- Non-food Packaging

- Trigger Spray Bottle Market

Trigger Spray Bottle Market Size Share, and Growth Forecast, 2026 - 2033

Trigger Spray Bottle Market by Material (Polyethylene (PE), Polyethylene Terephthalate (PET), Others), Capacity (100-250 ml, Above 250 ml, Others), Application, and Regional Analysis for 2026 - 2033

Trigger Spray Bottle Market Size and Trends Analysis

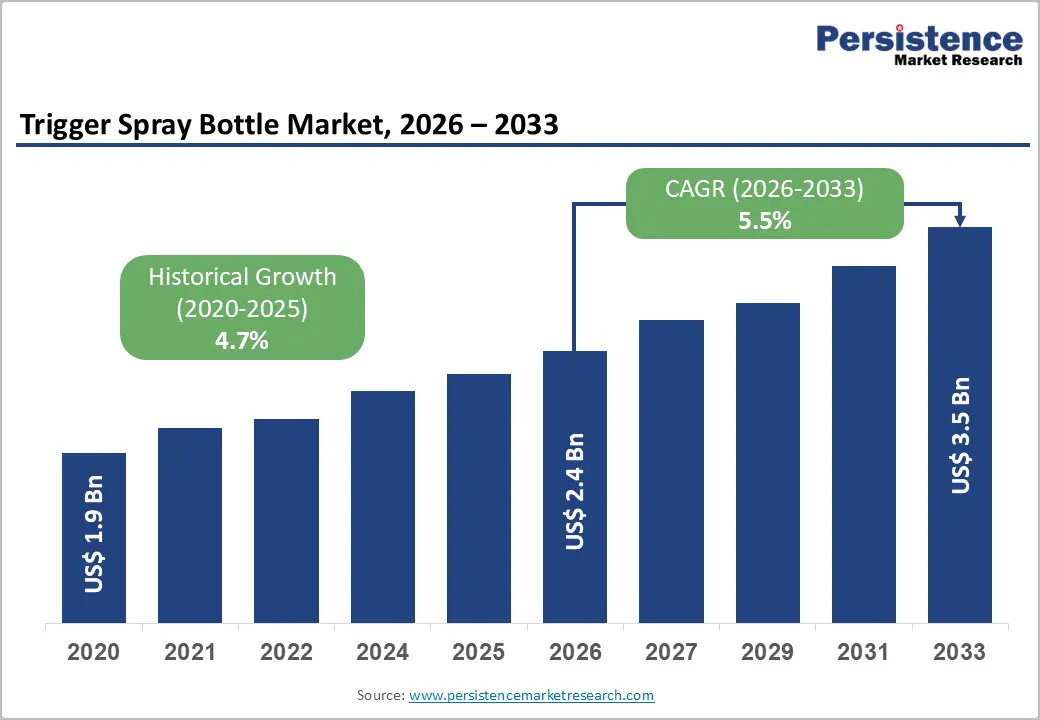

The global trigger spray bottle market size is likely to be valued at US$2.4 billion in 2026 and is expected to reach US$3.5 billion by 2033, growing at a CAGR of 5.5% between 2026 and 2033, driven by sustained volume growth in household cleaning and personal-care product categories, increasing regulatory pressure for recyclable packaging designs, and continuous product-level innovation such as all-plastic trigger mechanisms and recyclable closures.

Manufacturers are actively shifting toward polyolefin-based recyclable triggers, incorporating post-consumer recycled (PCR) plastics, and introducing larger-capacity formats for industrial and agricultural applications. Short-term market risks include raw material price volatility and supply chain restructuring following major industry consolidation.

