- Automation & Robotics

- Substation Automation Market

Substation Automation Market Size, Share, and Growth Forecast, 2026 - 2033

Substation Automation Market By Component (Load Tap Changer Controllers, Others), Module Type (Intelligent Electronic Devices (IEDs), Others), Communication Channel (Optical Fiber, Ethernet, Others), and Regional Analysis for 2026 - 2033

Substation Automation Market Share and Trends Analysis

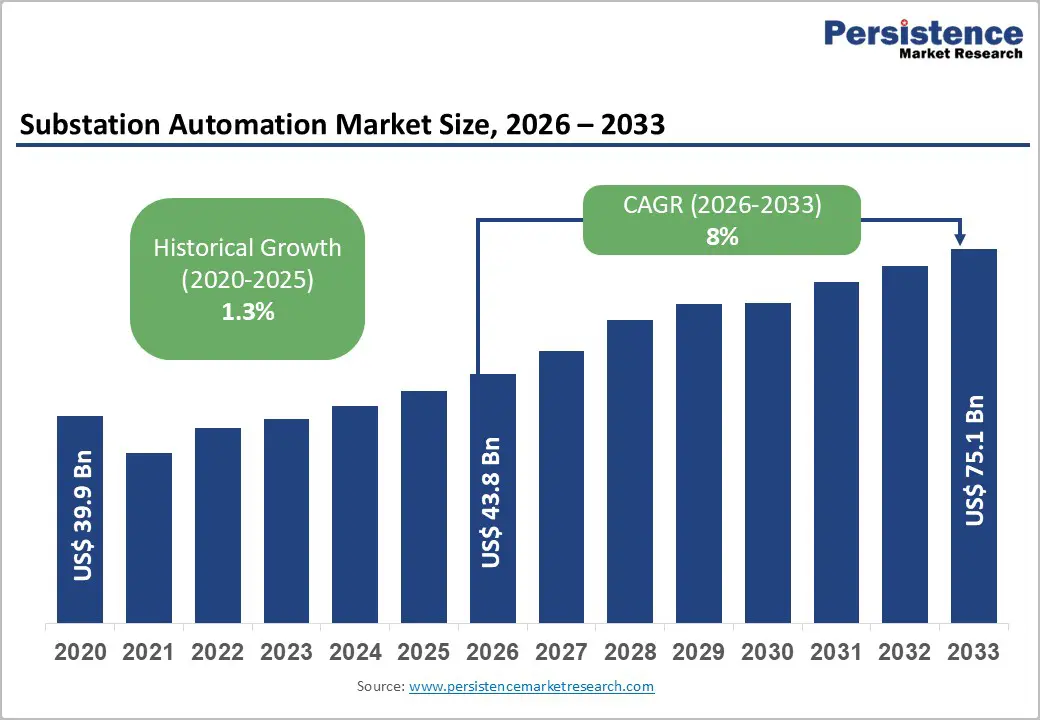

The global substation automation market size is likely to be valued at US$43.8 Billion in 2026, and is estimated to reach US$75.1 Billion by 2033, growing at a CAGR of 8% during the forecast period 2026 - 2033, driven by the growing intensity of grid modernization initiatives, substantial renewable energy integration requirements, and critical cybersecurity infrastructure investments across developed and emerging economies.

The market has seen modest growth due to delayed adoption cycles and implementation challenges, but is expected to accelerate significantly as utilities increasingly prioritize operational efficiency, grid resilience, and digital transformation in line with global decarbonization and energy security goals.

Key Industry Highlights

- Dominant Module Types: IEDs are set to command around 28.3% of the revenue share in 2026, while cybersecurity solutions are likely to grow the fastest at 11.2% CAGR through 2033, as regulatory mandates and cyberattack frequency escalate.

