- Transportation & Logistics

- Utility Equipment Market

Utility Equipment Market Size, Share, and Growth Forecast, 2025 - 2032

Utility Equipment Market By Product (Garbage Trucks, Street Sweepers, Static Compactors), Power Source (Electric Utility Equipment, Conventional Utility Equipment), End-use (Municipality Utility Equipment, Industrial Utility Equipment, Others), Regional Analysis 2025 - 2032

Utility Equipment Market Share and Trends Analysis

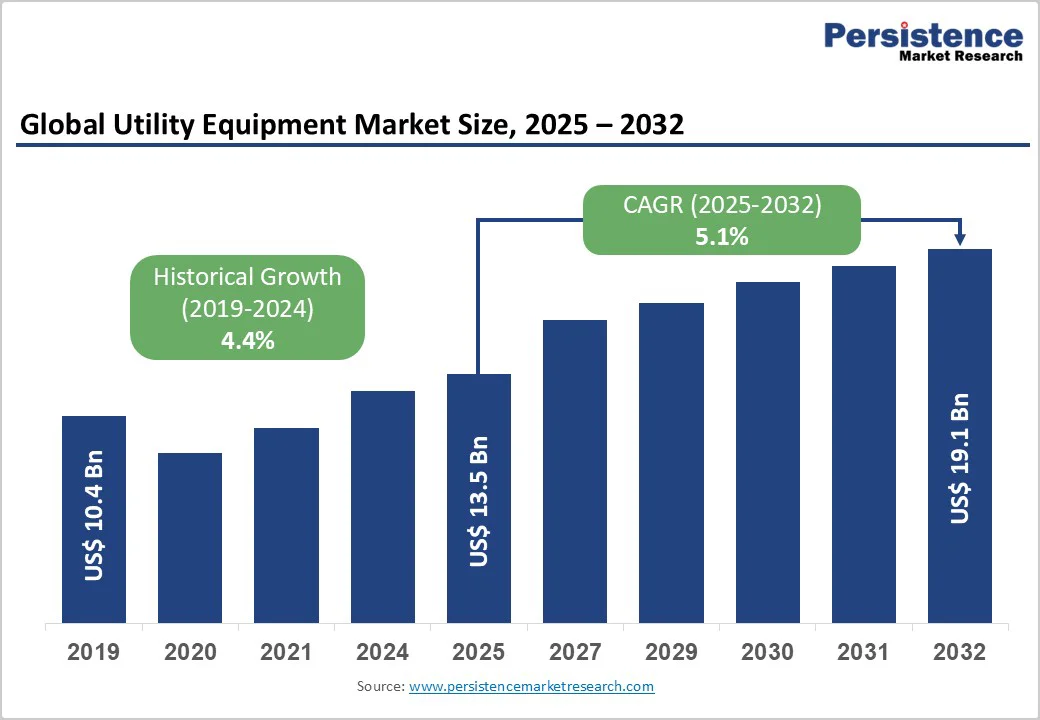

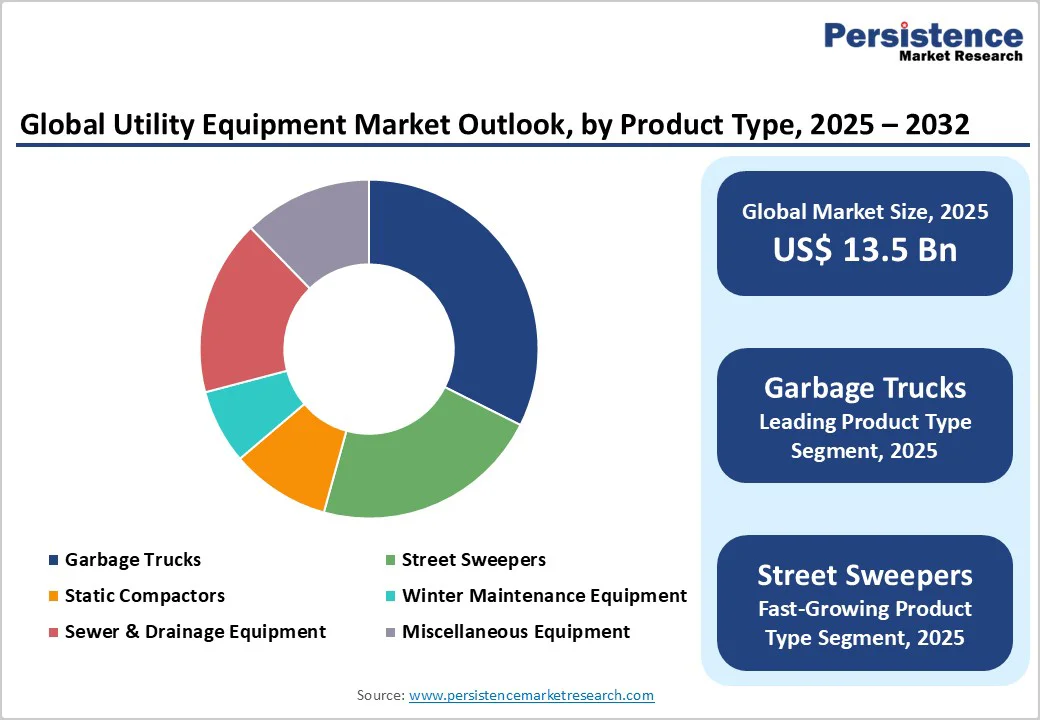

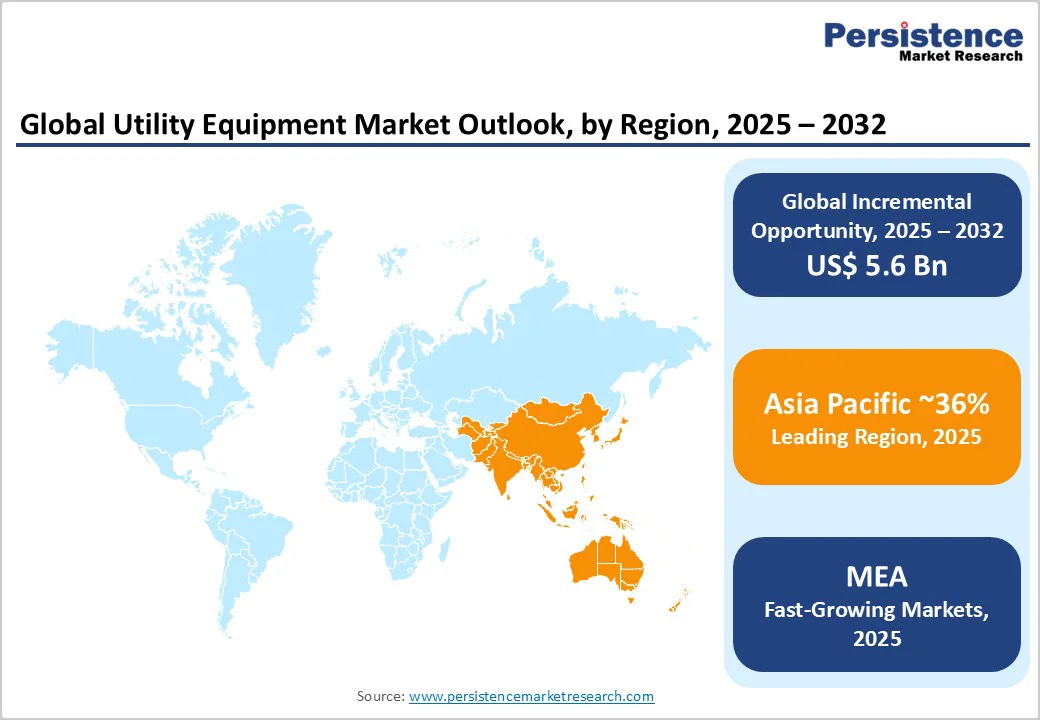

The global utility equipment market size is likely to value at US$ 13.5 billion in 2025 and is projected to reach US$ 19.1 billion by 2032, growing at a CAGR of 5.1% between 2025 and 2032.

The market is growing due to rising urban needs, aging infrastructure upgrades, and faster adoption of eco-friendly city services in developed and emerging regions. Growth is driven by government infrastructure investments, strict environmental rules requiring cleaner equipment, and efficiency-boosting technologies. Aging utilities in developed markets demand full equipment replacements, while rapid urban growth in Asia Pacific and emerging economies fuels new projects, ensuring steady demand across products and regions.

