- Non-food Packaging

- UV-Protected Tarpaulin Sheets Market

UV-Protected Tarpaulin Sheets Market Size, Share, and Growth Forecast, 2026 - 2033

UV-Protected Tarpaulin Sheets Market by Material (Polyethylene, Vinyl/PVC, Others), Thickness (100-200 GSM, 50-100 GSM, Others), Size, Application, and Regional Analysis for 2026 - 2033

UV-Protected Tarpaulin Sheets Market Size and Trends Analysis

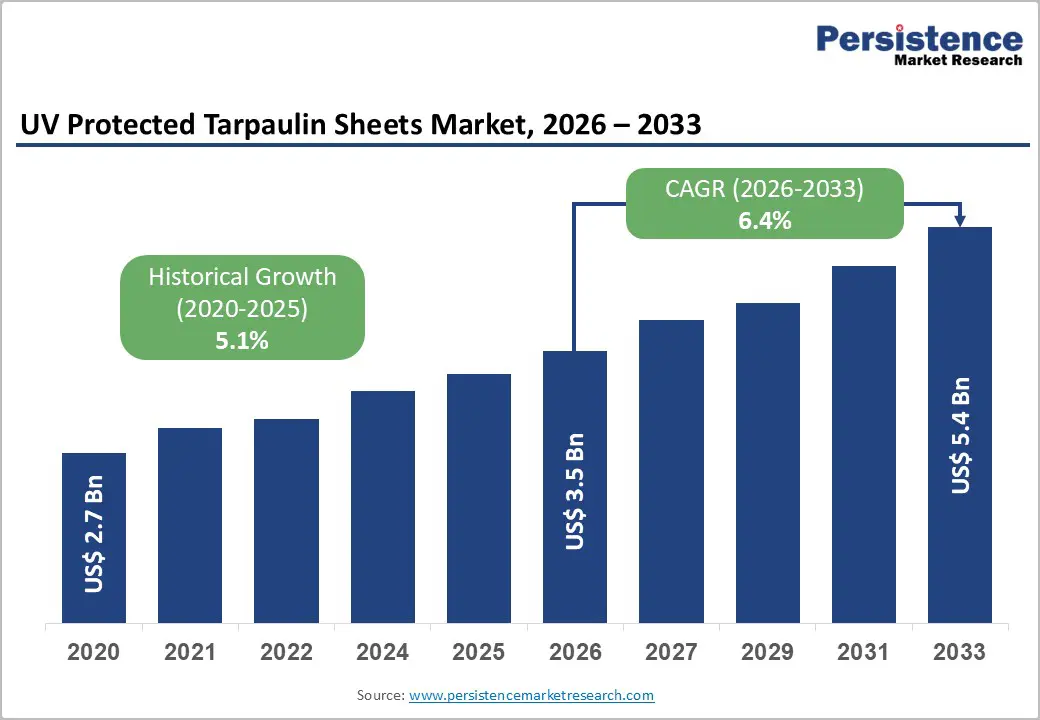

The global UV-protected tarpaulin sheets market size is likely to be valued at US$3.5 billion in 2026 and is expected to reach US$5.4 billion by 2033, growing at a CAGR of 6.4% between 2026 and 2033, driven by sustained infrastructure investment, expanding logistics and warehousing footprints, and rising agricultural demand for durable, UV-resistant coverings.

The market benefits from increasing adoption of polyethylene (PE) and coated PVC formulations that extend outdoor service life under high solar exposure. Shorter replacement cycles in emerging economies and gradual premiumization toward higher-performance, laminated, and coated tarpaulins are improving revenue per square meter, reinforcing long-term market expansion.

