- Pharmaceuticals

- Vaginitis Treatment Drug Market

Vaginitis Treatment Drug Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Vaginitis Treatment Drug Market by Drug Class (Antibiotics, Antifungals, Antiprotozoals, Others), Indication (Bacterial Vaginitis, Yeast Infections (Candidiasis), Trichomoniasis, Others), Route of Administration (Oral, Topical, Intravaginal), Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies, Others), and Regional Analysis from 2026 to 2033

Vaginitis Treatment Drug Market Share and Trends Analysis

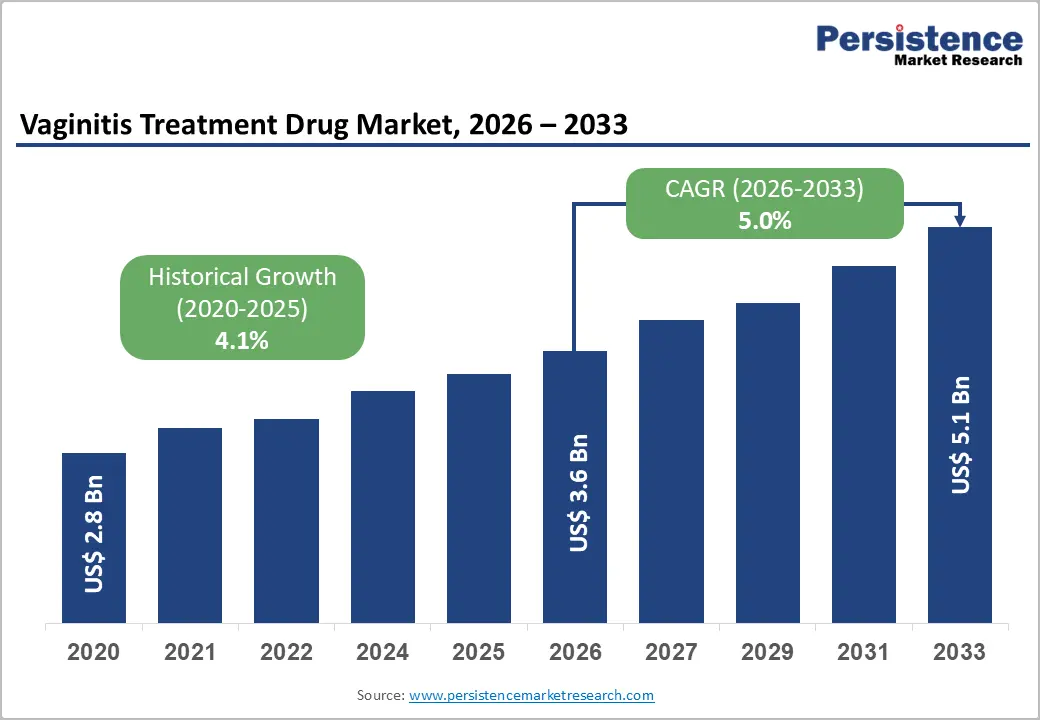

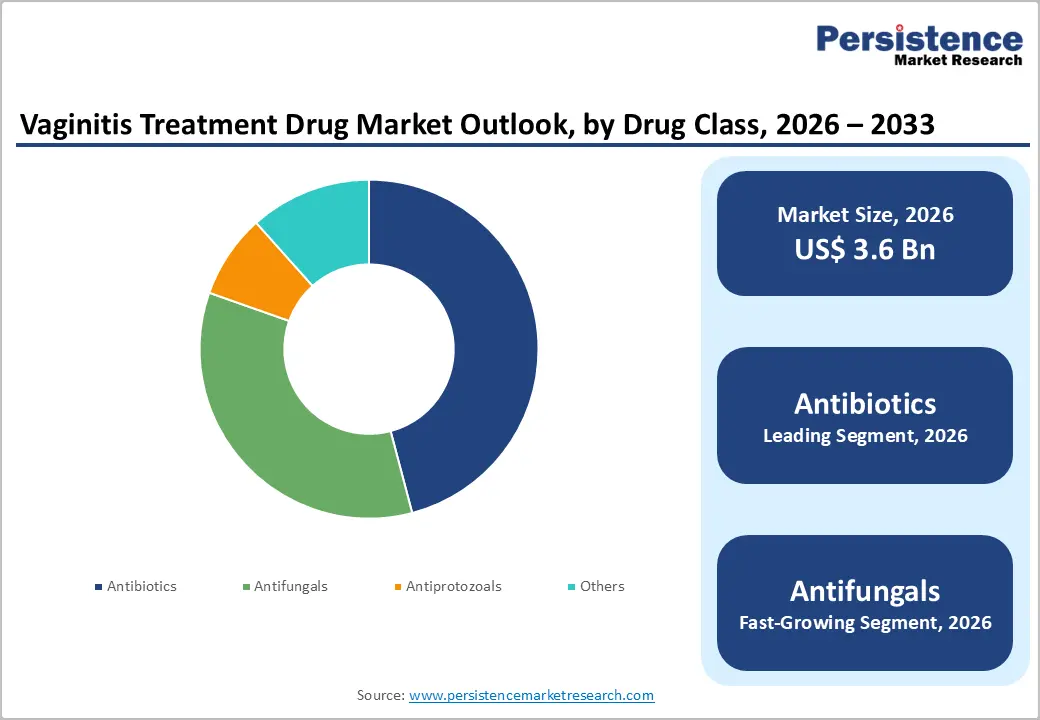

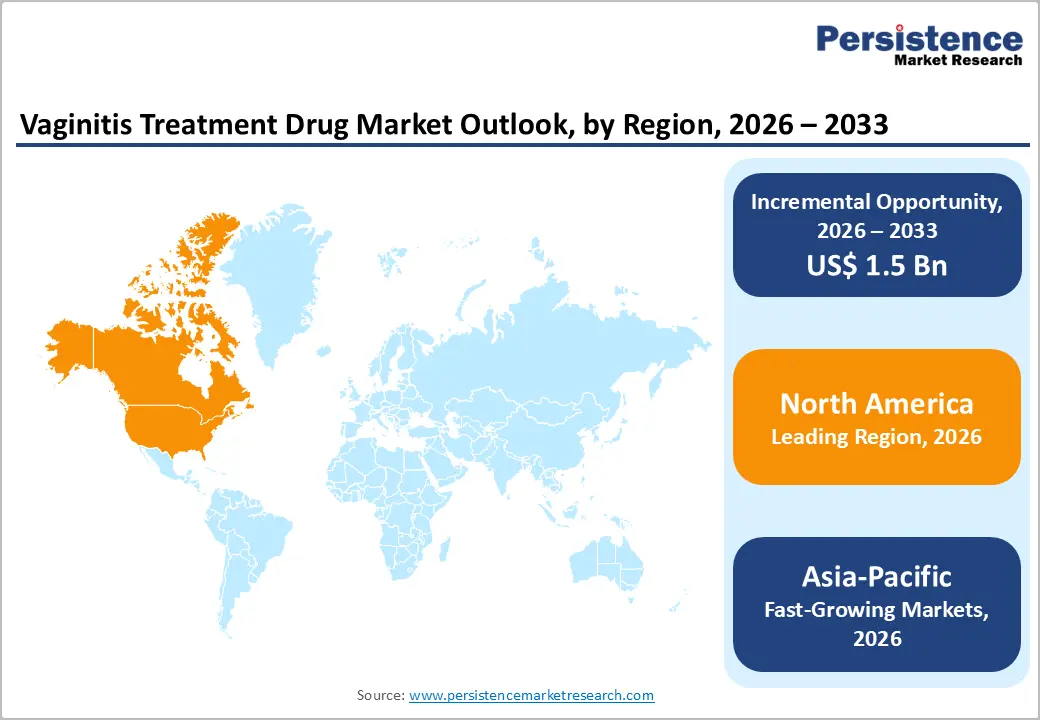

The global vaginitis treatment drug market is estimated at US$3.6 billion in 2026 and is projected to reach US$5.1 billion by 2033, with a 5.0% CAGR over the forecast period.

