- Medical Devices

- Volumetric Pumps Market

Volumetric Pumps Market Size, Share, and Growth Forecast, 2025 - 2032

Volumetric Pumps Market By Pump Type (Reciprocating Pumps, Others), Technology (Traditional Pumps, Smart Pumps, Others), Application (Analgesia, Chemotherapy, Parenteral Nutrition, Blood Product Administration, Others), and Regional Analysis for 2025 - 2032

Volumetric Pumps Market Share and Trends Analysis

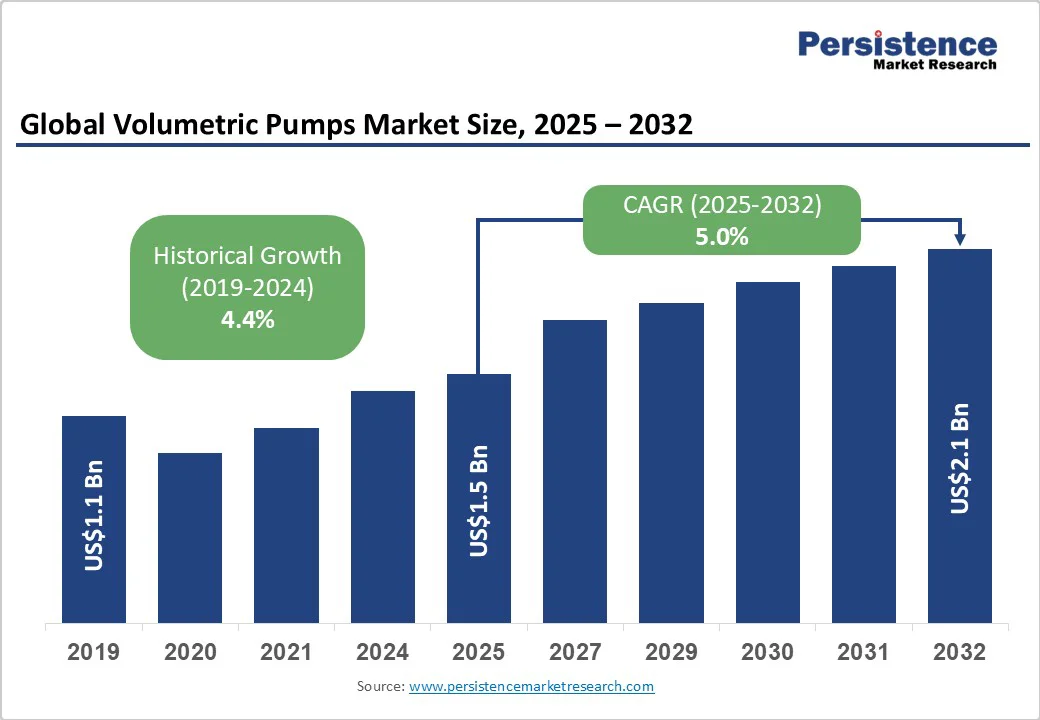

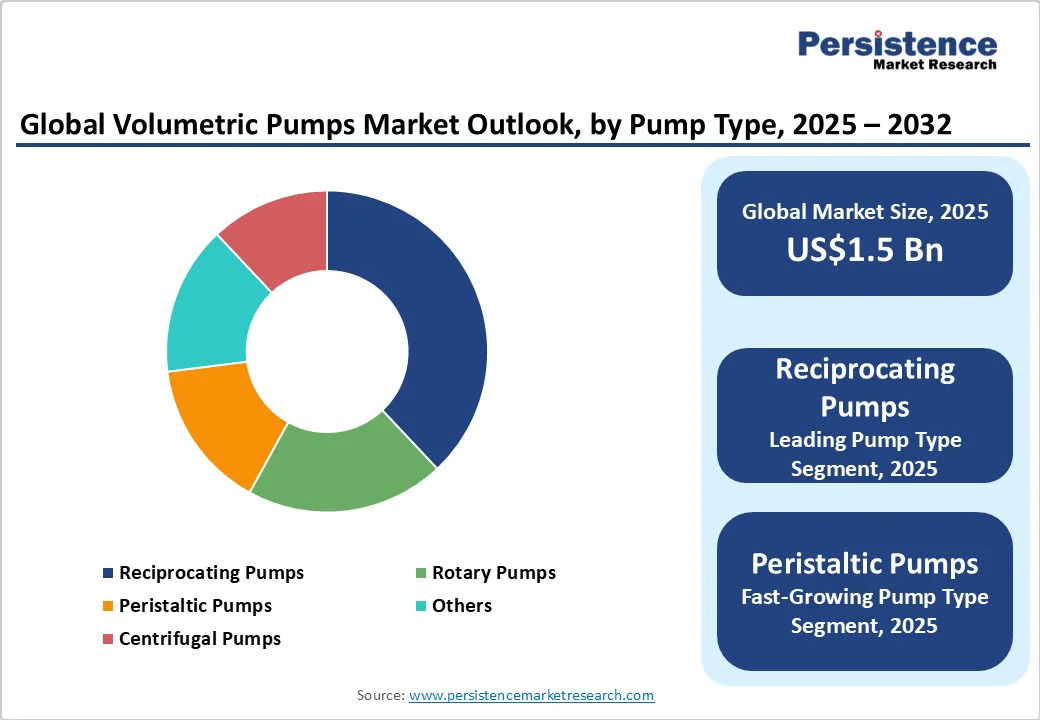

The global volumetric pumps market size is likely to be valued at US$1.5 Bn in 2025. It is estimated to reach US$2.1 Bn by 2032, growing at a CAGR of 5% during the forecast period 2025−2032, due to an increasing preference for outpatient and home-infusion therapies, coupled with escalating investments in smart-pump technologies and IoT-enabled healthcare.