Key Industry Highlights

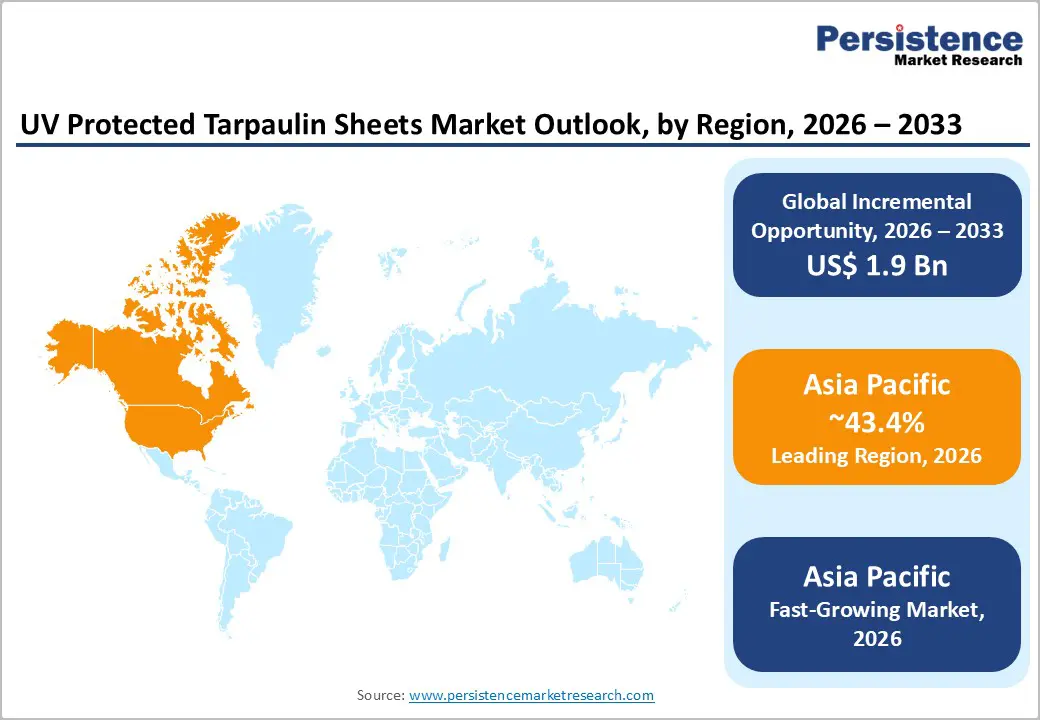

- Leading Region: Asia Pacific is projected to account for 43.4% of the market share in 2026, supported by large-scale construction activity, high agricultural usage, and strong manufacturing and export capacity in China, India, and ASEAN countries.

- Fastest-growing Region: Asia Pacific, due to accelerating infrastructure development, logistics expansion, and rising demand for cost-efficient UV-stabilized tarpaulins in emerging economies.

- Investment Plans: Ongoing investments in capacity expansion, coating and lamination technologies, and localized manufacturing in Asia Pacific and North America, with a strong focus on PVC-coated and UV-stabilized polyethylene tarpaulins to support higher-value applications and longer product lifecycles.

