- Medical Devices

- External Fixators Market

External Fixators Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

External Fixators Market by Product (Manual Fixators, and Computer-Aided Fixators), by Fixation Type (Unilateral and Bilateral, Circular, Hybrid, and Others) by Application (Orthopedic Deformities, Fracture Fixation, Infected Fracture, Limb Correction, and Others) by End-user (Hospitals, Orthopedic and Trauma Centers, and Ambulatory Surgery Centers), and Regional Analysis from 2026 to 2033

External Fixators Market Share and Trends Analysis

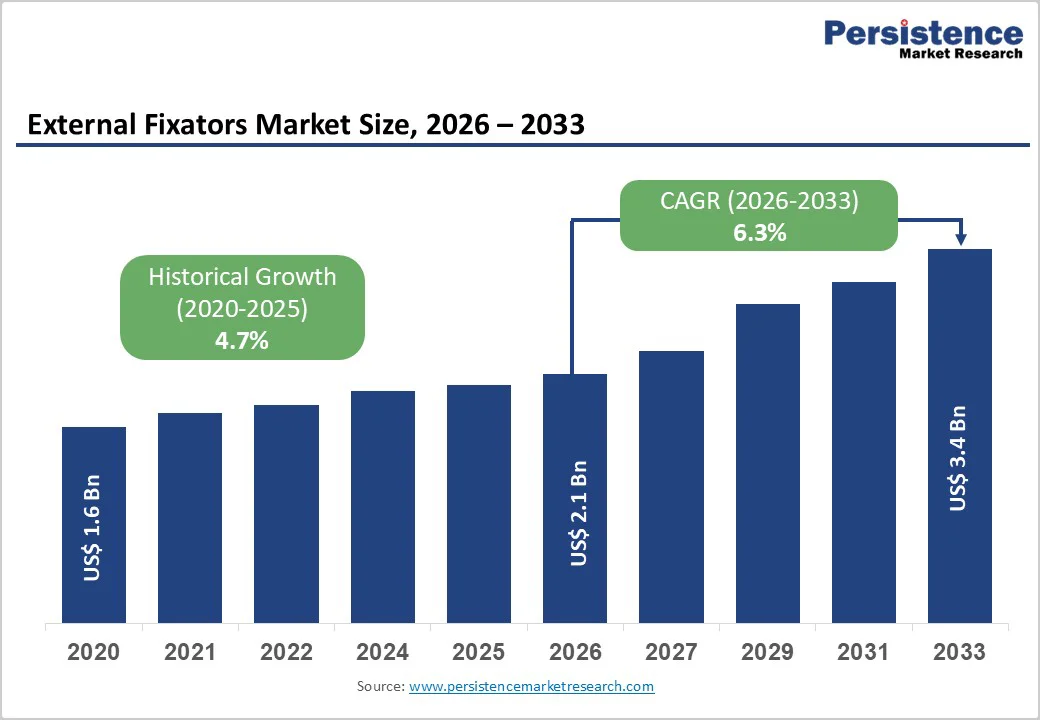

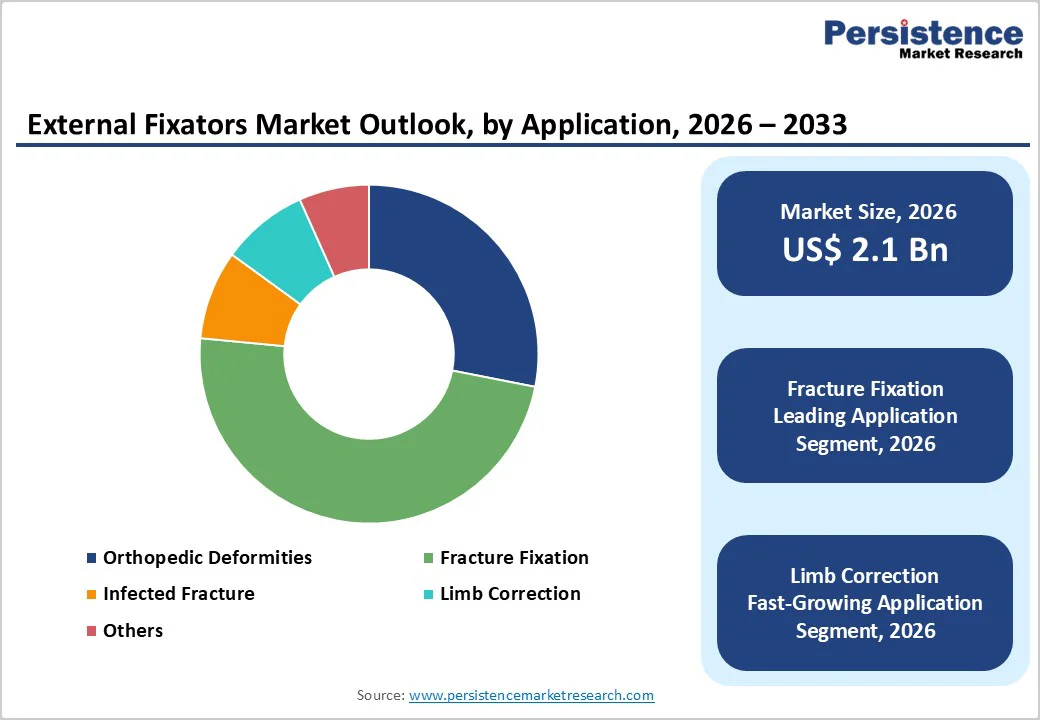

The global external fixators market size is likely to be valued at US$ 2.1 billion in 2026 and projected to reach US$ 3.4 billion, growing at a CAGR of 6.3% during the forecast period from 2026 to 2033.

Global demand for external fixators is rising rapidly, driven by the growing global burden of trauma injuries, increasing fracture incidence from road accidents, falls, and sports injuries, and expanding clinical emphasis on early stabilization to prevent complications.

