- Pharmaceuticals

- Digestive Remedies Market

Digestive Remedies Market Size, Share, and Growth Forecast 2026 - 2033

Digestive Remedies Market by Product Type (Antacids, Laxatives, Anti-diarrheal products, Digestive enzymes, Probiotics & prebiotics, Herbal/natural remedies, Acid-reducing drugs including PPIs and H2 blockers, Others), by Application (Acid reflux/heartburn, Constipation, Diarrhea, Indigestion, Others), by Form (Tablets, Capsules, Powders, Liquids, Gummies/gels), by Sales Channel (Pharmacies & drugstores, Online stores, Supermarkets/hypermarkets, Hospital pharmacies) and Regional Analysis, 2026-2033.

Digestive Remedies Market Size and Trend Analysis

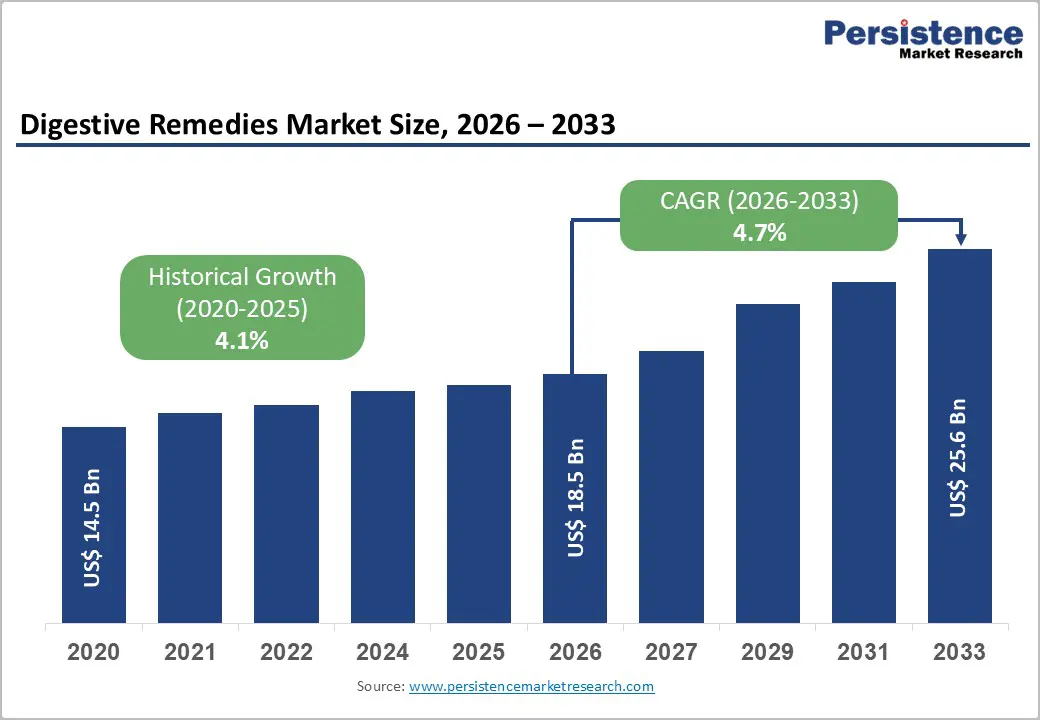

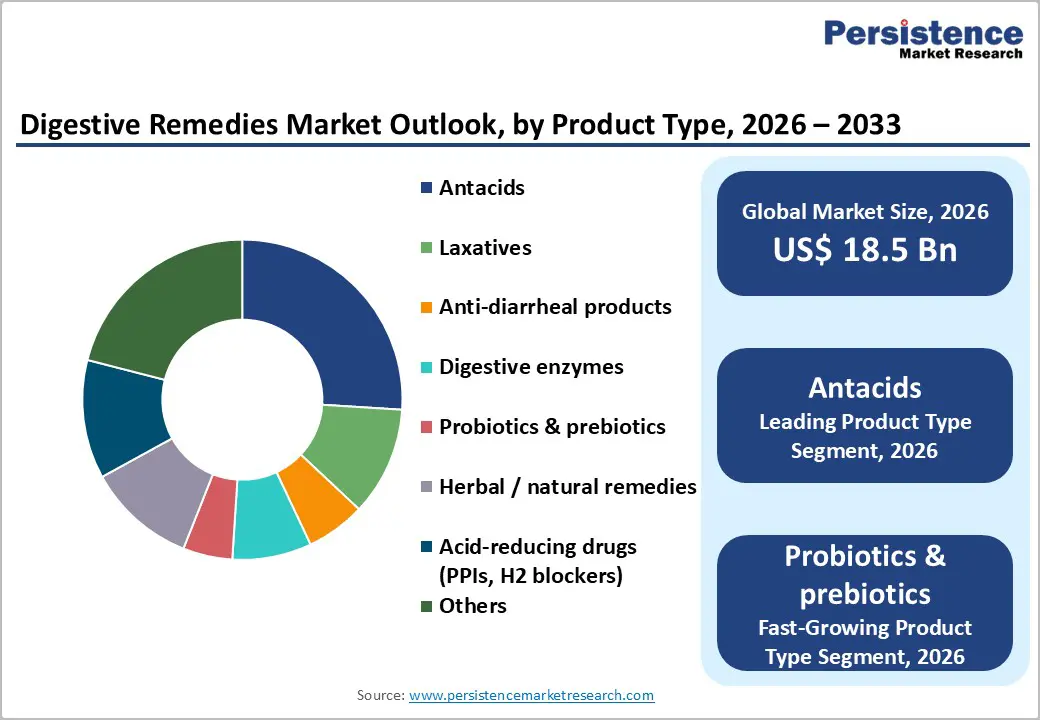

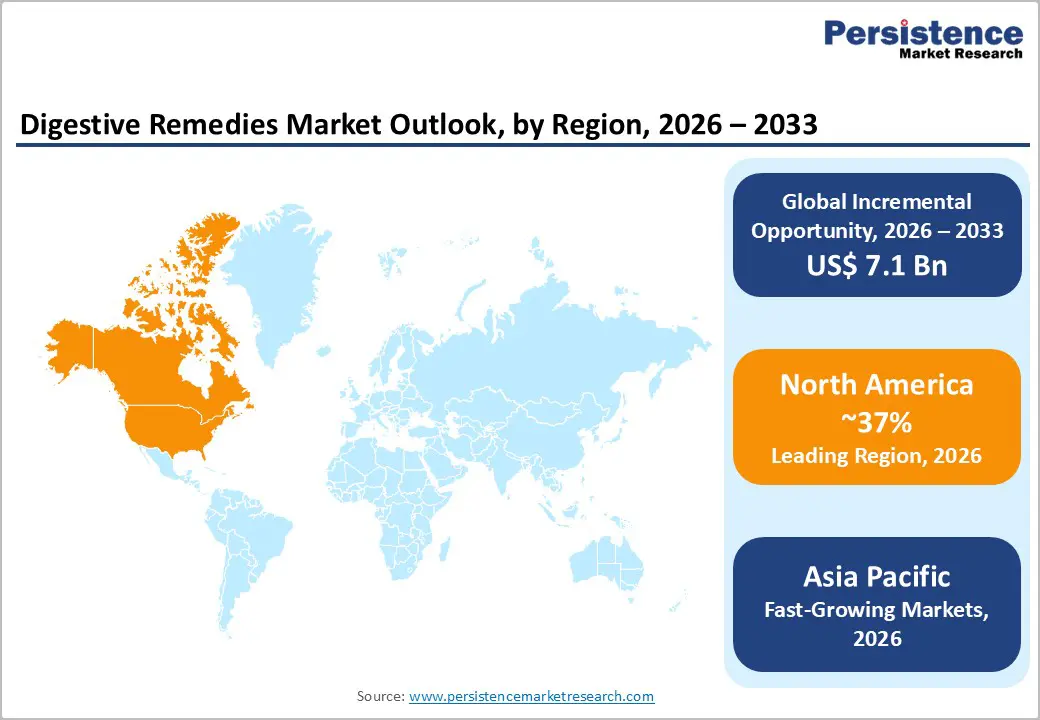

The global Digestive Remedies Market is expected to be valued at US$ 18.5 billion in 2026 and projected to reach US$ 25.6 billion by 2033, growing at a CAGR of 4.7% between 2026 and 2033.

