- Nutraceuticals & Functional Foods

- Digestive Health Supplements Market

Digestive Health Supplements Market Size, Share, and Growth Forecast 2026 - 2033

Digestive Health Supplements Market by Product Type (Probiotics, Prebiotics, Enzymes), Form (Capsules, Tablets, Powder, Others), Sales Channel (Supermarkets, Pharmacies, Online Stores, Specialty Stores), by Regional Analysis, 2026 - 2033

Digestive Health Supplements Market Share and Trends Analysis

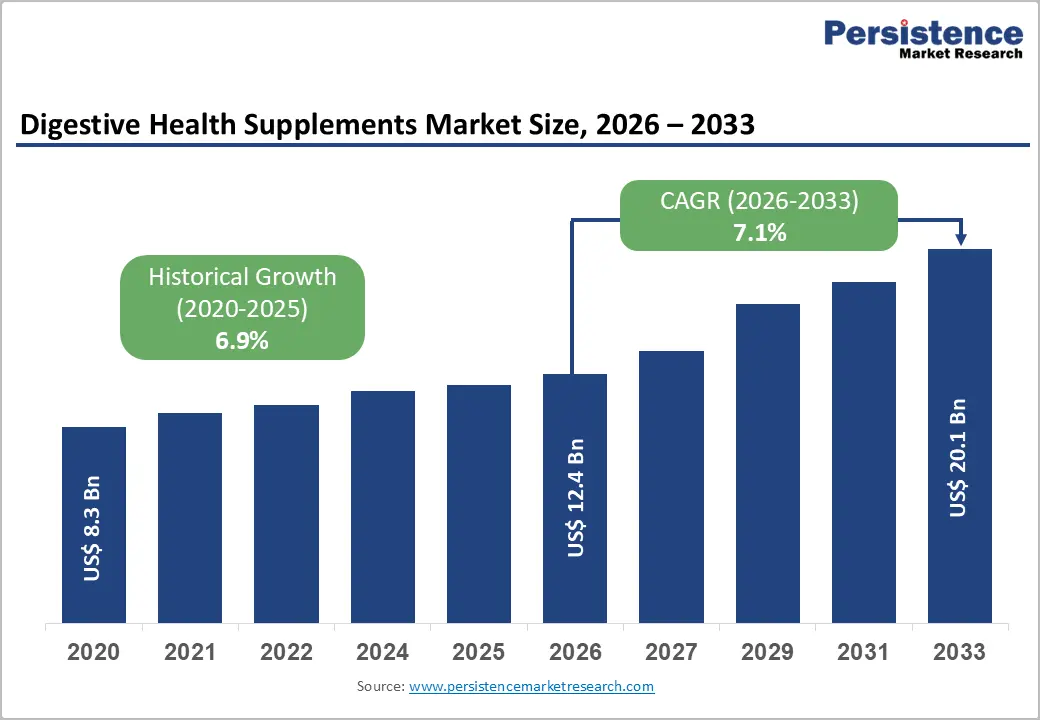

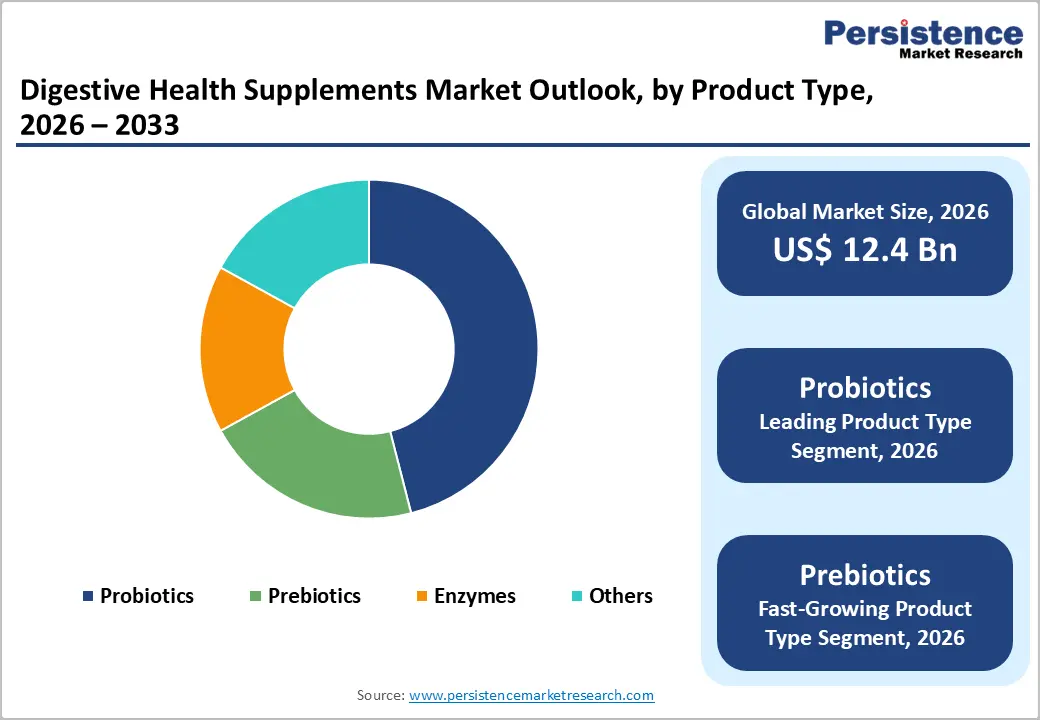

The global digestive health supplements market size is expected to be valued at US$ 12.4 billion in 2026 and projected to reach US$ 20.1 billion by 2033, growing at a CAGR of 7.1% between 2026 and 2033. Robust growth is underpinned by the high and rising burden of functional gastrointestinal disorders, with global irritable bowel syndrome prevalence estimates ranging between 13.21% and 17.14% depending on diagnostic criteria, alongside a pooled global functional dyspepsia prevalence of about 8.4%, which together create sustained demand for symptom-relieving and microbiome-modulating products. At the same time, digestive diseases overall accounted for about 2.56 million deaths and nearly 88.99 million disability-adjusted life years worldwide in 2019, highlighting the scale of unmet need that encourages consumers and healthcare professionals to adopt supportive supplements.

Demand is also amplified by the mainstreaming of dietary supplements in daily health routines, with the Council for Responsible Nutrition (CRN) reporting that about 74% of U.S. adults use dietary supplements and 55% qualify as regular users. Within this landscape, probiotic supplements have become a core growth engine: data shared by the International Probiotics Association (IPA) indicate that the global probiotic supplements market was already around US$ 8.2 billion in 2022, while European probiotic food and supplement sales reached roughly €9.5 billion in 2022, with supplements representing a significant and fast-growing share. Coupled with the expansion of e-commerce and personalized nutrition platforms, these structural trends support steady medium-term growth for digestive health supplements across product types and regions.

Key Industry Highlights:

