- Chipsets & Processors

- Touchscreen Controller Market

Touchscreen Controller Market Size, Trends, Share, and Growth Forecast, 2025 - 2032

Touchscreen Controller Market by Technology (Resistive, Capacitive [Projected and Surface], Surface Acoustic Wave, Infrared, Optical Imaging), Interface (Inter-Integrated Circuit, Serial Peripheral Interface, Universal Serial Bus, Universal Asynchronous Receiver/Transmitter - UART, Human Interface Device Over Universal Serial Bus), End-use, and Regional Analysis for 2025 - 2032

Touchscreen Controller Market Size and Trend Analysis

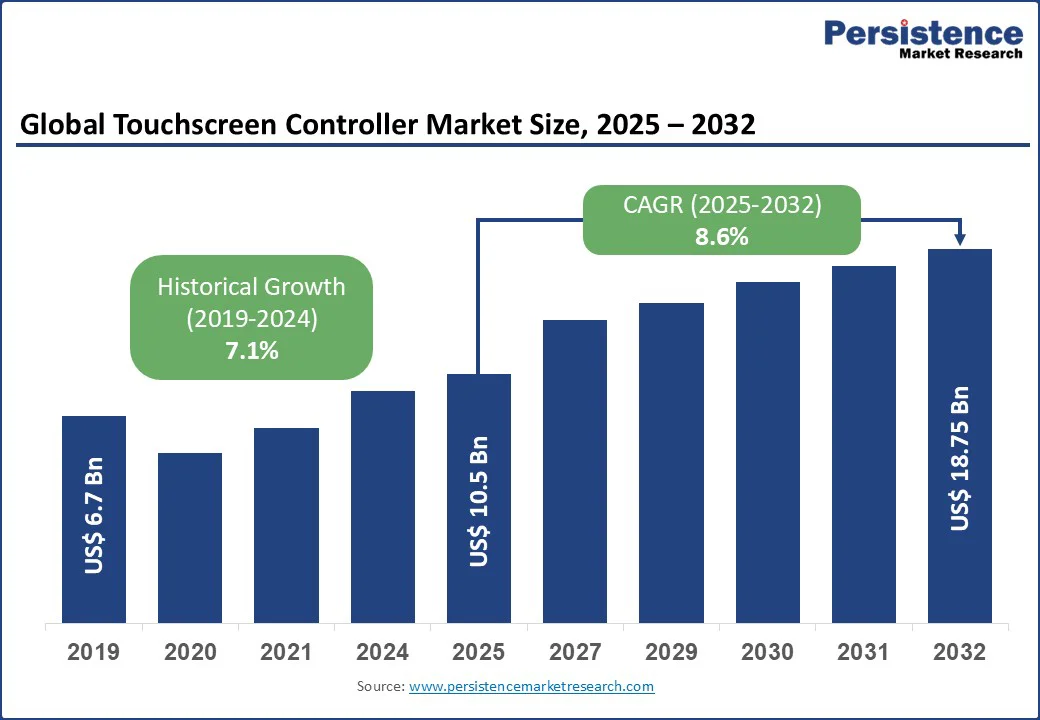

The global touchscreen controller market size is expected to reach US$10.5 billion in 2025 and increase to US$18.7 billion by 2032, growing at a CAGR of 8.6% during the forecast period from 2025 to 2032. The market is experiencing robust growth, driven by the increasing adoption of touch-enabled devices across consumer electronics, automotive, and healthcare sectors.

