- Industrial Machinery

- Air-Operated Double Diaphragm (AODD) Pump Market

Air-Operated Double Diaphragm (AODD) Pump Market Size, Share, and Growth Forecast 2026 - 2033

Air-Operated Double Diaphragm Pump Market by Material Type (Polypropylene (PP), PolyVinylidene Fluoride (PVDF), Stainless Steel (SS), Aluminum), Max Flow Rate (<100 LPM, 100-300 LPM, 300-500 LPM, 500-700 LPM, >700 LPM), Industry (Paints and Coatings, Food and Beverages, Pharmaceutical, Electronics, Wastewater Treatment, Oil & Gas, Other), and Regional Analysis for 2026 - 2033

Air-Operated Double Diaphragm (AODD) Pump Market Size and Trend Analysis

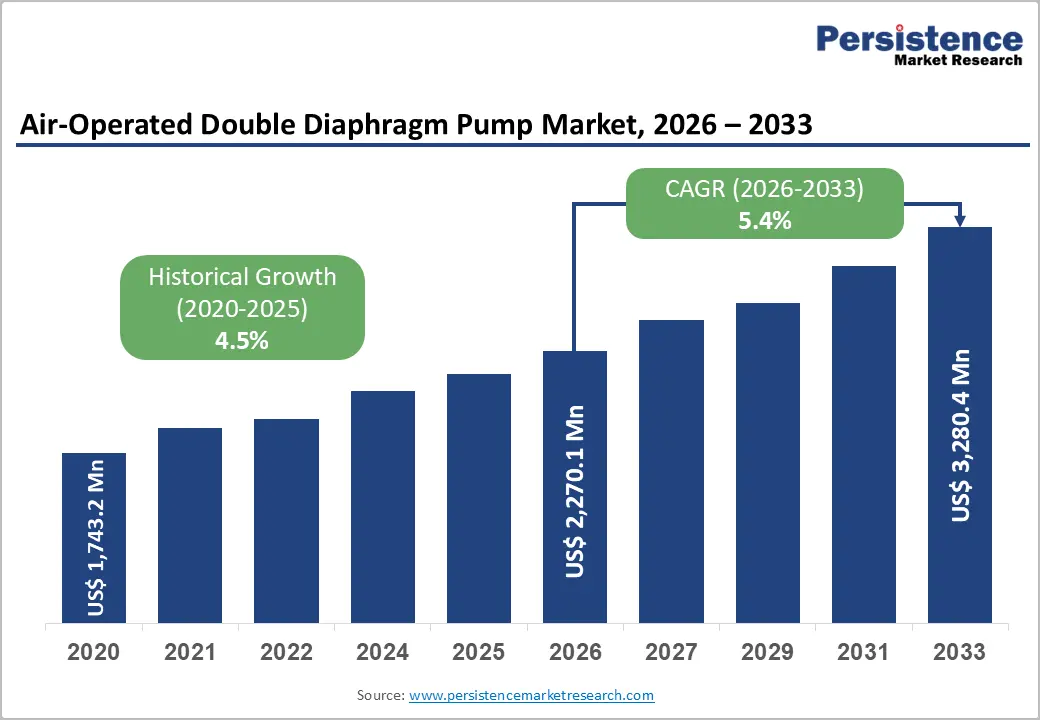

The global air-operated double diaphragm (AODD) pump market size is supposed to be valued at US$ 2.27 billion in 2026 and is projected to reach US$ 3.28 billion by 2033, growing at a CAGR of 5.4% between 2026 and 2033. The market is steadily expanding due to the rising demand for reliable fluid-handling solutions across hazardous and corrosive applications.

Growth is primarily supported by expanding industrial processing capacity, stricter wastewater discharge regulations enforced by agencies such as the U.S. Environmental Protection Agency (EPA), and rising investments in food, pharmaceutical, and specialty chemicals manufacturing. Additionally, AODD pumps offer dry-run capability, self-priming features, and explosion-proof suitability, making them critical in compliance-driven industries operating under standards defined by organizations such as the International Organization for Standardization (ISO) and the American Petroleum Institute (API).

