- Specialty & Fine Chemicals

- Drywall & Building Plasters Market

Drywall & Building Plasters Market Size, Share, and Growth Forecast 2026 - 2033

Drywall & Building Plasters Market by Product Type (Gypsum-based, Cement-based, Lime-based, Clay, Other), Application (Wall Construction, Ceiling Construction, Interior Decoration, Exterior Finishes, Other), End-user (Residential, Commercial, Industrial, Other), and Regional Analysis for 2026 - 2033

Drywall & Building Plasters Market Size and Trend Analysis

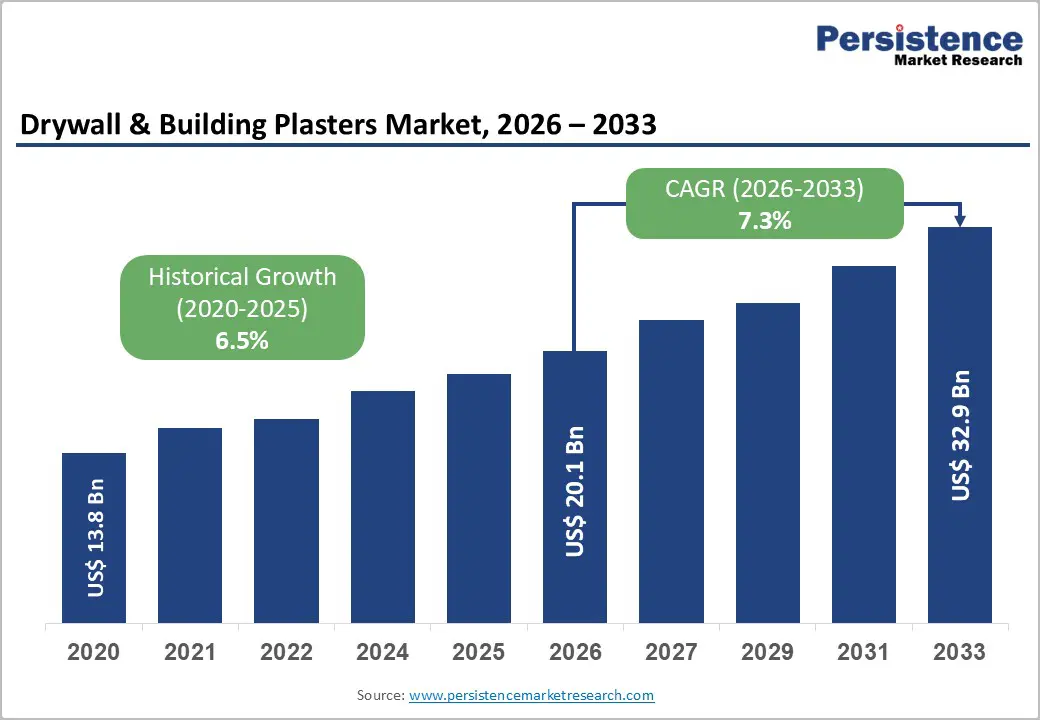

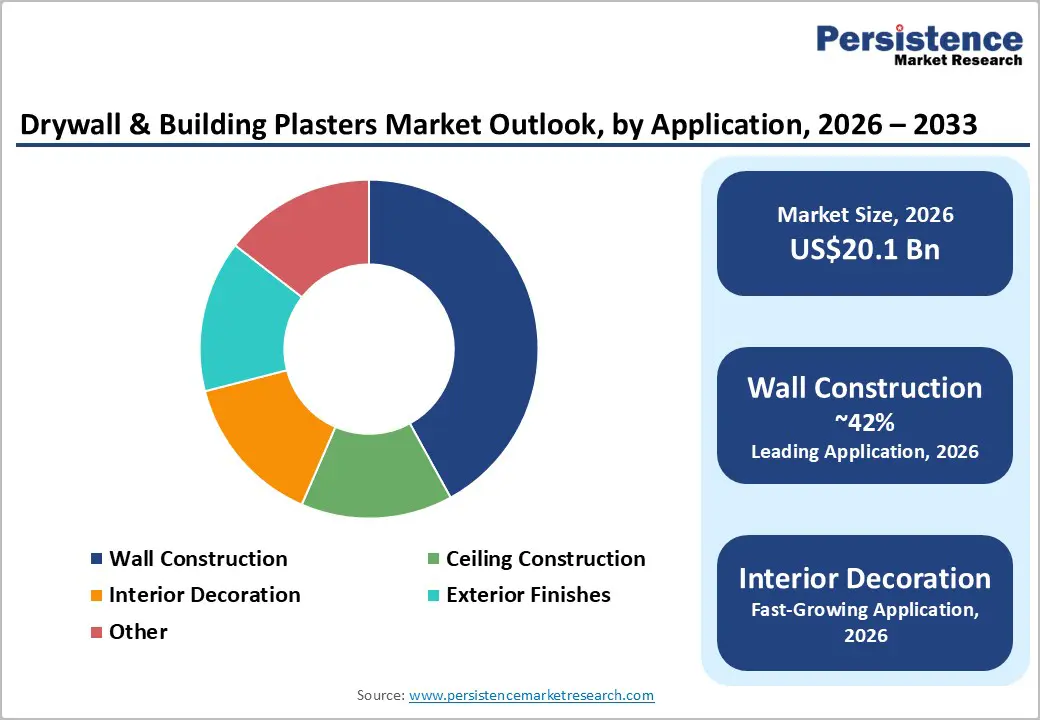

The global Drywall & Building Plasters market size is supposed to be valued at US$ 20.1 Bn in 2026 and is projected to reach US$ 32.9 Bn by 2033, growing at a CAGR of 7.3% between 2026 and 2033. The market's robust expansion is primarily driven by accelerating urbanization and substantial infrastructure investments across emerging economies, particularly in the Asia-Pacific region, where countries such as China and India are experiencing unprecedented construction activity.

The growing preference for lightweight, fire-resistant, and cost-effective building materials in both residential and commercial construction projects has positioned gypsum-based drywall and plaster as essential components of modern building practices. Furthermore, stringent building safety regulations mandating fire-resistant materials, coupled with the increasing adoption of energy-efficient and sustainable construction methodologies aligned with green building certifications like LEED and BREEAM, are catalyzing market demand across developed and developing regions.

Key Industry Highlights:

- Leading Region: North America maintains market leadership, with a 38% market share, driven by the United States' position as the world's largest wallboard consumer, a mature construction ecosystem, stringent fire safety regulations, and established distribution networks supporting the residential construction recovery.

- Fastest Growing Region: Asia Pacific emerges as the fastest-growing regional market, propelled by unprecedented urbanization dynamics, substantial infrastructure investment programs across China and India, rapid adoption of modern construction methodologies in Southeast Asian emerging economies, and residential construction growth.

- Dominant segment: Gypsum-based products command approximately 58% market share within product type segmentation, driven by superior fire resistance properties containing 21% chemically combined water, ease of application, rapid installation capabilities, and cost-effectiveness relative to traditional plastering methods.

- Fastest-growing segment: Among end users

- Residential construction remains dominant and is growing rapidly, accounting for nearly 62% of global drywall installations, supported by urban housing demand, renovation cycles in North America and Europe, and mass housing and smart-city initiatives in the Asia Pacific.

