- Non-food Packaging

- Tobacco Packaging Market

Tobacco Packaging Market Size, Share, and Growth Forecast, 2025 - 2032

Tobacco Packaging Market By Material (Paper and Paperboard, Plastics), Packaging Type (Primary, Secondary), Product Form (Cigarette Soft Pack, Cigarette Hard Pack), Tobacco Type (Smoking Tobacco, Smokeless Tobacco), and Regional Analysis for 2025 - 2032

Tobacco Packaging Market Size and Trends Analysis

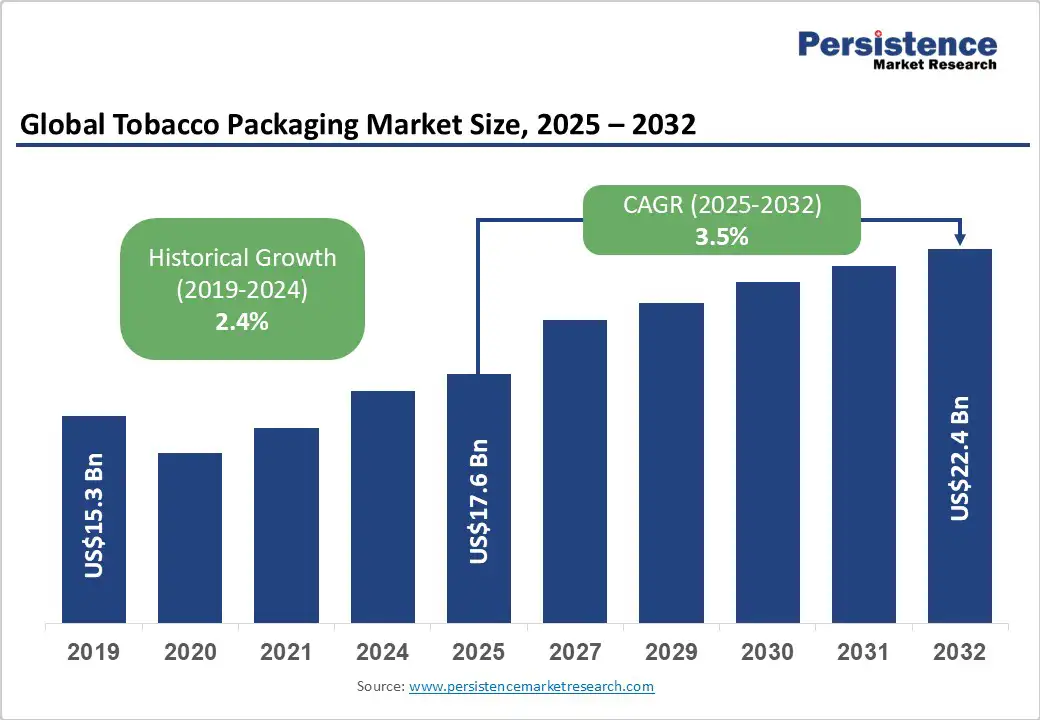

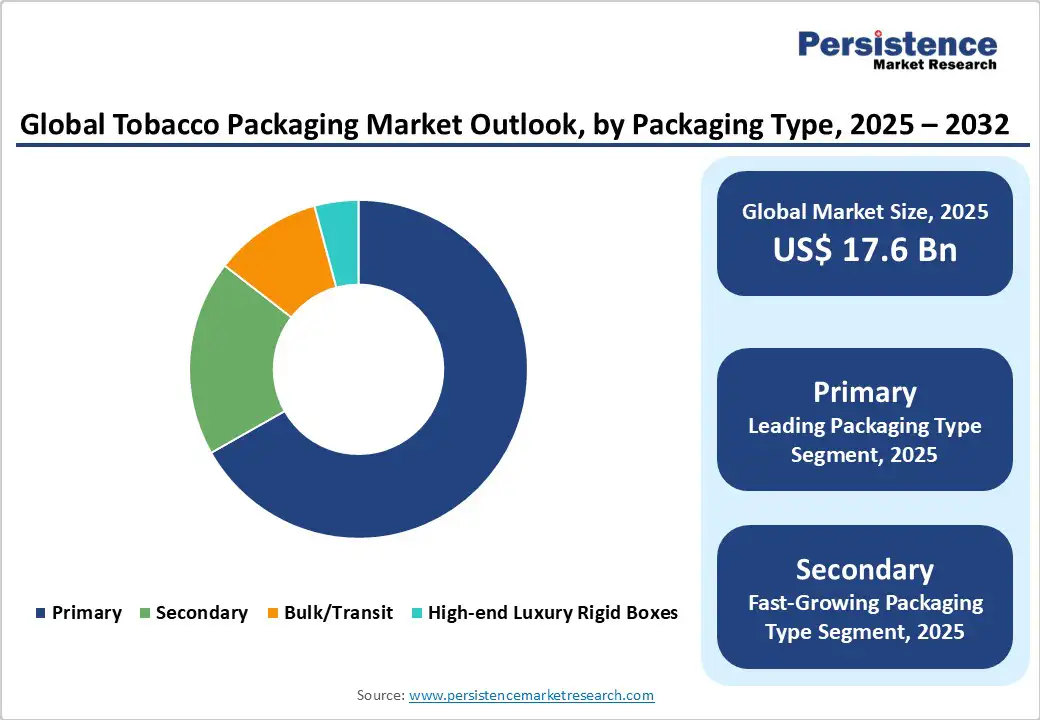

The global tobacco packaging market size is likely to be valued at US$17.6 Billion in 2025 and is estimated to reach US$22.4 Billion in 2032, growing at a CAGR of 3.5% during the forecast period 2025 - 2032, driven by the rise of plain packaging laws and mandatory graphic health warnings globally, which compels manufacturers to redesign packs frequently.