Key Industry Highlights:

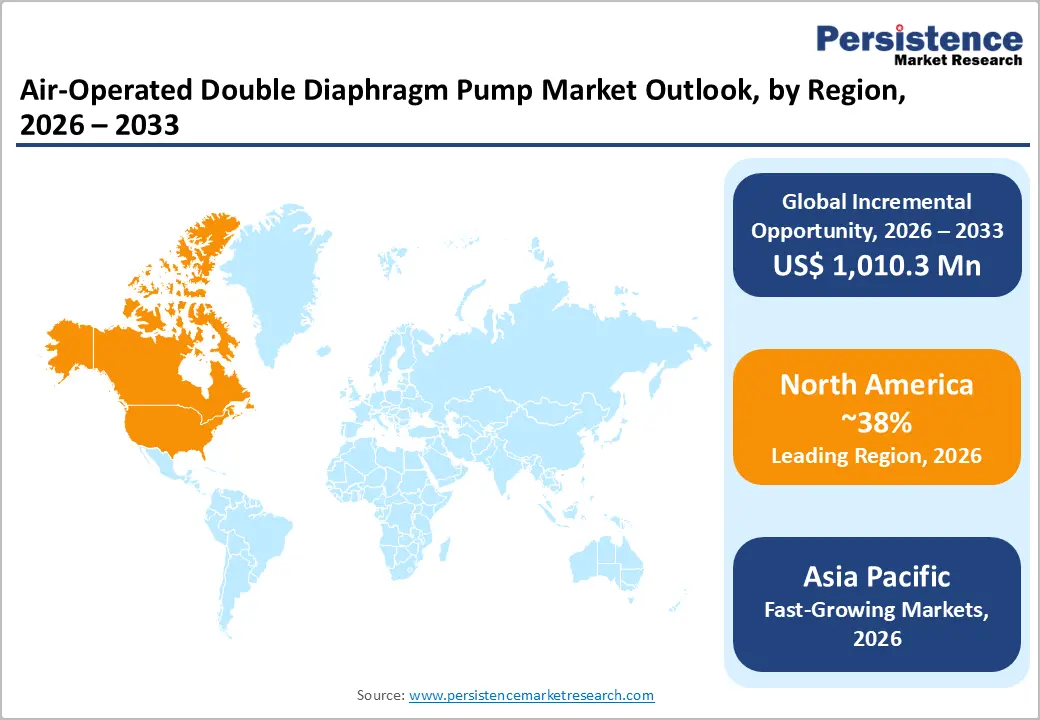

- Leading Region: North America dominates with 38% market share, driven by extensive chemical manufacturing infrastructure, stringent safety regulations enforced by OSHA, and an established industrial base supporting consistent replacement demand and aftermarket services.

- Fastest-Growing Region: Asia Pacific is projected to grow the fastest through 2033, driven by manufacturing expansion in China and India, semiconductor investments exceeding $450 billion, and environmental compliance driving wastewater treatment equipment procurement.

- Dominant Material Type: Polypropylene commands 42% share due to its cost-effectiveness, broad chemical compatibility with acids and alkalis, and suitability for general industrial applications, including chemical processing, mining, and wastewater treatment.

- Fastest Growing Material Type: PVDF material type segment grows at 6.2% CAGR driven by pharmaceutical industry expansion, semiconductor manufacturing growth, and increasing FDA regulatory requirements for ultra-pure, chemically resistant fluid handling equipment.

- Key Opportunity: Battery manufacturing expansion for electric vehicle production creates demand for specialized AODD pumps that handle aggressive electrode slurries and lithium carbonate electrolytes, with global battery production capacity projected to increase by 6x by 2030 per IEA projections.