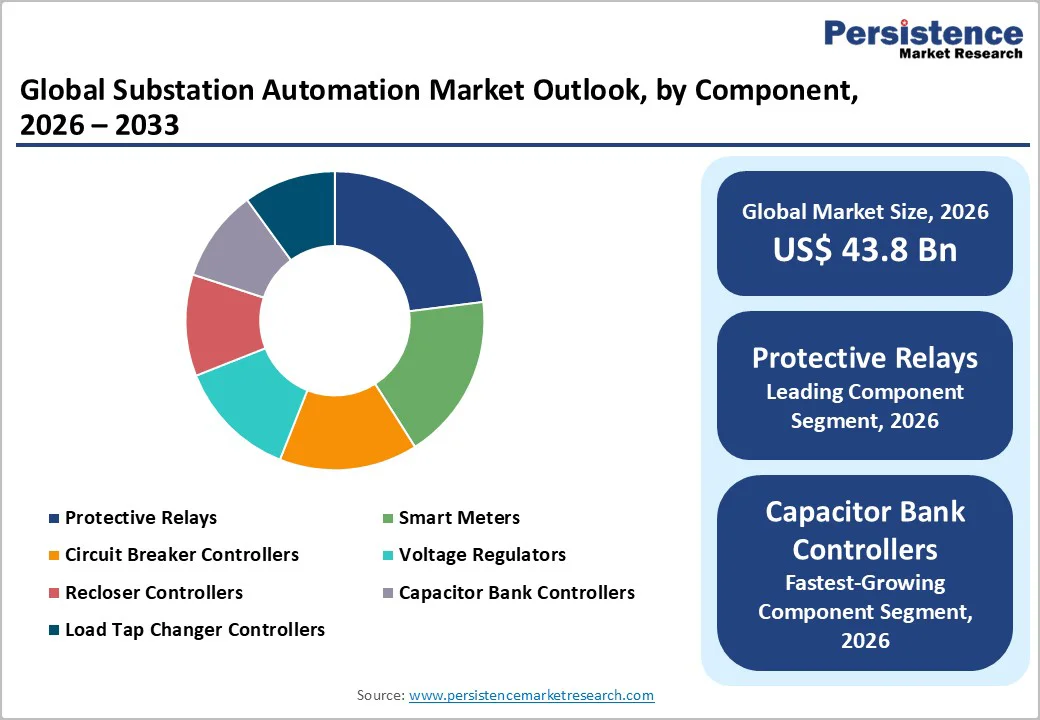

- Leading Components: Protective relays are expected to lead with 22.5% in 2026, while capacitor bank controllers are likely to be the fastest-growing during 2026 - 2033, reflecting reactive power management requirements in high-renewable-penetration grids.

- Dominant Communication Channel: Optical fiber is anticipated to lead with an estimated 35.7% share in 2026, while wireless technologies are slated to represent the fastest-growing channel segment from 2026 to 2033.

- Regional Leadership: Asia Pacific is poised to dominate with an estimated 32.5% share in 2026 and the highest CAGR through 2033, led by electrification drives in China, India, and Southeast Asian nations.

- Competitive Environment: Competitive dynamics include capacity enhancements through mergers, strategic cybersecurity partnerships, and expansion into emerging markets, targeting India and Southeast Asia.

- May 2025: ABB introduced the Relion® REC615, a versatile, modular relay that integrates protection, control, monitoring, and automation for medium-voltage secondary distribution systems, offering enhanced fault location and cybersecurity features.

| Key Insights | Details |

|---|---|

| Substation Automation Market Size (2026E) | US$43.8 Bn |

| Market Value Forecast (2033F) | US$75.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 8% |

| Historical Market Growth (CAGR 2020 to 2025) | 1.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Grid Modernization and Smart Grid Deployment as Primary Growth Catalyst

Grid modernization is the primary driver of market growth, as utilities upgrade aging infrastructure and replace legacy systems with intelligent, interconnected automation platforms. Increasing grid complexity from expanding wind and solar integration, along with stricter reliability regulations, is accelerating adoption.

Government initiatives and major funding programs in the U.S., EU, and Asia Pacific further support investments by linking renewable energy targets to advanced automation for real-time monitoring and load balancing. Modernized substations reduce losses, improve fault detection and isolation, extend equipment life, and deliver substantial operational savings and strong long-term returns.