Key Industry Highlights:

- Dominant Product Segments: Garbage Trucks lead with 32% market share. Street Sweepers emerge as fastest-growing segment at a positive CAGR through 2032, reflecting environmental focus and urban cleanliness priorities

- Power Source Transformation: Conventional equipment maintains 84% dominance; Electric equipment projects highest growth at 9.5% CAGR, driven by sustainability mandates and total cost of ownership advantages

- End-Use Leadership: Municipal applications command 68% market share; Airport segment demonstrates fastest growth through 2032, supported by air traffic expansion and safety requirements

- Regional Growth Dynamics: Asia Pacific dominates with 36% market share, representing primary long-term growth engine; North America achieves prominent 4.7% CAGR; Europe maintains 21% share with sustainability leadership

- Technology Evolution: Electrification, IoT integration, telematics, and automation transform competitive dynamics, with manufacturers investing substantially in digital capabilities and zero-emission solutions

- Strategic Investments: Major manufacturers including Volvo CE announce multi-billion-dollar production capacity expansions; smart city initiatives drive ?1.47 lakh crore infrastructure investments in India alone, accelerating equipment deployment

| Key Insights | Details |

|---|---|

| Utility Equipment Market Size (2025E) | US$ 13.5 Billion |

| Market Value Forecast (2032F) | US$ 19.1 Billion |

| Projected Growth CAGR (2025 - 2032) | 5.1% |

| Historical Market Growth (2019 - 2024) | 4.4% |

Market Dynamics Analysis

Drivers - Infrastructure Modernization and Urban Expansion Imperatives

Global urbanization represents the most significant demand catalyst for utility equipment, with the United Nations projecting that 70 percent of the world's population will reside in urban areas by 2050.

This demographic shift generates unprecedented pressure on municipal service infrastructure. In the United States alone, electric utilities are investing nearly $208 billion on power grid infrastructure in 2025, with total investments exceeding US$1.1 trillion over the next five years according to the Edison Electric Institute.

The Infrastructure Investment and Jobs Act (IIJA) has allocated over $568 billion for state-level projects, including roads, bridges, airports, and EV charging stations as of November 2024. Municipal solid waste management infrastructure requirements are equally substantial, with the sector projected to grow significantly at a CAGR of 3.3%.

Indian cities alone are expected to generate 435 million tonnes of solid waste by 2050, necessitating massive equipment deployment. This infrastructure imperative creates sustained, multi-decade demand cycles for garbage trucks, street sweepers, sewer equipment, and winter maintenance machinery across global markets.

Regulatory Compliance and Environmental Sustainability Mandates

Stringent environmental regulations are fundamentally reshaping utility equipment specifications and accelerating replacement cycles. Municipal authorities worldwide face mounting pressure to reduce emissions, improve air quality, and demonstrate environmental stewardship.

The European Union's Green Deal-linked public works pipeline is compressing procurement cycles from 18-24 months to as few as 12 months, with contractors increasingly favoring Stage V-compliant or electric models even when premiums exceed ten percent to secure eligibility for Green Deal tenders. Street sweeper adoption is being driven by environmental regulations and air quality standards, with the global market grow at a CAGR of 4.4% through 2034.

In January 2025, FEMA funded nearly $2.6 million to restore critical roads in Puerto Rico municipalities, while hundreds of European cities received federal funding for safer street infrastructure. The EPA's Clean Watershed Needs Survey estimates the U.S. will require more than $630 billion over the next 20 years for safe drinking water supply infrastructure. These regulatory drivers ensure sustained investment in compliant, environmentally superior utility equipment.

Restraints - High Capital Investment and Equipment Costs

Advanced utility equipment, particularly electric and automated variants, requires substantial upfront capital investments that constrain adoption rates among budget-limited municipal authorities and smaller private operators.

Electric refuse trucks and automated street sweepers command significant price premiums over conventional alternatives, while also necessitating supporting infrastructure investments including charging stations, specialized maintenance facilities, and technician training programs.

Static compactor systems, while offering 4:1 to 10:1 compaction ratios and substantial transport cost savings, require permanent installation and integration investments that deter smaller operators.

Municipal budget constraints, particularly in developing markets and smaller jurisdictions, limit the pace of fleet modernization despite clear operational and environmental advantages. Rising raw material costs, supply chain disruptions from China and South Korea, and proposed safeguard duties on steel further pressure OEM margins and equipment affordability, particularly impacting smaller manufacturers and cost-sensitive buyers.