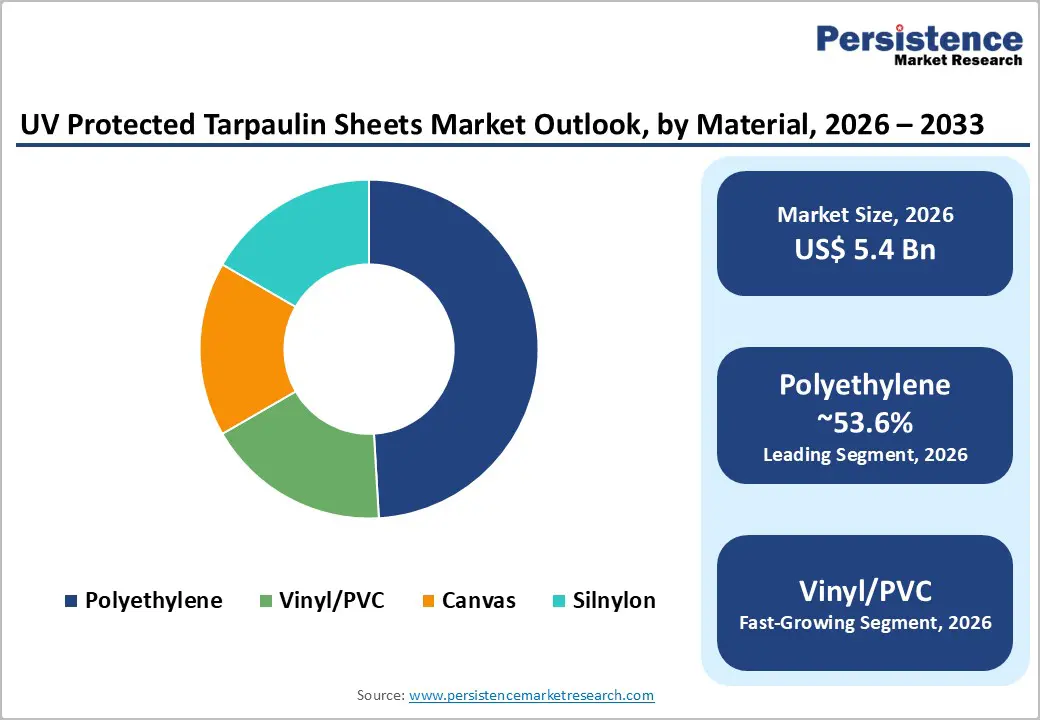

- Dominant Material: Polyethylene (PE) is expected to hold a 53.6% market share, driven by its cost efficiency, high-volume production capability, and widespread use across construction, agriculture, and logistics applications.

- Leading Thickness: The 100-200 GSM segment is estimated to account for 41.7% of the market, favored for its optimal balance of durability, UV resistance, and cost across medium-duty industrial and agricultural applications.

| Key Insights | Details |

|---|---|

| UV Protected Tarpaulin Sheets Market Size (2026E) | US$3.5 Bn |

| Market Value Forecast (2033F) | US$5.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Construction and Infrastructure Investment

Large-scale construction and infrastructure development constitute a primary driver of demand for UV-protected tarpaulin sheets. Tarpaulins are widely used for scaffolding protection, temporary roofing, site enclosures, material coverage, and civil works protection. Demand is especially strong for 100-200 GSM and above-200 GSM tarpaulins, which provide higher tensile strength and longer outdoor durability. Public infrastructure programs and private commercial construction activity directly correlate with tarpaulin consumption volumes. Revenue growth is amplified by the rising use of laminated and coated tarpaulins, which command higher unit prices than basic woven sheets. Even during periods of moderate growth in construction volume, value expansion continues due to specification upgrades and increased safety and durability requirements.

Agricultural Protection and Climate Resilience

Agriculture remains a structurally important end-use segment for UV-protected tarpaulin sheets, covering applications such as crop protection, grain storage, greenhouse covers, irrigation pond liners, and equipment shielding. Increasing climate volatility, including higher temperatures, intense solar radiation, and unpredictable rainfall patterns, has increased replacement frequency and average consumption per hectare. UV-stabilized polyethylene and PVC tarpaulins are increasingly preferred due to their longer field life and reduced risk of crop loss. In Asia Pacific and other agrarian economies, seasonal procurement cycles generate concentrated volume demand. The expansion of commercial farming and mechanization further supports higher per-unit usage, reinforcing the growth assumptions embedded in the 2026-2033 forecast.

Logistics, Warehousing, and Transportation Expansion

The expansion of logistics infrastructure, open storage yards, and transportation fleets has materially increased demand for UV-protected tarpaulin sheets. Applications include truck and trailer covers, pallet protection, container sheeting, and temporary outdoor storage. Growth in e-commerce, third-party logistics, and just-in-time distribution models has shortened replacement cycles, particularly for 50-200 GSM tarpaulins. Fleet operators increasingly prioritize life-cycle cost efficiency, leading to greater adoption of UV-stabilized, coated, and reinforced tarpaulins with longer service lives. This shift toward higher-value products supports a revenue growth rate that exceeds historical averages.