Key Industry Highlights

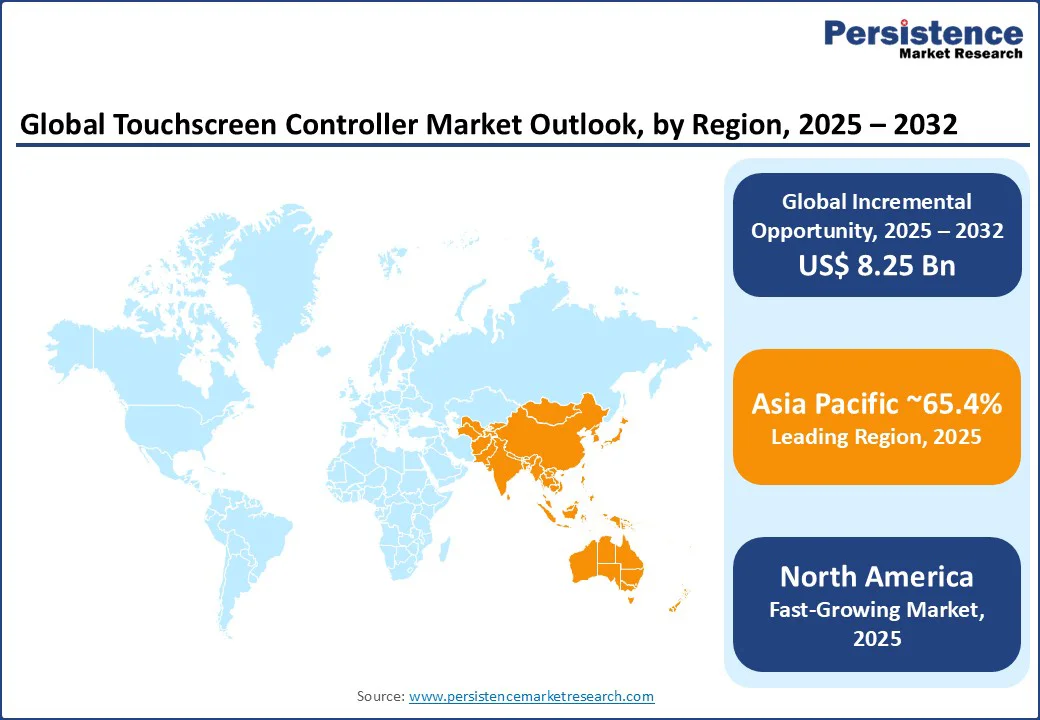

- Leading Region: Asia Pacific is likely to register a 65.4% share in 2025, driven by high production of consumer electronics and rapid industrialization in countries such as China and South Korea.

- Fastest-growing Region: North America is the fastest-growing region, fueled by strong demand in the automotive and healthcare sectors, supported by advanced technological infrastructure.

- Investment Plans: China’s 14th Five-Year Plan (2021–2025) emphasizes smart manufacturing and IoT, boosting demand for touchscreen controllers in industrial applications. China has committed to building smart factories and accelerating the integration of digital technology with the real economy.

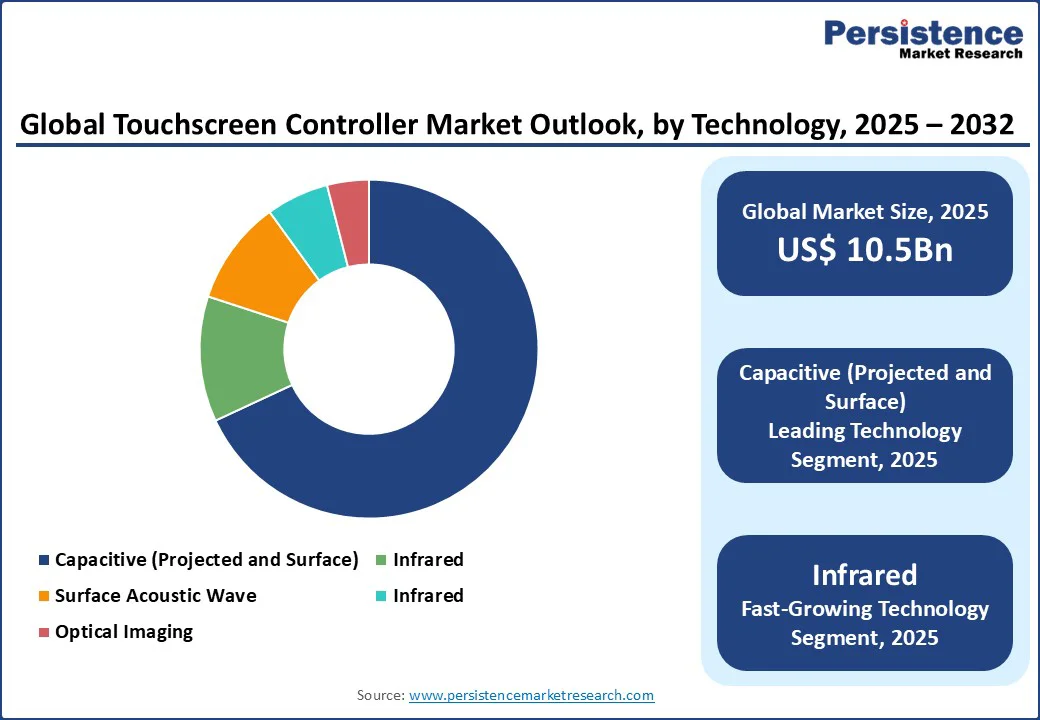

- Dominant Technology: Capacitive technology dominates with a 68.2% share in 2025, due to its responsiveness and widespread use in smartphones and tablets.

- Leading End-use: Consumer electronics contribute over 42.5% revenue share, driven by global demand for smartphones, tablets, and wearable devices.

| Key Insights | Details |

|---|---|

|

Touchscreen Controller Market Size (2025E) |

US$ 10.5Bn |

|

Market Value Forecast (2032F) |

US$ 18.7Bn |

|

Projected Growth (CAGR 2025 to 2032) |

8.6% |

|

Historical Market Growth (CAGR 2019 to 2024) |

7.1% |

Market Dynamics

Driver - Rising Adoption of Touch-Enabled Devices in Consumer Electronics

The touchscreen controller market is expanding rapidly, driven by the growing adoption of touch-enabled devices in the consumer electronics sector. Devices such as smartphones, tablets, and wearables depend on responsive capacitive touchscreen controllers known for their high accuracy and multi-touch support. The emergence of foldable smartphones and bezel-less displays has further increased the need for advanced touchscreen solutions.