As countries continue to pursue net-zero electricity generation goals and face increasingly variable renewable generation sources, substation automation becomes essential for millisecond-response automation and dynamic grid control.

Investments in intelligent electronic devices, communication protocols, and advanced analytics, which integrate IoT, Artificial Intelligence, and machine learning (ML), foster real-time monitoring, predictive maintenance, and enhanced grid performance. This convergence of technological innovation, regulatory push, and infrastructural necessity ensures sustained growth in the market in the coming years.

Cybersecurity Vulnerability and Interoperability Complexity

Cybersecurity threats pose a major challenge to the market as attacks on power infrastructure continue to rise. Substation control systems are prime targets, and a single coordinated breach can trigger widespread outages, financial losses, and regulatory penalties. Many utilities hesitate to adopt advanced automation without strong cybersecurity, yet most lack the expertise to secure digital substations effectively.

Implementing protections such as network segmentation, intrusion detection, and continuous monitoring significantly increases project costs. Interoperability issues, legacy system limitations, and differing regional regulations further complicate deployments, leading to delays and overruns-especially for mid-sized utilities. These factors collectively slow adoption, underscoring the need for integrated security solutions and standardized industry practices.

Increasing Rural Electrification and Grid Expansion Momentum

Emerging economies are propelling the market by investing heavily in electrification and grid modernization projects. Middle- and low-income countries of Sub-Saharan Africa, South Asia, and Southeast Asia are focusing on expanding and modernizing their power infrastructure to meet rising electricity demand and achieve universal access goals.

These efforts are supported by international financial institutions such as the World Bank and regional development banks, which provide concessional financing and technical assistance. Unlike developed markets that prioritize retrofitting, emerging markets benefit from greenfield projects that allow deployment of standardized, modern substation automation systems, reducing complexity and costs.

India exemplifies this trend with initiatives such as the Saubhagya scheme and Smart Grid Mission targeting widespread automated substation deployment across rural areas. Similar electrification drives in Vietnam, Indonesia, and the Philippines are fueling pipeline growth.

The financial frameworks often blend public development funds, climate finance, and domestic budgets, enabling greater participation from emerging technology providers alongside established global vendors. Consequently, emerging markets are expected to increase their share of the market substantially, creating additional opportunities in training, localized manufacturing, and technology partnerships that foster ecosystem expansion and sustainable growth.

Category-wise Analysis

Component Insights

Protective relays are the leading component segment, expected to hold about 22.5% of the market revenue share in 2026. They serve as critical safety devices that detect electrical faults and trigger circuit isolation to prevent damage and injury. Although around 40% of substations still use legacy electromechanical relays, the transition toward advanced microprocessor-based relays offering better sensitivity, reliability, and integration is gaining traction.

These modern relays support advanced communication protocols, remote diagnostics, and predictive maintenance. Protective relays also offer a stable cost component in substation projects, largely driven by grid modernization and equipment lifecycle replacement cycles rather than discretionary spending.

Capacitor bank controllers are likely to grow the fastest through 2033. These devices manage reactive power compensation, ensuring voltage stability and power factor correction in distribution networks. Unlike traditional fixed capacitors, modern controllers feature real-time voltage sensing and automated switching, essential for handling fluctuations from increasing renewable energy sources.

Growing renewable integration, smart grid deployment, and the need to prevent voltage regulation failures that can cause outages are fueling the adoption of capacitor bank controllers. Advanced technologies, such as ML algorithms for optimized switching, boost efficiency gains, helping utilities improve grid stability and operational reliability.

Module Type Insights

Intelligent electronic devices (IEDs) dominate the module type segment, projected to capture about 28.3% of the revenue share in 2026. IEDs are integrated microprocessor-based control units can replace multiple discrete devices by combining functions such as protective relaying, metering, communication, and data storage.