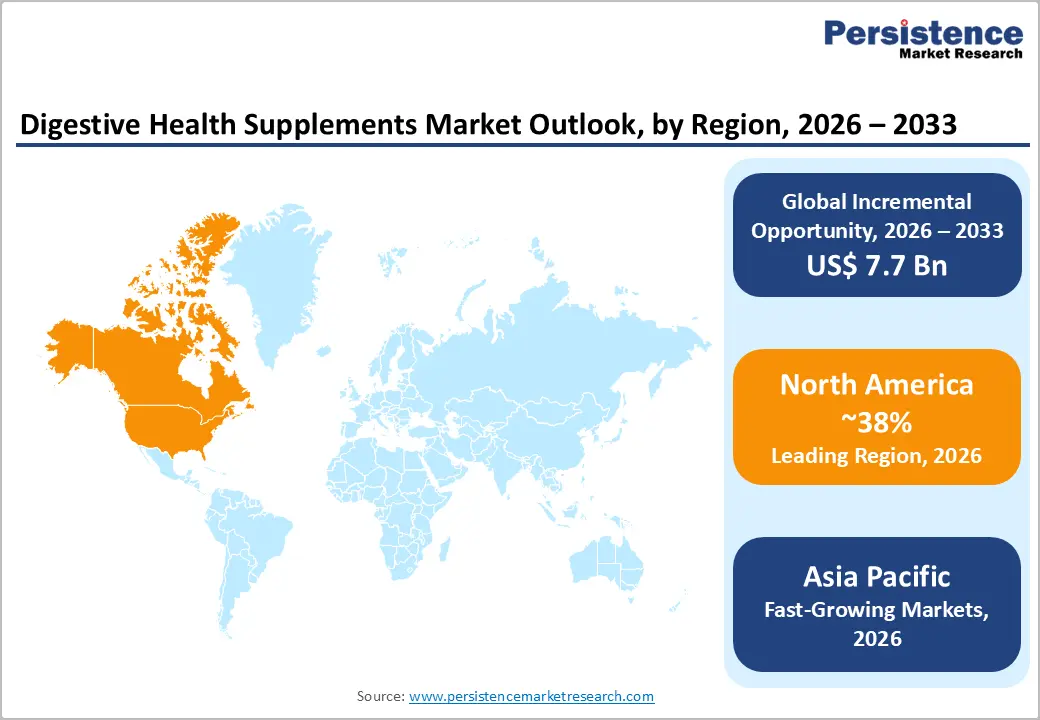

- North America leads the digestive health supplements market, underpinned by a high burden of digestive diseases affecting 60-70 million Americans, strong supplement penetration with about 74% of adults using supplements, and a well-established regulatory and retail ecosystem focused on preventive gut-health solutions.

- Asia Pacific represents the fastest-growing region, as large populations in China, Japan, India, and ASEAN adopt probiotics, prebiotics, and digestive enzymes amid rising awareness of microbiome health, expanding middle-class incomes, and rapid development of supportive probiotic regulations.

- Probiotics are the dominant product type, capturing about 46% of global digestive health supplement revenues in 2025 and supported by extensive clinical evidence, strong physician endorsement, and robust consumer adoption across Europe, North America, and Asia Pacific.

- Capsules are the leading dosage form, with technical data showing they account for roughly 50% of new nutraceutical product launches and more annual product introductions than any other supplement format, while gummies and other novel forms deliver the fastest growth momentum.

| Key Insights | Details |

|---|---|

| Digestive Health Supplements Market Size (2026E) | US$ 12.4 billion |

| Market Value Forecast (2033F) | US$ 20.1 billion |

| Projected Growth CAGR (2026 - 2033) | 7.1% |

| Historical Market Growth (2020 - 2025) | 6.9% |

DRO Analysis

Drivers - High Burden of Digestive and Functional Gastrointestinal Disorders

A major growth driver for the digestive health supplements market is the high and persistent burden of digestive and functional gastrointestinal diseases globally. Meta-analytic data suggest that irritable bowel syndrome affects between 13.21% and 17.14% of adults worldwide depending on Rome III versus Rome IV criteria, while functional dyspepsia affects about 8.4% of the global adult population, with higher prevalence in women. Broader functional gastrointestinal disorders are also widespread, with one international study reporting that about 49% of females and 36.6% of males met criteria for at least one FGID, including constipation, dyspepsia, and IBS. In the United States, the National Institute of Diabetes and Digestive and Kidney Diseases (NIDDK) estimates that 60-70 million people live with digestive diseases, driving tens of millions of ambulatory visits and substantial healthcare expenditure. As patients seek non-prescription, long-term strategies to manage bloating, discomfort, irregularity, and related symptoms, demand for probiotics, prebiotics, and digestive enzymes that support gut function and microbiota balance continues to rise.

Shift Toward Preventive and Personalized Nutrition Anchored in Microbiome Science

The market also benefits from a powerful shift toward preventive health and personalized nutrition, whereby consumers use supplements proactively to maintain wellness rather than only to treat acute disease. Surveys conducted for CRN and Ipsos show that around 74% of Americans use dietary or nutritional supplements, with roughly 92% of users agreeing that supplements are essential to maintaining their health and many seeking tailored regimens. Over the three decades since the Dietary Supplement Health and Education Act (DSHEA) of 1994 defined the regulatory framework for supplements as a category of food, the U.S. domestic dietary supplements market has grown from about 4,000 products to more than 80,000, supporting a domestic market estimated near US$ 60 billion and an international market around US$ 200 billion. At the same time, clinical research increasingly shows that probiotic interventions can beneficially modulate gut microbiota and outcomes in high-risk groups such as older Chinese adults with chronic metabolic and cardio-cerebrovascular diseases, reinforcing the rationale for targeted probiotic supplementation in aging populations. Together, rising health literacy, better access to microbiome science, and the proliferation of evidence-backed formulations underpin robust, long-term demand for digestive health supplements.