Hospitals and specialty orthopedic centers offer unilateral, bilateral, circular, and hybrid fixator systems to support fracture management, deformity correction, and limb reconstruction. Rising investments in trauma-care infrastructure, expansion of orthopedic departments, and the growth of integrated emergency-care programs are accelerating global adoption.

Key Industry Highlights

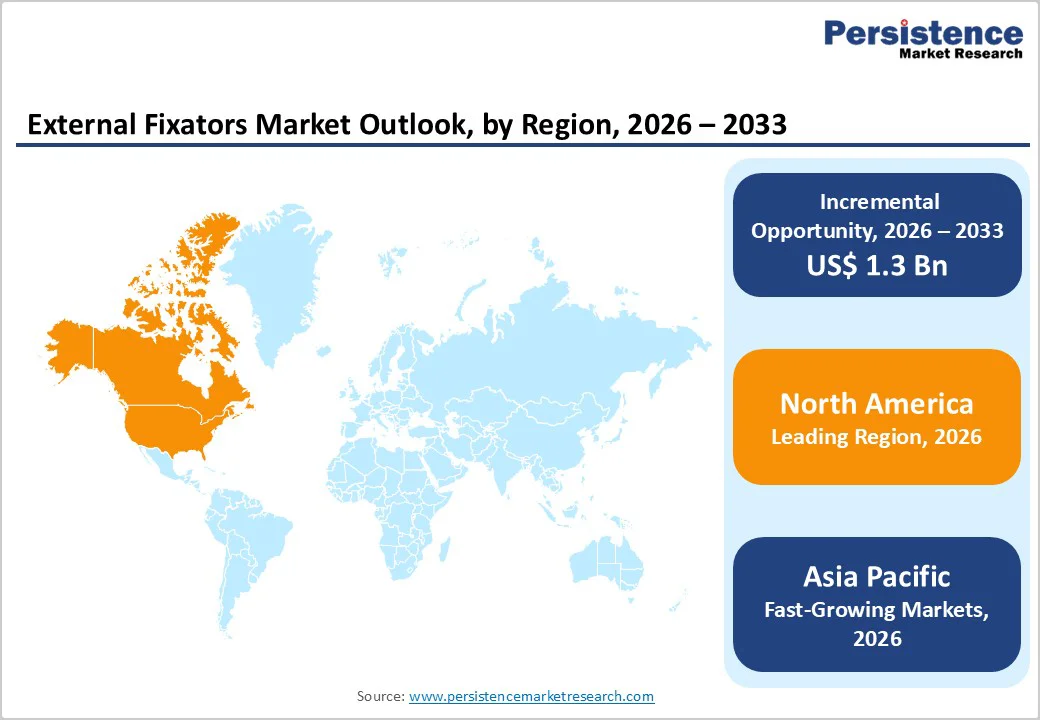

- Leading Region: North America holds the largest share at 46.3%, supported by advanced trauma-care infrastructure, strong adoption of modular external fixators, high healthcare expenditure, and early access to FDA-approved fixation technologies.

- Fastest-Growing Region: Asia Pacific is expanding the fastest due to a large trauma patient pool, rapid modernization of orthopedic facilities, increasing medical tourism, and growing investments in trauma-care capacity.

