- Food Packaging

- Foodservice Packaging Market

Foodservice Packaging Market Size, Share, and Growth Forecast 2026 - 2033

Foodservice Packaging Market by Material Type (Plastic, Paper & Paperboard, Aluminum, Biodegradable / Compostable Materials, Misc.), Product Type (Containers & Clamshells, Cups & Beverage Packaging, Trays & Boxes, Plates & Bowls, Flexible Packaging), End-user (Quick Service Restaurants (QSRs), Full-Service Restaurants (FSRs), Cafés & Coffee Chains, Institutional Foodservice, Online Food Delivery / Cloud Kitchens), and Regional Analysis, 2026-2033

Foodservice Packaging Market Size and Trend Analysis

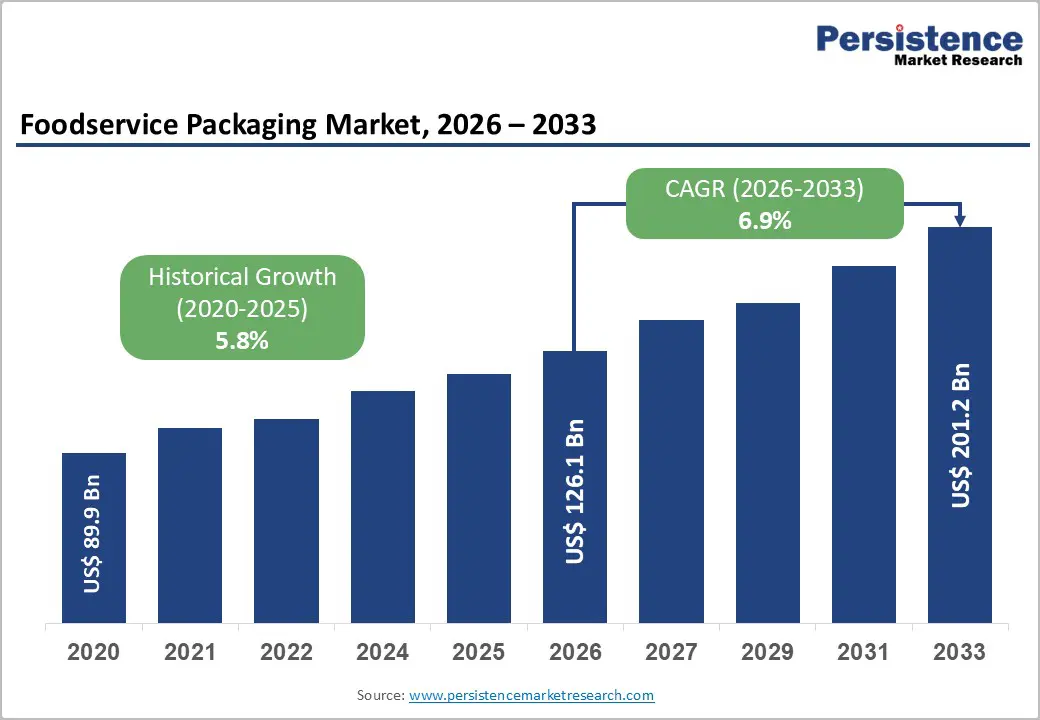

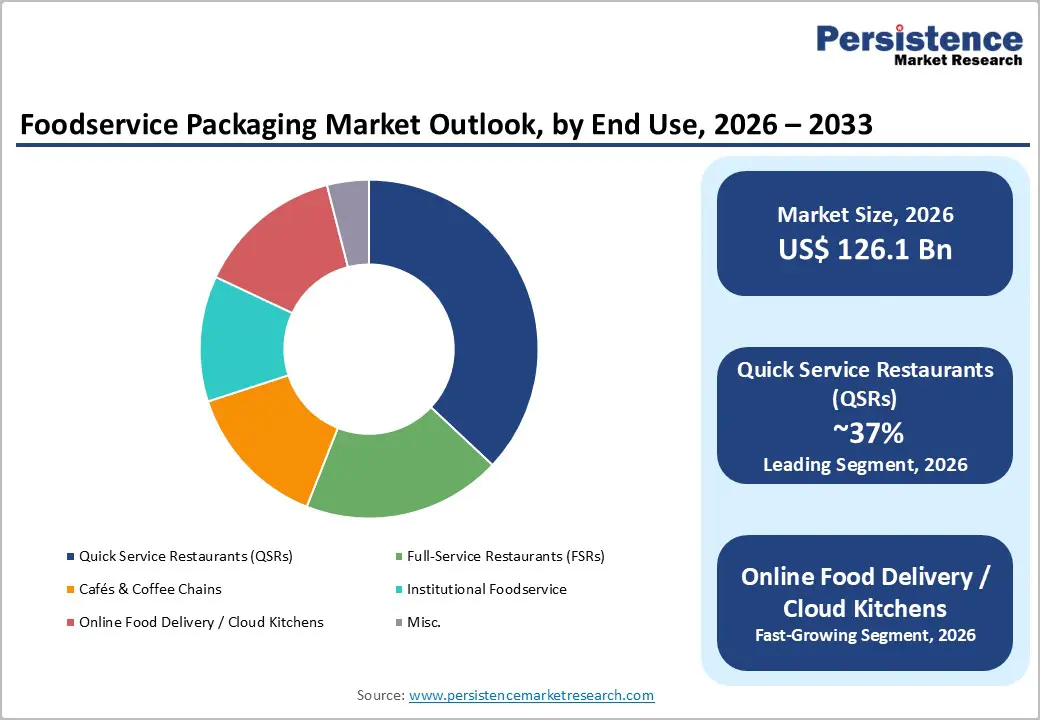

The global foodservice packaging market size is expected to be valued at US$ 126.1 Bn in 2026 and projected to reach US$ 201.2 Bn, growing at a CAGR of 6.9% between 2026 and 2033.