| Key Insights | Details |

|---|---|

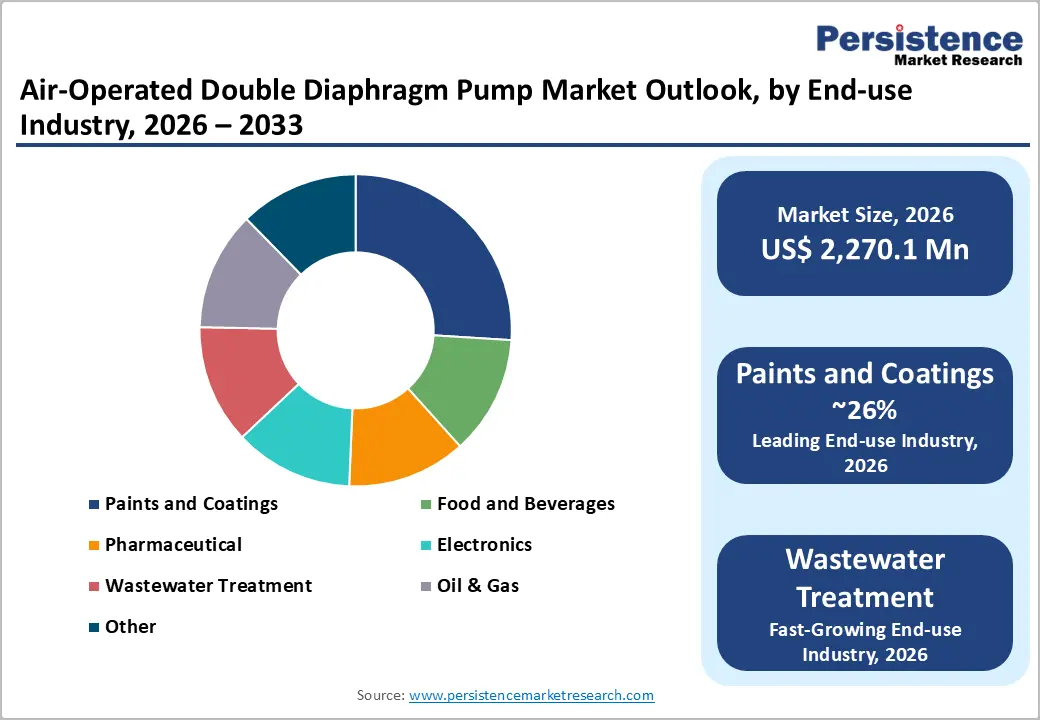

| Air-Operated Double Diaphragm (AODD) Pump Market Size (2026E) | US$ 2.27 Bn |

| Market Value Forecast (2033F) | US$ 3.28 Bn |

| Projected Growth CAGR (2026 - 2033) | 5.4% |

| Historical Market Growth (2020 - 2025) | 4.5% |

Market Dynamics Analysis

Drivers - Expansion of Wastewater Treatment Infrastructure

Global investments in industrial wastewater treatment are rising, driving strong demand for AODD pumps. Over 80% of wastewater in developing regions remains untreated, prompting regulatory actions by agencies such as the EPA and EEA to enforce stricter discharge standards and encourage the adoption of corrosion-resistant pumping systems. AODD pumps, particularly PP and PVDF types, are widely used for chemical dosing and sludge handling due to their durability and low maintenance requirements.

Growing wastewater infrastructure across Asia-Pacific and North America continues to strengthen demand. Additionally, global water scarcity and SDG-aligned mandates require wastewater treatment capacity to expand by 40% by 2030. In the U.S., funding through State Revolving Funds and the Bipartisan Infrastructure Law supports major system upgrades, reinforcing AODD pumps’ role in compliance-driven operations.

Expansion of Chemical Processing and Pharmaceutical Manufacturing

The global chemical industry continues to expand, thereby increasing the need for reliable fluid transfer solutions. Air-Operated Double Diaphragm (AODD) pumps are gaining prominence in batch processing operations for their ability to handle corrosive chemicals, solvents, and high-viscosity materials while minimizing contamination risks. In the pharmaceutical sector, stringent FDA and EMA requirements for sterile manufacturing have accelerated the adoption of sanitary-grade AODD pumps made from 316L stainless steel and PVDF, materials known for superior chemical resistance.

Growing pharmaceutical output, rising by 3.2% annually between 2020 and 2024, has further driven investment in compliant fluid handling systems. Additionally, the U.S. chemical industry’s shipments exceeding US$ 555 billion in 2024 underscore robust demand for advanced pumping technologies.

Restraint - Dependence on compressed air and operational energy considerations

Traditional AODD pumps depend on compressed air, increasing operating costs in facilities where air generation is expensive or where strict energy-efficiency mandates apply. Although electric-operated diaphragm pumps and improved pneumatic air-distribution systems help reduce this burden, lifecycle energy costs remain a challenge, especially in regions with high electricity prices or carbon-intensity regulations.

As a result, buyers now prioritize total cost of ownership and increasingly favor solutions that lower air consumption or incorporate electric drive options. AODD pumps also require dedicated compressed-air systems, which add significant capital and operational expenses. Compressed-air systems account for roughly 10% of industrial electricity use, operate at only 10-15% efficiency, and may incur losses of up to 70%, making electrically driven alternatives more attractive for continuous, energy-intensive applications.

