- Advanced Materials

- Veneer Sheets Market

Veneer Sheets Market Size, Share, and Growth Forecast, 2025 - 2032

Veneer Sheets Market by Product Type (Natural Veneer Sheets, Reconstituted (Engineered) Veneer Sheets, Paper-Backed Veneer Sheets, Phenolic-Backed Veneer Sheets, Wood-on-Wood Veneer Sheets, Others), Wood Species (Oak, Maple, Cherry, Others), Application (Furniture and Cabinetry, Wall Paneling and Ceilings, Doors and Partitions, Flooring, Architectural Millwork, Others), and Regional Analysis for 2025 - 2032

Veneer Sheets Market Share and Trends Analysis

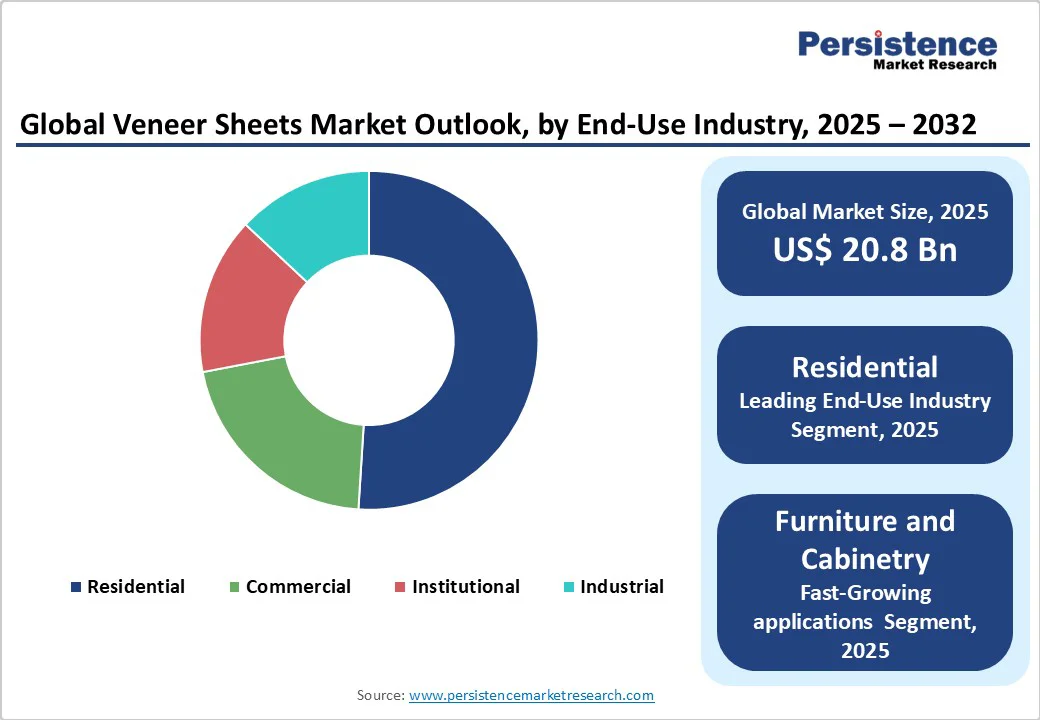

The global veneer sheets market size is likely to be valued at US$ 20.8 billion in 2025, and is projected to reach US$ 31.9 billion by 2032, growing at a CAGR of 6.3% during the forecast period 2025 - 2032.

Strong demand for sustainable and aesthetically appealing interior finishes is driving market expansion, supported by rising residential and commercial construction activities worldwide. Additionally, innovations in engineered veneer technologies are enhancing performance characteristics and broadening application scopes across furniture, millwork, and architectural sectors.