Key Industry Highlights

- Leading Material: Paper and paperboard hold nearly 84.2% of the market share in 2025, spurred by recyclability, cost-efficiency, and ease of printing health warnings.

- Dominant Packaging Type: Primary packaging, approximately 66.8% of the tobacco packaging market share in 2025, as it protects the product and displays mandatory warnings.

- Key Product Form: Soft packs recorded about 49.1% of the market share in 2025, owing to their lightweight and pocket-friendly design.

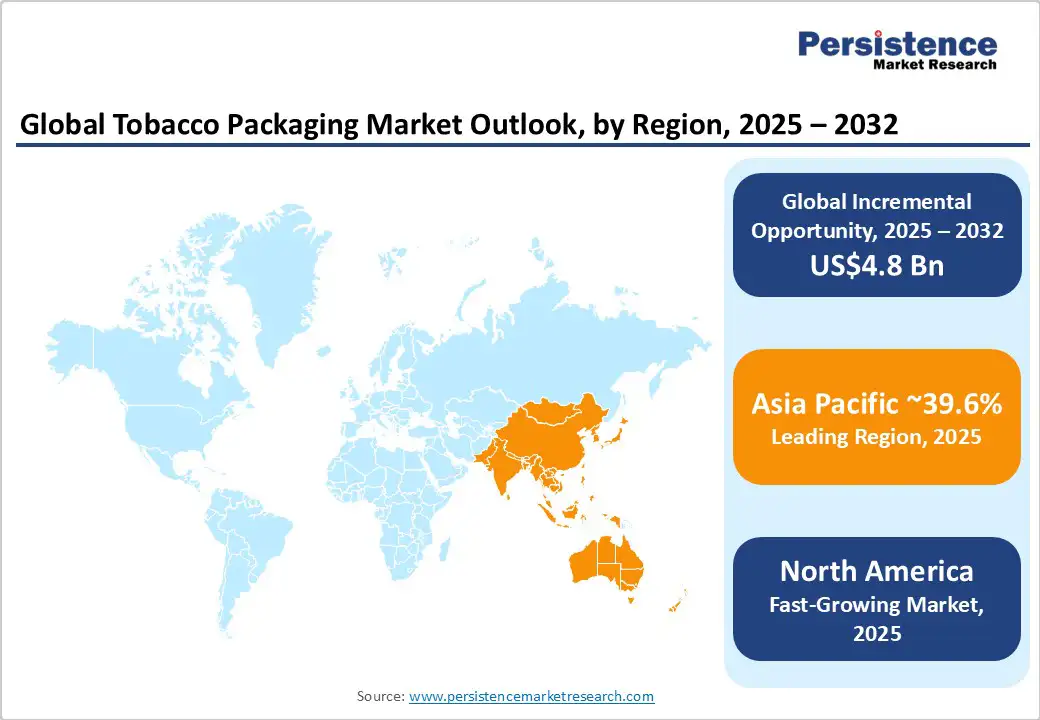

- Leading Region: Asia Pacific, with about 39.6% of the market share in 2025, boosted by high smoking prevalence and surging e-cigarette adoption.