- Leading Product Segment: Manual fixators dominate the market due to their extensive use in emergency stabilization and fracture-care algorithms, offering high reliability and broad clinical acceptance.

- Fastest-Growing Product Segment: Computer-aided fixators grow rapidly as rising trauma and deformity cases support broader use of digitally assisted systems that enhance alignment accuracy and surgical efficiency.

- Leading Application Segment: Fracture fixation remains the top application, driven by rising fracture volumes, strong preference for minimally invasive stabilization, and expanding integration of external fixators into standardized trauma-care pathways.

- Fastest-Growing Application Segment: Limb correction is scaling quickly as demand increases for advanced deformity-correction solutions, distraction osteogenesis procedures, and specialized limb-lengthening treatments.

| Key Insights | Details |

|---|---|

| External Fixators Market Size (2026E) | US$ 2.1 Bn |

| Market Value Forecast (2033F) | US$ 3.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.7% |

Market Dynamics

Driver - Rising Global Fracture Incidence and Advancements in Minimally Invasive Fixation Technologies

The global external fixators market is experiencing accelerated demand, primarily driven by the rising incidence of fractures worldwide, fueled by road-traffic accidents, occupational injuries, falls among the elderly, and sports-related trauma. As trauma volumes grow, healthcare systems increasingly rely on external fixation systems for rapid stabilization, especially in emergency and polytrauma scenarios.

For instance, in 2023, the International Osteoporosis Foundation reported that wrist fractures accounted for 33.1% of all cases and spine fractures for 20.1%, highlighting the growing global fracture burden.

This rising incidence especially among older adults and individuals with low bone density directly fuels demand for external fixators, as healthcare providers increasingly rely on rapid, minimally invasive stabilization solutions for managing high-volume trauma and fragility fractures.

Their ability to provide immediate structural support with minimal disruption to soft tissues makes them indispensable in acute orthopedic care. The growing geriatric population particularly vulnerable to fragility fractures further amplifies procedural volumes across hospitals and trauma centers.

The shift toward minimally invasive orthopedic procedures is strengthening the role of external fixators in modern surgery. Surgeons favor these systems for their reduced blood loss, lower infection risk, and compatibility with staged reconstruction protocols.

Continuous technological advancements, including lightweight carbon-fiber frames, enhanced modular designs, and computer-aided alignment tools, are improving surgical precision, patient comfort, and procedural efficiency. These innovations support better clinical outcomes in deformity correction, limb lengthening, and complex fracture management, while enabling more predictable postoperative recovery.

Together, rising fracture incidence and sophisticated fixator technologies are reshaping global orthopedic treatment pathways and accelerating market growth.

Restraints - Clinical Risks and Competition from Alternative Fixation Methods

The global external fixators market faces notable challenges due to clinical risks associated with device use, particularly pin-tract infections and other postoperative complications. These infections, along with patient discomfort, can lead to delayed recovery, prolonged hospital stays, and, in severe cases, revision procedures.

Such concerns may reduce patient acceptance and influence surgeons’ choice of fixation method, especially in settings where strict infection control protocols are difficult to maintain. Additionally, complications such as loosening of pins, soft-tissue irritation, and nerve or vascular injury require careful monitoring and can limit broader adoption in certain patient populations, particularly the elderly or immunocompromised.

Moreover, the availability of alternative internal fixation methods presents a competitive restraint. The increasing use of plates, screws, and intramedullary nails for fracture stabilization offers surgeons options that provide rigid fixation, reduced external hardware exposure, and potentially lower infection risk.

For less complex fractures or those in well-vascularized bone, internal fixation often becomes the preferred approach, reducing reliance on external fixators. The combination of clinical risks and the presence of established internal fixation alternatives limits market penetration in some regions, particularly in high-income countries where advanced surgical infrastructure supports a wide range of fixation techniques.

Together, these factors pose a challenge to growth despite rising trauma and deformity cases globally.

Opportunity - Technological Advancements and Infrastructure Expansion Driving Market Opportunities

The global external fixators market is witnessing significant growth driven by rapid adoption of computer-aided and digital fixation platforms. Navigation-assisted frames, 3D preoperative planning tools, and AI-based alignment systems are enabling surgeons to achieve higher precision, reduce operative times, and improve patient outcomes in complex fracture management and limb reconstruction procedures.

These innovations not only enhance surgical accuracy but also increase confidence in performing minimally invasive procedures, encouraging broader clinical adoption. Simultaneously, the development of lightweight, patient-friendly materials, such as carbon-fiber rods, titanium alloys, and bioengineered coatings, is improving patient comfort, reducing postoperative complications, and enabling faster rehabilitation.