The global market for vaginitis treatments is steadily growing, driven by rising demand for targeted therapies, the adoption of digital healthcare, and technological advances in drug development. North America dominates owing to robust infrastructure, stringent regulations, and robust manufacturing. The Asia-Pacific region is the fastest-growing, supported by expanding healthcare facilities, government initiatives, rising patient awareness, and investment in diagnostics and manufacturing.

Key Industry Highlights:

- Dominant Segment: Antibiotics hold a significant share of the market, capturing 45.9% in 2025. They are primarily used to treat bacterial vaginosis, offering high effectiveness against pathogenic bacteria. Prescription-based formulations enable targeted management, reduce recurrence, and support combination therapies, making them essential in treating bacterial causes of vaginitis.

- Dominant Region: North America leads with around 39.9% share in 2025, supported by advanced healthcare infrastructure, high treatment awareness, and strong regulatory frameworks. The Asia-Pacific region is the fastest-growing, driven by expanding healthcare access, government initiatives, rising patient awareness, and increased investment in diagnostic and treatment capacity.

- Growth Indicator: The increasing prevalence of bacterial and fungal vaginitis, rising demand for targeted and effective therapies, increasing OTC adoption, and advances in drug delivery and diagnostics are driving market growth.

- Market Opportunity: Opportunities exist in next-generation antifungal formulations, combination therapies, personalized treatment approaches, scalable OTC distribution, and expansion into emerging regions with growing women’s health awareness.

| Key Insights | Details |

|---|---|

| Vaginitis Treatment Drug Market Size (2026E) | US$ 3.6 Bn |

| Market Value Forecast (2033F) | US$ 5.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.0% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.1% |

Market Dynamics

Driver: Increasing Demand for Targeted and Effective Therapies

The global burden of bacterial vaginosis (BV), the most common cause of vaginitis, underscores the demand for targeted therapies. According to the World Health Organization (WHO), BV prevalence among women of reproductive age ranges from 23% to 29% globally, indicating a widespread need for effective treatment options that address this microbial imbalance. Similarly, National Health and Nutrition Examination Survey (NHANES) data show that nearly 29% of U.S. women aged 14-49 have symptomatic or asymptomatic BV, reinforcing the large population requiring clinical intervention. Concurrently, yeast infections affect an estimated 20-25% of women at least once in their lifetime, a major driver for antifungal treatments. These high prevalence rates are translating into increased physician visits, prescriptions, and screening, creating robust demand for therapies that are both targeted against specific pathogens and capable of reducing recurrence.

Technological and clinical advances, including improved diagnostics that differentiate bacterial versus fungal vaginitis, enhance therapeutic precision. The increased adoption of pH measurement, Gram stain microscopy, and molecular testing enables clinicians to tailor interventions, thereby improving outcomes and justifying increased utilization of targeted antibiotics and antifungals. Moreover, rising awareness among women about reproductive health leads to earlier diagnosis and treatment, expanding the patient pool seeking clinically effective therapies rather than empirical self-care alone.

Restraints: High Cost of Prescription Medications in Certain Regions

High prescription drug costs represent a key restraint for the vaginitis treatment drug market, particularly in high-income regions with advanced healthcare infrastructure. In the United States, commercial insurance data indicate that total all-cause healthcare costs for women treated for bacterial vaginosis average nearly $8,987 per patient per year, with BV-related expenses increasing with treatment complexity. These costs include not only medication costs but also multiple outpatient visits and follow-ups, effectively raising the financial barrier for some patients. Prescription antibacterials and antifungals, while clinically effective, often carry higher copayments than over-the-counter options, potentially reducing access for underinsured patients.