- Fastest-growing Region: North America, augmented by the rising use of smokeless products and the ongoing adoption of tamper-proof packaging solutions.

- Government Initiative: The Government of Uruguay launched plain or standardized packaging of tobacco products due to an executive decree issued by President Tabaré Vázquez. Plain packaging has been proven to discourage people from taking up tobacco use, and is mainly effective for children and young people.

| Key Insights | Details |

|---|---|

| Tobacco Packaging Market Size (2025E) | US$17.6 Bn |

| Market Value Forecast (2032F) | US$22.4 Bn |

| Projected Growth (CAGR 2025 to 2032) | 3.5% |

| Historical Market Growth (CAGR 2019 to 2024) | 2.4% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Use of Paperboard to Improve Sustainability and Reduce Costs

Tobacco manufacturers are shifting from plastic laminates and metallic foils to paperboard packaging as sustainability regulations tighten worldwide. Paperboard delivers recyclability, low carbon footprints, and compliance with upcoming eco-design mandates such as the EU’s Packaging and Packaging Waste Regulation (PPWR), which takes effect in 2025.

Various companies, including British American Tobacco and Japan Tobacco International, have introduced recyclable paper-based cigarette packs and inner liners to replace non-recyclable film layers. Beyond environmental compliance, paperboard also provides a cost advantage as it reduces material import dependence and simplifies supply chains.

Expansion of Plain-pack Rules and Graphic Health Warnings

The spread of plain packaging and improved warning mandates is creating continuous redesign requirements across markets. Canada, the Netherlands, and Laos have recently updated packaging laws, compelling tobacco firms to modify pack layouts, typography, and warning placements. Canada’s 2023 rule mandating health warnings printed directly on individual cigarettes also triggered packaging adjustments to maintain consistency with new warning rotations.

Indonesia’s 2024 regulation requires large pictorial warnings covering 50% of pack surfaces. These frequent legislative updates compel packaging manufacturers to develop flexible production systems and compliant print technologies. Even though branding opportunities are shrinking, the recurring demand for compliant designs and rapid rollouts continues to generate steady demand for specialized packaging solutions.

Barrier Analysis - Rising Excise Taxes Curbing Tobacco Consumption

The steady increase in tobacco excise duties across key markets has directly reduced cigarette demand, limiting the requirement for new packaging volumes. Governments are using taxation as a deterrent to smoking. The U.S. and several countries in Asia Pacific have implemented annual duty hikes that push retail prices upward.

As smokers either quit or shift to illicit and low-priced alternatives, legitimate cigarette sales decline, cutting packaging procurement for legal producers. This tax-driven contraction, while effective for public health, creates a sustained headwind for tobacco packaging suppliers that depend heavily on consistent production volumes.

Standardized Packaging Laws Diminishing Branding Value

The ongoing adoption of plain and standardized packaging regulations globally has severely restricted how tobacco brands differentiate themselves. Australia, the U.K., France, and Canada now require plain packs with uniform color, font, and size, leaving minimal scope for creative design or premium finishes.

Even emerging economies such as Thailand and Laos have followed suit, eroding the role of packaging as a marketing tool. With visual branding eliminated, companies no longer invest in specialty printing, embossing, or foil effects. This shift has reduced the strategic and financial importance of packaging design in brand identity, compressing margins for suppliers that once relied on premium branding features to sustain profitability.

Opportunity Analysis - Automation-compatible Packaging for HTP and E-cig Products

The growth of Heated Tobacco Products (HTPs) and e-cigarettes is creating opportunities for packaging solutions that are compatible with high-speed automated production lines. Unlike traditional cigarettes, these products often use pods, sticks, or cartridges that require precise sealing, labeling, and protective inserts.