- Key market opportunity: The biggest opportunity lies in low-carbon, high-performance interior systems aligned with net-zero building targets. Leveraging synthetic gypsum, circular manufacturing, and advanced plasters can position suppliers to capture premium demand from green buildings and deep energy-efficiency retrofits worldwide.

| Key Insights | Details |

|---|---|

|

Drywall & Building Plasters Market Size (2026E) |

US$ 20.1 Bn |

|

Market Value Forecast (2033F) |

US$ 32.9 Bn |

|

Projected Growth CAGR (2026–2033) |

7.3% |

|

Historical Market Growth (2020–2025) |

6.5% |

Market Dynamics

Drivers - Surging global construction activity and urbanization

The rapid expansion of residential and commercial construction in emerging economies is a key factor driving growth in the global drywall and building plaster market. In 2023, the construction sector grew by approximately 3.4%, with emerging markets advancing at around 5.6%, compared with only 0.5% growth in advanced economies. Major national initiatives, such as China’s commitment of US$ 4.2 trillion under its 14th Five-Year Plan and strong non-residential construction growth exceeding 10.3% annually in Vietnam, the Philippines, and Indonesia, further reinforce this momentum.

With the United Nations projecting that 68% of the global population will live in urban areas by 2050, demand for efficient, cost-effective building solutions will intensify. Drywall and plaster systems address this need through rapid installation, reduced labor dependency, and consistent performance in high-density developments.

Stringent Fire Safety Regulations and Enhanced Building Code Requirements

The increasing stringency of global fire safety regulations has become a significant catalyst for the adoption of fire-resistant drywall and gypsum-based building materials. Gypsum board, which contains roughly 21% chemically bound water, releases steam when subjected to high temperatures, thereby reducing heat transfer and limiting flame spread. Type X gypsum panels deliver one-hour fire-resistance ratings, while advanced Type C panels, reinforced with additional glass fibers, achieve flame-spread ratings as low as 15, well below the NFPA Class A threshold of 25.

Furthermore, the European Union’s revised Energy Performance of Buildings Directive (EU/2024/1275) mandates zero-emission standards for new buildings by 2030 and requires substantial energy-efficiency improvements in existing residential structures. These regulatory developments, reinforced by insurance requirements for fire-rated assemblies, increasingly guide stakeholders toward gypsum-based solutions offering reliable fire performance, acoustic control, and compliance across jurisdictions.

Restraints - Fluctuating Raw Material Costs and Supply Chain Vulnerabilities

The Drywall and Building Plasters Market is highly volatile due to fluctuations in gypsum, energy, and transportation costs. In the United States, crude gypsum production remained around 22 million tons in 2023–2024, while imports reached 8.1 million tons in 2023, underscoring reliance on cross-border supply chains. Average mine-gate prices for crude gypsum rose from US$ 8.6 per ton in 2019–2020 to US$ 13 per ton in 2024, with calcined gypsum increasing from US$ 34–35 per ton to nearly US$ 63 per ton.

These rising input costs compress margins and may elevate installed costs for end-users, limiting adoption in price-sensitive markets. Ongoing supply chain disruptions, declining synthetic gypsum output linked to reduced coal-based power generation, inflationary pressures in Europe, and high transportation costs for bulk materials further constrain manufacturers’ ability to maintain competitive pricing and market reach.

Skilled Labor Shortages and Installation Complexity Challenges

The global construction industry faces persistent shortages of skilled labor that directly affect drywall installation productivity and quality. Although gypsum board systems reduce on-site labor compared with traditional wet plaster methods, proper installation, joint finishing, and surface preparation still require specialized expertise to meet fire-rating and aesthetic standards. In the Asia Pacific region, these shortages have increased interest in prefabricated building materials. However, deviations from tested assembly configurations can compromise fire-resistance performance.

Maintaining consistent installation quality across both residential projects and large commercial developments, such as complex ceiling systems, shaft walls, and fire-rated corridors, remains a significant challenge. Training programs have not kept pace with rising construction demand, leading to higher wages for experienced installers and increased project costs. Additionally, alternative lightweight construction systems, including structural insulated panels and modular technologies, are intensifying competition in labor-constrained markets.

