- Oil & Gas

- Subsea Monitoring & Controls Market

Subsea Monitoring & Controls Market Size, Share, and Growth Forecast, 2025 - 2032

Subsea Monitoring & Controls Market by System Type (Topside Control Systems, Underwater Control Systems), Component (Subsea Control Modules, Umbilicals, Umbilical Termination Assemblies (UTAs), Sensors, Master Control Stations), Water Depth (Shallow Water, Deep Water, Ultra-Deepwater), Application, and Regional Analysis for 2025 - 2032

Subsea Monitoring & Controls Market Size and Trends Analysis

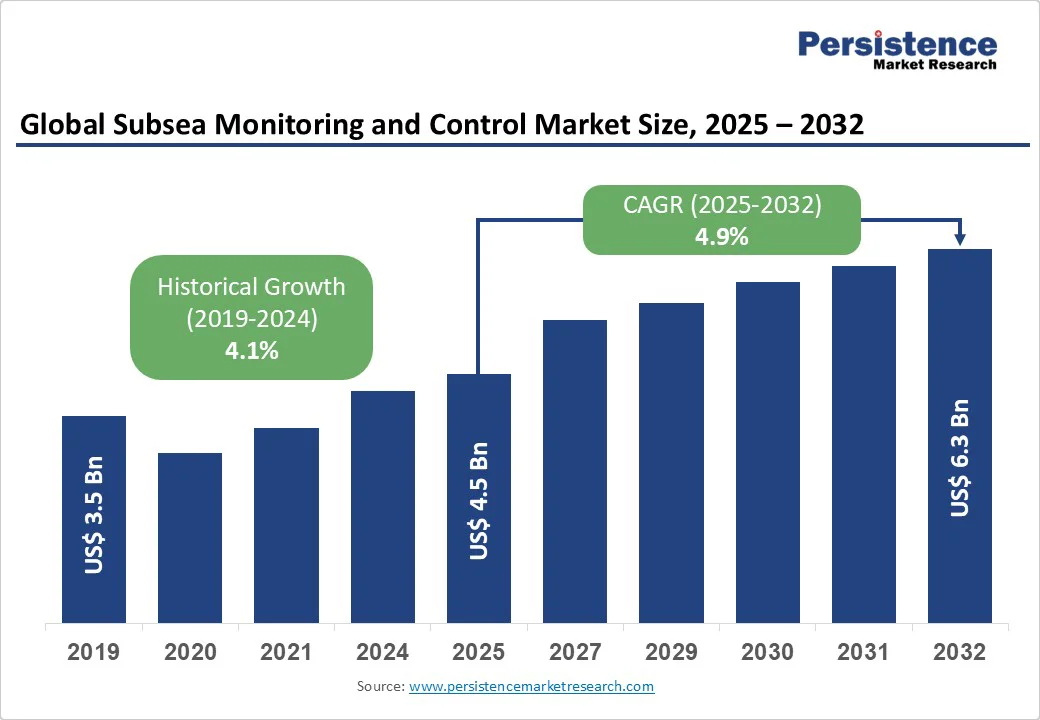

The global subsea monitoring & controls market size is likely to be valued at US$ 4.5 Bn in 2025 and is expected to grow to US$ 6.3 Bn by 2032, achieving a CAGR of 4.9% during the forecast period from 2025 to 2032.

The subsea monitoring & controls market is witnessing consistent growth, propelled by escalating demand for sophisticated offshore oil & gas exploration technologies, advancements in real-time monitoring systems, and increasing adoption in deepwater and ultra-deepwater projects.

Key Industry Highlights:

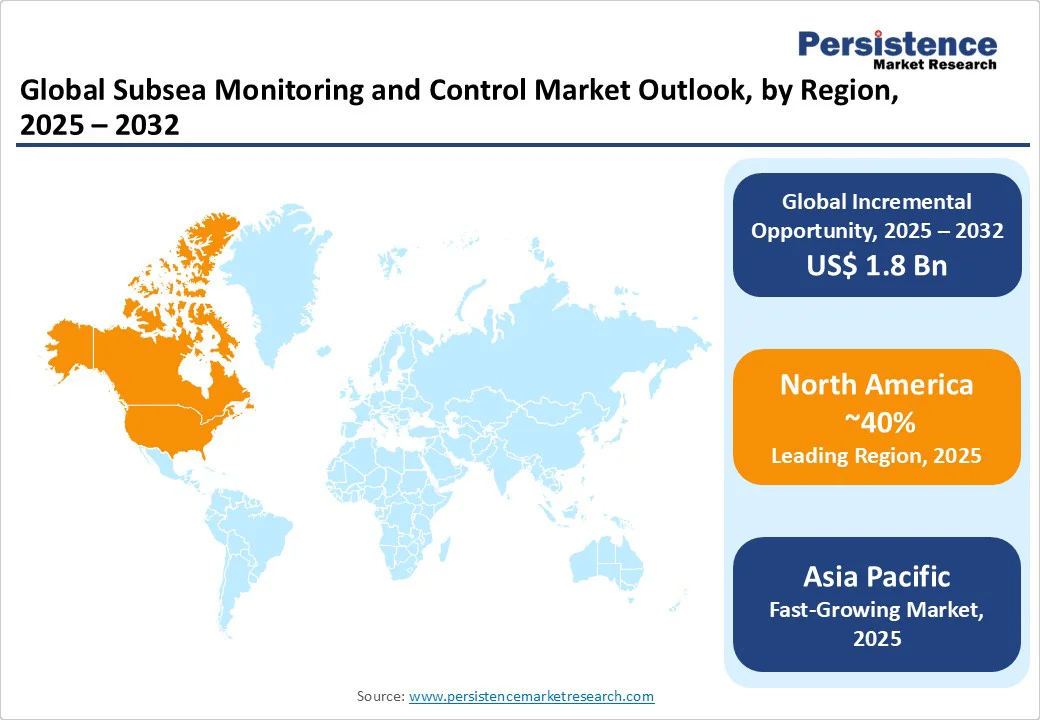

- Leading Region: North America, capturing a 33% market share in 2025, driven by extensive deepwater drilling in the Gulf of Mexico and stringent U.S. safety regulations.

- Fastest-growing Region: Asia Pacific, fueled by offshore energy investments, deepwater exploration, and renewable projects in China, India, and Australia.

- Dominant System Type: Underwater Control Systems, holding approximately 55% market share, due to their critical role in direct seafloor operations for valve and flow management.

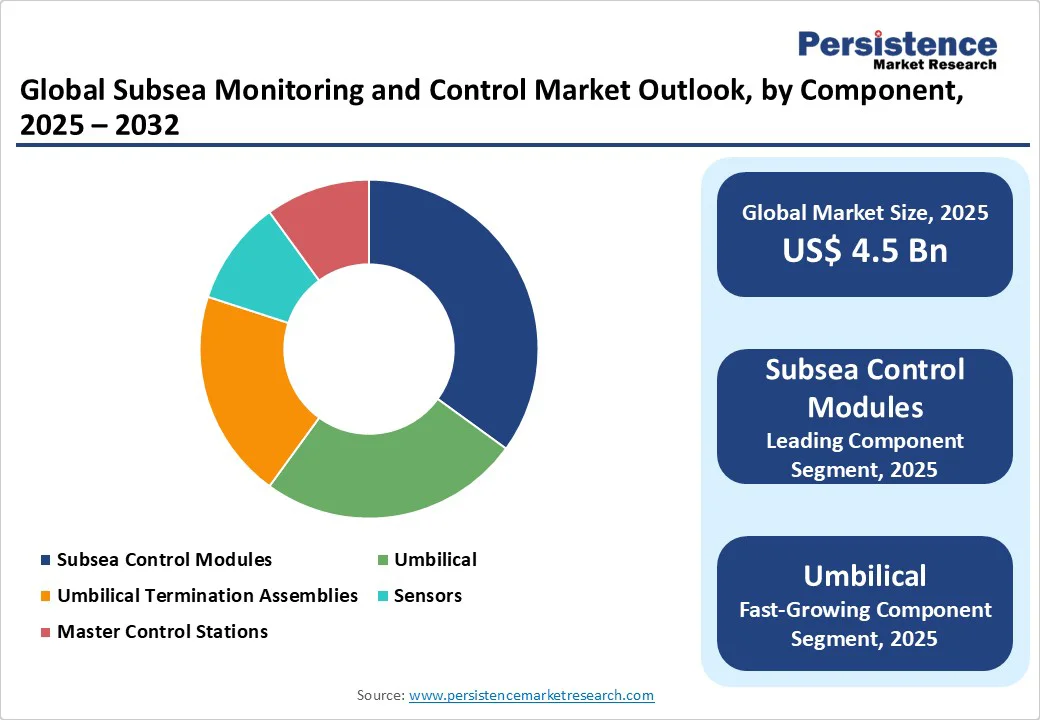

- Leading Component: Subsea Control Modules, contributing over 30% of market revenue, driven by their modularity and reliability in high-pressure subsea environments.