Key Industry Highlights

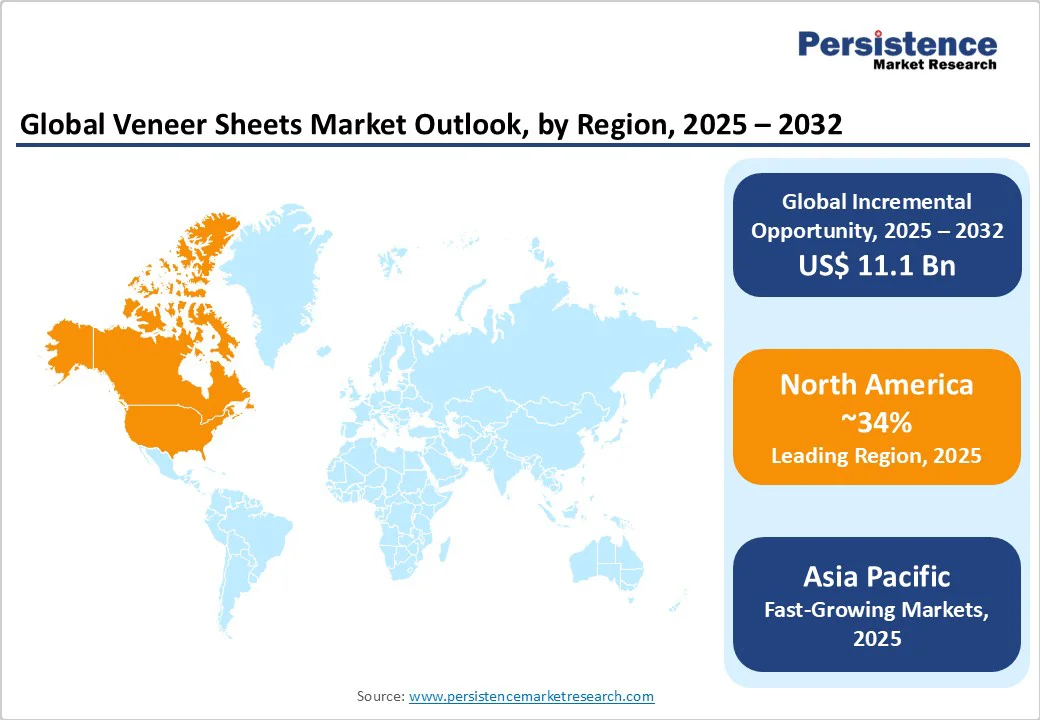

- Leading region: North America is set to dominate in 2025 due to stringent sustainability regulations and well-established distribution networks fostering high veneer adoption.

- Fastest Growing Regional Market: Asia Pacific is poised for the highest CAGR through 2032, with rapid urbanization and expanding real estate development driving engineered veneer demand.

- Dominant Segment: Furniture and cabinetry is the largest application, accounting for over 40% of market share in 2025, driven by remodeling and replacement cycles.

- Fastest Growing Segment: Reconstituted (Engineered) Veneer Sheets are expanding at over 8% annually, propelled by technological advancements and cost efficiencies.

- Key Market Opportunity: Digital printing on veneer substrates for customized patterns and textures offers high-margin prospects in luxury and boutique interiors.

| Key Insights | Details |

|---|---|

| Veneer Sheets Market Size (2025E) | US$ 20.8 Bn |

| Market Value Forecast (2032F) | US$ 31.9 Bn |

| Projected Growth CAGR (2025 - 2032) | 6.3% |

| Historical Market Growth (2019-2024) | 5.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Demand for Sustainable Building Materials

The demand for sustainable building materials is on the rise as consumers and architects show a growing preference for eco-friendly options. This shift is leading to an increased adoption of natural veneer sheets made from responsibly sourced timber. Government regulations aimed at promoting sustainable construction practices, particularly in Europe and North America, are further driving this demand.

This trend is supported by recognized green building certification systems such as LEED and BREEAM, which advocate for the use of wood-based finishes, highlighting the veneer sheets market as a significant beneficiary of the movement towards sustainable design.

Recent advancements in reconstituted and paper-backed veneer sheets have led to substantial enhancements in both dimensional stability and surface durability. As a result, engineered veneers have become a more cost-effective alternative to traditional solid wood panels.

This surge can be attributed to the dual benefits of reduced material waste and heightened design flexibility, which together allow for more sustainable and innovative production methods. These technological enhancements not only improve the performance of engineered veneers but also facilitate large-format applications in wall paneling and cabinetry. This expansion of usability significantly broadens the addressable market for manufacturers.

Volatility in Raw Material Price

Fluctuations in timber and resin prices create substantial challenges for veneer producers. Between 2021 and 2023, the global market for softwood lumber experienced dramatic spikes due to factors such as supply chain disruptions, increased demand, and changes in trade policies.

This surge significantly impacted profit margins for manufacturers, leading many to pass these increased costs onto end consumers. Such pricing volatility can deter investment in premium veneer products, particularly in price-sensitive markets where consumers are hesitant to pay higher prices for luxury finishes.