In emerging markets, out-of-pocket spending can be proportionally high due to limited insurance penetration and price variability. Healthcare access disparities, where diagnostic capability is lower often result in patients delaying formal clinical care and resorting to ineffective or inappropriate therapies (‘home remedies’), which can worsen disease progression and demand more expensive prescription drugs later. Government guidelines on antimicrobial use also highlight that inappropriate antibiotic use contributes to antimicrobial resistance, necessitating newer, often more costly empiric regimens.

These financial barriers can slow uptake of effective prescriptions and delay appropriate therapy, particularly among segments of the population with limited insurance coverage or in regions with weak drug pricing regulation.

Opportunity: Development of Next-Generation Antifungal and Antibiotic Formulations

The increasing global prevalence of chronic and recurrent vaginitis creates substantial opportunities for next-generation drug development. Traditional therapies for bacterial vaginosis and yeast infections have demonstrated high recurrence rates up to 50-80% within a year after standard antibiotic treatment, signaling an unmet clinical need. This recurrence often stems from biofilm-associated bacterial persistence and incomplete restoration of healthy vaginal microbiota, driving demand for more effective or sustained-release formulations, biofilm-disrupting therapies, and microbiome-modulating agents.

Government-supported initiatives targeting antimicrobial resistance and new drug discovery, such as the CDC’s Antimicrobial Resistance Investment Map, which shows investments in innovative research projects, indirectly support broader antibacterial innovation, including next-generation vaginitis agents. Additionally, programs like CARB-X and other public-private partnerships are accelerating the early-stage development of novel antibacterial products, creating a healthier pipeline of differentiated agents that could translate into improved treatment for resistant or recurrent infections.

There is also growing interest in alternative therapeutic modalities (e.g., probiotics, live biotherapeutic products, microbiome transplants) aimed at restoring normal vaginal flora rather than merely suppressing pathogens. Clinical and academic research increasingly supports such approaches as adjuncts or substitutes for conventional drugs, presenting new commercial avenues. Overall, expanding next-generation antibiotic and antifungal formulations represents a strong market opportunity, aligning clinical need with technological innovation and public health priority.

Category-wise Analysis

By Drug Type Insights

Antibiotics occupies 45.9% share of the global market in 2025, because bacterial vaginosis (BV), a condition caused by bacterial imbalance is the most common form of vaginitis and requires antibacterial therapy for effective treatment. Epidemiological data show BV accounts for approximately 40%-50% of all vaginitis cases, making it the leading indication by volume of prescriptions. In the United States alone, BV affects an estimated 29% of women aged 14-49 years (about 21 million women), demonstrating its high burden. BV is primarily treated with antibiotics such as metronidazole and clindamycin, recommended by health authorities such as the WHO and standard treatment guidelines for restoring healthy vaginal flora. The consistent reliance on these antibiotics for BV management accounts for their dominant share of the vaginitis drug market.

By Indication Insights

Bacterial vaginitis (bacterial vaginosis) dominates the vaginitis treatment market because it is the most prevalent cause of vaginal infection compared with other etiologies, such as yeast or protozoal infections. Clinical data indicate that BV accounts for about 40%-50% of vaginitis cases, with vulvovaginal candidiasis (yeast) representing only 20%-25% and trichomoniasis substantially less, underscoring BV’s relative frequency. Globally, systematic reviews estimate BV prevalence among women of reproductive age ranges from 23% to 29%, reflecting its substantial public health impact. Because many women with vaginal symptoms are ultimately diagnosed with BV, clinical demand for targeted antibiotic treatment is higher than for antifungals or antiprotozoals. Consequently, bacterial vaginitis drives the largest share of treatment utilization and market value.

Regional Insights

North America Vaginitis Treatment Drug Market Trends

North America dominates the vaginitis treatment drug market with 39.9% share in 2025, due to advanced healthcare infrastructure, widespread disease awareness, and strong access to both prescription and over-the-counter therapies. U.S. public health data indicate that roughly 29% of women aged 14-49 experience bacterial vaginosis one of the most common forms of vaginitis underscoring high treatment demand. The region benefits from well-established gynecological services, extensive insurance coverage, and robust clinician networks that facilitate early diagnosis and treatment. Moreover, women’s healthcare spending in North America estimated at ~38-40% of the global women’s health market reflects higher per-capita healthcare utilization and technology adoption, which supports broad uptake of therapeutics. These factors collectively reinforce North America’s dominant share in the global vaginitis drug market.