- Leading Application: Production, accounting for 60% of market revenue, propelled by the need for real-time wellhead monitoring in offshore fields.

| Key Insights | Details |

|---|---|

| Subsea Monitoring & Controls Market Size (2025E) | US$ 4.5 Bn |

| Market Value Forecast (2032F) | US$ 6.3 Bn |

| Projected Growth (CAGR 2025 to 2032) | 4.9% |

| Historical Market Growth (CAGR 2019 to 2024) | 4.2% |

Market Dynamics

Drivers: Intensifying Focus on Deepwater and Ultra-Deepwater Exploration and Production

The subsea monitoring & controls market is primarily driven by the intensifying focus on deepwater and ultra-deepwater exploration and production (E&P), which accounts for 40% of global offshore oil output. The U.S. Energy Information Administration (EIA) projects that deepwater production in the Gulf of Mexico will reach 2.1 Mn barrels per day in 2025, a 16% increase from 2025, necessitating advanced monitoring systems to manage high-pressure reservoirs safely.

This is fueled by the depletion of shallow-water reserves, pushing operators to deeper frontiers; global investments in deepwater E&P surged to US$ 50 Bn in 2025, with subsea monitoring & controls critical for flow assurance, leak detection, and preventing environmental incidents such as the 2010 Deepwater Horizon spill. In Asia Pacific, China’s offshore spending grew 15% year-over-year in 2025, particularly in the Bohai Bay and South China Sea, where underwater control systems enable precise valve actuation in depths exceeding 1,500 meters.

Recent trends underscore these dynamics: Baker Hughes reported an 18% revenue increase from subsea digital solutions in Q2 2025, driven by AI-enhanced sensors that improve recovery rates by 5-7% in processing applications.

Halliburton’s deployment of 500+ subsea control modules in Gulf of Mexico fields since 2025 has boosted uptime to 98%, reflecting strong ROI in production efficiency. As global oil demand stabilizes at 104 Mn barrels per day by 2030, subsea monitoring & controls remain indispensable for safe, efficient extraction from complex reserves, reinforcing the market’s growth momentum.

Restraints: High Initial Costs and Technical Complexities

High capital costs and technical complexities pose significant restraints to market. Installation of ultra-deepwater systems averages US$ 5-10 Mn per unit, deterring smaller operators in emerging markets such as Africa and Southeast Asia. Supply chain disruptions, driven by geopolitical tensions, have increased component costs by 15-20% in 2024-2025, particularly for umbilicals and sensors reliant on rare earth materials, as per industry analyses.

Harsh subsea conditions-pressures up to 15,000 psi and temperatures near 4°C-elevate failure risks, with annual rates in deepwater reaching 5%, necessitating costly remotely operated vehicle (ROV) interventions costing US$ 1-2 million per incident.

Stringent regulatory frameworks add further challenges. The U.S. Bureau of Ocean Energy Management (BOEM) imposes environmental impact assessments that delay projects by 6-12 months, while Europe’s OSPAR Convention enforces strict chemical discharge limits, raising compliance costs for control modules by 25%.

In the Asia Pacific, bureaucratic hurdles in Indonesia and Vietnam have stalled 20% of planned deepwater tie-backs in 2025. A global shortage of 85,000 subsea engineers by 2030, as projected by the Society of Underwater Technology, exacerbates integration errors, increasing downtime by 10-15%. Economic volatility, with Brent crude prices dipping to US$ 70/barrel in mid-2025, constrains E&P budgets, with majors such as ExxonMobil deferring 15% of subsea upgrades.

Opportunities: Digitalization and Renewable Energy

The subsea monitoring & controls market is ripe with opportunities, driven by digitalization and the renewable energy pivot. IoT-enabled systems could generate US$ 1.5 Bn in new revenues by 2030 through predictive analytics that reduce maintenance costs by 30%.

Offshore wind projected 234 GW capacity by 2030, demands adaptive controls for dynamic cabling, with Europe’s North Sea projects offering US$ 20 Bn in contracts. Siemens’ hybrid solutions for turbine foundations exemplify this trend. In the Asia Pacific, India’s US$7 Bn offshore wind target by 2030 drives shallow-water sensor demand, while China’s Pearl River Mouth Basin gas fields seek ultra-deepwater umbilical.