Barrier Analysis - Raw Material Price Volatility

UV-protected tarpaulin manufacturers remain exposed to volatility in polymer feedstocks, particularly polyethylene, polypropylene, and PVC resins. Fluctuations in crude oil-linked inputs, logistics costs, and regional supply disruptions can result in 8-15% swings in cost of goods sold for producers. Smaller and non-integrated manufacturers face limited hedging capabilities, increasing margin pressure during high-price cycles. A sustained 20% increase in polymer prices can reduce gross margins by approximately 6-8 percentage points, constraining investment in capacity expansion, product innovation, and quality upgrades.

Low-Cost Imports and Quality Variability

The market experiences ongoing pricing pressure from low-cost imports, particularly in commoditized PE tarpaulin segments. While these products compete aggressively on price, performance consistency and UV durability vary widely. This variability in quality complicates procurement decisions and suppresses pricing across entry-level segments. Although premium, certified tarpaulins retain stronger margins, commoditized segments remain structurally constrained. Trade measures and technical procurement specifications provide partial protection, yet inconsistent enforcement limits their effectiveness as long-term corrective mechanisms.

Opportunity Analysis - Product Premiumization and Advanced Coatings

Rising awareness of life-cycle costs and durability is driving demand for laminated, multilayer, and fire-retardant, UV-protected tarpaulins. These premium products command higher average selling prices and longer replacement cycles, improving customer value propositions. If premium products account for an incremental 8-12% of unit volume by 2030, the resulting revenue upside could reach US$200-350 million within the forecast period, based on prevailing price differentials. Standardization, certification, and warranty programs are expected to accelerate adoption across construction, logistics, and industrial applications.

Emerging Markets and Localized Manufacturing

Rapid urbanization, infrastructure expansion, and agricultural modernization across South Asia, Southeast Asia, Africa, and parts of Latin America represent significant growth opportunities. Establishing localized manufacturing or joint ventures reduces logistics costs, shortens lead times, and enables climate-specific product customization. Redirecting even 5-8% of global export volumes to regional production can improve operating margins by 3-5 percentage points while capturing demand from municipal, cooperative, and infrastructure buyers in high-growth markets.

Category-wise Analysis

Material Insights

Polyethylene is anticipated to account for approximately 53.6% of the market share in 2026, maintaining its position as the dominant material in the market. Its cost-effectiveness, lightweight, and strong compatibility with UV stabilizers make PE the material of choice for high-volume applications across construction, agriculture, and logistics. PE tarpaulins are widely used as scaffold covers, crop and grain protection sheets, temporary roofing, and pallet covers in outdoor storage yards. Their ease of processing supports mass production and broad distribution, enabling strong penetration in both developed and emerging economies. Seasonal agricultural cycles and ongoing infrastructure activity ensure consistent baseline demand, reinforcing PE’s leadership despite moderate pricing.

Vinyl- and PVC-based tarpaulins are projected to be the fastest-growing material segment, supported by their high tensile strength, superior weather resistance, and long service life. PVC tarpaulins are increasingly specified for heavy-duty and premium applications, including truck side curtains, roll-up covers, marine protection, and long-term construction enclosures. Over the forecast period, PVC is expected to capture incremental share within the overall material mix, benefiting from continued advances in coating technologies, heat-weldability, and surface treatments that enhance durability, color stability, and custom printing capabilities. These performance attributes support higher average selling prices and position PVC as the preferred material for fleet operators, event infrastructure providers, and industrial users who prioritize lifecycle performance over initial cost.