Key Industry Highlights

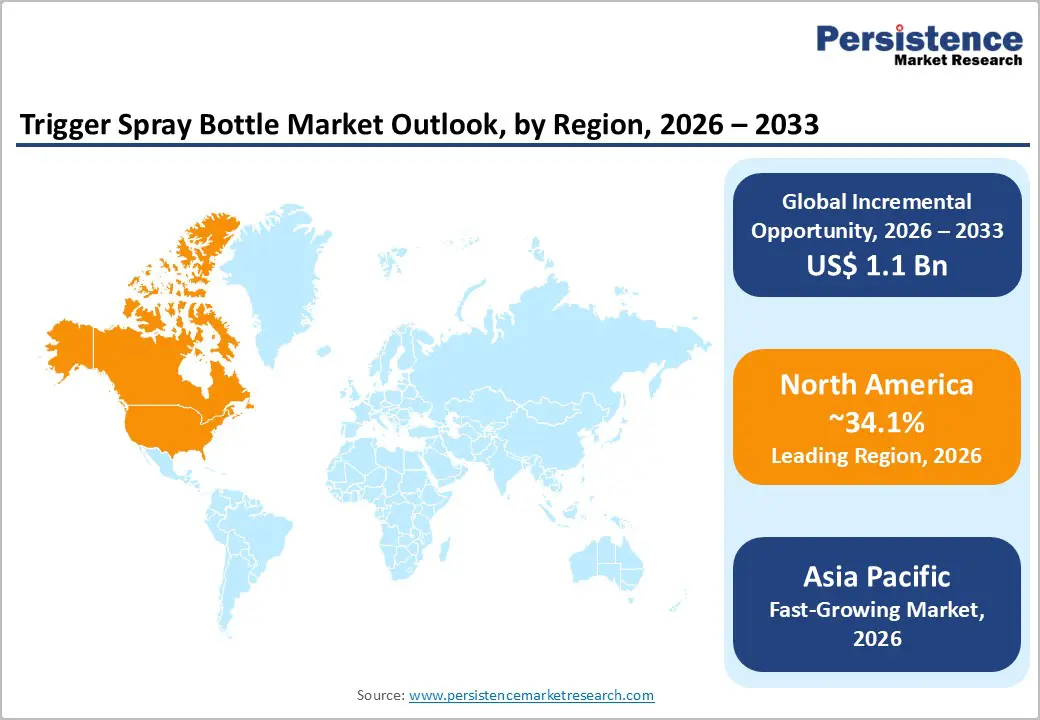

- Leading Region: North America is projected to account for approximately 34.1% of market share, driven by high per-capita consumption of homecare cleaning products, strong private-label penetration, and early adoption of recyclable and PCR-inclusive trigger spray designs across the U.S. retail ecosystem.

- Fastest-growing Region: Asia Pacific, projected to record the highest growth rate through 2033, supported by rapid urbanization, rising hygiene awareness, expansion of modern retail and e-commerce, and cost-competitive manufacturing capabilities in China, India, and ASEAN markets.

- Investment Plans: Investments are concentrated in mono-material trigger innovation, PCR sourcing, and high-speed automated assembly lines, particularly in North America and Europe, while Asia Pacific continues to attract capacity expansion and export-oriented manufacturing investments to support global supply chains.