Supply Chain Vulnerabilities and Extended Lead Times

The utility equipment sector faces persistent supply chain challenges affecting production schedules, pricing stability, and market growth. The construction equipment industry in India experienced headwinds including extended monsoons, rising raw material costs, and supply chain disruptions particularly from China and South Korea during 2024-25.

Capital investment in distribution line transformers increased prominently as a direct result of supply chain and manufacturing issues. Chip shortages and component availability constraints have impacted equipment production across multiple segments. Labor shortages in both manufacturing and field operations create bottlenecks, with many infrastructure projects experiencing substantial delays and cost increases during construction and operations phases.

Geopolitical tensions affect critical material supply chains, while fluctuating commodity prices introduce pricing uncertainty. These supply chain vulnerabilities increase total cost of ownership unpredictability and complicate long-term procurement planning for municipal authorities and private operators.

Market Opportunities

Smart City Infrastructure Integration and Digital Transformation

Smart city initiatives globally create substantial opportunities for utility equipment featuring advanced digital capabilities and system integration. The Smart Cities Mission in India has invested INR 1.47 lakh crore to enhance urban infrastructure, completing 91% of 8,075 projects with installations including 84,000 CCTV cameras, 17,026 km of SCADA-monitored water pipelines, and 9,194 digitally tracked waste management vehicles.

Automated waste collection systems using underground vacuum technology reduce traffic congestion, emissions, and operational costs while integrating seamlessly with IoT sensors and AI-driven analytics for real-time monitoring. Telematics-enabled equipment provides actionable insights for fleet optimization, predictive maintenance scheduling, and route efficiency improvements.

The utility asset management market is growing at a CAGR of 9.95% during 2025 - 2032, driven by smart technology adoption. Equipment manufacturers offering IoT connectivity, data analytics platforms, and integration capabilities with broader smart city ecosystems can command premium positioning and capture growing municipal technology budgets allocated for digital transformation initiatives.

Emerging Market Infrastructure Development and Urbanization

Rapid urbanization and infrastructure development in emerging markets, particularly across Asia Pacific, present exceptional growth opportunities. Asia is projected to account for more than two-thirds of global infrastructure investment through 2030, reflecting rapid urbanization, population growth, and industrial expansion.

China, India, and Southeast Asian nations are experiencing unprecedented urban growth requiring comprehensive municipal service infrastructure deployment. India's infrastructure spending, airport expansions, and smart city programs drive substantial utility equipment demand, with the construction equipment market showing resilience despite modest 3% growth in 2024-25.

Africa and Latin America similarly face substantial infrastructure deficits requiring equipment investments. Equipment manufacturers establishing local production capabilities, distribution networks, and service infrastructure in high-growth emerging markets can capture substantial volume growth, albeit often at lower price points than developed market premium segments.

Category-wise Analysis

Product Type Analysis

Garbage Trucks represent the dominant product segment, commanding a 32% share in 2025, reflecting their critical role in municipal solid waste management systems worldwide.

Leading manufacturers including McNeilus Truck & Manufacturing, Heil Environmental, Dennis Eagle, and Labrie Enviroquip Group dominate through decades of experience and extensive distribution networks. Increasing environmental concerns and strict regulations concerning air and water pollution are compelling municipalities to adopt advanced refuse collection vehicles.

The segment benefits from continuous fleet replacement cycles, capacity expansions matching urban growth, and technology upgrades including electric powertrains and automated collection systems that enhance operational efficiency and reduce environmental impact.

Street sweepers emerge as the fastest-growing product segment, driven by heightened environmental sustainability focus and urban cleanliness standards. The global street sweeper market is projected to grow at a CAGR of 4.4% through 2034. Rapid urbanization and infrastructure development create sustained demand for effective street cleaning technologies that reduce dust, litter, and pollutants affecting air quality and drainage systems.

Technological advancements including electric and autonomous street sweepers enhance efficiency, cost savings, and environmental friendliness, attracting public and private sector investment. The segment's growth reflects increasing municipal budget allocations for visible cleanliness improvements, regulatory compliance requirements, and smart city infrastructure integration priorities.

Power Source Analysis

Conventional Utility Equipment maintains overwhelming market dominance with an 84% share in 2025, reflecting established technology maturity, lower upfront costs, and extensive service infrastructure supporting diesel and gasoline-powered equipment. Conventional equipment delivers proven reliability, extended operating ranges, and rapid refueling capabilities essential for demanding municipal service applications.