Thickness Insights

The 100-200 GSM category is anticipated to hold around 41.7% of market share in 2026, reflecting its optimal balance between durability, flexibility, and cost efficiency. Tarpaulins in this GSM range are extensively used on construction sites, in warehouses, and for agricultural storage, including machinery covers and produce protection. They provide sufficient UV resistance and mechanical strength for repeated outdoor exposure while remaining easy to handle and transport. Standardization across this GSM range enables manufacturers to realize economies of scale, while buyers favor it for medium-duty applications where performance reliability is critical but over-engineering is unnecessary.

The 50-100 GSM segment is anticipated to register the fastest growth rate, supported by rising demand from consumer, retail, and light-duty commercial applications. These thinner tarpaulins are commonly used for household covers, protecting small equipment, garden and DIY use, and short-term e-commerce packaging during transit. Improvements in UV-stabilization chemistry have significantly enhanced performance, enabling lighter fabrics to withstand outdoor exposure without a commensurate increase in cost. The rapid expansion of retail distribution networks and online marketplaces has driven high unit turnover, making this segment particularly attractive for volume-driven manufacturers and private-label brands.

Regional Insights

North America UV-Protected Tarpaulin Sheets Market Trends - Premium Fleet, Infrastructure, and System-Based Demand Stability

North America represents a mature but value-rich market for UV-protected tarpaulin sheets, supported by steady construction activity, logistics modernization, and large-scale fleet operations. The U.S. leads regional demand due to ongoing infrastructure investment, a well-developed transportation sector, and a strong preference for premium, certified tarpaulin systems over basic commodity sheets. Applications such as truck and trailer covers, roll-tarp systems, and industrial site protection account for a significant share of regional revenue, driving higher average selling prices.

Regulatory and procurement standards emphasize certified performance related to UV resistance, flame retardancy, tensile strength, and durability, which favors established manufacturers and system providers. Companies such as Shur-Co and US Tarp (now operating under Shur-Co following its acquisition) have expanded their footprint through product innovation and consolidation, strengthening aftermarket service offerings and system-based sales rather than standalone sheets. The rollout of electric and automated roll-tarp systems for fleet operators has further shifted demand toward integrated solutions, reinforcing North America’s premium positioning. Investment activity in the region increasingly targets product innovation, system integration, and replacement demand rather than greenfield capacity expansion. Growth is supported by trucking fleet upgrades, infrastructure maintenance projects, and warehouse expansion linked to e-commerce, resulting in stable, long-term value growth despite modest volume increases.

Europe UV-Protected Tarpaulin Sheets Market Trends - Regulation-Driven High-Specification and Coated Fabric Dominance

Europe’s market is shaped by stringent regulatory frameworks, high specification requirements, and a strong preference for coated and laminated fabrics. Demand is driven less by volume and more by performance, compliance, and durability, particularly in transport, industrial protection, marine, and event infrastructure applications. Germany leads the region due to its extensive logistics network and industrial base, while the U.K., France, and Spain demonstrate balanced demand across construction, agriculture, and temporary structural coverings.

European manufacturers such as Sioen, Heytex, Mehler, and Serge Ferrari play a critical role in setting market standards by supplying high-performance PVC-coated and technical tarpaulins with long service life and regulatory compliance. These companies have invested heavily in advanced coating technologies, surface treatments, and sustainable formulations to meet evolving environmental and chemical regulations. As a result, European buyers increasingly specify certified, traceable materials, raising entry barriers for low-quality imports. Regulatory harmonization across the region increases compliance costs but strengthens quality-based competition and supports premium pricing. Growth is sustained by industrial asset protection, marine and coastal use, and rising demand for temporary structures for events, exhibitions, and sports infrastructure. This environment favors technically capable producers and limits commoditization, preserving Europe’s position as a high-value regional market.