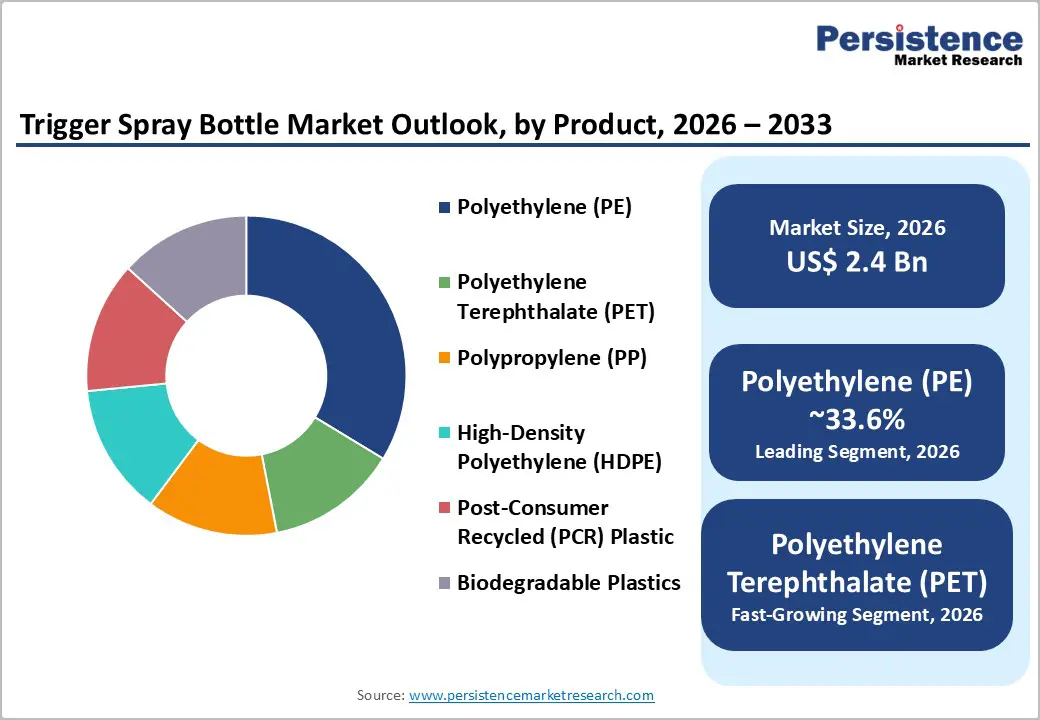

- Dominant Material: Polyethylene (PE) is anticipated to hold 33.6% market share, favored for its low cost, chemical resistance, processing flexibility, and compatibility with high-volume homecare applications and existing polyolefin recycling streams.

- Leading Application: Homecare is estimated to account for 34.7% of market share in 2026, supported by high turnover of surface cleaners, glass cleaners, and multipurpose sprays, as well as strong demand from both branded and private-label consumer packaged goods manufacturers.

| Key Insights | Details |

|---|---|

| Trigger Spray Bottle Market Size (2026E) | US$2.4 Bn |

| Market Value Forecast (2033F) | US$3.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.7% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Growth in Household Cleaning and Hygiene Categories (Volume-Driven Demand)

Demand for household cleaning products has remained structurally elevated following changes in consumer hygiene behavior, urbanization trends, and higher cleaning frequency across residential and institutional settings. Trigger spray bottles are a preferred dispensing format for surface cleaners, disinfectants, glass cleaners, and multipurpose sprays, thanks to their controlled dosing and ease of use. The expansion of product variants, including concentrated formulations, refill-ready sprays, and multi-surface solutions, has increased SKU counts and directly raised unit demand for trigger bottles. As brands increasingly upgrade packaging for functional differentiation and consumer convenience, household-grade trigger formats are expected to grow faster than the broader rigid packaging market, reinforcing their role as a high-volume consumption component.

Sustainability and Recyclability Requirements Shaping Material Choice

Regulatory frameworks and corporate sustainability commitments are accelerating the transition toward recyclable and circular packaging solutions. Policymakers and brand owners are promoting mono-material designs and higher PCR content to meet recycling targets and extended producer responsibility requirements. In response, suppliers are introducing all-plastic trigger assemblies, including plastic springs and mono-polyolefin constructions, which improve recyclability by eliminating metal components. This shift is increasing demand for PET-, PE-, and PP-compatible trigger systems and strengthening the commercial viability of PCR feedstocks. Over time, the structural transition toward recyclable trigger designs is expanding the premium segment and reshaping procurement specifications across major end-use industries.

Product Innovation and Supplier R&D (Performance and Cost Optimization)

Continuous engineering improvements in trigger spray mechanisms are expanding application scope while lowering total ownership costs. Innovations such as reduced actuation force, adjustable spray patterns, enhanced sealing, and metal-free internal components have improved ergonomics, durability, and compatibility with a wider range of formulations. These advances have enabled broader adoption in cosmetics, industrial cleaning, and agricultural spraying applications, where precision and reliability are critical. Product innovation strengthens supplier differentiation, improves long-term customer retention among branded OEMs, and supports higher average selling prices for premium trigger assemblies.