Opportunity - Synthetic Gypsum Adoption and Circular Economy Integration

The growing adoption of synthetic gypsum offers significant opportunities for manufacturers to enhance sustainability performance, lower raw material costs, and address supply constraints. The global Synthetic Gypsum Market was valued at US$ 2,299.3 million in 2025 and is expected to grow at a 4.6% CAGR through 2032, supported by regulations promoting industrial waste utilization and circular economy principles. Synthetic gypsum, primarily produced through flue-Gas desulfurization processes, accounts for nearly 60% of the market and provides performance comparable to natural gypsum while reducing raw material extraction by an estimated 28%.

Major producers such as USG Corporation in North America and leading European manufacturers increasingly rely on FGD-based gypsum to meet environmental targets. Companies that invest in processing capacity, form partnerships with industrial byproduct generators, and pursue sustainability-focused product strategies are well positioned to capture environmentally conscious market segments.

Renovation and Remodeling Wave in Developed Markets

The renovation and remodeling market in North America and Europe has emerged as a major growth driver, distinct from new construction trends. In the United States, renovation spending rose to US$509 billion in 2025 after two years of decline, with nearly 40% of residential buildings constructed before 1970 requiring wall upgrades to meet modern fire, insulation, and acoustical standards.

In Europe, the drive toward zero-emission buildings by 2050, supported by interim energy-efficiency targets for 2030 and 2033, necessitates extensive retrofitting of aging structures, particularly in Spain, where over 80% of buildings fall below required efficiency levels. This regulatory-driven demand is increasing the use of gypsum board systems with enhanced thermal performance, moisture resistance, and pre-decorated features. Companies offering advanced renovation-focused products and technical support continue to capture high-margin opportunities in these mature markets.

Category-wise Analysis

Product Type Insights

Gypsum-based products dominate the drywall and building plasters market, accounting for about 58% of the total share due to their superior fire resistance, ease of application, rapid installation, and cost-effectiveness. Gypsum board is widely used for interior walls and ceilings across residential, commercial, and institutional buildings because of its versatility and ability to enhance indoor comfort through moisture regulation and acoustic insulation.

Gypsum plaster is increasingly preferred over cement-based alternatives for its smooth finish, fast setting time, and inherent fire-resistant properties. Synthetic Gypsum Market growth, driven by sustainability initiatives and industrial waste utilization from power generation facilities, further reinforces gypsum-based products' market leadership as manufacturers successfully position recycled-content offerings to environmentally-conscious specifiers while maintaining performance equivalence with natural gypsum formulations across demanding commercial and institutional applications requiring certified fire ratings and acoustic performance.

Application Insights

Wall construction remains the leading application segment, accounting for nearly 42% of market demand, underscoring the essential role of drywall systems in creating interior partitions, demising walls, and exterior wall furring assemblies across diverse building types. The dominance of gypsum wallboard in this segment is supported by its lightweight, which reduces structural loads, and by factory-controlled quality, which minimizes field variability. Its compatibility with electrical and plumbing installations further accelerates construction timelines compared with masonry or poured-in-place concrete.

Gypsum board’s Class A fire rating, with flame-spread indices of 15 or lower, meets stringent safety requirements in multifamily corridors, hotel guest rooms, and commercial demising walls. Type X and Type C assemblies provide one-to two-hour fire-resistance ratings while achieving STC values above 50. Growing demand for open-plan offices and flexible retail environments is also driving the adoption of demountable gypsum-based partition systems.

End-user Insights

The Residential segment remains the leading end-use category, accounting for approximately 46% of market share, driven by strong global housing demand across affordable, mid-range, and luxury developments. Drywall systems have become standard in residential construction due to their affordability, rapid installation, and design flexibility, enabling efficient project delivery and diverse architectural finishes. The Asia-Pacific region offers substantial growth opportunities, with India’s residential construction expanding by 15.7% annually in 2025, supported by large-scale housing programs such as PM Awas Yojana Urban 2.0.

China also maintains considerable activity, with developers focusing on interior finishing to accelerate cash flow. In North America, gypsum board is universally used in wood-frame housing, particularly in fire-rated assemblies. Renovation demand further strengthens the segment, as homeowners increasingly adopt moisture-resistant, sound-insulated, and pre-decorated drywall solutions.