Tech giants such as Samsung Electronics and Goodix Technology have reported a notable rise in controller shipments in 2024, driven by the surge in 5G smartphone production in the Asia Pacific. Government-backed digitalization efforts are also fueling market demand. For example, India’s Digital India initiative has led to the installation of over 500,000 Common Service Centers (CSCs), many of which are equipped with touchscreen kiosks for public service access.

These trends underscore how innovation, rising tech adoption, and supportive policies are key drivers of the touchscreen controller market’s growth through 2032.

Restraint - High Development Costs and Competition from Alternative Technologies

The touchscreen controller market faces challenges due to high development costs and competition from alternative input technologies. Designing advanced touchscreen controllers, particularly for capacitive displays, requires a significant investment in R&D for precision and compatibility with a diverse range of devices. The 2023 semiconductor supply chain disruptions and resulting price volatility further escalated production costs, disproportionately affecting smaller and mid-sized manufacturers.

Additionally, alternative technologies, such as voice recognition and gesture-based interfaces, are gaining traction, particularly in automotive and smart home applications. For instance, Amazon’s Alexa and Google’s gesture control systems pose competitive threats to touch-based interfaces. Moreover, the lack of standardization in some regions and concerns over touchscreen durability in industrial or outdoor environments limit broader adoption. These factors pose significant restraints, particularly in cost-sensitive markets, which could potentially slow the overall growth of the touchscreen controller industry.

Opportunity - Growing Demand in Automotive and Healthcare Sectors

The increasing integration of touch-enabled systems in the automotive and healthcare sectors presents significant opportunities for the touchscreen controller market. In automotive applications, touchscreen controllers are essential for infotainment systems, navigation displays, and advanced driver-assistance systems (ADAS). According to the IEA's Global EV Outlook 2023, the total fleet of EVs (excluding two- and three-wheelers) is expected to grow from nearly 30 million in 2022 to about 240 million in 2030 in the Stated Policies Scenario (STEPS), driving demand for robust touchscreen controllers.

In healthcare, touch-enabled medical devices, such as diagnostic monitors and surgical interfaces, rely on precise controllers to function effectively. Companies such as STMicroelectronics are developing controllers with enhanced durability for medical applications. Government incentives, such as the EU’s NextGenerationEU plan, support smart healthcare and automotive innovations, creating opportunities for manufacturers to develop advanced, reliable touchscreen controllers to meet evolving industry needs through 2032.

Category-wise Analysis

By Technology

- Capacitive touchscreen controllers hold the largest market share, approximately 68.2% in 2025, due to their high sensitivity, multi-touch support, and widespread adoption in consumer electronics, such as smartphones and tablets. Companies such as Synaptics Incorporated and Goodix Technology lead with advanced capacitive controllers, catering to demand in Asia Pacific and North America for high-resolution displays.

- Infrared touchscreen controllers are the fastest-growing segment, driven by their durability and suitability for large-format displays in retail and industrial applications. Their ability to function in harsh environments, such as dusty or wet conditions, makes them ideal for kiosks and interactive signage. Companies like NXP Semiconductors are expanding their offerings in Europe and North America.

By Interface

- The Inter-Integrated Circuit (I2C) interface dominates the touchscreen controller market, holding approximately 44.8% market share in 2025, due to its low power consumption and compatibility with a wide range of devices, particularly in consumer electronics. Companies such as Texas Instruments and Microchip Technology offer I2C-based controllers, supporting efficient communication in smartphones and wearables across the Asia Pacific and North America.

- The Universal Serial Bus (USB) interface is the fastest-growing segment, driven by its high-speed data transfer and versatility in industrial and automotive applications. USB-based controllers are increasingly adopted in touch-enabled dashboards and industrial control panels, with players such as STMicroelectronics expanding their portfolios in Europe and North America.

By End-use

- The consumer electronics sector is expected to account for over 42.5% of market revenue in 2025, driven by the global proliferation of smartphones, tablets, and wearable devices. Touchscreen controllers are critical for delivering seamless user experiences, with major players such as Samsung Electronics and Synaptics supplying controllers for high-demand markets in the Asia Pacific and North America.

- The automotive sector is the fastest-growing end-use segment, propelled by the integration of touch-enabled infotainment systems and navigation displays in electric and autonomous vehicles. Companies such as Renesas Electronics and Analog Devices are innovating with rugged controllers for automotive applications, driven by growth in North America and Europe.