Asia Pacific UV-Protected Tarpaulin Sheets Market Trends - Cost-Competitive Mass Production with Infrastructure-Led Volume Growth

Asia Pacific leads the UV protected tarpaulin sheets market with approximately 43.4% market share and remains the fastest-growing region through the forecast period. The region benefits from a combination of agricultural demand, extensive infrastructure development, and cost-competitive manufacturing capacity. China dominates global production and exports, supplying polyethylene and PVC tarpaulins to both domestic and international markets. Large manufacturers such as DERFLEX and other Chinese exporters continue to expand coated fabric and lamination capacity, supporting both commodity and higher-value product segments. India represents one of the fastest-growing domestic consumption markets, driven by infrastructure expansion, rural development programs, and high agricultural usage. Local manufacturers such as Narmada Polyfab, Vikash Tarpaulins, and other regional brands are gaining share by offering climate-specific GSM ranges and UV-stabilized products tailored to local conditions. Government-led infrastructure projects and increased mechanization in agriculture are sustaining demand for medium and large-format tarpaulins.

ASEAN countries, including Vietnam, Thailand, and Indonesia, are emerging as both consumption and secondary manufacturing hubs, benefiting from export-oriented production and rising domestic logistics activity. Environmental regulations and plastic waste policies are gradually influencing product design across the region, encouraging the use of recyclable materials, improved UV additives, and longer-lasting fabrics. These shifts are pushing manufacturers toward higher-quality offerings, supporting continued volume growth alongside gradual value uplift across the Asia Pacific.

Competitive Landscape

The global UV-protected tarpaulin sheets market exhibits moderate fragmentation, with numerous regional manufacturers serving commoditized PE segments and a smaller group of specialized players dominating premium PVC and system-based applications. Value concentration is higher in heavy-duty and transport-oriented tarpaulin systems, while basic tarpaulins remain highly competitive on price.

Recent years have seen increased consolidation, new product launches in electric and automated tarp systems, expanded agricultural tarpaulin offerings, and capacity investments in coated fabric production. Strategic focus areas include system integration, geographic expansion, and innovation in higher-performance materials.

Leading companies emphasize product differentiation, cost optimization, geographic expansion, and aftermarket services. Innovation in coatings, laminations, and integrated tarp systems is increasingly central to competitive positioning.

Key Industry Developments

- In November 2025, Shur-Co unified its flatbed and tarpaulin businesses under the Shur-Co brand to improve market clarity and streamline product offerings across roll tarp, electric systems, and cargo-covering solutions.

- In April 2025, Shur-Co launched its new Shur-Lok E-Series Electric Roll Tarp System, enabling the effortless conversion of manual tarps to electric roll systems for grain trailers and fleets, enhancing operational efficiency and durability in transport and logistics.

Companies Covered in UV-Protected Tarpaulin Sheets Market

- Shur-Co

- DERFLEX

- Sioen Industries

- Serge Ferrari Group

- Heytex Group

- Mehler Texnologies

- US Tarp

- Cunningham Covers

- TenCate

- Laird Plastics

- Trivantage

- Narmada Polyfab

- Vikash Tarpaulins

- Shree Ram Tarpaulins

- G S Tarpaulin Industries

- Tarp Supply Inc.

- Canadian Tarpaulin Manufacturers

- Batra Tarpaulin Industries

Frequently Asked Questions

The global UV protected tarpaulin sheets market size is valued at US$3.5 billion in 2026.

By 2033, the UV protected tarpaulin sheets market is expected to reach US$5.4 billion.

Key trends include premiumization toward PVC and coated fabrics, rising demand from infrastructure and logistics, wider use of UV-stabilized polyethylene in agriculture, growth of retail and e-commerce distribution for standardized sizes, and increasing focus on longer service life and certified performance.

By material, polyethylene (PE) is the leading segment, accounting for 53.6% market share, supported by its cost-efficiency and wide usage across construction, agriculture, and storage applications.

The UV protected tarpaulin sheets market is projected to grow at a CAGR of 6.4% between 2026 and 2033.

Major players include Shur-Co, DERFLEX, Sioen Industries, Serge Ferrari Group, and Heytex Group.