Conventional equipment manufacturers are responding through efficiency improvements, emission reduction technologies, and hybrid alternatives that bridge toward full electrification while maintaining operational capabilities municipal operators require for uninterrupted service delivery across diverse environmental conditions and demanding duty cycles.

Electric utility equipment represents the market's highest-growth segment through 2032, driven by environmental regulations, total cost of ownership advantages, and technological maturation. Electric equipment delivers zero direct emissions, substantially reduced noise pollution, lower fuel and maintenance costs, and alignment with municipal sustainability commitments.

Leading manufacturers are launching comprehensive electric product lines, with Dennis Eagle's eCollect electric garbage truck gaining traction across European municipalities, and Volvo CE introducing electric excavators with 450 kWh batteries designed for full-day operation.

Battery technology improvements, charging infrastructure expansion, and government incentives are accelerating adoption curves. Municipal utilities are prioritizing electric fleet transitions supported by grid modernization investments and renewable energy integration.

End-use Analysis

Municipal applications dominate the utility equipment market with a commanding 68% share in 2025, reflecting local governments' primary responsibility for public infrastructure management including waste collection, street cleaning, water/sewer maintenance, and winter road maintenance.

Municipal authorities worldwide face mounting service demands from urban population growth, aging infrastructure replacement requirements, and elevated environmental standards. Municipal budgets now emphasize visible service upgrades, smart city tech, and sustainability. Steady replacement cycles and government funding drive demand, favoring trusted manufacturers offering reliable equipment, cost efficiency, and strong service networks.

Airport applications emerge as the fastest-growing end-use segment with prominent CAGR through 2032, driven by global air traffic expansion and stringent operational safety requirements. Airports require specialized, high-performance equipment for rapid clearing, de-icing, and maintenance to minimize flight delays and ensure operational safety during adverse weather.

The aircraft ground support equipment market is projected to grow from USD 11.7 billion in 2025 to USD 18.6 billion by 2032 at a CAGR of 6.8%, supporting broader airport infrastructure modernization. Airport operators increasingly adopt electric GSE to reduce emissions, meet sustainability targets, and improve operational efficiency.

The segment's growth reflects rising global air travel demand, airport capacity expansions particularly in Asia Pacific, and accelerating adoption of automated and electric equipment aligned with smart airport initiatives and environmental compliance mandates.

Regional Market Insights

North America Utility Equipment Market Trends

North America demonstrates the most prominent regional CAGR of 4.7% through 2032, positioning as a critical growth market despite a mature infrastructure baseline. The United States leads regional growth driven by unprecedented utility infrastructure investments, with electric utilities spending nearly $208 billion in 2025 and over $1.1 trillion projected over five years.

The IIJA provides sustained federal funding momentum, allocated significant investment for infrastructure projects as of November 2024.

Aging infrastructure replacement requirements drive substantial equipment demand, with the EPA estimating $630 billion needed over 20 years for drinking water infrastructure alone. North American municipalities lead electric equipment adoption, supported by stringent emission standards, comprehensive charging infrastructure, and strong sustainability commitments.

The region's mature regulatory environment, advanced technology adoption, and substantial public/private infrastructure investments ensure sustained market growth despite higher baseline market penetration versus emerging regions.

Europe Utility Equipment Market Trends

Europe commands a significant 21% global market share in 2025, reflecting the region's advanced environmental regulations, comprehensive municipal service standards, and leadership in sustainable equipment adoption. Germany dominates European utility equipment demand driven by robust transit infrastructure projects, residential construction, and renewable energy initiatives supported by technology and sustainability leadership.

The EU Green Deal-linked public works pipeline accelerates procurement cycles and mandates Stage V-compliant or electric equipment for tender eligibility. France is investing substantially in transport infrastructure with a $108.1 billion railway development plan through 2040, while maintaining focus on electric construction equipment adoption.

European municipalities lead global electrification trends, with Dennis Eagle's eCollect electric garbage truck exemplifying regional technology leadership. Regulatory harmonization, comprehensive recycling programs, and ambitious carbon neutrality targets drive sustained investment in premium, environmentally superior utility equipment across the region's mature markets.