Sustainability standards significantly contribute to the promotion and adoption of eco-friendly veneers in the wood products industry. However, these standards also introduce considerable compliance challenges that manufacturers must navigate.

In recent years, regulations addressing formaldehyde emissions and the use of harmful chemical treatments have become increasingly stringent, particularly within the United States and European Union (EU). These regulations not only necessitat

dergo extensive and often costly certification and testing processes to validate their products’ compliance.

Expansion in Urbanizing Markets

The rapid urbanization coupled with increasing disposable incomes in Asia Pacific and Latin America is generating significant opportunities for various sectors. In particular, India and Indonesia are experiencing an impressive 15% annual growth rate in residential construction, a trend that is driving up the demand for cost-effective decorative veneers.

These veneers are not only essential for aesthetic appeal but also for creating functional and modern living spaces to accommodate the growing urban population. To fully capitalize on this trend, companies should consider establishing local production facilities. Doing so would not only help them mitigate import duties and reduce logistics costs but also allow them to respond more quickly to market demands.

Digital printing on veneer substrates has emerged as a transformative technique in the interior décor market, enabling the creation of bespoke patterns and textures that align with the growing consumer demand for personalized designs. Recent advancements in high-resolution printing technology have led to the establishment of printing lines capable of producing runs of under 100 square meters with minimal setup time.

This flexibility is particularly beneficial for boutique furniture makers and luxury millwork studios, allowing them to create unique pieces tailored to individual customer preferences. This opens up high-margin niche markets but also enhances brand differentiation for manufacturers who embrace these technological innovations.

Category-wise Analysis

Product Type Insights

Natural veneer sheets are expected to lead with approximately 37% market share in 2025, owing to their authentic wood aesthetics and strong consumer preference for organic textures. The increase in the consumption of natural veneer is backed by their widening demand in high-end residential and hospitality projects.

The enduring appeal of genuine wood grain, coupled with certifications from FSC and PEFC, underpins this segment's leadership. Reconstituted veneer, while growing rapidly, remains secondary due to perception of inferior quality despite enhanced durability.

Wood Species Insights

Oak veneer sheets are projected to hold the largest market share of around 29% in 2025, primarily due to the highly prized grain patterns, hardness, and broad adaptability of oak across furniture and flooring applications. These qualities make oak veneer a preferred choice for manufacturers and consumers seeking durable yet visually appealing wood surfaces.

The supply chains for oak are firmly established in key markets such as Europe and North America, ensuring stable availability and competitive pricing, which further bolsters its market position. This growth trend is supported by a rising demand for sustainable and premium wood finishes in residential and commercial interiors, as furniture makers and designers emphasize quality, ecological responsibility, and aesthetic versatility.

In sum, the oak veneer segment continues to benefit from a combination of natural wood appeal, supply chain maturity, and expanding application in various consumer and architectural products.

Application Insights

Furniture and cabinetry are projected to dominate the veneer sheets market with an estimated 42% share in 2025, driven by remodeling trends and replacement cycles prevalent in mature markets. The segment benefits significantly from public-sector contracts focused on refurbishing schools and office facilities, which has increased the use of veneers in custom casegoods production.

With the rise of modular furniture, veneer finishes have become especially valuable, offering a premium aesthetic appeal at a lower cost compared to solid wood alternatives, making them attractive to both manufacturers and consumers. Moreover, advancements in manufacturing technologies such as paper-backed veneers have enhanced the versatility and cost-effectiveness of veneer sheets, further solidifying their leading position in furniture and cabinetry applications.

Regional Insights

North America Veneer Sheets Market Trends

North America is forecasted to dominate the veneer sheets market share in 2025, led by the U.S., with innovative veneers being increasingly integrated into sustainable housing projects and hospitality refurbishments. Regulatory frameworks such as California’s CARB emissions limits have accelerated adoption of formaldehyde-free adhesives in veneer production.

Meanwhile, Canada’s lumber export policies affecting raw material supply have prompted regional veneer mills to diversify into engineered sheets for stable margins. In Canada and Mexico, renovation markets are stimulated by aging housing stock, increasing demand for mid-range veneer products.

Strategic partnerships between U.S. veneer exporters and Mexican millworkers have streamlined cross-border supply chains, fostering competitive pricing and rapid delivery for construction projects.