Market trajectory is anchored by the shift toward off-premises dining, the build-out of cloud kitchens, and accelerated regulatory pressure favoring fiber-based and compostable formats.

According to the U.S. Bureau of Labor Statistics, restaurant takeout and delivery occasions have outpaced dine-in growth since 2020, while the European Commission’s Single-Use Plastics Directive has rewired procurement choices across 27 EU member states. Operator consolidation among QSR chains and higher per-capita packaged-meal consumption further reinforce demand visibility through 2033, with brand-owner sustainability commitments accelerating substrate substitution.

Key Industry Highlights:

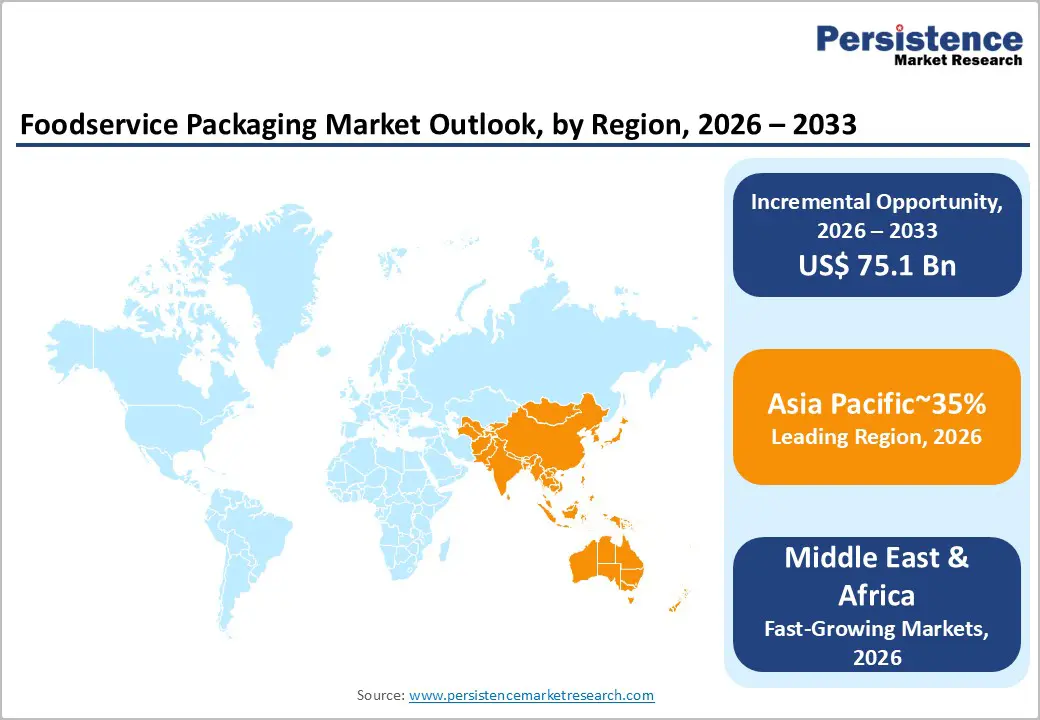

- Leading Region: Asia Pacific is the leading region with a 35% share in 2025, anchored by China and India’s mass-scale online food delivery ecosystems, dense QSR networks, and rapidly proliferating cloud-kitchen footprints across urban centers.