Regional Insights

North America Drywall & Building Plasters Market Trends

North America retains market leadership, supported by the United States’ position as the world’s largest wallboard consumer and a mature construction environment defined by standardized building practices, strict fire-safety codes, and strong distribution networks. USG Corporation, now part of Knauf, continues to hold leading positions in the region’s wallboard and ceilings segments.

Regulatory frameworks such as the IBC and NFPA standards mandate fire-resistant assemblies, strengthening gypsum board demand. Recent investments, including Saint-Gobain’s US$235 million upgrade in Florida and the rising adoption of synthetic gypsum, underscore a growing focus on sustainability and capacity expansion, with Canada and Mexico contributing to additional regional growth.

Europe Drywall & Building Plasters Market Trends

Europe represents a highly regulated market driven by strict energy-efficiency requirements, sustainability mandates, and a strong focus on building renovation to meet long-term climate-neutrality goals. The revised Energy Performance of Buildings Directive (EU/2024/1275) requires residential buildings to achieve at least an E energy rating by 2030 and a D rating by 2033, progressing toward a zero-emission building stock by 2050. These mandates necessitate large-scale retrofitting, particularly in Spain, where over 80% of buildings fall below required efficiency levels.

Construction activity in major markets, including Germany, the United Kingdom, France, and Spain, is expected to rebound modestly in 2025 as inflation eases. Leading manufacturers such as Etex, Knauf, and Saint-Gobain continue investing in capacity expansion, sustainability initiatives, and gypsum-recycling programs, reflecting the region’s shift toward circular-economy practices and harmonized building standards.

Asia Pacific Drywall & Building Plasters Market Trends

Asia Pacific is the fastest-growing and largest regional market, driven by rapid urbanization, major infrastructure programs, and the adoption of modern construction methods. China, while experiencing residential market moderation, continues to see substantial construction activity, with wallboard volumes demonstrating resilience as developers prioritize accelerating interior finishing work.

India's construction market expansion reflects robust public and private sector investment, with the extended National Infrastructure Pipeline (NIP) allocating resources across critical infrastructure, including the Mumbai-Ahmedabad High-Speed Rail and Chennai-Bengaluru Expressway, alongside a US$12 billion expansion of 15 metro rail systems across cities, featuring energy-efficient designs. The PM Awas Yojana Urban 2.0 program, launched in 2024, targets the construction of 10 million affordable, eco-friendly homes by 2027, systematically driving gypsum board demand in cost-sensitive residential applications where installation speed and material efficiency provide economic advantages over traditional masonry construction.

Competitive Landscape

The drywall & building plasters market is moderately to highly concentrated globally, with a small group of multinational manufacturers controlling a significant share of wallboard capacity. Six leading companies, Saint-Gobain S.A., Knauf Group, Etex S.A., Georgia-Pacific LLC, National Gypsum Company, and Yoshino Gypsum Co., Ltd., collectively hold about 81% of the worldwide market. These firms differentiate through extensive product portfolios, including standard, fire-rated, moisture-resistant, and acoustic boards and plasters, supported by broad distribution networks and strong specification influence among architects and contractors. Strategic priorities focus on expanding capacity in high-growth regions, improving energy efficiency and recycling processes, and introducing low-carbon board lines.

Key Developments:

- September 2024: Saint-Gobain Canada completed a major expansion and electrification upgrade at its Sainte-Catherine gypsum wallboard plant, transforming it into North America’s first zero-carbon (Scopes 1 and 2) gypsum wallboard facility and increasing production capacity by up to 40% while cutting CO- emissions by about 44,000 tons/year.

- May 2024: CGC Inc. (division of USG Corporation) broke ground on a new 220,000 square foot wallboard manufacturing plant in Alberta, Canada, designed to create more than 200 jobs during construction and significantly expand the domestic supply of gypsum panels for Western Canada.