Europe Veneer Sheets Market Trends

Europe is offering a variety of lucrative opportunities, with Germany leading in veneer consumption and premium oak and maple veneers being specified in automotive interiors and luxury retail fits. French regulations on volatile organic compound (VOC) emissions have driven innovation in waterborne adhesives for veneer lamination.

The U.K. market sees steady growth in paper-backed veneer panels for modular offices, driven by office space reconfiguration trends post-pandemic. Regulatory harmonization under the EU Timber Regulation (EUTR) has also ensured traceability, favoring certified veneer sources and boosting market transparency. At the same time, Spain’s decorative millwork sector has reported a 6% increase in veneer exports to North Africa, capitalizing on proximity and free-trade agreements.

Asia Pacific Veneer Sheets Market Trends

Asia Pacific is expected to be the fastest-growing regional market from 2025 to 2032. China maintains the largest volume demand in the region, fueled by mass housing and commercial construction. Domestic mills are expanding production of phenolic-backed veneer sheets to meet plywood industry requirements. Demand trends in Japan is skewed toward premium cherry and maple veneers for high-end furniture, with annual import growth of 8%.

On the other hand, India’s booming real estate sector is driving engineered veneer adoption, as local manufacturers invest in UNIPOL-like processes to produce consistent-quality products. ASEAN countries, particularly Indonesia and Malaysia, are emerging as veneer exporters, leveraging abundant timber resources and lower production costs to challenge established suppliers.

Competitive Landscape

The global veneer sheets market structure is moderately consolidated, with leading players such as GREENLAM INDUSTRIES LTD., BASF SE, and Carlisle Companies Inc. collectively holding a combined share of around 32%. These companies leverage extensive distribution networks, innovative product portfolios, and strategic acquisitions to deepen market penetration.

In contrast, regional mills are competing on cost and customization, investing in digital printing technologies and formaldehyde-free adhesives. Emerging business models include direct-to-designer e-commerce platforms and on-demand veneer trimming services, enhancing responsiveness to boutique project requirements.

Key Market Developments

- In September 2025, Oakwood Veneer Company increased the availability of its large-format veneer sheets, responding to growing demand from furniture and architectural markets. The expansion allows for greater design flexibility with fewer seams in panels, meeting the needs of high-end projects. Oakwood’s enhanced production capabilities ensure timely delivery and consistent quality for large custom veneer applications. This move supports manufacturers and designers seeking premium, seamless wood surfaces for sophisticated interiors.

- In September 2025, Foster + Partners Industrial Design and Isokon unveiled the 'Join' collection at the London Design Festival, featuring a lounge chair, footstool, and tables crafted using advanced plywood and veneer layering techniques. The collection highlights innovative design achieved through hands-on prototyping, with pieces inspired by folding methods that transform flat veneered timber sheets into ergonomic, three-dimensional forms. Available in birch, walnut, oak, and stained finishes, the collection offers functional, minimalist aesthetics suitable for both residential and commercial environments.

- In April 2025, F/List introduced a new heat-release-compliant wood veneer designed specifically for premium aircraft cabin interiors, debuting at Aircraft Interiors Expo (AIX) 2025. This innovative veneer meets stringent fire safety standards while maintaining the natural beauty and elegance of wood, allowing aircraft designers to create luxurious yet compliant cabin environments. The product caters to the growing demand for high-quality, lightweight, and fire-safe materials in business and commercial aviation interiors. F/List’s advancement represents a blend of craftsmanship and safety technology, enhancing both aesthetics and regulatory compliance in aircraft design.

Companies Covered in Veneer Sheets Market

- Carlisle Companies Inc.

- GCP Applied Technologies

- Kingspan Group

- BASF SE

- Soprema Group

- Owens Corning

- W. R. Meadows, Inc.

- Knauf Insulation

- Firestone Building Products

- Henry Company

- GREENLAM INDUSTRIES LTD.

- Sauers & Company Veneers

- Oakwood Veneer

- Veneer Technologies

- FormWood Industries, Inc.

Frequently Asked Questions

The global veneer sheets market is projected to reach US$ 20.8 billion in 2025.

Key drivers include the rising demand for sustainable building materials, government green building regulations, and technological advances in engineered veneers boosting performance.

The market is poised to witness a CAGR of 6.3% from 2025 to 2032.

Digital printing technologies on veneer substrates enabling customized, high-margin designs for luxury and niche interiors present highly lucrative opportunities in the market.

Leading market players include GREENLAM INDUSTRIES LTD., BASF SE, and Carlisle Companies Inc.