- Power Generation, Transmission, & Distribution

- Synchronous Generator Market

Synchronous Generator Market Size, Share, and Growth Forecast, 2025 - 2032

Synchronous Generator Market by Product Type (Alternator Type, Self-Excited Type, Static Synchronous Generator), Application (Power Generation, Marine Applications, Renewable Energy Systems, Industrial Applications), End-use, and Regional Analysis for 2025 - 2032

Synchronous Generator Market Size and Trends Analysis

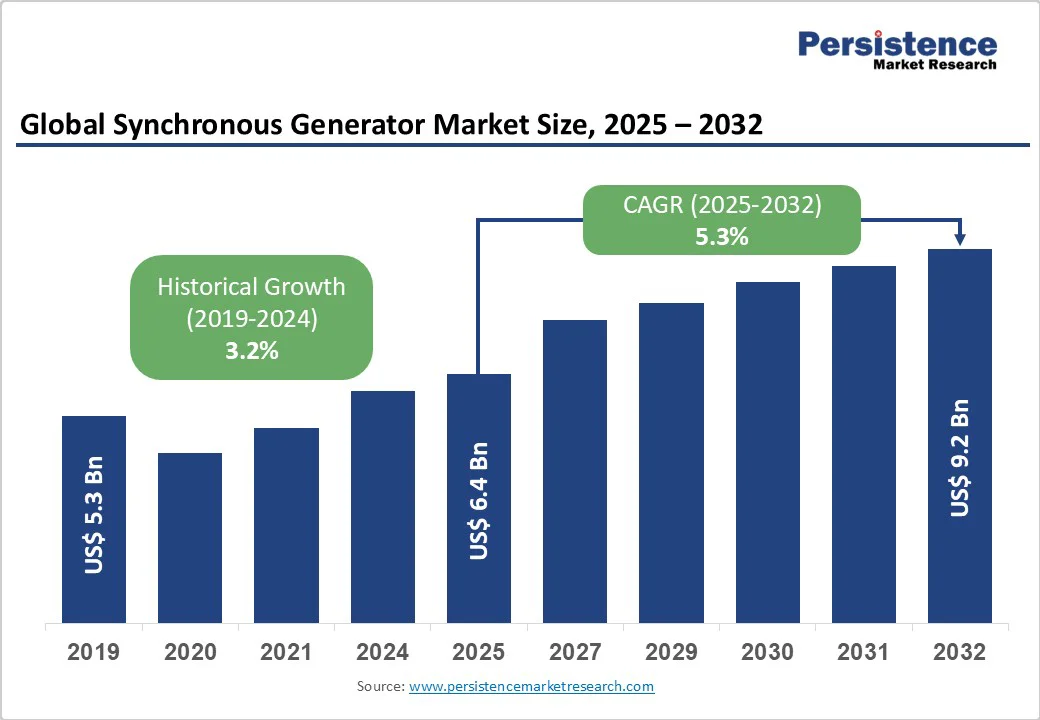

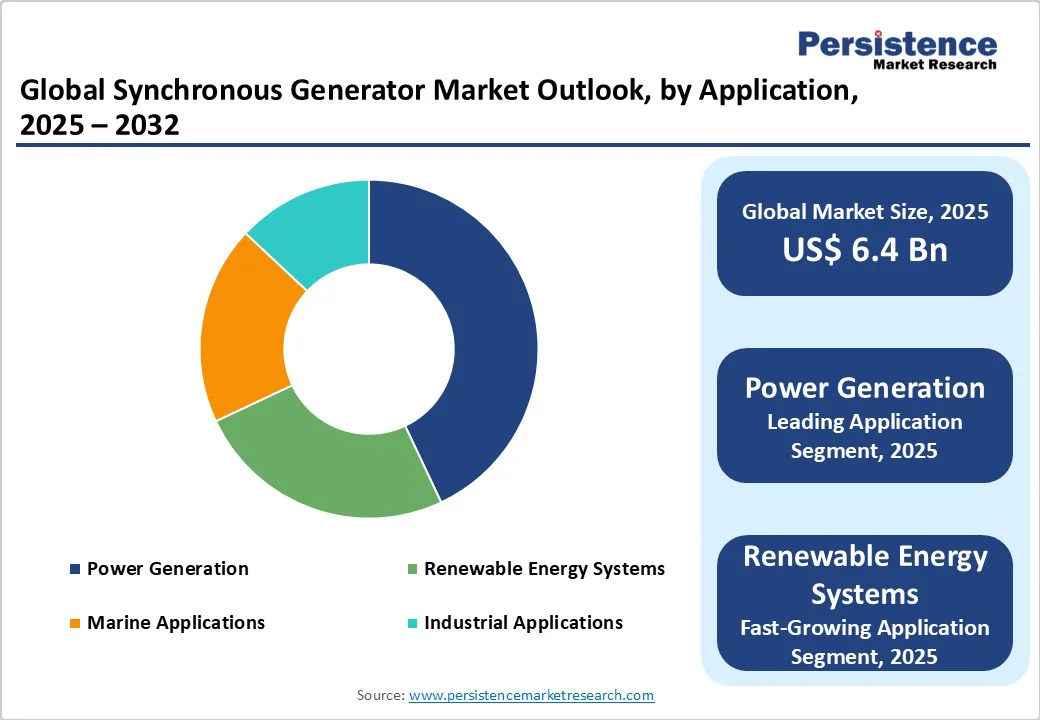

The global synchronous generator market size is likely to be valued at US$ 6.4 Bn in 2025 and is expected to