Limited Efficiency in High-Head Applications

Pneumatic operation restricts AODD pumps to low- and medium-head applications below 50 meters, resulting in reduced performance in high-pressure environments as defined by Hydraulic Institute standards. These pumps also consume two to three times more compressed air than electric alternatives, increasing operating costs by up to 25% in continuous operations. This efficiency gap limits adoption in mining and deep-well oil and gas applications, slowing overall market momentum.

Emerging smart pump technologies with IoT-enabled monitoring and predictive maintenance are further challenging AODD competitiveness. Magnetically driven and progressive cavity pumps provide comparable chemical resistance with lower energy use and maintenance needs. Additionally, the EU Ecodesign Directive and potential German regulations for pneumatic equipment by 2027 are expected to favor more energy-efficient electric systems, reducing AODD uptake in compliance-driven markets.

Opportunity - Adoption in Battery Manufacturing and Electronics Production

The rapid growth of the electric vehicle industry is driving exceptional demand for lithium-ion battery manufacturing, with the IEA indicating that global capacity must increase sixfold by 2030 to meet production targets. This expansion requires specialized fluid-handling systems for electrode slurry preparation, electrolyte transfer, and cell-washing processes. AODD pumps made from PVDF and conductive materials are well-suited for handling aggressive battery chemistries and preventing contamination. NETZSCH Pumps & Systems notes their effectiveness in transferring highly viscous lithium carbonate slurries containing abrasive solids.

Major investments, such as Tesla’s Gigafactory expansions and CATL’s facilities in China and Hungary, necessitate large-scale deployment of these pumps. Additionally, semiconductor fabrication plants, backed by over $450 billion in global investments, depend on ultra-pure chemical delivery systems where AODD pumps’ leak-free and pulsation-dampening performance provides a critical advantage.

Emerging Markets Infrastructure Development and Mining Activities

Rapid industrialization across Southeast Asia, Africa, and Latin America is accelerating investments in water treatment, mining, and manufacturing infrastructure. The Asian Development Bank estimates that the Asia-Pacific will require about US$ 1.7 trillion in annual infrastructure spending through 2030, with significant allocations for industrial and municipal water systems. Mining operations, especially copper, lithium, and rare earth extraction, require durable dewatering and slurry-handling equipment.

Mining equipment expenditure in Australia increased by 12% in 2024, supporting the growing use of AODD pumps for tailings management and reagent dosing, as they can handle abrasive materials without impeller damage. Chile’s copper sector, producing over 5.6 million metric tons annually, represents a strong replacement market as facilities modernize. Graco’s Husky pumps offer high durability for handling mud, water, and abrasive slurries.

Category-wise Analysis

Material Insights

Polypropylene (PP) holds a 40% share of the material segment due to its cost efficiency and strong chemical resistance in non-metallic applications. Its ISO 10993 biocompatibility and FDA approvals further reinforce its suitability for food and beverage processing, while its corrosion-resistant properties make it widely preferred for handling paints, coatings, and other aggressive fluids. Government initiatives, such as China’s Made in China 2025 program and guidance from the U.S. Environmental Protection Agency, promote the use of durable, non-metallic materials in fluid handling systems.

Manufacturers are also increasing investments in PP-based technologies; for example, Unibloc Hygienic Technologies expanded Flotronic® pump production in 2023 to strengthen North American supply. Its affordability and non-reactive nature make PP especially valuable in industries with frequent fluid changeovers or moderate flow requirements.

Flow Rate Insights

The 100-300 LPM segment holds a leading share of 38%, due to its ability to balance efficiency, portability, and performance in mid-scale industrial operations. It is widely used in paints and coatings, supported by engineering data showing reliable handling of viscosities up to 10,000 cP without priming issues. API 674 compliance further strengthens its suitability for oil and gas batching, while case studies from wastewater facilities highlight its dependable performance across variable flow conditions.

The segment is driven by strong adoption in batch chemical manufacturing, paint formulation, and food processing, where moderate throughput and precise volumetric control are essential. Its standardized air-consumption profile also integrates seamlessly with existing compressed-air infrastructure, ensuring sustained replacement demand and stable aftermarket revenue.