Barrier Analysis - Raw-Material Price Volatility and Upstream Supply Concentration

Trigger spray bottles depend heavily on polyolefins and engineered plastics, whose pricing is influenced by fluctuations in feedstock costs, regional capacity constraints, and energy-market dynamics. Sudden increases in resin prices can compress margins, particularly for small and mid-sized manufacturers with limited hedging capability. Price volatility may also trigger short-term inventory corrections and delayed procurement cycles among downstream buyers. Historically, resin price spikes have resulted in measurable margin erosion for contract manufacturers, increasing operational risk and limiting pricing flexibility.

Market Consolidation and Procurement Pressure from Large Buyers

Ongoing consolidation across the packaging value chain has increased purchasing power among large consumer goods companies, intensifying price competition for trigger suppliers. Smaller manufacturers face growing pressure to invest in sustainability certifications, tooling upgrades, and compliance systems to remain eligible suppliers. These capital requirements raise entry barriers and may reduce supplier diversity, potentially slowing innovation among smaller players. Recent large-scale acquisitions have already altered supplier bargaining dynamics and reinforced the importance of scale and portfolio breadth.

Opportunity Analysis - Recyclable All-Plastic Triggers and PCR Integration

The shift toward mono-material trigger designs presents a substantial revenue opportunity within the premium segment. As brands prioritize circularity and recyclability, demand for all-plastic triggers compatible with established recycling streams is accelerating. If recyclable-compatible triggers account for even a moderate share of incremental unit demand by 2030 in developed markets, the resulting revenue potential would represent a significant expansion within the trigger category. Suppliers that invest in plastic-spring technology, mono-polyolefin assemblies, and secured PCR supply agreements are well positioned to capture premium pricing and secure long-term contracts.

Asia Pacific Manufacturing Expansion and Customization

Asia Pacific offers strong growth potential due to rapid urbanization, expanding middle-class populations, and the rise of modern retail and e-commerce channels. Demand spans both cost-sensitive household products and higher-margin specialty applications in cosmetics and personal care. Establishing or expanding local manufacturing capabilities enables suppliers to serve regional brands efficiently while supporting export-oriented production. Given its growth trajectory, the Asia Pacific is expected to contribute the largest share of incremental global trigger spray bottle volumes through 2033.

Category-wise Analysis

Material Insights

Polyethylene is anticipated to retain its position as the leading material segment, holding a 33.6% market share, driven by its favorable cost structure, processing flexibility, and strong chemical resistance across a wide range of formulations. Low-density polyethylene (LDPE) is extensively used in flexible components such as dip tubes and nozzle seals, while high-density polyethylene (HDPE) is preferred for rigid bottles and load-bearing trigger components due to its strength and durability. PE-based trigger systems are particularly dominant in high-volume home care applications, where price sensitivity, supply reliability, and compatibility with existing recycling streams are critical procurement criteria. In North America and parts of Europe, manufacturers have introduced PE-compatible trigger designs engineered for recyclability within polyolefin waste streams, enabling brand owners to meet sustainability targets without costly modifications to filling lines or tooling. These attributes collectively support PE’s continued leadership across mass-market applications.

PET is anticipated to emerge as the fastest-growing material segment as recyclability and circular-economy considerations increasingly influence packaging decisions. PET’s lightweight structure, transparency, and strong consumer recognition as a recyclable material make it particularly attractive for brands seeking visible sustainability credentials. Growth is most pronounced in regions with advanced collection, sorting, and reprocessing infrastructure, where PET recycling rates are well established and commercially viable. Personal care and premium homecare brands are increasingly pairing PET bottles with PET-compatible or mono-material trigger systems to enable end-to-end recyclability. Suppliers are actively collaborating with bottle manufacturers to ensure mechanical compatibility, spray performance consistency, and structural integrity, positioning PET as a strategic growth material for sustainability-led packaging portfolios.