The strong uptake of advanced pumps in emerging economies, driven by expanding healthcare infrastructure and increased budgetary allocations for chronic disease management by governments, is reinforcing overall market momentum. Positive regulatory reforms further catalyze market entry and product innovation.

Key Industry Highlights

- Leading Pump Type: Reciprocating pump types are slated to lead with approximately 38% share in 2025, while peristaltic pumps are likely to grow at the fastest CAGR during 2025-2032.

- Dominant Application: Chemotherapy applications are anticipated to dominate 31% of revenues in 2025, with enteral feeding growing at a 5.8% CAGR through 2032.

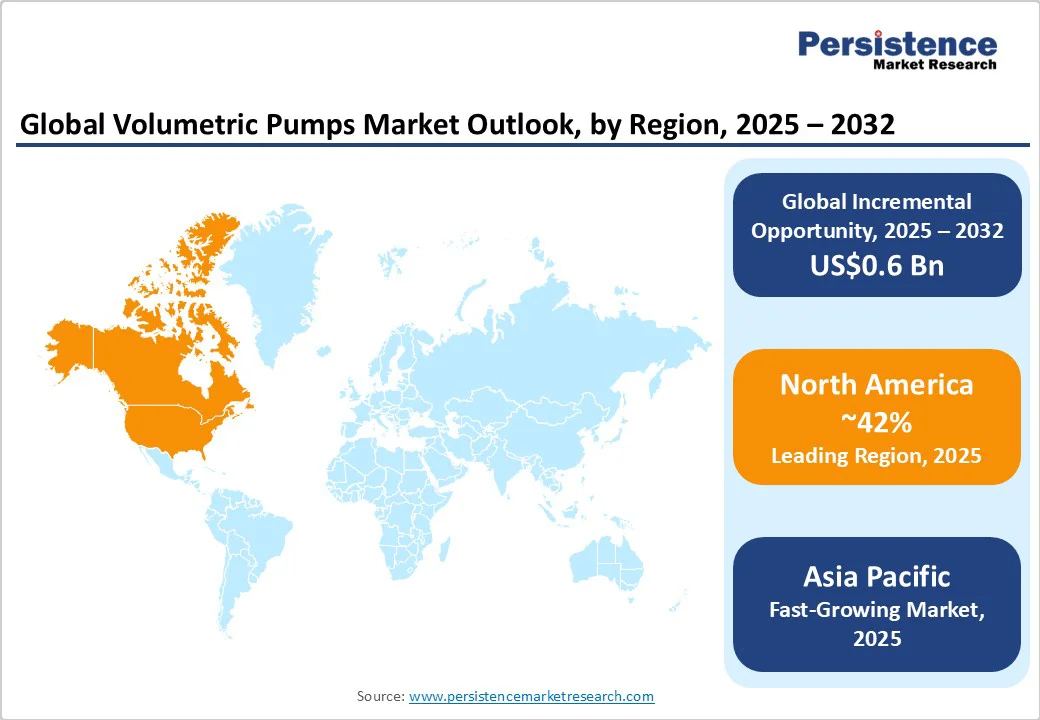

- Leading Region: North America is expected to account for an estimated 42% share in 2025, driven by FDA safety initiatives and the integration of telehealth.