Modern IEDs feature advanced connectivity, cybersecurity protocols, and cloud integration for remote diagnostics and firmware updates. IED replacement also aligns with typical substation maintenance cycles, providing stable and predictable demand. While incremental innovations continue, the segment remains resilient to disruption due to stringent regulatory and safety standards.

Cybersecurity solutions are the fastest-growing substation automation module segment from 2026 to 2033, driven by rising regulatory requirements and growing cyberattack risks. These solutions include intrusion detection and prevention systems, anomaly detection analytics, SIEM platforms, and ICS-specific endpoint protection.

They command premium pricing due to specialized ICS expertise, strict compliance certifications, and limited competition. Growth is further accelerated by NERC CIP revisions and increasing utility awareness of operational vulnerabilities. Emerging providers such as CyberX, Nozomi Networks, and Claroty are gaining share alongside traditional IED vendors expanding their cybersecurity portfolios.

Communication Channel Insights

Optical fiber communication is poised to lead with an estimated 35.7% share in 2026, favored for its immunity to electromagnetic interference, long-distance signal integrity, and inherent cybersecurity advantages. Utilities have invested decades in building extensive fiber infrastructure, supporting mature and stable market growth.

Components such as fiber transceivers are standardized and commodity-priced, limiting vendor differentiation. The segment is expected to grow steadily, driven mainly by broader substation automation expansion and technological upgrades such as higher bandwidth and improved reliability, rather than by shifts away from this established communication medium.

Wireless communication is the fastest-growing channel in substation automation, as it enables the quick deployment of connectivity without the need for expensive fiber optic infrastructure, especially in rural and remote substations where fiber installation costs are high. Advancements in 4G/LTE and 5G provide the necessary bandwidth and low latency for real-time automation needs.

Although cybersecurity risks exist, these are increasingly mitigated through strong encryption and authentication protocols. Wireless adoption is rising rapidly in cost-sensitive emerging markets, while more established regions show slower uptake. Leading technology providers such as Cisco, Ericsson, and Nokia are expanding wireless solutions, driving competition and market growth beyond traditional fiber-based systems.

Regional Insights

North America Substation Automation Market Trends

In North America, the U.S. provides the regional growth anchor, driven by the Infrastructure Investment and Jobs Act (2021), allocating US$65 Billion for grid modernization and US$47 Billion specifically for grid resilience and cybersecurity improvements.

Federal matching requirement provisions incentivize state public utility commissions to approve rate base recovery mechanisms for substation automation investments, reducing utility capital allocation constraints. The aging U.S. electricity grid creates compelling replacement economics, with utilities recognizing that substation automation deployment extends asset operational lifespans 8-12 years and reduces catastrophic failure risks.

Canada's electricity sector is deploying comparable modernization initiatives, with provincial utilities in Ontario, British Columbia, and Alberta committing substantial capital to distribution automation and substation intelligence technologies aligned with renewable energy integration targets. Mexico offers exciting emerging market opportunities, with private utilities such as Grupo México and government-sponsored rural electrification initiatives generating substation automation demand.

The North America market is characterized by intense competitive dynamics, with established vendors such as ABB and Siemens competing aggressively alongside emerging software-centric providers offering cloud-based monitoring and analytics platforms.

Europe Substation Automation Market Trends

In Europe, the EU's climate and energy policy architecture provides uniquely powerful market drivers, with the Green Deal mandating climate neutrality by 2050 and the Renewable Energy Directive establishing 80% renewable penetration targets for 2032. Germany, leading European grid modernization efforts, has been extensively deploying distribution substations with integrated automation capabilities as part of the Energiewende initiative.

German utilities are leveraging EU standardization initiatives to procure interoperable automation solutions, reducing vendor lock-in risks and accelerating technology adoption. France is also modernizing its distribution substations under the Électricité de France plan, emphasizing enabling demand-response coordination for achieving renewable integration targets.

The Europe market is characterized by strong cybersecurity compliance with the NIS2 Directive, growing emphasis on grid resilience amid energy security concerns, and a competitive vendor landscape where European-headquartered companies gain advantages compared to non-European entities due to regulatory familiarity and established utility relationships.