- Leading Material Type: Plastic remains the dominant material with a 49% share in 2025, sustained by cost economics, established thermoforming infrastructure, superior barrier performance, and mono-material recyclable PP designs aligned with global EPR roadmaps.

- Fast-Growing Material Type: Biodegradable and compostable materials are the fastest-growing segment at a 7.0% CAGR through 2033, propelled by EU PPWR mandates, U.S. state-level PFAS bans, brand-owner sustainability commitments, and rapid bagasse and PHA commercialization.

- Key Opportunity: The largest opportunity lies in next-generation compostables and smart-packaging integration for cloud kitchens, where TTI sensors, QR traceability, and PFAS-free fiber molding unlock premium-priced institutional and delivery contracts.

DRO Analysis

Drivers - Online Food Delivery and Cloud Kitchen Footprint Reshapes Packaging Demand

The reorganization of foodservice around delivery-first formats is the single largest pull on packaging volumes. The National Restaurant Association reported that off-premise sales accounted for over 74% of U.S. restaurant traffic in 2024, while credible online sources place the global online food delivery user base above 2.5 billion in 2025.

Cloud kitchens were estimated to have surpassed 75,000 operational units worldwide by 2024, depend exclusively on packaging to deliver brand experience and food integrity. This dependency converts every order into a packaging unit: leak-proof containers, vented lids, insulated sleeves, translating into recurring, high-frequency demand from a customer base operators cannot reach without packaging intermediation.

Consumer Premiumization and Brand-Led Packaging Investment

Foodservice operators treat packaging as a brand touchpoint, particularly in coffee chains and premium QSRs. Starbucks Corporation disclosed in its 2024 Global Environmental and Social Impact Report that packaging-led brand recall directly influenced repeat-visit metrics across more than 38,000 stores.

A 2024 Smithers industry study indicated that print decoration and structural design now represent over 18% of total packaging cost in premium foodservice categories, up from roughly 11% in 2019. Operators willingly absorb this premium because branded packaging functions as out-of-home advertising during delivery, reinforcing pricing power for converters offering customization, short-run flexography, and digital print.

Restraints - Regulatory Pressure on Single-Use Plastics

Comprehensive bans and Extended Producer Responsibility (EPR) mandates are compressing margins for legacy plastic converters. The European Union’s Packaging and Packaging Waste Regulation (PPWR), adopted in 2024, mandates that all packaging be recyclable by 2030 and prohibits select single-use plastic foodservice items outright.

India’s Ministry of Environment, Forest and Climate Change banned 19 identified single-use plastic items in 2022, while China’s National Development and Reform Commission has phased out non-degradable plastic bags across foodservice in major cities. These measures force capital reallocation toward fiber, PLA, and bagasse lines, creating a transitional drag on profitability for plastic-dominant portfolios.

Raw Material Volatility and Recycled-Fiber Supply Tightness

Input cost instability undercuts contract pricing for converters. The U.S. Energy Information Administration recorded resin price swings exceeding 40% between 2022 and 2024, while FAO pulp price indices showed virgin Kraft pulp moving from US$ 950/ton to over US$ 1,400/ton within an 18-month window.

Recycled fiber availability, central to compliance with recycled-content mandates, is constrained by collection inefficiencies in emerging markets where the OECD estimates recovery rates remain below 20%. Converters lacking long-term supply agreements with mills face squeezed margins and delivery risk on fixed-price foodservice contracts.

Opportunities - Commercialization of Bagasse, PHA, and Molded Fiber Compostables

The fastest-moving white space sits in next-generation compostable formats that close the cost-performance gap with plastic. The U.S. Department of Agriculture’s BioPreferred Program has expanded its certified-product database to over 17,000 bio-based items, signaling federal procurement pull.

PepsiCo announced in 2024 a multi-million-dollar investment in PHA-based packaging via partnership with Danimer Scientific, while McDonald’s Corporation committed to source 100% of guest packaging from renewable, recycled, or certified sources by 2025 across more than 40,000 outlets. Capacity investments in continuous-pulp molding lines at Huhtamaki Oyj alone earmarked EUR 100 million for fiber-based foodservice signal that compostables, projected to register a 7.0% CAGR through 2033, will be the principal demand-creation channel for the next decade.