Application Insights

The homecare segment is anticipated to continue dominating overall demand, accounting for 34.7% of market share, supported by the extensive use of trigger spray bottles in surface cleaners, glass cleaners, disinfectants, and multipurpose household sprays. High product turnover, frequent repurchase cycles, and the widespread presence of private-label offerings drive substantial unit volumes across retail channels. Supermarkets, mass merchandisers, and online platforms favor standardized trigger formats that support operational efficiency and shelf consistency. Suppliers that align closely with consumer packaged goods procurement cycles, offer scalable production capacity, and deliver cost-optimized trigger designs consistently secure long-term supply agreements in this segment. As refill-ready and concentrated formulations gain traction, homecare demand is expected to remain a stable volume anchor for the market.

The cosmetics and personal care segment is the fastest-growing end-use segment over the forecast period. Brands are increasingly adopting trigger spray formats for applications such as hair mists, leave-in conditioners, body sprays, facial mists, and on-the-go sanitizing products, where controlled dosing and uniform spray distribution enhance user experience. Growth is reinforced by heightened hygiene awareness, premiumization of personal care routines, and the rapid expansion of e-commerce and subscription-based retail models. Packaging differentiation through fine-mist performance, premium surface finishes, and leak-resistant, e-commerce-ready designs enables higher margins compared to traditional home care applications. As personal care brands continue to prioritize aesthetics, functionality, and sustainability, trigger spray systems are becoming a more integral component of premium packaging strategies.

Regional Insights

North America Trigger Spray Bottle Market Trends - Retail-Driven Volume Demand and Sustainability-Led Design Innovation

North America is expected to account for approximately 34.1% of global market share, supported by high household cleaning consumption, a well-established organized retail ecosystem, and early adoption of recyclable packaging formats. The U.S. dominates regional demand due to high per-capita usage of packaged surface cleaners, disinfectants, and specialty sprays, alongside strong private-label penetration across retailers such as Walmart, Costco, and Target. Major homecare brands, including Clorox, SC Johnson, and Reckitt, continue to rely heavily on trigger spray formats across flagship products, reinforcing sustained baseline demand.

Regulatory momentum, particularly state-level extended producer responsibility (EPR) frameworks and retailer-led sustainability scorecards, is accelerating the transition toward mono-material trigger designs and the integration of post-consumer recycled (PCR) content. In response, packaging suppliers in the region are investing in recyclable trigger innovation, automation, and high-speed assembly lines to meet both volume and sustainability requirements. These developments reinforce North America’s leadership position and set design benchmarks that often influence global product rollouts.

Europe Trigger Spray Bottle Market Trends - Regulation-First Adoption of Mono-Material and Premium Trigger Systems

Europe accounts for a substantial share of global demand, with Germany, the U.K., France, and Spain serving as key consumption hubs across both home care and personal care applications. Regulatory harmonization under the EU Packaging Waste Directives has effectively made recyclability and material efficiency baseline procurement requirements rather than optional differentiators. Leading multinational brands such as Unilever and Henkel have increasingly specified mono-material triggers and PCR-inclusive components across European product portfolios to align with corporate sustainability roadmaps and regional compliance standards. The region also exhibits strong demand for premium cosmetic and personal-care packaging, particularly in Western Europe, supporting higher average selling prices for fine-mist and design-enhanced trigger systems. Investment activity is concentrated around mono-material tooling, long-term PCR sourcing partnerships, and refill and reuse pilots, with several retailers testing concentrated and refillable spray solutions to reduce packaging intensity. As a result, Europe continues to influence global trigger design trends through regulation-driven innovation and premiumization.