Industry Insights

The paints and coatings sector represents the largest end-use segment, accounting for approximately 26% of market share due to AODD pumps’ ability to efficiently handle high-viscosity, shear-sensitive formulations containing pigments, resins, and additives. The global paints and coatings industry, valued at over US$ 180 billion, relies extensively on these pumps for circulation, filtration, and packaging operations where color consistency and the prevention of air entrainment are essential.

The AODD pumps effectively transfer coatings with viscosities ranging from 50 to 50,000 centipoise, covering the majority of industrial formulations. The automotive refinishing segment, which accounts for around 15% of coatings demand, benefits from its ability to manage two-component systems and minimize contamination during color changes. Moreover, growing adoption of low-VOC, water-based coatings, where centrifugal pumps often underperform, continues to strengthen AODD pump usage.

Regional Insights

North America Air-Operated Double Diaphragm (AODD) Pump Market Trends

The United States leads the North American AODD pump market, supported by a large chemical manufacturing base and OSHA regulations that favor leak-free, explosion-proof technologies. The U.S. chemical industry shipped over US$555 billion in products in 2024, and major Gulf Coast facilities rely heavily on AODD pumps. EPA enforcement of Clean Water Act standards is accelerating adoption, with US$ 5.8 billion allocated through State Revolving Funds in 2024 to upgrade more than 14,000 treatment works.

Canada’s mining industry, producing significant potash and copper volumes, contributes to steady demand for slurry-handling pumps. Market leadership is further reinforced by industrial modernization, environmental compliance, and federal programs promoting energy-efficient equipment. The growing adoption of IoT-enabled smart pump technologies continues to strengthen North America’s competitive position.

Europe Air-Operated Double Diaphragm (AODD) Pump Market Trends

Germany leads AODD pump adoption in Europe, supported by its strong chemical and automotive industries, with chemical output reaching €222 billion in 2024 and major companies such as BASF, Bayer, and Evonik operating large-scale facilities. Its Mittelstand manufacturers also rely on these pumps for coatings, adhesives, and pharmaceutical intermediates. The EU’s ATEX Directive favors air-operated pumps in hazardous chemical zones, while France uses specialized models for radioactive fluid handling.

Spain’s rapidly expanding desalination capacity and the UK’s £48 billion pharmaceutical sector further strengthen regional demand. Europe’s food, beverage, and pharmaceutical industries increasingly use PVDF-based pumps for sanitary applications. Strict regulations, including the EU Food Contact Materials Regulation and REACH, along with sustainability initiatives under the EU Green Deal, are driving adoption of energy-efficient, leak-proof ball-valve AODD pumps across major European markets.

Asia Pacific Air-Operated Double Diaphragm (AODD) Pump Market Trends

Asia Pacific is the fastest-growing region in the AODD pump market, driven by rapid industrialization, expanding pharmaceutical production, and increasing infrastructure and water treatment investments in countries such as China, India, and Japan. China accounts for about 45% of the Asia Pacific AODD pump demand, driven by large-scale chemical manufacturing expansion and environmental remediation efforts. Chemical output exceeding ¥14 trillion in 2024 has increased the need for advanced fluid-andling systems, while the 14th Five-Year Plan’s wastewater compliance targets are prompting widespread adoption across more than 300 cities.

India’s role as a major pharmaceutical producer, responsible for 60% of global vaccines, is boosting demand for sanitary, compliant AODD pumps. Japan’s semiconductor sector, supported by projected investments of ¥7 trillion through 2030, relies on ultra-pure pumps for precise chemical delivery. Southeast Asian nations such as Vietnam and Thailand are attracting chemical manufacturing shifts, contributing to regional growth.

Competitive Landscape

The air-operated double diaphragm (AODD) pump market is moderately consolidated, with the top five manufacturers accounting for about 55% of global market share. Leading companies differentiate through advanced material technologies, proprietary air-distribution valve systems, and integrated monitoring solutions. Expansion strategies emphasize emerging markets via local manufacturing partnerships and distributor networks, while acquisitions target specialized pump technologies and regional firms with established customer bases. Key competitive factors include diaphragm durability measured in millions of cycles, improved air-consumption efficiency that lowers operating costs by 15-20%, and strong aftermarket service capabilities. Companies are also adopting equipment-as-a-service models, predictive maintenance supported by IoT sensors, and modular designs that enable rapid material-of-construction changes.