reach US$ 9.2 Bn by 2032, growing at a CAGR of 5.3% during the forecast period from 2025 to 2032, driven by the increasing need for reliable power generation in renewable energy integration, rising adoption of efficient electrical systems across industries, and advancements in modular and high-efficiency technologies.

Key Industry Highlights:

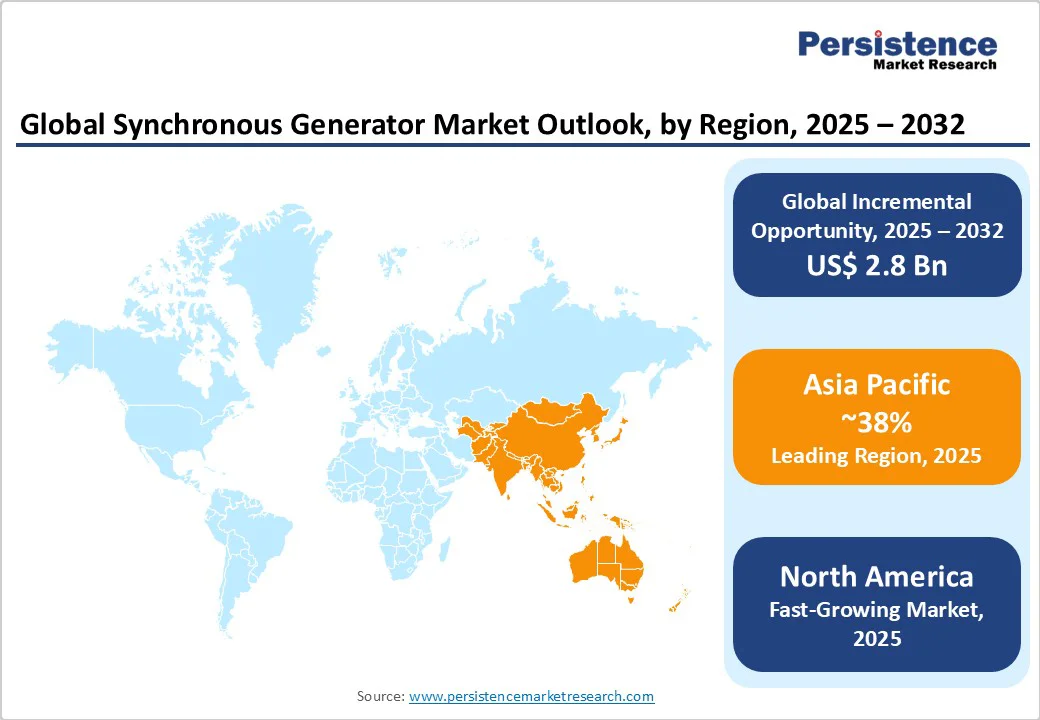

- Leading Region: Asia Pacific is likely to account for a 38% share in 2025, driven by rapid industrialization, expanding renewable energy projects, growing electricity demand, and increasing investments in power generation infrastructure across countries such as China and India.