These material innovations also facilitate modular and customizable fixator designs, meeting the diverse needs of trauma and orthopedic patients.

Furthermore, the expansion of trauma-care infrastructure in emerging economies is creating substantial market opportunities. Investments in upgrading emergency departments, orthopedic units, and specialized trauma centers are increasing procedural capacity and accessibility for complex fracture stabilization and deformity correction.

Growing healthcare expenditure, supportive government policies, and partnerships with global orthopedic device manufacturers are accelerating the adoption of advanced fixation systems in regions such as Asia Pacific and Latin America. Together, technological innovation and infrastructure expansion are creating a favorable environment for market growth, enabling wider clinical adoption and improving treatment outcomes for trauma and orthopedic patients worldwide.

Category-wise Analysis

By Product Insights

The manual fixators segment is projected to dominate the global external fixators market in 2026, accounting for a significant revenue share of 60.4%. This leadership is driven by the widespread clinical adoption of manual external fixators as the standard of care for acute fracture stabilization, deformity correction, and emergency trauma management.

Their ability to provide reliable stabilization, support rapid application in emergency settings, and offer cost-effective treatment options underpins their extensive use across hospitals and orthopedic centers. Continued improvements in modular designs, biocompatible materials, and ease-of-application systems further enhance their adoption.

Rising incidence of road-traffic injuries, expanding trauma-care capacity, and strong clinical familiarity with traditional fixator systems reinforce the dominant position of manual fixators in global orthopedic practice.

By Fixation Type Insights

The unilateral and bilateral segment is projected to dominate the global external fixators market in 2026, accounting for a significant revenue share of 38.4%. This dominance stems from the extensive use of unilateral and bilateral fixators for treating a wide range of fractures, including long-bone injuries, open fractures, and polytrauma cases.

Their widespread adoption across trauma departments, supported by efficient application techniques, strong clinical outcomes, and flexible configuration options, drives substantial demand. Routine fracture diagnosis through radiographic screening, established orthopedic treatment pathways, and guideline-supported stabilization strategies further contribute to higher utilization.

Growing trauma cases, increasing sports injuries, and emphasis on early fracture care reinforce the strong market positioning of unilateral and bilateral fixation systems.

By End-user Insights

The hospitals segment is projected to dominate the global external fixators market in 2026, capturing a revenue share of 56.7%. Hospitals, particularly tertiary-care centers, trauma units, and academic orthopedic institutions, serve as primary hubs for fracture management, deformity correction, and complex limb reconstruction.

Their ability to handle high patient volumes, manage polytrauma cases, and perform advanced external fixation procedures under multidisciplinary teams supports strong hospital-based demand. Moreover, hospitals play a central role in emergency trauma care, orthopedic surgical training, and clinical evaluation of next-generation fixation technologies.

Their extensive surgical capacity, integration of advanced imaging and navigation tools, and leadership in managing severe orthopedic injuries solidify hospitals as the leading end-user segment globally.

Region-wise Insights

North America External Fixators Market Trends

North America is expected to maintain global dominance in the external fixators market with a market share value of 45.9%, supported by its advanced healthcare infrastructure, strong orthopedic trauma care systems, and widespread adoption of unilateral, circular, and hybrid fixation devices.

The U.S. leads the region due to frequent FDA approvals of new external fixation systems, strong presence of leading orthopedic device manufacturers, and extensive collaborations between trauma centers, hospitals, and academic surgical research institutions.

Major orthopedic networks continuously evaluate next-generation fixators, computer-assisted alignment platforms, and minimally invasive fixation systems, accelerating clinical integration. Rising demand for timely fracture management, deformity correction, and decentralized trauma care continues to drive investments from large healthcare systems.

The region also benefits from strong reimbursement frameworks for orthopedic trauma procedures, high clinician preference for modular and computer-aided external fixators, and expanding adoption of digitized pre-operative planning tools.

Increasing investment in trauma infrastructure, surgical navigation platforms, and AI-supported orthopedic workflow management is improving treatment efficiency. Additionally, rising public awareness of injury prevention, sports-related trauma, and limb-reconstruction options continues to strengthen North America’s long-term leadership in the global external fixators market.

Europe External Fixators Market Trends

Europe shows steady and mature adoption of external fixator solutions, supported by strong public-health systems, well-established orthopedic trauma networks, and stringent surgical guidelines across major markets such as Germany, the U.K., France, Italy, Switzerland, and the Nordic countries.

Robust epidemiological surveillance, orthopedic registries, and consistent clinical validation of fixation techniques support the deployment of unilateral, circular, and hybrid fixators across primary and specialty orthopedic centers.