Market expansion is fundamentally driven by three distinct, non-overlapping mechanisms rather than traditional demand saturation patterns. First, the transition from commodity antacid segments toward clinically validated probiotic and enzyme categories creates pricing power expansion, with scientific validation enabling 20-30% premium pricing over generic alternatives and establishing 8.6% CAGR growth velocity substantially exceeding mature antacid segment decline. Second, the emergence of unexpected demand vectors through GLP-1 adoption for anti-obesity applications creates secondary constipation effects, driving laxative demand increments disconnected from traditional gastrointestinal disease progression and generating estimated 9% of new laxative shoppers utilizing anti-obesity medications. Third, regional market maturation asymmetries position Asia-Pacific as fastest-growing segment through simultaneous forces: rising disposable incomes enabling premium product access, integration of traditional medicine systems with modern clinical validation, and rapid e-commerce penetration establishing direct-to-consumer supply chains in previously underserved populations.

Key Highlights:

- Leading Region: North America leads with 37% market share in 2025, supported by mature healthcare, high consumer awareness, OTC accessibility, and rising GLP-1 use boosting constipation product demand.

- Fastest Growing Region: Asia Pacific grows fastest with 14%+ CAGR through 2032, driven by rising incomes, integration of traditional and modern therapies, urbanization, and expanding e-commerce.

- Dominant Product Segment: Antacids hold 26% share in 2025, offering easy access and quick relief, though growth is limited by pricing pressures and shift toward clinically validated alternatives.

- Fastest Growing Product Segment: Probiotics & prebiotics grow at 8.6% CAGR, fueled by clinical validation, improved bioavailability, and growing gut health awareness.

- Key Opportunity: Gut-brain axis research and psychobiotics offer high growth, premium pricing, and differentiation beyond traditional GI treatments.

| Key Insights | Details |

|---|---|

| Digestive Remedies Market Size (2026E) | US$ 18.5 billion |

| Market Value Forecast (2033F) | US$ 25.6 billion |

| Projected Growth CAGR (2026-2033) | 4.7% |

| Historical Market Growth (2020-2025) | 4.1% |

Market Dynamics

Market Growth Drivers

Clinical Validation and Premium Positioning of Probiotic-Prebiotic Combination Therapies

Clinical validation and premium positioning of probiotic–prebiotic combination therapies are emerging as strong drivers for the digestive remedies market. Increasing clinical evidence demonstrating the effectiveness of synbiotic formulations in improving gut microbiota balance, reducing IBS symptoms, enhancing digestion, and supporting immune health is strengthening physician and consumer confidence. As these combinations move beyond wellness claims to clinically supported benefits, they are gaining acceptance in both preventive and therapeutic digestive care. At the same time, companies are positioning these products as premium solutions, emphasizing strain specificity, targeted indications, superior survivability, and advanced delivery technologies. This allows higher pricing and repeat usage, particularly among urban and health-conscious consumers. The convergence of scientific credibility and premium branding is expanding market value, encouraging long-term consumption, and driving faster growth of probiotic–prebiotic therapies within the broader digestive remedies landscape.

Emerging Demand Vectors Through Pharmaceutical Side Effect Mitigation and Lifestyle-Related Gastrointestinal Dysfunction

Emerging demand for digestive remedies is being strongly driven by the growing need to manage pharmaceutical side effects and lifestyle-related gastrointestinal dysfunctions. Long-term use of antibiotics, painkillers, oncology drugs, and metabolic therapies frequently disrupts gut flora, leading to acidity, diarrhea, constipation, and bloating, increasing reliance on supportive digestive solutions. At the same time, modern lifestyles marked by irregular eating habits, high-fat and processed diets, stress, alcohol consumption, and sedentary behavior are accelerating the incidence of chronic digestive complaints. Urban populations are increasingly experiencing functional disorders such as indigestion, IBS, and acid reflux at younger ages. This dual burden—drug-induced gastrointestinal imbalance and lifestyle-driven digestive stress—is shifting consumer focus toward preventive and adjunct digestive care. As awareness rises, demand is expanding beyond episodic relief toward routine, long-term digestive health management.

Market Restraints

Commodity Pricing Pressure and Margin Compression in Mature Antacid Segments

The digestive remedies market confronts structural margin compression within mature antacid segments, which command 26% market share in 2025 while experiencing minimal growth velocity. Antacids market growth of only 3.3% CAGR through 2034 reflects commodity positioning where over-the-counter availability and consumer price sensitivity create intense competitive pressure constraining profitability. Calcium carbonate and aluminum hydroxide-based formulations offer minimal differentiation opportunities, establishing price-based competition dynamics that compress margins across manufacturer portfolios. The transition of consumer preference toward plant-based and natural alternatives driven by clean-label movements further erodes traditional antacid market shares, with manufacturers unable to justify premium pricing for synthetic chemical formulations in context of emerging herbal and enzyme-based alternatives. Product accessibility through supermarkets and drugstores at aggressive promotional pricing further accelerates margin compression, establishing structural headwinds constraining revenue expansion potential within commodity segments despite underlying demand persistence.