- Fastest-growing Region: North America is emerging as the fastest-growing market in the Synchronous Generator sector, fueled by increasing adoption of smart grid technologies and modernization of aging power infrastructure.

- Dominant Product Type: Alternator Type, commanding nearly 49% share, due to its cost-effectiveness, reliable synchronization, and widespread adoption in power generation for various applications.

- Leading Application: Power Generation, accounting for over 43% revenue, driven by the need for stable electricity output and grid integration in expanding energy networks.

| Key Insights | Details |

|---|---|

| Synchronous Generator Market Size (2025E) | US$ 6.4 Bn |

| Market Value Forecast (2032F) | US$ 9.2 Bn |

| Projected Growth (CAGR 2025 to 2032) | 5.3% |

| Historical Market Growth (CAGR 2019 to 2024) | 3.2% |

Market Dynamics

Driver - Increasing Integration of Renewable Energy Sources

The increasing integration of renewable energy sources is a significant driver transforming the global energy market. This shift is fueled by advancements in energy storage solutions, smart grid technologies, and the adoption of decentralized energy systems that enable more efficient and reliable power distribution. Digital technologies, such as artificial intelligence and the Internet of Things, are further enhancing system optimization, forecasting, and operational efficiency, supporting a smoother transition to cleaner energy sources.

For instance, Octopus Energy, a UK-based renewable energy company, is expanding its AI division, Kraken, into an independent entity. Kraken supports a growing number of customers globally, including major utilities such as EDF and Tokyo Gas, and continues to scale its platform to facilitate wider renewable adoption.

In India, policies such as GST reduction and subsidies on the use of renewable energy equipment are expected to decrease costs for electricity distribution companies, encourage investment in green energy, and improve the financial health of utilities. These technological and regulatory initiatives collectively accelerate the adoption of renewable energy, demonstrating its critical role as a driver for growth and sustainability in the energy and utilities sector worldwide.

Restraint - High Initial Capital and Maintenance Costs

High initial capital investment and ongoing maintenance costs remain a key restraint in the energy and utilities market, particularly for renewable energy integration. Setting up advanced infrastructure such as solar farms, wind turbines, energy storage systems, and smart grids requires substantial upfront expenditure, which can be a barrier for smaller utilities and emerging market players.

In addition, maintaining this infrastructure demands continuous monitoring, skilled personnel, and specialized equipment, further increasing operational costs. For instance, large-scale wind and solar projects often involve long construction periods and high installation costs, which can delay returns on investment.

Deploying smart grid systems and integrating AI-based management platforms requires significant technological investments and periodic software updates. In regions such as India, while policy support exists, the high capital requirements limit the pace of adoption among smaller distributors.

This restraint affects the overall market growth by slowing deployment rates and increasing dependency on government subsidies or financing. Consequently, high upfront and maintenance costs remain a persistent challenge that market players must strategically address through financing models, partnerships, and cost-optimization technologies to sustain growth in the energy and utilities sector.

Opportunity - Advancements in Modular and Digital-Twin Enabled Generator Technologies

Advancements in modular and digital-twin enabled generator technologies present a strong opportunity for the energy and utilities market. Modular generator designs allow for scalability, faster deployment, and improved flexibility in meeting fluctuating power demands.

Instead of investing in large, fixed systems, utilities and industries can adopt modular units that can be expanded or reduced as needed, lowering risks and improving cost efficiency. This is particularly valuable in remote areas, emergency response applications, and developing regions where energy infrastructure is still evolving.

The integration of digital-twin technology is transforming generator operations. Digital twins create real-time, virtual replicas of physical assets, enabling predictive maintenance, performance monitoring, and simulation of different operating conditions. By detecting inefficiencies and predicting component failures before they occur, digital twins can significantly reduce downtime and maintenance costs.