Manufacturers such as Philip Morris International are investing heavily in standardized, machine-ready pack formats to ensure efficiency and reduce production errors. In Japan and South Korea, where HTP adoption is high, packaging suppliers are innovating with modular cartons, easy-fill trays, and pre-lined sleeves that integrate smoothly with automated assembly systems.

Rising Adoption of Unit-level Anti-counterfeit Technology

As counterfeit tobacco and illicit vaping products proliferate, companies are integrating anti-counterfeit features directly onto individual packs. Unit-level technologies such as serialized QR codes, holographic foils, and invisible forensic inks enable traceability throughout the supply chain, helping governments and manufacturers combat fraud.

British American Tobacco recently expanded its partnership with track-and-trace platforms in Europe to include serialized codes on cigarette sticks and HTP units. Similarly, the FDA and WHO have encouraged the adoption of unit-level identifiers in high-risk markets such as Southeast Asia. These measures not only protect brand integrity but also create opportunities for packaging suppliers to deliver specialized security printing.

Category-wise Analysis

Material Insights

Paper and paperboard are predicted to hold around 84.2% of the market share in 2025 as they combine versatility, cost-efficiency, and regulatory compliance. They are easy to print on, allowing high-quality graphics and clear health warnings, which remain essential even under plain-pack laws. Also, paper-based packs are lightweight, stackable, and compatible with automated packing machines, reducing production complexity.

Plastic is expected to see steady growth due to its durability, moisture resistance, and tamper-proof capabilities. Several pouches for snus, nicotine pouches, and e-cigarette pods rely on multi-layer plastic laminates to maintain product freshness and prevent contamination. Plastic films are also used as inner liners in paperboard cartons, combining the structural strength of paper with the protective properties of plastic.

Packaging Type Insights

Primary packaging is speculated to capture nearly 66.8% of the market share in 2025 as it directly encases the product, ensuring protection, freshness, and compliance with health regulations. Cigarette packs, HTP stick cartons, and nicotine pouches all fall under primary packaging, serving as the first line of defense against moisture, contamination, and damage.

It also functions as the main platform for mandatory health warnings, plain-pack compliance, and branding, making it essential for regulatory adherence and consumer communication.

Secondary packaging is gaining impetus as manufacturers focus on bulk handling, logistics efficiency, and brand presentation beyond individual units. Outer cartons, shrink-wrapped trays, and multipacks simplify transportation, reduce damage during shipment, and facilitate automated retail stocking. With the rise of HTPs, e-cigarettes, and nicotine pouches, secondary packs are being used to group pods or sticks into ready-to-sell bundles, improving convenience for retailers and consumers.

Product Form Insights

Soft packs are anticipated to hold a share of approximately 49.1% in 2025 as they are lightweight, flexible, and cost-efficient while providing adequate protection for cigarettes and HTP sticks. Their foldable design reduces shipping volume, which lowers transportation costs and simplifies storage for manufacturers and retailers. Soft packs further allow quick printing of health warnings and branding elements where permitted, making them suitable for markets with partial branding regulations.

Pouches and sachets are poised to witness a considerable CAGR through 2032, backed by the rising popularity of nicotine pouches, snus, and other smokeless alternatives, especially in Europe and North America. These formats deliver portion-controlled, discreet consumption and extended shelf life, while maintaining product freshness through airtight, moisture-resistant laminates. Growth is particularly high in markets with strict cigarette regulations or smoking bans.

Regional Insights

Asia Pacific Tobacco Packaging Market Trends

In 2025, Asia Pacific is estimated to account for approximately 39.6% of the market share as the market is constantly shifting toward standardized and plain packaging due to strict government norms. Thailand, Singapore, and Australia have already implemented plain packaging laws that remove logos and brand colors and replace them with uniform drab-colored packs and large graphic health warnings.

Thailand became the first country in Asia Pacific to enforce plain packaging in 2019, followed by Singapore in 2020. In 2024, Laos also introduced plain cigarette packs, marking steady progress among ASEAN nations. These reforms are part of a broad movement supported by the World Health Organization to reduce tobacco appeal, especially to young consumers; however, Indonesia, Myanmar, and Vietnam are still in transition.