- Fastest-growing Regional Market: Asia Pacific is set to capture 22% of the volumetric pumps market share in 2025, and the regional market is projected to expand at an estimated 6.2% CAGR through 2032, led by China’s Healthy China 2030 and India’s public-private partnership drives in healthcare delivery.

- New Product Launches: Terumo India introduced its TeruFusion Advanced Infusion Systems, featuring enhanced safety protocols such as precise flow-rate control, air-in-line detection, and multi-level occlusion alarms to minimize infusion errors, designed for hospital and critical-care settings.

| Key Insights | Details |

|---|---|

|

Volumetric Pumps Market Size (2025E) |

US$1.5 Bn |

|

Market Value Forecast (2032F) |

US$2.1 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

5% |

|

Historical Market Growth (CAGR 2019 to 2024) |

4.4% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Expansion of Home-Infusion and Ambulatory Care

Several international health bodies, such as the World Health Organization (WHO), have been highlighting the tangible annual rise in home-care infusion utilization, driven by aging populations and cost-containment imperatives. The U.S. Centers for Medicare & Medicaid Services estimates that home infusion therapy reduces hospitalization costs by up to 30%, prompting payers to expand coverage for volumetric pumps in non-acute settings.

Consequently, suppliers are forging partnerships with home-health providers and telehealth platforms to embed dose error-reduction systems and remote monitoring features. This integration is projected to unlock a US$450 Mn incremental opportunity by 2032, with home-care segment growth outpacing hospital bedside use significantly, reflecting shifting care delivery models and patient preference for decentralized treatment.

Proliferation of Smart and Connected Pumps

Industry associations indicate that smart pump adoption is surpassing traditional pump sales, with connected-device shipments growing at a rate of approximately 15% CAGR globally, thereby aiding the growth of the volumetric pumps market. The U.S. FDA’s mandate for dose-error reduction software in infusion devices by 2026 is compelling original equipment manufacturers (OEMs) to accelerate R&D investments in integrated drug libraries, wireless connectivity, and analytics platforms.

These innovations are enabling predictive maintenance services and subscription-based software upgrades, which are expected to create new recurring revenue streams by 2030. Market incumbents and new entrants are thus prioritizing API-enabled ecosystems and cybersecurity certifications to capture the high-growth smart-pump segment.

Barrier Analysis - High Upfront Capital and Maintenance Costs

Volumetric pumps require significant capital expenditure, with average unit pricing ranging from US$3,000 to US$8,000, excluding software licenses. Hospitals and clinics in cost-sensitive regions are delaying upgrades, resulting in an installed base retention rate above 70% for legacy devices that are older than five years. Annual maintenance contracts can amount to 10%–15% of the pump's purchase price, straining operating budgets.

Consequently, price-competitive pressure is intensifying, leading some providers to defer replacement cycles by up to two years, which risks product obsolescence and safety non-compliance. Risk quantification suggests that every year of delay may reduce an OEM’s addressable market.

Regulatory and Compliance Complexity

All medical devices, including volumetric pumps, are subject to stringent regulatory approvals across multiple jurisdictions. Divergent requirements, such as CE marking under the EU MDR, FDA 510(k) clearances, and PMDA registration in Japan, necessitate parallel clinical validation studies, which can inflate the time-to-market by 12–18 months and incur significant additional expenditures per product line in regulatory costs. Post-market surveillance mandates and software update certifications further escalate operating costs. For smaller OEMs and new entrants, these barriers can deter innovation, effectively limiting competition to a handful of established players and constraining product diversity in certain regions.

Opportunity Analysis - Strengthening Healthcare Infrastructure in Burgeoning Markets

The rapid expansion of healthcare infrastructure in the Asia Pacific and Latin America is creating significant opportunities in the market. China and India alone are projected to grow at 6.2% and 7.1% CAGR, respectively, driven by government stimulus and public–private hospital partnerships. Localized manufacturing and low-cost device strategies can unlock price-sensitive segments with addressable patient populations. OEMs can forge distribution alliances and co-develop training programs with regional associations (for example, the Indian Society of Gastroenterology) to navigate market access and accelerate adoption.

Convergence with Digital Therapeutics

The integration of volumetric pumps with digital therapeutic platforms is expected to represent an emerging segment by 2032. Wearable and implantable infusion systems, paired with AI-driven adherence tracking apps, are meeting unmet needs in chronic disease management, such as diabetes and pain therapy.

Reimbursement agencies in Europe and Canada are piloting outcomes-based funding models that reward demonstrable improvements in adherence, incentivizing OEMs to bundle hardware with software-as-a-service. This convergence is fostering multi-stakeholder collaborations among device makers, health IT vendors, and payers to co-create value-based care solutions.