For instance, leading generator manufacturers are increasingly embedding sensors and IoT platforms into their systems to provide data-driven insights for utilities, ensuring improved reliability and longer equipment lifespans. Modular systems and digital twins offer a pathway toward more resilient, efficient, and sustainable energy solutions. Their adoption is expected to enhance operational flexibility, reduce lifecycle costs, and accelerate innovation in the global energy and utilities sector.

Category-wise Analysis

Product Type Insights

Alternator type dominates, and is expected to account for 49% share in 2025. Its dominance stems from its cost-effectiveness, seamless synchronization with AC grids, and ease of integration with power systems for applications such as utilities and renewables. Alternator-type synchronous generators, such as those offered by ABB and VEM motors, enable precise frequency control, high efficiency, and scalability, making them a preferred choice for industries such as energy and marine.

The static synchronous generator segment is the fastest-growing, driven by industries with high-efficiency requirements, such as renewable energy and industrial automation. Static synchronous generators offer greater compactness and reduced maintenance, appealing to large enterprises with complex power needs.

The growing focus on grid modernization and variable speed drives, such as those in electric vehicle charging infrastructure, is accelerating the adoption of static systems in regions such as North America and Europe, with significant growth potential in high-stakes applications.

Application Insights

Power generation leads the synchronous generator market, holding a 43% share in 2025. The segment’s dominance is driven by the need for stable baseload power and grid synchronization in expanding energy networks, particularly in fossil-to-renewable transitions. Generator subsystems streamline the integration of prime movers, reduce harmonics, and improve operational efficiency, making them critical for providers such as Siemens and GE.

The renewable energy systems segment is the fastest-growing, fueled by the rapid growth of wind and solar installations and the need for inertia support in intermittent sources. The rise in hybrid renewable platforms and the increasing demand for grid-forming capabilities have spurred the adoption of generators in this sector. The Asia Pacific region, with its booming renewable needs, is driving rapid adoption in this segment.

End-Use Insights

Energy and utilities hold the largest market share, accounting for approximately 40% of revenue in 2025. Energy and utilities end-use allow vendors such as ABB and Robert Bosch to maintain close relationships with customers, offer tailored generators, and provide dedicated support. This end-use is particularly dominant in applications with complex requirements, such as power generation and renewables, where customized solutions are critical.

The aerospace end-use is the fastest-growing, driven by the increasing adoption of advanced electrical systems and the rise of hybrid-electric propulsion for aircraft and drones. These platforms offer seamless access to synchronous generators, enabling faster development and integration with other power services. The growing popularity of aerospace-focused electrification among governments and manufacturers is accelerating the adoption of generator solutions through this end-use, particularly in North America and Europe.

Regional Insights

North America Synchronous Generator Market Trends

North America is emerging as the fastest-growing market in the synchronous generator sector, driven by the increasing adoption of smart grid technologies and the urgent need to modernize aging power infrastructure.

The region’s electricity demand continues to rise due to rapid industrialization, the electrification of transport, and the growing reliance on digital technologies such as data centers and cloud computing. This is prompting utilities and independent power producers to invest heavily in reliable and efficient synchronous generators to ensure grid stability and uninterrupted supply.

The modernization of existing infrastructure is another key growth catalyst. Much of the power generation and transmission network in the United States and Canada is several decades old, creating significant opportunities for replacement and upgrades. Smart grid integration enhances system efficiency, enables renewable energy incorporation, and improves fault detection, all of which increase the demand for advanced synchronous generators.

Furthermore, supportive government initiatives, tax incentives for clean energy projects, and private sector investments in distributed power systems are accelerating market expansion. With a strong presence of leading manufacturers and a focus on resilient, sustainable, and digitally enabled power systems, North America is positioned to lead the synchronous generator market in the coming years.

Europe Synchronous Generator Market Trends

Europe is emerging as a significant player in the synchronous generator market, supported by strong institutional frameworks, collaborative energy programs, and ambitious decarbonization goals.