North America Tobacco Packaging Market Trends

In North America, tobacco packaging norms vary widely, with Canada emerging as the clear leader in tobacco control. Canada was the first country in the region to implement plain packaging for all tobacco products in 2019, removing all logos, colors, and brand imagery.

The country took another major step in August 2023 by becoming the first in the world to print health warnings directly on individual cigarettes. These rules aim to reduce smoking appeal and are part of Canada’s goal to bring national smoking rates below 5% by 2035.

The U.S. has faced years of legal and political delays in implementing graphic warning labels. The U.S. Food and Drug Administration (FDA) finalized rules in 2020 that required cigarette packs to display graphic health images covering half the front and back surfaces.

Tobacco companies filed multiple lawsuits arguing that the rule violated free speech. In March 2024, a federal appeals court upheld the regulation, but a Texas court issued another injunction in early 2025, delaying enforcement until at least 2026. For now, U.S. cigarette packs still carry text-only Surgeon General warnings, making it one of the few high-income countries without pictorial labels.

Europe Tobacco Packaging Market Trends

Europe has one of the most advanced tobacco packaging regulatory frameworks in the world, led by the European Union’s Tobacco Products Directive (TPD). Under this directive, all member states must ensure that cigarette and roll-your-own tobacco packs display combined text and pictorial health warnings covering 65% of the front and back surfaces.

Tobacco packaging must include information on quitting and product ingredients. This harmonized approach has reduced brand visibility across the EU, pushing tobacco companies to compete more on product distribution and less on visual identity.

Environmental sustainability is now changing how tobacco packaging is designed in Europe. The new Packaging and Packaging Waste Regulation (PPWR), which comes into effect in February 2025, will require all packaging to be recyclable or reusable by 2030.

This is pushing cigarette manufacturers and packaging suppliers to shift toward paper-based laminates and mono-material solutions. Companies are also removing metallic foils and plastic film layers that complicate recycling.

Competitive Landscape

The global tobacco packaging market is highly competitive, with a few global players such as Amcor, WestRock, Mondi, and CCL Industries, as well as several regional converters that serve domestic cigarette manufacturers. Most tobacco companies maintain long-term contracts with these suppliers to ensure consistent quality, compliance with changing laws, and fast design updates.

Some leading tobacco producers, including Philip Morris International and British American Tobacco, also manage parts of their packaging in-house to safeguard intellectual property and reduce turnaround times for new regulatory labels or plain packaging designs.

Key Industry Developments

- In August 2025, Belgium’s Health Minister Frank Vandenbroucke declared that the country would require cigars, cigarillos, cigarette papers, filters, tubes, and all other herbal products intended for smoking to adopt standardized green-brown packaging with uniform fonts and health warnings.

- In August 2025, Black Buffalo Inc. launched its bold new packaging graphics across its award-winning portfolio of smokeless tobacco alternative products containing pharmaceutical-grade nicotine.

Companies Covered in Tobacco Packaging Market

- Amcor plc

- Mondi Group

- International Paper Company

- Smurfit Westrock

- Sonoco Products Company

- Philip Morris International Inc.

- Innovia Films Ltd.

- Japan Tobacco International

- Siegwerk Druckfarben AG & Co. KGaA

- Treofan Film International

- ITC Limited (Packaging & Printing)

- Stora Enso Oyj

- Huhtamaki Oyj

- Shenzhen Jinjia Group Co. Ltd.

- Oji Holdings Corp.

- Jindal Poly Films Ltd.

- DS Smith plc

- SCHUR Flexibles Holding

- British American Tobacco plc

Frequently Asked Questions

The tobacco packaging market is projected to reach US$17.6 Billion in 2025.

Frequent regulatory updates and rising plain-pack mandates are the key market drivers.

The tobacco packaging market is poised to witness a CAGR of 3.5% from 2025 to 2032.

The adoption of anti-counterfeit technologies and the shift toward recyclable paperboard are the key market opportunities.

Amcor plc, Mondi Group, and International Paper Company are a few key market players.