Product Quality, Stability, and Regulatory Compliance Barriers Limiting Probiotic Market Penetration

The probiotic and prebiotic segments confront significant technical barriers constraining market expansion and profitability potential. Probiotic shelf-life limitations and bacterial strain viability degradation create substantial manufacturing and distribution challenges, with tropical climates and ambient temperature exposure demonstrating pronounced adverse impacts on product efficacy. Quality consistency challenges have manifested through documented product recall incidents, which undermine consumer confidence and brand reputation, establishing regulatory compliance requirements constraining market participants unable to implement robust manufacturing quality control infrastructure. Tropical Asian and Southeast Asian climates demonstrate particularly pronounced constraints on probiotic product stability, limiting market penetration in regions demonstrating highest growth potential. Regulatory complexity across heterogeneous jurisdictional frameworks including inconsistent prebiotic classification policies and varying probiotic strain approval requirements creates operational complexity and capex requirements for manufacturers seeking to achieve multi-regional distribution. Strain identification and characterization requirements impose substantial research and documentation obligations constraining smaller competitors unable to finance clinical validation infrastructure.

Market Opportunities

Emerging Gut-Brain Axis Research Validating Psychobiotic Applications and Expanding Addressable Market Beyond Traditional Gastrointestinal Indications

The digestive remedies market is experiencing addressable market expansion through emerging psychobiotic applications targeting mental health, stress, and sleep dysfunction through microbiota-modulating mechanisms. Gut-brain axis research demonstrating bidirectional communication between intestinal microbiota and central nervous system establishes novel therapeutic applications for probiotic interventions extending beyond traditional gastrointestinal indications. Clinical research publications validating microbial metabolite production including short-chain fatty acids’ influence on neurochemistry create scientific foundation for consumer marketing campaigns positioning probiotics as mood-optimization and stress-management solutions. This market expansion mechanism positions probiotic formulations as daily wellness supplements integrated into preventive health regimens rather than symptom-driven treatments, enabling sustained consumer spending independent of acute gastrointestinal dysfunction episodes.

Category-wise Insights

Product Type Analysis

Antacid Dominance Within Commodity Segment Constrained by Form Factor and Clinical Validation Transition Dynamics

Antacids maintain dominant positioning within digestive remedies market with 26% market share in 2025, leveraging accessibility advantages, immediate symptom relief mechanisms, and established consumer familiarity spanning decades. Calcium carbonate and aluminum hydroxide-based formulations command market share predominantly through over-the-counter availability in pharmacies, supermarkets, and convenience channels, establishing low barriers to consumer access. However, structural market dynamics demonstrate accelerating share migration toward clinically validated alternatives, with probiotic and enzyme categories experiencing 8.6% and 9.4% CAGR respectively substantially exceeding antacid growth. GERD prevalence affecting 20% of United States population establishes substantial antacid consumer base maintaining stable demand independent of clinical validation; however, emerging consumer preference for plant-based and natural formulations constrains premium pricing power. Competitive intensity within antacid segments from over-the-counter generic products priced aggressively creates margin compression dynamics limiting profitability expansion. Laxative category dominance within constipation treatment applications, commanding 55.2% market share driven by consumer accessibility and established therapeutic efficacy, demonstrates resilience constrained primarily by episodic usage patterns versus chronic supplement integration.

Application Analysis

Acid Reflux and Indigestion: Establishing Primary Addressable Market with Emerging Gut Health Diagnostics, Creating Growth Acceleration Vector

Acid reflux and heartburn applications establish the largest end-use category within digestive remedies market, driven by GERD prevalence rates of 20% in developed markets and accelerating incidence in emerging economies experiencing rapid urbanization. Chronic acid reflux management traditionally dominated by antacid products is experiencing gradual transition toward proton pump inhibitor and H2 blocker prescription alternatives providing superior efficacy for chronic symptom management. The application demonstrates structural demand resilience independent of market maturation, with underlying patient populations maintaining continuous requirement for symptom relief solutions. Indigestion applications demonstrate broader addressability across consumer segments, with enzyme supplementation and probiotic alternatives gaining market share through positioning as root-cause interventions addressing digestive dysfunction versus symptomatic antacid relief. Constipation applications experiencing exceptional 6.7% CAGR through 2034 demonstrate emerging demand vectors through GLP-1 induced side effects and rising awareness of fiber supplementation and laxative efficacy for chronic constipation management. Irritable bowel syndrome applications leveraging prebiotic and probiotic interventions emerging as fastest-growing segment within digestive remedies market, with prebiotic supplement CAGR of 11.3% through 2033 validating consumer shift toward functional microbiota optimization versus acute symptom treatment.