The region is undergoing a large-scale energy transition, with countries such as Germany, France, the United Kingdom, and Italy leading investments in renewable energy integration and grid modernization. Synchronous generators play a vital role in maintaining grid stability and reliability, especially as intermittent sources such as wind and solar are added to the energy mix.

The European Union’s policies, including the Green Deal and energy security strategies, are encouraging investments in advanced power generation infrastructure, creating opportunities for both domestic and international generator manufacturers. Additionally, Europe’s focus on modernizing aging transmission networks and replacing conventional systems with high-efficiency alternatives is boosting demand.

Collaborative cross-border energy projects and interconnections across member states are also contributing to a more resilient and integrated power system, where synchronous generators remain critical for frequency regulation and backup supply.

With strong regulatory support, increasing renewable energy capacity, and a commitment to carbon neutrality, Europe is positioned to be a key growth market for synchronous generators, reinforcing its role in shaping global energy transition trends.

Asia Pacific Synchronous Generator Market Trends

Asia Pacific holds a significant share of the global synchronous generator market in 2025, supported by rapid industrialization, expanding renewable energy projects, rising electricity demand, and substantial investments in power generation infrastructure. Countries such as China, India, Japan, and South Korea are at the forefront of this growth, with large-scale manufacturing, urbanization, and infrastructure development creating consistent demand for reliable power solutions.

China continues to dominate regional growth through its aggressive investments in renewable energy and smart grid modernization, while India is accelerating power sector reforms and expanding both conventional and renewable generation capacity to meet its surging energy needs. The region’s transition toward renewable integration, such as wind and hydro projects, is also driving the adoption of synchronous generators to maintain grid stability.

Additionally, government initiatives supporting energy security and rural electrification further enhance market prospects. Increasing foreign direct investment, coupled with collaborations between global generator manufacturers and regional utilities, is expanding technology adoption across the region.

With a strong focus on sustainable energy solutions and modernization of existing infrastructure, the Asia Pacific is expected to remain a pivotal hub for synchronous generator demand, reinforcing its role as a global leader in power generation growth.

Competitive Landscape

The global synchronous generator market is characterized by intense competition, regional strengths, and a mix of global and niche players. In developed regions such as North America and Europe, large firms such as ABB, Siemens Energy, and Robert Bosch dominate through scale, advanced R&D capabilities, and established partnerships with energy agencies. In the Asia Pacific, rapid industrialization and increasing demand for efficient generators are attracting significant investments from both international players, such as VEM motors and Shihlin Electric & Engineering, and regional vendors.

Companies are focusing on product innovation, modular designs, and strategic alliances to gain a competitive edge. The development of digital-twin powered and high-efficiency generators has emerged as a key differentiator, enabling faster adoption in power generation, renewables, and industrial sectors.

Strategic collaborations, acquisitions, and digital-first approaches for supply chain and marketing are further intensifying the competitive landscape. The industry exhibits a dual nature, consolidated at the top by global giants while remaining fragmented across numerous regional and niche players catering to local preferences and cost-sensitive segments.

Key Developments

- In July 2024, ABB announced a new flexible 20 MW-class modular synchronous generator, designed to provide balancing power for modern grids.

- In July 2024, VEM Motors successfully tested an 850 kW motor at its Wernigerode facility for Helen (Helsinki Energy), intended for a large heat pump plant for heating and cooling, achieving IE4 efficiency class.

Companies Covered in Synchronous Generator Market

- VEM motors

- ABB

- Mecc Alte

- Shihlin Electric & Engineering

- Techtop

- Victron Energy

- Letrika

- Sicme Motori

- Robert Bosch

- SycoTec

- Brush HMA

- Others

Frequently Asked Questions

The global synchronous generator market is projected to reach US$ 6.4 Bn in 2025.

The increasing integration of renewable energy sources is a key driver.

The synchronous generator market is poised to witness a CAGR of 5.3% from 2025 to 2032.

Advancements in modular and digital-twin enabled generator technologies are a key opportunity.

ABB, VEM motors, Mecc Alte, Robert Bosch, and Shihlin Electric & Engineering are key players.