Category-wise Analysis

Pump Type Insights

Reciprocating pumps are expected to account for 38% of the market share in 2025, due to their exceptional precision dosing capabilities and robust service life characteristics that align perfectly with the requirements of a critical-care environment. The fundamental design of reciprocating pumps, utilizing back-and-forth piston motion within a cylinder, enables precise control over fluid displacement, making them ideal for applications requiring exact flow rates and high-pressure delivery. Manufacturing innovations in reciprocating pump design focus on enhancing reliability and reducing maintenance requirements in healthcare settings. Modern piston pumps incorporate advanced sealing technologies, corrosion-resistant materials, and modular component designs that facilitate easy maintenance and extend operational life, thereby lowering the total cost of ownership for healthcare facilities. This results in reduced downtime and consistent performance over extended service periods.

Peristaltic pumps represent the fastest-growing segment with a projected CAGR of 6.1% from 2025 to 2032, fueled by their exceptional suitability for sterile and single-use applications in biopharmaceutical and laboratory workflows. These pumps utilize flexible tubing compression to move fluids, ensuring complete isolation between the fluid and pump mechanism, eliminating contamination risks that are critical in pharmaceutical and biotechnology applications. The sterile transfer capabilities of peristaltic pumps align perfectly with pharmaceutical industry requirements for contamination-free fluid handling. These pumps enable the precise dosing of active pharmaceutical ingredients (APIs), the transfer of sterile solutions, and filling operations without risk of cross-contamination.

Application Insights

Chemotherapy infusion is anticipated to lead with a market share of 31% in 2025, driven by the increasing cancer prevalence worldwide and advancing treatment methodologies. The shift toward outpatient chemotherapy delivery creates demand for portable, precise infusion systems that support patient mobility while maintaining therapeutic accuracy. The diversification of chemotherapy delivery methods supports various pump-type requirements across different treatment protocols. Volumetric pumps maintain dominance in hospital inpatient oncology departments due to their high dosing precision and programmability, particularly for high-risk and multi-drug regimens. Elastomeric pumps are likely to gain traction in outpatient settings due to their compact, battery-free design and suitability for home-based chemotherapy administration.

Enteral feeding is set to emerge as the fastest-growing application with a forecast 5.8% CAGR through 2032, driven by aging populations and shifts toward home-based gastrointestinal therapy. The rising incidence of chronic diseases and demographic aging contribute to the rising demand for enteral nutrition support, with geriatric populations particularly requiring effective feeding solutions to maintain nutritional status. The global enteral feeding devices market exhibits this growth trajectory, with feeding pumps leading the product segment due to their precision in delivering nutrients. Home healthcare trends have accelerated enteral feeding pump adoption as patients increasingly prefer receiving care in comfortable home environments. Smart enteral feeding pumps incorporate wireless connectivity, integrated alarms, and real-time monitoring capabilities, enabling healthcare providers to remotely oversee patient care.

Technology Insights

Traditional pumps are predicted to retain a 60% market share in 2025, driven by lower initial capital costs, operational familiarity among healthcare staff, and adequate performance for routine applications that do not require advanced connectivity features. Healthcare organizations with limited IT infrastructure or budget constraints continue to rely on traditional pumps for basic infusion needs while gradually transitioning to smarter technologies. These pumps offer straightforward operation with mechanical controls, eliminating concerns about software compatibility, cybersecurity risks, or complex programming requirements.

Wireless-enabled devices project the fastest growth at approximately 9.5% CAGR from 2025 to 2032, owing to the digitization of hospitals across several countries and interoperability mandates under HL7 and FHIR standards. Wireless connectivity enables smart pumps to connect to hospital networks, facilitating real-time data transmission, remote monitoring capabilities, and integration with clinical workflow systems. The technological advancement supports hundreds of pumps connecting to single servers within health systems, enabling centralized software updates and comprehensive data analytics. Wireless-enabled infusion pumps contribute to these ecosystems by providing continuous infusion data, supporting automated documentation, and enabling clinical decision support systems. The connectivity capabilities facilitate compliance with regulatory requirements for medical device integration and support quality reporting initiatives that demonstrate improvements in patient safety.

Regional Market Insights

North America Volumetric Pumps Market Trends

North America is poised for an estimated 42% share of the volumetric pumps market in 2025, with the U.S. contributing over 35% of regional market value. This market dominance reflects the region's advanced healthcare infrastructure, comprehensive regulatory framework, and substantial investment in medical device innovation. The mature healthcare system in North America supports widespread adoption of sophisticated infusion technologies across diverse clinical settings, from large academic medical centers to specialized outpatient facilities.