The Eastern Europe market of Poland, the Czech Republic, and Romania represents emerging opportunity zones, with EU infrastructure funding mechanisms and renewable energy obligations driving grid modernization initiatives.

Asia Pacific Substation Automation Market Trends

Asia Pacific is anticipated to capture the largest share of the substation automation market, commanding an estimated 32.5% in 2026, and is projected to grow at the highest CAGR through 2033. China provides the dominant regional growth engine, with the State Grid Corporation implementing the largest substation automation deployment globally as part of the XII Five-Year Plan.

The country's smart grid modernization objectives explicitly identify substation automation as critical infrastructure enabling renewable energy integration and cross-regional transmission optimization. Government-directed technology mandates favor domestic equipment vendors such as NARI Technology and Guodian Electric, creating protectionist market dynamics that limit multinational vendor market share.

India is expected to offer the most dynamic growth opportunities, with the Smart Grid Mission targeting 120+ pilot cities and cumulative substation automation deployments estimated to be in billions through 2033.

Government policies, including the PM-KUSUM scheme, mandating rooftop solar integration across distribution networks, and the Integrated Power Development Scheme (IPDS), earmarking dedicated substation automation budgets, are driving market expansion.

The India substation automation market is attracting aggressive vendor competition from both multinational corporations and emerging Indian technology providers. Southeast Asia is also experiencing an accelerated deployment of substation automation driven by electrification initiatives, industrial manufacturing growth, and renewable energy integration mandates.

Competitive Landscape

The global substation automation market is moderately consolidated, with ABB, Siemens, Schneider Electric, and Eaton accounting for over half of revenue, supported by strong utility relationships, regulatory expertise, and integrated hardware-software platforms. These players invest heavily in advanced analytics, AI-driven maintenance, and cybersecurity.

Regional specialists such as Hitachi Energy and Mitsubishi Electric focus on niche segments, while regulatory complexity and integration challenges limit new entrants. However, digitalization is enabling software-focused firms to enter through cloud-based solutions. Market consolidation is expected to rise as major vendors acquire smaller firms and expand integration partnerships.

Key Industry Developments

- In November 2025, Huawei unveiled intelligent perimeter sensing technology for substations at CEPSI 2025, integrating AI with advanced sensors to deliver real-time, precise intrusion detection, enhance security monitoring, and strengthen substation protection while supporting smarter, more resilient grid security management.

- In September 2025, GridStrong, a New York AI platform automating grid compliance and operations, raised US$10 Million in Seed funding led by Congruent Ventures to advance product development and expand adoption among renewable and utility operators, already serving over half of major North American asset owners.

- In July 2025, Hitachi Energy secured a deal worth up to US$700 Million with E.ON to supply transformers for Germany’s grid modernization, supporting national energy security and resilience efforts and reinforcing Hitachi Energy’s leadership as demand for reliable power infrastructure accelerates.

Companies Covered in Substation Automation Market

- ABB Ltd.

- Siemens AG

- Alstom Grid

- Eaton Corporation

- Schneider Electric SE

- Hitachi Energy

- Mitsubishi Electric Corporation

- GE Grid Solutions

- Parker Hannifin Corporation

- Schweitzer Engineering Laboratories, Inc.

- NARI Technology Co., Ltd.

- Guodian Electric Co., Ltd.

- Nozomi Networks, Inc.

- Cisco Systems, Inc.

- Ericsson

Frequently Asked Questions

The global substation automation market is projected to reach US$43.8 Billion in 2026.

Growing intensity of grid modernization initiatives, substantial renewable energy integration requirements, and critical cybersecurity infrastructure investments across developed and emerging economies are driving the substation automation market.

The substation automation market is poised to witness a CAGR of 8% from 2026 to 2033.

Prioritization of operational efficiency and grid resilience by utilities and digital transformation investments aligned with global decarbonization targets and energy security mandates are key market opportunities.

ABB Ltd., Siemens AG, Alstom Grid, and Eaton Corporation are some of the key players in the substation automation market.