The region demonstrates high integration of advanced fixation materials, standardized fracture-management protocols, and evidence-based deformity correction pathways aimed at improving alignment outcomes and reducing complication risks.

Europe’s favorable regulatory framework, emphasis on safety and performance, and strong contributions from orthopedic research centers support continuous evaluation of next-generation external fixation technologies. Growing demand for lightweight modular fixators, improved circular fixation systems, and digitally planned deformity-correction procedures continues to strengthen uptake.

Regional device manufacturers are investing in product innovation, GMP-compliant production, and resilient supply chains. Government initiatives promoting injury prevention, early fracture management, and digital monitoring of post-surgical outcomes further drive Europe’s overall market growth.

Asia Pacific External Fixators Market Trends

Asia Pacific is projected to be the fastest-growing region for external fixators with a CAGR of 8.5%, driven by rising healthcare expenditure, increasing burden of road-traffic injuries, and rapid expansion of trauma and orthopedic care facilities.

Countries such as China, Japan, South Korea, Singapore, and India are increasing adoption of unilateral, circular, and hybrid external fixators across hospitals, orthopedic centers, and government-supported trauma programs. Growing availability of cost-effective devices and regional manufacturing capabilities is improving affordability and expanding access across second-tier cities and community healthcare settings.

Government-supported trauma-care modernization, investments in emergency response systems, and partnerships with global orthopedic companies for technology transfer are accelerating adoption. Increasing need for early fracture detection, standardized trauma workflows, and minimally invasive deformity-correction solutions is driving strong clinical uptake.

Orthopedic surgeons across Asia Pacific are increasingly participating in global trauma research networks, adopting advanced surgical protocols to enhance outcomes. Expanding private healthcare systems, rising medical tourism, and the growth of specialized limb-reconstruction centers continue to support robust market expansion across the region.

Competitive Landscape

The global external fixators market is highly competitive, with active participation from Johnson & Johnson, Stryker, Zimmer Biomet, Smith+Nephew, and Orthofix Medical Inc.

These companies leverage strong orthopedic trauma, limb reconstruction, and fixation system portfolios to expand their presence across hospitals, trauma centers, and specialized orthopedic care networks. Rising fracture incidence and increasing demand for deformity correction continue to drive the adoption of unilateral, circular, hybrid, and computer-aided external fixation systems.

Manufacturers are prioritizing advanced modular fixator designs, computer-assisted alignment technologies, and lightweight biocompatible materials, while focusing on regulatory approvals, scaled production, and partnerships with healthcare institutions to improve surgical access and support global market expansion.

Key Industry Developments:

- In January 2025, Fusion Orthopedics USA, LLC expanded its product portfolio with the addition of the Metalogix External Fixation Systems. The integration of Metalogix’s operations, distribution channels, and hospital accounts into Fusion’s network has been substantially completed, strengthening the company’s presence in the global external fixators market and enhancing its ability to serve trauma and orthopedic care providers.

- In September 2023, Orthofix Medical Inc., announced the full U.S. commercial launch of the Galaxy Fixation Gemini™ system and reported the successful completion of the first clinical cases. As the latest addition to the Galaxy product line, this stable external fixation system is available in multiple sterile procedure kit configurations, providing a ready-to-use solution for the treatment of upper and lower limb fractures resulting from trauma. This launch strengthens Orthofix’s portfolio in trauma and orthopedic care.

Companies Covered in External Fixators Market

- Johnson & Johnson

- Stryker

- Zimmer Biomet

- Smith+Nephew

- Orthofix Medical Inc.

- TST Tıbbi Aletler San. Ve Tic. Ltd. Şti.

- Response Ortho

- Tasarimmed Tıbbi Mamuller San. Tic A.Ş.

- Auxein

- Acumed LLC, a Marmon Medica

- Narang Medical Limited

- Ortho Life Systems Pvt. Ltd.

- GWS Surgicals LLP

- Biomedortho

- Others

Frequently Asked Questions

The global external fixators market is projected to be valued at US$ 2.1 Bn in 2026.

The global external fixators market is driven by rising trauma and fracture incidence, increasing orthopedic deformity cases, and growing adoption of computer-aided and circular fixation systems.

The global external fixators market is poised to witness a CAGR of 6.3% between 2026 and 2033.

Key opportunities include expanding use of digital surgical planning, growth in limb reconstruction procedures, and increasing adoption of advanced hybrid and computer-assisted fixator technologies in emerging markets.

Johnson & Johnson, Stryker, Zimmer Biomet, Smith+Nephew, and Orthofix Medical Inc., are some of the key players in the external fixators market.