Restraints - Regulatory Complexity and Stringent Claim Substantiation Requirements

Despite attractive growth prospects, the digestive health supplements market faces regulatory complexity that can slow innovation and raise compliance costs. In the United States, products positioned as dietary supplements fall under DSHEA, which treats them as a category of food and does not require pre-market approval by the Food and Drug Administration (FDA) but places responsibility for safety and truthful, non-misleading claims squarely on manufacturers. Structure-function and health claims must be substantiated by evidence acceptable to experts, yet supporting data need not be publicly disclosed, prompting scrutiny from regulators and consumer advocates. In Europe, the European Food Safety Authority (EFSA) has historically rejected most probiotic health claims, and a 2024 review of probiotic claims regulations highlights divergent approaches between the EU, U.S., and Asia-Pacific, making cross-border harmonization challenging for global brands. In Southeast Asia, only a subset of countries have specific probiotic regulations, and requirements around strain listing, minimum viable counts, and labeling differ meaningfully across markets, complicating regional market access strategies.

Safety Concerns, Quality Variability, and Limited Consumer Understanding

Another restraint is the ongoing concern about product quality, safety in vulnerable populations, and uneven consumer understanding of when and how to use digestive health supplements. Scientific reviews of probiotic safety note that while probiotics are generally well tolerated in healthy individuals, cases of Saccharomyces boulardii fungemia and rare bacteremia have been reported in critically ill or immunocompromised patients, underscoring the need for careful risk-benefit assessment in hospital settings. Regulators such as the Food Safety and Standards Authority of India (FSSAI) mandate that probiotic foods and supplements use approved strains and typically maintain viable counts of at least 10^8 CFU per recommended daily serving, with lower counts allowed only when supported by clinical evidence. However, global reviews of dietary supplements continue to identify variability in strain labeling, CFU counts at end-of-shelf-life, and stability across formats, while many consumers still conflate probiotics, prebiotics, and digestive enzymes or use them without professional guidance. These factors can erode trust, limit repeat purchase, and expose companies to regulatory or reputational risk if not proactively managed through quality systems and education.

Opportunities - Acceleration of Prebiotics, Synbiotics, and Advanced Microbiome-targeted Solutions

One of the most attractive opportunities lies in the rapid expansion of prebiotics, synbiotics, and next-generation microbiome-targeted solutions within the digestive health supplements portfolio. Consensus statements from Asia-Pacific gastroenterology experts highlight growing clinical interest in optimizing gut microbiota composition to prevent and manage disorders ranging from IBS to inflammatory bowel disease, with probiotics and related interventions playing an increasing role in regional practice. Market data from IPA show that probiotic supplements already constitute a multi-billion-dollar segment with high single-digit CAGRs, while European probiotic supplement sales alone exceeded about €1.6 billion in 2022 when e-commerce volumes are included.

As research supports the complementary roles of prebiotic fibers, specific probiotic strains, and postbiotics, companies can capture incremental value by formulating synbiotic products that deliver clinically supported outcomes such as reduced bloating, improved stool consistency, or enhanced immune resilience in clearly defined user groups. This creates a particularly strong runway for prebiotics, identified as one of the fastest-growing product types in several digestive and probiotic supplement sub-markets, as brands respond to consumer interest in “feeding the good bacteria” and pairing microbiome support with broader metabolic and bone-health benefits.