Smart Packaging Integration for Cloud Kitchens and Institutional Foodservice

QR-enabled, NFC-tagged, and time-temperature-indicator (TTI) packaging unlocks operational value beyond containment. The U.S. Food and Drug Administration’s New Era of Smarter Food Safety blueprint explicitly promotes traceability technology, while GS1, the global barcode standards body, reports a 300% jump in 2D-code adoption for food packaging between 2022 and 2024.

Institutional foodservice operators Compass Group plc and Sodexo S.A., together serving over 75 million meals daily, are piloting TTI labels on hot-meal trays to reduce food-safety incidents. Converters that integrate sensor printing or RFID inlays into clamshells and cups can capture premium-priced contracts in healthcare, education, and corporate foodservice channels.

Category-wise Insights

Material Type Insights

Plastic retains a 49% share of the global foodservice packaging market in 2026, anchored by polypropylene, polyethylene terephthalate, and expanded polystyrene formats across cold and hot food applications. Its dominance is underpinned by cost economics PlasticsEurope data show resin pricing remains 35-50% below equivalent fiber alternatives on a per-unit-weight basis and by unmatched barrier performance for liquid-tight containment.

The American Chemistry Council notes that polypropylene clamshells offer thermal stability up to 120°C, supporting microwave-reheat occasions critical for delivery. Although regulatory headwinds favor fiber, the installed converter base of over 30,000 plastic-thermoforming lines globally, combined with mono-material PP designs achieving compliance under the APR Design Guide, sustains plastic’s dominance through the forecast horizon.

Product Type Insights

Containers & clamshells account for approximately 34% of foodservice packaging revenue in 2026, reflecting their indispensability across hot meals, salads, and combo formats in delivery and takeout. The National Restaurant Association documented that over 60% of U.S. restaurant orders in 2024 left the premises, with clamshell formats serving as the default carrier.

Pactiv Evergreen Inc. and Anchor Packaging LLC report clamshell SKUs as their highest-volume foodservice category. Structural rigidity, stackability for delivery couriers, and compatibility with both PP and molded-fiber substrates make clamshells the operational backbone for QSRs, ghost kitchens, and meal-kit operators. Innovations in tamper-evident hinges and leak-proof seals continue to widen clamshell applicability into soup, curry, and sauce-heavy cuisines.

End-user Insights

Quick Service Restaurants (QSRs) command roughly 37% of foodservice packaging consumption in 2026, a position underpinned by the segment’s transactional volume and rigorous specification regime. The International Foodservice Manufacturers Association reports that the top global QSR chains including McDonald’s, Yum! Brands, Restaurant Brands International, and Subway collectively operate over 220,000 outlets and serve more than 100 million customers daily.

This concentration creates packaging contracts in tens of millions of units per SKU, favoring large-format converters with multi-plant capability. QSR Magazine reported drive-thru’s share of QSR transactions at 44% in 2024, keeping per-occasion packaging intensity elevated.

Regional Insights

North America Foodservice Packaging Market Trends and Insights

North America holds a 27% share of the global foodservice packaging market in 2026. Regional maturity is shaped by dense QSR networks, an entrenched delivery ecosystem, and progressive state-level EPR legislation in California, Oregon, Maine, and Colorado. Adoption of recycled-content and certified-compostable formats is the dominant trend.

U.S. Foodservice Packaging Market Size

The U.S. foodservice packaging market is valued at approximately US$ 28 Bn in 2026, driven by the country’s ~200,000 QSR units catalogued by IBISWorld, a delivery ecosystem led by DoorDash, Uber Eats, and Grubhub that processes more than 3 billion annual orders, and accelerating state-level EPR legislation. Procurement at chains like Chick-fil-A, Chipotle, and Panera Bread explicitly favors PFAS-free fiber formats, reshaping converter portfolios.

Europe Foodservice Packaging Market Trends and Insights

Europe holds a 23% share of the global market in 2026. The region operates under the most stringent regulatory regime, with the Single-Use Plastics Directive and the 2024 PPWR mandating fiber substitution, recyclability, and recycled-content thresholds. Mono-material PE-coated paperboard and bagasse adoption are the defining trends.

Germany Foodservice Packaging Market Size

Germany’s foodservice packaging market is valued at approximately US$ 5.7 Bn in 2026, driven by Deutsche Umwelthilfe-supported deposit-return systems for reusable cups, mandatory reusable-packaging offerings at foodservice outlets under the VerpackG law since 2023, and a dense bakery-café network exceeding 11,000 outlets. Demand for DIN EN 13432-certified compostables is the strongest in the EU.