Regional Insights

North America Digestive Remedies Market Trends

North America continues to lead the digestive remedies market due to its high prevalence of gastrointestinal disorders, strong consumer awareness, and widespread use of over-the-counter digestive products. The region benefits from well-established healthcare infrastructure and easy access to pharmacies, supermarkets, and online channels, supporting strong product penetration. Rising incidence of acid reflux, obesity-related digestive issues, and stress-induced gut disorders has increased routine consumption of antacids, probiotics, and digestive enzymes. Consumers in North America also show a strong preference for preventive digestive health, driving demand for probiotics, prebiotics, and natural formulations. Additionally, continuous product innovation, premiumization, and clinically backed formulations have strengthened brand loyalty and repeat purchases, reinforcing North America’s position as the leading regional market for digestive remedies.

Asia Pacific Digestive Remedies Market Trends

Asia Pacific is emerging as a high-growth region in the digestive remedies market, driven by rapid urbanization, changing dietary habits, and increasing prevalence of gastrointestinal disorders. Rising consumption of processed foods, irregular meal patterns, and growing stress levels are contributing to higher incidences of acidity, indigestion, and constipation across both urban and semi-urban populations. Expanding middle-class income and improving healthcare access are enabling greater adoption of over-the-counter digestive remedies. The region is also witnessing strong demand for herbal and traditional digestive products, supported by long-standing use of natural remedies in countries such as India and China. Growth in e-commerce pharmacies, increased health awareness, and rising acceptance of probiotics and digestive enzymes among younger consumers are further accelerating market expansion across Asia Pacific.

Competitive Landscape

Market Structure Analysis

The competitive landscape of the digestive remedies market is marked by the presence of major global pharmaceutical and consumer health companies competing with niche nutraceutical and specialty gut-health brands. Established players leverage strong distribution networks, broad product portfolios, and significant marketing investments to maintain market share in segments like antacids, laxatives, and acid-reducing therapies. Meanwhile, newer entrants focus on innovative, clinically validated probiotic-prebiotic combinations and herbal formulations to capture premium and wellness-oriented consumers.

Companies Covered in Digestive Remedies Market

- Johnson & Johnson

- Procter & Gamble Co.

- GlaxoSmithKline plc (GSK)

- Pfizer Inc.

- Abbott Laboratories

- Bayer AG

- Sanofi S.A.

- Takeda Pharmaceutical Company

- Reckitt Benckiser Group plc

- Nestlé S.A.

- Danone S.A.

- Yakult Honsha Co., Ltd.

Frequently Asked Questions

The global Digestive Remedies Market is projected to achieve a valuation of US$ 18.5 billion in 2026.

The Digestive Remedies Market experiences growth propulsion through three distinct mechanisms: clinical validation enabling premium pricing for probiotic and enzyme categories at 8.6% and 9.4% CAGR, respectively, GLP-1 induced constipation side effects creating unexpected laxative demand vectors, and regional income convergence in Asia-Pacific driving premium digestive health supplement adoption among emerging middle-class consumer segments.

North America maintains global market leadership with 37% regional share in 2025, driven by mature healthcare infrastructure, established over-the-counter medication accessibility, and rising consumer awareness regarding digestive health optimization, supporting sustained premium-positioned product adoption through the forecast period.

Gut-brain axis research validating psychobiotic applications for mental health and stress management represents the highest-potential growth opportunity, establishing addressable market expansion beyond traditional gastrointestinal indications and enabling 15-25% premium pricing relative to commodity digestive enzyme offerings through clinical evidence and direct-to-consumer brand positioning.

The Digestive Remedies Market is dominated by Johnson & Johnson, Procter & Gamble, GlaxoSmithKline, Pfizer, Abbott Laboratories, and Bayer AG from pharmaceutical manufacturers, alongside Nestlé, Danone, and Yakult Honsha from functional food companies, collectively establishing diversified positioning across antacid, enzyme, probiotic, and herbal remedy categories through integrated distribution infrastructure and brand recognition.