its Alinity m HCV real-time PCR assay's regulatory clearances to include additional European CE-IVD and ANVISA (Brazil) certifications, extending the platform's global regulatory footprint for high-throughput HCV viral load testing across North American, European, and Latin American markets.

- June 2025: A recent study had reported evidence suggesting the presence of Hepatitis C virus (HCV) in cells lining the human brain, expanding scientific understanding of the virus beyond its traditionally recognized liver-specific infection.

Companies Covered in Hepatitis C Virus Testing Market

- OraSure Technologies, Inc.

- Abbott Laboratories Inc.

- Siemens Healthcare GmbH

- Bio Rad Laboratories Inc.

- Ortho Clinical Diagnostic Inc. (Johnson & Johnson)

- QIAGEN N.V.

- Thermo Fisher Scientific Inc.

- Roche Diagnostics (F. Hoffman-La Roche Ltd.)

- Hologic, Inc.

- Becton, Dickinson and Company

- Fujirebio

- bioMérieux

- Grifols

- Luminex Corporation

- Others

Frequently Asked Questions

The global Hepatitis C Virus Testing market is estimated to be valued at US$ 1.6 billion in 2026.

Rising HCV prevalence, expanded screening programs, improved diagnostics, blood safety regulations, and antiviral treatment uptake.

North America leads with approximately 39% of global revenues in 2025.

Expansion of point-of-care molecular testing, screening in underserved regions, and integration with elimination programs.

Roche Diagnostics (F. Hoffmann-La Roche Ltd.), Abbott Laboratories Inc., Siemens Healthineers, OraSure Technologies, Inc., Hologic, Inc., bioMérieux S.A.