The regulatory environment significantly influences market development through FDA safety initiatives and guidance documents that establish performance standards for infusion pump manufacturers. The FDA's Infusion Pump Improvement Initiative, launched in 2010, implemented comprehensive requirements including detailed engineering information in premarket submissions, safety assurance cases, and enhanced design validation testing. These regulatory standards create market barriers for entry while ensuring high-quality, safe devices reach healthcare providers.

Europe Volumetric Pumps Market Trends

Europe is anticipated to account for approximately 28% in 2025, with Germany, the U.K., and France leading regional development. The European Union (EU)'s Medical Device Regulation (MDR) creates comprehensive regulatory harmonization that facilitates cross-border device approvals while establishing stringent safety and performance standards. This regulatory framework simplifies market entry for qualified manufacturers while ensuring high-quality devices reach European healthcare systems. The transition from Medical Devices Directive (MDD) to MDR requirements creates both opportunities and challenges for volumetric pump manufacturers. Enhanced technical documentation requirements, clinical evaluation standards, and post-market surveillance obligations increase regulatory compliance costs while ensuring improved device safety and performance. The regulation requires CE marking validation, EUDAMED registration, and comprehensive quality management systems that demonstrate ongoing compliance with European safety standards.

Asia Pacific Volumetric Pumps Market Trends

Asia Pacific is expected to secure an estimated 22% share of the global volumetric pumps market in 2025, with China, Japan, and India driving regional growth. The region demonstrates exceptional growth potential with a projected 6.2% CAGR through 2032, reflecting rapid hospital expansion, medical tourism development, and healthcare infrastructure modernization across ASEAN countries. This growth trajectory positions Asia Pacific as the fastest-growing regional market for volumetric infusion pumps globally. China's healthcare development initiatives under Healthy China 2030 have opened up substantial market opportunities for advanced medical device adoption.

The government's strategic focus on smart healthcare systems and smart hospital development drives demand for digital infusion pumps that integrate with hospital IT infrastructure. At the same time, India's public-private partnership model for healthcare service delivery creates opportunities for infusion pump manufacturers to participate in large-scale healthcare infrastructure development projects. The government's focus on essential healthcare services accessibility drives demand for cost-effective, reliable infusion solutions that serve diverse patient populations. These policy initiatives support market expansion while encouraging technology transfer and local capability development.

Competitive Landscape

The global volumetric pumps market landscape is moderately consolidated, with the top five players commanding approximately 55% share. Leading OEMs, which include B. Braun Melsungen, Baxter International, Fresenius Kabi, ICU Medical, and Medtronic, are leveraging broad product portfolios and global service networks.

Mid-tier and regional players account for the fragmented remainder, focusing on niche applications and cost-competitive offerings. Barriers to entry remain high due to regulatory complexity and the installed base replacement cycles, which sustain incumbents’ market influence.

Key Industry Developments

- In May 2025, Medtronic announced plans to spin off its diabetes unit into a standalone public company within 18 months. The division, generating US$2.76 Bn in FY2025 with 10.7% YoY growth, will be led by Que Dallara and aims to compete with Abbott, Dexcom, Insulet, and Tandem through integrated insulin pump and CGM offerings.

- In March 2025, Sequel announced the integration of its Twiist hybrid closed-loop insulin system with Abbott’s FreeStyle Libre 3 Plus CGM. Launching in the U.S. in Q2 2025, Twiist offers real-time glucose-based insulin adjustments, advanced iiSure™ safety features, and is approved for users aged six and up. It includes a free trial month and pricing up to US$50/month with no long-term commitment.

Companies Covered in Volumetric Pumps Market

- B. Braun Melsungen AG

- Baxter International Inc.

- Fresenius Kabi AG

- ICU Medical Inc.

- Medtronic plc

- Smiths Group plc

- Terumo Corporation

- Becton, Dickinson and Company

- CareFusion

- Moog Inc.

- Nipro Corporation

- Chongqing Joycome Medical

- Weigao Group

Frequently Asked Questions

The volumetric pumps market is projected to reach US$1.5 Bn in 2025.

Increasing preference for outpatient and home-infusion therapies and expanding governmental budgets for managing chronic conditions are driving the market.

The volumetric pumps market is poised to witness a CAGR of 5% from 2025 to 2032.

Growing investments in smart-pump technologies and IoT-enabled healthcare and improving healthcare infrastructure in developing economies represent key market opportunities.

B. Braun Melsungen AG, Baxter International Inc., and Fresenius Kabi AG are some of the key players in the volumetric pumps market.