Digital Commerce, Omnichannel Distribution, and Personalized Gut-health Offerings

A second major opportunity arises from the convergence of digital commerce, data-driven personalization, and omnichannel retail models. In Europe, IPA Europe data show that probiotic supplement online sales nearly doubled from about €99 million in 2020 to roughly €190 million in 2021, and subsequent analyses indicate that online probiotic supplement revenues continued to grow at double-digit rates through 2024. This shift reflects consumers’ increasing comfort with purchasing microbiome-support products via e-commerce platforms and cross-border marketplaces, especially when domestic regulatory environments restrict on-pack probiotic claims. Companies such as Amway and others are investing in microbiome-focused innovation hubs and analytical approaches that match individual fecal microbiome profiles with specific probiotic blends, paving the way for more personalized gut-health subscription services and diagnostics-linked supplement regimens. As wearable devices, at-home microbiome testing, and digital coaching converge, brands that integrate personalized recommendations, evidence-based formulations, and seamless online replenishment are well-positioned to capture outsized growth in the digestive health supplements market.

Category-wise Analysis

Form Insights

By form, capsules are the dominant delivery format in the digestive health supplements market, especially for probiotic and enzyme-based products. Technical reviews of dietary supplement dosage forms note that capsules are the “go-to” format in the U.S. nutraceutical market, with approximately 3,000-3,200 capsule-based products launched annually over the last several years more than any other single dosage form. A global white paper analyzing nutraceutical launches indicates that capsules, including softgels and hard capsules, collectively account for about 50% of new product introductions, reflecting manufacturers' preference for formats that offer dose accuracy, stability, and protection of sensitive ingredients such as live bacterial cultures. Consumer research similarly shows that capsules and tablets remain the preferred formats for around 42-41% of U.S. supplement users, even as interest in gummies and chewables grows, underscoring capsules’ entrenched position for serious, efficacy-focused products such as digestive health supplements. While powders and emerging formats (gummies, liquids, stick packs grouped under “Others”) are growing rapidly, for example, increased by about 44% between 2019 and 2020 capsules currently maintain the largest share of volume and value in the digestive health segment due to their practicality and clinical image.

Sales Channel Insights

Across sales channels, pharmacies and related brick-and-mortar outlets emerge as the leading route to market for digestive health supplements, while online stores represent the fastest-growing channel. Survey data commissioned by the Consumer Healthcare Products Association (CHPA) show that about 73% of U.S. voters identify local brick-and-mortar retailers—particularly pharmacies and chain drug stores as their most common point of purchase for supplements, underscoring the central role of pharmacy-based counseling and trust in this category. Complementary CRN survey results reveal that approximately 93% of supplement users had purchased products through mass-market retail within the past year, while only about 25% reported buying supplements online, confirming the dominance of physical outlets even in digitally advanced markets. At the same time, probiotic-specific market insights from IPA Europe and Lumina Intelligence indicate that online probiotic supplement sales in Europe grew from roughly €99 million in 2020 to around €190 million in 2021, and continued to record 15-20% year-on-year growth through 2024, making e-commerce the most dynamic sales channel. For digestive health supplements, this translates into a landscape where pharmacies and supermarket pharmacy aisles hold the largest current share, while online stores and specialty digital platforms deliver the highest incremental growth and support cross-border brand expansion.

Regional Insights

North America Digestive Health Supplements Market Trends and Insights

North America dominates the Digestive Health Supplements Market due to strong consumer awareness, high healthcare spending, and a well-established nutraceutical industry. The region benefits from widespread adoption of preventive healthcare practices, with consumers increasingly focusing on gut health, immunity, and overall wellness. Probiotics remain the most popular product category, supported by clinical research and frequent product innovations. There is also a growing demand for prebiotics and enzyme-based supplements as digestive disorders such as bloating, IBS, and lactose intolerance become more common.

The presence of major market players, advanced retail infrastructure, and strong e-commerce penetration further supports market growth. Additionally, clean-label, plant-based, and personalized nutrition trends are gaining traction, with consumers preferring natural and scientifically backed ingredients. The aging population and rising interest in functional foods and dietary supplements continue to drive consistent demand, reinforcing North America’s position as the leading regional market.