U.K. Foodservice Packaging Market Size

The U.K. foodservice packaging market is valued at approximately US$ 4.9 billion in 2026, driven by HM Revenue & Customs’ Plastic Packaging Tax of GBP 217.85/ton on packaging with under 30% recycled content, aggressive grab-and-go expansion by Pret A Manger, Costa Coffee, and Greggs across 30,000-plus outlets, and the WRAP-coordinated UK Plastics Pact recyclability targets.

Asia Pacific Foodservice Packaging Market Trends and Insights

Asia Pacific holds a 35% share of the global foodservice packaging market in 2026, the largest globally. Momentum is propelled by urbanization, the explosive scale of online food delivery in China, India, and Southeast Asia, and the proliferation of cloud kitchens. China’s Ministry of Ecology and Environment plastic-reduction rules are reshaping urban demand, while QSR penetration continues to deepen.

China Foodservice Packaging Market Size

China’s foodservice packaging market is valued at approximately US$ 15.7 billion in 2026, driven by Meituan and Ele.me processing over 70 million food-delivery orders daily per company-disclosed metrics, the National Development and Reform Commission’s phased plastic-bag ban now covering all prefecture-level cities, and the country’s >500,000 chain QSR outlets including KFC, Pizza Hut, and Luckin Coffee with 20,000Plus stores.

India Foodservice Packaging Market Size

India’s foodservice packaging market is valued at approximately US$ 7.4 Bn in 2026, driven by Swiggy and Zomato’s combined daily order volumes exceeding 3 million, the FSSAI’s mandatory food-contact compliance regulations, and the CPCB’s 2022 ban on 19 single-use plastic items. Rapid cloud-kitchen scaling operators like Rebel Foods running 450Plus internet restaurants anchors structural demand.

Competitive Landscape

The global foodservice packaging market is moderately fragmented, with the top 10 converters accounting for roughly 35-40% of revenue and a long tail of regional players serving local QSR and café accounts. Leaders compete on substrate breadth, R&D in fiber-molding and barrier coatings, and certification depth (BPI, TÜV OK Compost, PEFC, FSC).

Strategic moves include vertical integration into pulp and resin, acquisitions of compostable specialists, and partnerships with delivery platforms for branded programs. Capacity additions in Southeast Asia and Mexico, plus capex into PFAS-free fiber lines, are emerging as the differentiating R&D agenda.

Key Developments:

- In March 2025, Huhtamaki Oyj announced commissioning of a molded-fiber foodservice packaging plant in Goa, India, with annual capacity of 2.5 billion units, targeting QSR and cloud-kitchen demand across South Asia.

- In May 2025, Amcor and Metsä Group Partnered to develop molded fiber-based food packaging solutions by combining Amcor’s high-barrier film liner and lidding technology with Metsä Group’s Muoto™ wood-based molded fiber. The collaboration focuses on delivering recyclable, biodegradable, and high-performance packaging for food applications, enhancing shelf life of perishable products while advancing sustainable packaging adoption in the foodservice packaging market.

Companies Covered in Foodservice Packaging Market

- Amcor,

- Sealed Air

- Berry Global

- Smurfit Kappa

- Graphic Packaging Holding Company

- WestRock Company

- Huhtamaki

- Dart Container Corporation

- Anchor Packaging Inc.

- Pactiv LLC

- D&W Fine Pack

- New WinCup Holdings, Inc.

- Linpac Packaging Ltd

- Georgia-Pacific LLC

Frequently Asked Questions

The global foodservice packaging market is expected to be valued at US$ 126.1 Bn in 2026 and projected to reach US$ 201.2 Bn, advancing at a CAGR of 6.9% during the forecast period.

The dominant driver is the structural shift to off-premise dining and cloud kitchens. Off-premise sales crossed 74% of U.S. restaurant traffic in 2024, while global delivery users surpassed 2.5 billion, converting every order into a packaging unit.

Asia Pacific is likely to lead with a 35% share in 2026, anchored by China’s US$ 15.7 Bn market and India’s US$ 7.4 Bn market, driven by Meituan, Ele.me, Swiggy, and Zomato delivery scale and rapid cloud-kitchen build-out.

The single largest opportunity is the commercialization of bagasse, PHA, and molded-fiber compostables. Biodegradable/compostable materials are projected to advance at a 7% CAGR through 2033, propelled by EU PPWR, PFAS bans, and brand-owner mandates.

Major players include Amcor plc, Berry Global Inc., Sealed Air Corporation, Huhtamaki Oyj, Pactiv Evergreen Inc., Sonoco Products Company, Dart Container Corporation, WestRock Company, Graphic Packaging International, and Stora Enso Oyj.