Asia Pacific Utility Equipment Market Trends

Asia Pacific represents the dominant regional market with 36% global share in 2025 and projects the highest absolute growth through 2032, driven by rapid urbanization, infrastructure development imperatives, and massive government investments. The region accounts for over two-thirds of projected global infrastructure investment through 2030, reflecting substantial urbanization, population growth, and industrial expansion.

China leads regional demand through extensive municipal infrastructure projects, smart city initiatives, and domestic manufacturing capacity, with companies such as SANY and Zoomlion expanding globally. India represents exceptional growth potential, with cities projected to generate 435 million tonnes of solid waste by 2050 requiring comprehensive equipment deployment.

The Smart Cities Mission in India has invested INR 1.47 lakh crore across 8,075 projects, including digitally tracked waste management systems. Japan maintains advanced equipment standards with a focus on disaster resilience and aging infrastructure replacement.

Southeast Asian nations, including Indonesia, Vietnam, and the Philippines, experience rapid urban growth requiring greenfield infrastructure deployment. The region's diverse development stages, manufacturing cost advantages, and sustained urbanization momentum position Asia Pacific as the utility equipment market's primary long-term growth engine.

Competitive Landscape

The global utility equipment market remains moderately consolidated, led by global giants like Caterpillar, Komatsu, Deere, Volvo CE, SANY, and Hitachi, supported by vast product ranges and dealer networks. In garbage collection trucks, leaders such as McNeilus, Heil, Dennis Eagle, and Labrie dominate through legacy expertise and nationwide reach.

Specialized areas like winter maintenance, compactors, and airport support equipment remain fragmented, favoring niche players. Competition increasingly centers on electrification, telematics, automation, and smart fleet integration, as manufacturers pursue premium positioning aligned with municipal modernization and sustainability goals.

Strategic Developments

- Volvo Construction Equipment Strategic Investment in Crawler Excavator Production (June 2025): Volvo CE announced a strategic global investment of approximately 2,500 MSEK in crawler excavator production across facilities in South Korea, Sweden, and North America. This expansion enhances capacity and flexibility near key markets, improving operational efficiency, reducing delivery times, and lowering carbon emissions through localized production. The investment demonstrates commitment to meeting growing customer demand while preparing for sustainable solution deployment, reinforcing Volvo CE's market presence and competitive positioning in the excavator segment.

- McNeilus Volterra ZSL Electric Refuse Vehicle Recognition (2025): McNeilus Truck and Manufacturing's Volterra ZSL electric refuse and recycling collection vehicle won the 2025 "Coolest Thing Made in Tennessee" competition, highlighting industry leadership in electric waste collection technology. This recognition reflects accelerating municipal interest in zero-emission refuse equipment and validates manufacturers' electric vehicle development investments. The Volterra ZSL exemplifies the competitive shift toward electrified municipal fleets driven by environmental regulations and total cost of ownership advantages.

Companies Covered in Utility Equipment Market

- Caterpillar Inc.

- Komatsu Ltd.

- SANY Group Company Ltd.

- Volvo Construction Equipment

- Deere & Company (John Deere)

- Hitachi Construction Machinery

- Doosan Infracore

- Liebherr Group

- XCMG Group

- Zoomlion Heavy Industry Science & Technology Co., Ltd.

- McNeilus Truck and Manufacturing, Inc.

- Heil Environmental

- Dennis Eagle

- CNH Industrial

- JCB

Frequently Asked Questions

The global utility equipment market is likely to value at US$ 13.5 billion in 2025 and is experiencing robust expansion driven by infrastructure modernization requirements, and environmental sustainability mandates across developed and emerging markets worldwide.

Primary market drivers include accelerating urbanization with 70% of global population projected in urban areas by 2050, and technological innovations in electrification, automation, and IoT integration enhancing operational efficiency and total cost of ownership economics.

The utility equipment market is projected to grow at CAGR of 5.1% between 2025 and 2032.

Transformative opportunities include electric equipment adoption, smart city infrastructure integration with IoT and telematics capabilities, emerging market urbanization, particularly across the Asia Pacific, airport ground support equipment expansion driven by global air traffic growth, and municipal fleet electrification programs supported by substantial government incentives and environmental mandates.

Leading global manufacturers include Caterpillar Inc., Komatsu Ltd., SANY Group Company Ltd., Volvo Construction Equipment, Deere & Company, Hitachi Construction Machinery, Liebherr Group, XCMG Group, and other players.