Asia Pacific Digestive Health Supplements Market Trends and Insights

Asia Pacific is emerging as a high-growth region in the Digestive Health Supplements Market, driven by rising health awareness, urbanization, and changing dietary habits. Increasing consumption of processed foods and irregular lifestyles have led to a higher prevalence of digestive issues, boosting demand for gut health solutions. Countries like China, India, and Japan are witnessing strong growth due to expanding middle-class populations and improving access to healthcare products. Traditional knowledge of fermented foods and herbal remedies is also supporting the adoption of probiotics and plant-based supplements. Additionally, growing e-commerce platforms and digital health awareness campaigns are making these products more accessible to consumers. The demand for preventive healthcare, along with increasing disposable incomes, is further accelerating market expansion. As a result, Asia Pacific is expected to register the fastest growth, supported by both local manufacturers and international brands expanding their presence.

Competitive Landscape

The global digestive health supplements market is moderately fragmented, with a mix of established players and emerging brands competing across product categories. Companies focus on innovation, particularly in probiotics, prebiotics, and enzyme formulations, to differentiate their offerings. Strong emphasis is placed on clinical validation, clean-label ingredients, and personalized nutrition to attract health-conscious consumers. Strategic partnerships, product launches, and expansion into e-commerce channels are key competitive strategies. Additionally, regional players leverage traditional and herbal ingredients to gain a niche advantage.

Key Developments:

- In March 2026, Nature Made expanded its digestive health portfolio by launching new SuperGreens and Digestive Enzymes products, strengthening its presence in the gut health segment. The SuperGreens formulations included probiotics and nutrient-rich vegetable blends, while the Digestive Enzymes product featured a clinically studied blend of five enzymes designed to help break down various food groups and support digestive comfort.

- In February 2026, Opella partnered with the Long Chau Pharmacy and Vaccination Centre System in Vietnam to launch a community-focused initiative aimed at improving digestive and bone health awareness and management. The collaboration included a formal agreement to enhance pharmacist capabilities through training in disease knowledge, risk management, and patient counselling.

- In June 2025, Nature Made announced a strategic partnership with HelloFresh and New York Times bestselling author Justine Doiron to promote digestive health through integrated food and supplement solutions. The collaboration introduced limited-edition “gut-friendly” meal kits featuring fiber-rich, chef-curated recipes designed to support digestion, available for a defined period.

Companies Covered in Digestive Health Supplements Market

- Nestec S.A

- Nutricia NV

- Alimentary Health Limited

- Lonza Group Ltd

- Amway

- Bayer AG

- Herbalife Nutrition Ltd

- NOW Foods

- Nature’s Bounty

- Garden of Life®

- Zenwise

- HealthForce

- Olly, Pfizer Inc.

- Glanbia PLC

- Chr. Hansen Holding A/S

- IFF

- Yakult Honsha Co., Ltd.

Frequently Asked Questions

The global Digestive Health Supplements market is expected to reach about US$ 12.4 billion in 2026, based on the provided trajectory and supported by strong underlying growth in probiotics, prebiotics, and digestive enzyme categories.

Key demand drivers include the high global prevalence of functional gastrointestinal disorders such as IBS and functional dyspepsia together affecting more than 10-15% of adults alongside an increasing consumer focus on preventive health, microbiome support, and evidence-backed probiotic and prebiotic formulations.

North America leads the global Digestive Health Supplements market, reflecting the combination of 60-70 million Americans living with digestive diseases, high supplement penetration with about 74% of adults using supplements, and a mature regulatory and retail ecosystem favoring innovation in gut-health products.

A major opportunity lies in advanced microbiome-targeted solutions especially prebiotics, synbiotics, and personalized probiotic regimens leveraging growing clinical evidence, rapid e-commerce expansion, and consumer willingness to pay for targeted digestive comfort, immune support, and healthy-aging solutions.

Leading players include Nestec S.A. (Nestlé Health Science / Garden of Life®), Nutricia NV, Alimentary Health Limited, Lonza Group Ltd, Amway, Bayer AG, Herbalife Nutrition Ltd, NOW Foods, Nature’s Bounty, Garden of Life®, Zenwise, HealthForce, Olly, and other global and regional specialists in probiotics, enzymes, prebiotics, and digestive-health solutions.