Asia Pacific Trigger Spray Bottle Market Trends - High-Growth Consumption Fueled by Urbanization and Cost-Competitive Manufacturing

Asia Pacific is the fastest-growing regional market, driven by rising disposable incomes, rapid urbanization, and the expansion of modern retail and e-commerce platforms. China leads the region in manufacturing scale and export-oriented production of trigger spray components, supplying both domestic brands and international packaging programs. India and ASEAN markets are experiencing strong growth driven by rising hygiene awareness, expanding middle-class populations, and greater penetration of branded home-care and personal-care products. Global and regional brands such as Unilever, P&G, and Kao are expanding their trigger-based product portfolios in these markets, contributing to sustained volume growth. Although recycling infrastructure maturity varies widely across countries, a combination of emerging regulatory initiatives and voluntary brand commitments is encouraging greater adoption of PET and PCR materials. Asia Pacific’s cost-competitive manufacturing base, coupled with rising domestic consumption, positions the region as the largest contributor to incremental global volume growth through 2033, reinforcing its strategic importance in global supply chains.

Competitive Landscape

The global trigger spray bottle market is moderately fragmented, comprising global dispensing system manufacturers and regional packaging converters. Large integrated players benefit from scale, material access, and long-term contracts with multinational brand owners, while specialized suppliers compete through innovation and customization. Industry consolidation has increased concentration at the top end, enhancing scale efficiencies while raising competitive barriers.

Recent strategic activity includes acquisitions to expand geographic reach and technology portfolios, the launch of recyclable and all-plastic trigger systems, and capacity expansions in high-growth regions. These developments are reshaping supplier capabilities, strengthening sustainability credentials, and influencing long-term procurement relationships across the value chain.

Leading companies emphasize sustainability-driven product redesign, scale expansion through consolidation, and continuous innovation in ergonomics and performance. Vertical partnerships with bottle manufacturers and suppliers of recycled materials are increasingly used to deliver integrated, circular packaging solutions to brand owners.

Key Industry Developments:

- In February 2025, Tolco Corporation launched the Model 560™ Chemical Resistant Trigger Sprayer designed for aggressive chemistries (such as bleach and hydrogen peroxide), strengthening its portfolio for industrial and professional cleaning applications.

- In January 2025, Berry Global expanded its B Circular Range in the home care segment by introducing 35 new packaging items, many of which feature no metal parts and PCR content ranging from 30% to 100%, thereby reinforcing sustainable trigger and closure options for branded cleaning products.

Companies Covered in Trigger Spray Bottle Market

- AptarGroup, Inc.

- Silgan Dispensing Systems

- Berry Global Group, Inc.

- Albéa Group

- Rieke Packaging Systems

- Guala Dispensing

- Weener Plastics Group

- Canyon Corporation

- Taplast Group

- Richards Packaging Income Fund

- Sun-Rain Industrial Co., Ltd.

- Lompakko Oy

- Raepak Ltd.

- Yuyao WellPack Sprayer Co., Ltd.

- Ningbo Jinsheng Packaging Co., Ltd.

- Yuyao Bolian Sprayer Co., Ltd.

- Zhejiang Zhongyuan Packaging Co., Ltd.

- Sprayco Consumer Products

Frequently Asked Questions

The global trigger spray bottle market size is valued at approximately US$2.4 billion in 2026.

By 2033, the trigger spray bottle market is expected to reach around US$3.5 billion.

Key trends include mono-material trigger development, rising use of post-consumer recycled (PCR) plastics, growing preference for PET-based triggers to support circular packaging goals, and increasing demand for fine-mist and premium trigger systems in cosmetics and personal care.

By end-use, homecare is the leading segment, accounting for 34.7% of market share, driven by high-volume consumption of surface cleaners, glass cleaners, and multipurpose sprays across both branded and private-label product lines.

The trigger spray bottle market is projected to grow at a CAGR of 5.5% between 2026 and 2033.

Major players include AptarGroup, Inc., Silgan Dispensing Systems, Berry Global Group, Inc., Albéa Group, and Rieke Packaging Systems.