Regional Insights

Asia Pacific Touchscreen Controller Market Trends

Asia Pacific is poised for a 65.4% share in 2025. This growth is largely driven by the region’s status as a global hub for consumer electronics manufacturing and rapid industrialization in key countries such as China and South Korea.

China, recognized as the world’s largest smartphone manufacturing hub, significantly drives demand for touchscreen controllers, supported by data from the China Electronics Industry Association. Meanwhile, South Korea’s thriving display industry, led by giants such as Samsung Electronics, pioneers advancements in capacitive touchscreen controller technologies. Additionally, India’s government-backed Digital India initiative has accelerated the adoption of touch-enabled kiosks and smart devices across both the public and private sectors.

The region’s strong semiconductor ecosystem and ongoing smart manufacturing initiatives further strengthen its leadership position. These factors, combined, ensure sustained growth and innovation throughout the forecast period, up to 2032.

North America Touchscreen Controller Market Trends

North America is emerging as the fastest-growing region, propelled by robust demand from the automotive and healthcare sectors. The U.S. automotive industry extensively integrates touchscreen controllers in infotainment systems and Advanced Driver Assistance Systems (ADAS), enhancing vehicle safety and user experience. Meanwhile, Canada’s expanding healthcare sector fuels the need for touch-enabled medical devices, as highlighted by the Canadian Medical Association, which emphasizes the importance of digital healthcare innovations to improve patient outcomes.

Leading companies such as Texas Instruments and Synaptics hold strong market positions in the region, leveraging extensive distribution networks to support innovations in automotive and healthcare technologies. Additionally, growing consumer preference for high-performance, durable, and responsive touchscreen controllers further strengthens North America’s foothold. Supported by advanced technological infrastructure and ongoing research and development, the region is poised to continue its rapid growth, meeting the evolving demands of both the automotive and healthcare industries well into the future.

Europe Touchscreen Controller Market Trends

Europe is the second-fastest-growing region, driven by stringent safety regulations and rising demand across the automotive and retail sectors. The European automotive industry heavily relies on touchscreen controllers for advanced infotainment systems, enhancing user experience and compliance with evolving safety standards. Key countries such as Germany and France are at the forefront of this growth, with Germany’s booming retail sector driving the adoption of touch-enabled POS terminals for seamless transactions.

Additionally, the EU’s NextGenerationEU plan supports innovation in smart healthcare and automotive technologies, boosting demand for reliable and high-performance touchscreen controllers. Industry leaders such as STMicroelectronics and NXP Semiconductors are continuously developing cutting-edge solutions to meet stringent regulatory requirements and rising consumer expectations.

Competitive Landscape

The global touchscreen controller market is highly competitive, characterized by a fragmented landscape with numerous global and regional players. Leading companies such as NXP Semiconductors, Renesas Electronics, and Samsung Electronics dominate through extensive product portfolios and global distribution networks. Regional players, such as Goodix Technology, focus on localized offerings in the Asia Pacific. Companies are investing in advanced capacitive controllers and low-power interfaces to enhance market share, driven by demand in consumer electronics and automotive sectors.

Key Industry Developments

- February 2025: Microchip Technology expanded its maXTouch M1 line by introducing the ATMXT3072M1 and ATMXT2496M1 single-chip touchscreen controllers, designed to support large, curved automotive displays up to 34 inches. These new controllers feature up to 112 configurable channels, or 162 in ultra-wide mode, and address challenges such as thin display stack-ups, higher capacitive loads, and stronger display noise found in emerging technologies such as OLEDs and MicroLEDs.

- April 2025: Synaptics announced the S3930 series, a high-performance touch controller engineered for foldable OLED displays. The S3930 series offers improved touch signal filtering and isolation using multi-frequency-region parallel sensing (MFRPS), supports larger and thinner panels, and is optimized for LTPO and polarizer-less display designs.

Companies Covered in Touchscreen Controller Market

- NXP Semiconductors

- Renesas Electronics Corporation

- Samsung Electronics Co. Ltd.

- Texas Instruments Incorporated

- Analog Devices Inc.

- STMicroelectronics

- Microchip Technology Inc.

- Cypress (Infineon Technologies AG)

- Synaptics Incorporated

- Goodix Technology Inc.

- FocalTech Systems Co., Ltd.

- MELFAS Co. Ltd.

- Others

Frequently Asked Questions

The touchscreen controller market is projected to reach US$10.5 Bn in 2025.

Growing adoption of touch-enabled devices in consumer electronics and expanding applications in automotive and healthcare are the key market drivers.

The touchscreen controller market is poised to witness a CAGR of 8.6% from 2025 to 2032.

The rising demand in the automotive and healthcare sectors is the key market opportunity.

NXP Semiconductors, Renesas Electronics, Samsung Electronics, and Synaptics Incorporated are key market players.