Key Developments:

- January 2025: PSG®, a subsidiary of Dover Corporation, expanded its cryogenic pump capabilities by acquiring Cryogenic Machinery Corp. ("Cryo-Mach"). This strategic move enables PSG to integrate Cryo-Mach’s mission-critical centrifugal pumps and mechanical seals for liquefied gas applications, including oxygen, argon, and nitrogen.

- October 2024: Yamada Corporation introduced its NDP-500BS Series, a 2-inch stainless steel AODD pump achieving a maximum flow rate of 780 L/min. This model improves efficiency by 18% compared to previous designs while maintaining diaphragm longevity. The pump’s fluid flow path redesign reduces air consumption, making it suitable for high-demand industries like chemical processing and wastewater management

- Aug 2023, Wilden, part of PSG and Dover, announced that it has extended its line of small air-operated double-diaphragm (AODD) pumps with the addition of two new 6 mm (1/4") Bolted Plastic Pump models, the Pro-Flo® SHIFT Series PS25 and Accu-Flo™ Series A25PS. Providing the reliability, energy efficiency, and dependability required in challenging fluid-handling activities, the PS25 and A25PS AODD pumps are ideal for dosing and batching applications.

Top Companies in Air-Operated Double Diaphragm (AODD) Pump Market

- PSG Dover Group (Illinois, U.S.) is the global market leader, offering comprehensive AODD pump portfolios under the Wilden, Almatec, and Blackmer brands. The company maintains dominant positions across industrial, pharmaceutical, and food processing segments through continuous innovation in air valve efficiency and diaphragm materials. PSG's extensive global distribution network and aftermarket service infrastructure provide competitive advantages in capturing replacement demand.

- Graco Inc. (Minneapolis, U.S.) leverages its Husky brand's reputation for reliability in harsh chemical environments, commanding premium pricing in paint and coatings applications. The company's vertically integrated manufacturing includes proprietary elastomer formulations and precision machining capabilities, enabling rapid customization for specialized applications.

- IDEX Corporation (Lake Forest, U.S.) operates through its Viking Pump and Warren Rupp divisions, emphasizing engineered solutions for semiconductor, pharmaceutical, and specialty chemical applications. The company's acquisition strategy has expanded capabilities in ultra-pure materials and sanitary designs, positioning it favorably for high-growth electronics manufacturing markets.

Companies Covered in Air-Operated Double Diaphragm (AODD) Pump Market

- PSG Dover Group

- Graco Inc.

- IDEX Corporation

- Tapflo Group

- Verder International Group

- Aro Inc.

- Yamada Corporation

- Ingersoll-Rand PLC

- Warren Rupp, Inc.

- Xylem Inc.

- Flowserve Corporation

- Almatec Maschinenbau GmbH

- Sandpiper Pump

- All-Flo Pump Company

- Price Pump Company

Frequently Asked Questions

The global AODD pump market is projected to reach US$ 3,280.4 Mn by 2033, growing from US$ 2,270.1 Mn in 2026 to a CAGR of 5.4% during the forecast period.

The market is primarily driven by expanding chemical processing and pharmaceutical manufacturing sectors requiring reliable fluid handling equipment, coupled with rising investments in wastewater treatment infrastructure globally to meet stringent environmental regulations.

Polypropylene (PP) material type dominates with approximately 40% market share, favored for its cost-effectiveness, broad chemical compatibility with acids and alkalis, and suitability across general industrial applications, including chemical processing, mining, and wastewater treatment operations.

North America leads the market with 38% share, driven by extensive chemical manufacturing infrastructure worth over US$ 555 billion in annual output, stringent OSHA safety regulations, and an established industrial base supporting consistent replacement demand and comprehensive aftermarket services.

Battery manufacturing expansion for electric vehicle production represents a significant opportunity, requiring specialized AODD pumps for handling aggressive electrode slurries and lithium carbonate electrolytes. The Semiconductor Industry Association reports over $450 billion in announced semiconductor investments requiring ultra-pure chemical delivery systems, where AODD pumps provide critical advantages.

Key market players include PSG Dover Group, Graco Inc., IDEX Corporation, Flowserve Corporation, Xylem Inc., Tapflo Group, Verder International Group, Yamada Corporation, and Ingersoll-Rand PLC, among others, controlling approximately 55-60% combined market share.