- March 2023: Knauf Gips KG completed a multi-million-pound acquisition and commissioning of a plasterboard plant at Newport, South Wales, increasing U.K. gypsum board production capacity by around 20% and integrating on-site recycling and renewable-energy-based operations to reduce carbon footprint.

Top Companies in Drywall & Building Plasters Market

Saint-Gobain S.A. (Courbevoie, France) is one of the world’s largest building materials groups and a clear leader in gypsum boards and plasters through its CertainTeed and Gyproc brands. With extensive mining, manufacturing, and distribution assets across Europe, North America, Asia, and Latin America, the company focuses on light and sustainable construction, low-carbon wallboard (such as its CarbonLow™ and Infinaé ranges), and system-based interior solutions for residential and non-residential projects.

Knauf Gips KG (Iphofen, Germany) is a privately held multinational specializing in gypsum boards, plasters, and insulation systems, operating more than 150 production sites worldwide. The company has been aggressively expanding capacity in Europe, Asia, and Africa, including new wallboard plants and significant upgrades in Romania, Uzbekistan, Tanzania, and the U.K., often emphasizing energy efficiency, on-site recycling, and proximity to ports and quarries to optimize logistics. Its strong presence in both residential and commercial segments, combined with integrated dry construction solutions, positions Knauf as a key competitive benchmark.

USG Corporation (Chicago, U.S.), now part of Knauf Group, is a leading North American manufacturer of gypsum wallboard, plasters, and related interior solutions under the SHEETROCK® and CGC brands. The company operates integrated quarries and plants in the United States and Canada, with modernization programs underway at major facilities to improve automation, energy efficiency, and flexibility in using both natural and synthetic gypsum. Strategic investments in new plants in Alberta and upgrades in Ohio, Florida, and California are aimed at supporting housing growth and infrastructure renewal across North America.

Companies Covered in Drywall & Building Plasters Market

- Saint‑Gobain S.A.

- Knauf Gips KG

- USG Corporation

- Global Gypsum Company Co. Ltd.

- Etex S.A.

- Georgia Pacific LLC

- LafargeHolcim Ltd.

- CertainTeed Corporation

- Gyptec Iberica

- Fermacell GmbH

- National Gypsum Company

- Yoshino Gypsum Co., Ltd.

- Beijing New Building Materials (BNBM)

Frequently Asked Questions

The global Drywall & Building Plasters Market is expected to be valued at around US$ 20.1 Bn in 2026 and is projected to reach about US$ 32.9 Bn by 2033, reflecting a forecast CAGR of roughly 7.3% between 2026 and 2033, compared with an estimated historical CAGR of about 6.5% over 2020–2025.

Key demand drivers include steady growth in global construction output, faster expansion in emerging markets, rapid urbanization, and increasing emphasis on lightweight, fire‑resistant, and thermally efficient interior wall and ceiling systems that support green building and net‑zero targets.

On a product basis, Gypsum-based materials lead the market, with regular gypsum drywall alone accounting for 58% of global drywall shipments by area.

Asia Pacific emerges as the fastest-growing regional market driven by unprecedented urbanization, with 68% of the global population projected to reside in urban areas by 2050.

Significant opportunities include synthetic gypsum adoption and circular economy integration, where the Synthetic Gypsum Market is projected to grow at 4.6% CAGR through 2032, driven by environmental regulations encouraging industrial waste valorization and providing 28% reduction in raw material extraction needs.

Prominent players include Saint‑Gobain S.A., Knauf Gips KG, USG Corporation (and CGC Inc. in Canada), Etex S.A., Georgia Pacific LLC, National Gypsum Company, Global Gypsum Company Co. Ltd., Gyptec Iberica, Fermacell GmbH, and Yoshino Gypsum Co., Ltd., which collectively operate a large share of global wallboard capacity and shape technology, sustainability, and system specifications in the market.