Europe Vaginitis Treatment Drug Market Trends

Europe is a key region in the vaginitis treatment drug market due to its comprehensive healthcare systems, universal health coverage, and strong regulatory frameworks that ensure access to high-quality treatments. Across EU member states, bacterial vaginosis prevalence varies widely but remains clinically significant, contributing to sustained therapeutic demand. Countries such as Germany, the United Kingdom, and France provide widespread gynecological care through national health services, enabling early diagnosis and standardized treatment protocols. Additionally, European health authorities emphasize antimicrobial stewardship and women’s health initiatives, which promote appropriate use of antibiotics and antifungals while fostering professional education on vaginitis management. The region’s strong pharmaceutical manufacturing base also supports availability of effective drug options, making Europe a significant contributor to global market dynamics.

Asia-Pacific Vaginitis Treatment Drug Market Trends

The Asia-Pacific region is expected to experience the fastest growth, driven by expanding healthcare infrastructure, rising awareness of women’s health issues, and large patient populations in countries such as China and India. Government programs aimed at improving access to reproductive and gynecological care are increasing the diagnosis and treatment of vaginitis, while urbanization and growing disposable incomes enable more women to seek medical care. Public health data also show that BV prevalence in parts of Asia is comparable to or higher than in other regions, contributing to substantive unmet treatment needs. Additionally, the expansion of pharmaceutical production and distribution networks, alongside the rising adoption of OTC products and telehealth services, is facilitating broader market penetration. These combined forces position the Asia Pacific for rapid market growth.

Competitive Landscape

The vaginitis treatment drug market is competitive, with key players including Roche, AbbVie, Amgen, and Johnson & Johnson. Companies focus on innovation, diverse pipelines, and advanced formulations. Market positioning is driven by strategic collaborations, product launches, and global expansion, while sustained R&D investment and regulatory approvals shape long-term leadership in vaginitis therapeutics.

Key Industry Developments:

- In September 2025, Novartis received FDA approval for Rhapsido® (remibrutinib), marking it as the first oral, targeted BTK inhibitor for treating chronic spontaneous urticaria (CSU). The approval enables patients with CSU to access a novel oral therapy option, offering targeted treatment of underlying immune pathways. This milestone highlights Novartis’ continued innovation in immunology and dermatology therapeutics.

- In January 2025, Bayer UK launched the CanesMeno® educational hub and associated product range, aiming to enhance menopause support for women. The initiative provides information, guidance, and practical solutions to manage menopause symptoms, while introducing new products designed to improve well-being. This move reflects Bayer’s commitment to women’s health and education in the menopause care space.

Companies Covered in Vaginitis Treatment Drug Market

- Pfizer Inc.

- Viatris Inc.

- Novartis AS

- Bayer AG

- Sanofi S.A.

- Lupin Pharmaceuticals, Inc.

- Dr. Reddy's Laboratories Ltd

- Cipla Ltd.

- Sun Pharmaceutical Industries Limited

- Others

Frequently Asked Questions

The global vaginitis treatment drug market is projected to be valued at US$ 3.6 Bn in 2026.

Rising vaginitis prevalence, demand for targeted therapies, OTC adoption, advanced drug delivery, and women’s health awareness.

The global vaginitis treatment drug market is poised to witness a CAGR of 5.0% between 2026 and 2033.

Next-generation antifungal/antibiotic formulations, combination therapies, personalized treatments, OTC expansion, emerging markets, and microbiome-based innovations.

Pfizer Inc., Viatris Inc., Novartis AS, Bayer AG, Sanofi S.A., Lupin Pharmaceuticals, Inc.