Emerging technologies such as 5G subsea communication and blockchain for data security reduce latency by 40% in remote fields; Baker Hughes’ 2025 Angola pilot achieved 15% efficiency gains.

The decommissioning market requires monitoring for safe platform removal, particularly in the U.K. North Sea, with 150 planned retirements. Partnerships, such as TechnipFMC-Aker Solutions’ AI control ventures, could unlock US$ 500 Mn in joint projects. These opportunities, blending oil & gas with renewables, position the market for robust growth beyond 2032.

Category-wise Analysis

System Type Insights

Underwater control systems dominate the system type segment, expected to hold approximately 55% share in 2025. Their leadership stems from their critical role in direct seafloor operations, managing valves, pumps, and manifolds in remote deepwater fields.

These systems ensure fail-safe shutdowns and precise flow control, eliminating surface-dependent risks. Companies such as Halliburton integrate ROV-compatible designs, enhancing reliability in production-heavy applications.

Topside control systems are the fastest-growing segment, driven by demand for centralized integration in hybrid platforms such as floating production storage and offloading (FPSO) units, projected to grow 20% by 2030. These systems leverage fiber optics for seamless data relay, supporting AI-driven interventions in Brazil’s pre-salt fields, accelerating adoption amid digitalization trends.

Component Insights

Subsea control modules lead the component segment, commanding approximately 30% share in 2025. Their dominance is due to their role as the operational core, integrating electronics for hydraulic actuation and sensor fusion in high-pressure environments.

These modules offer modularity for rapid retrofits, reducing installation time by 25%, and are favored in processing for chemical injection. TechnipFMC’s designs ensure compatibility with high-voltage umbilical, guaranteeing durability at 10,000-meter depths.

Umbilical are the fastest-growing component, propelled by the need for extended power and data transmission in ultra-deepwater. Lightweight, corrosion-resistant materials cut deployment costs by 15%, suiting fields such as Guyana’s Stabroek block. Integration with 5G for low-latency monitoring in Asia Pacific’s basins drives rapid growth.

Water Depth Insights

Deep water (500-1,500 meters) dominates the water depth segment, holding a 42% share in 2025. Its prominence is due to balancing accessibility and resource richness, hosting 60% of new subsea tie-backs, per BOEM data. Sensors and UTAs ensure flow integrity in prolific basins like the Gulf of Mexico, supporting widespread adoption.

Ultra-deepwater (>1,500 meters) is the fastest-growing, driven by untapped reserves projected to yield 9 Mn barrels per day in the near future. High-pressure module advancements address extreme conditions, with Norway’s Barents Sea investments fueling growth amid energy transitions.

Application Insights

Production dominates the application segment, with a 60% share in 2025, driven by real-time wellhead monitoring to optimize yields, supported by an 8% rise in global E&P in 2025. The deployment of master control stations (MCS) plays a pivotal role in this trend, as they facilitate intervention-free operations by remotely managing subsea equipment and reducing the need for costly and time-intensive offshore interventions.

Processing is the fastest-growing application, boosted by subsea separation technologies enhancing recovery by 10%. The demand for processing applications is further accelerated by the rise in subsea tie-back projects, where smaller satellite fields are linked to existing infrastructure to reduce capital expenditure.

Regional Insights

North America Subsea Monitoring & Controls Market Trends

North America leads the market, holds the 37% market share, driven by mature offshore infrastructure and innovation. The U.S. fuels demand through deepwater leasing in the Gulf of Mexico, with 2025 lease sales awarding 90 Mn acres, spurring US$ 15 Mn in subsea investments.

BOEM’s spill prevention mandates boost underwater system adoption, with Baker Hughes and Halliburton leading in IoT modules. Canada’s East Coast fields emphasize methane detection. Offshore fields in Newfoundland and Labrador are placing increasing emphasis on methane detection and emissions monitoring, aligning with the country’s decarbonization goals and international commitments to climate action. Subsea control systems equipped with advanced sensors are being deployed to ensure environmental compliance and strengthen operator accountability.

Europe Subsea Monitoring & Controls Market Trends

Europe is a key market, accounting for a leading market share, supported by regulatory rigor and offshore maturity. Norway, the U.K., and the Netherlands drive growth; Norway’s €5 Bn Johan Castberg budget fuels ultra-deepwater control demand for gas exports.

The U.K. market trends highlight a 4.8% growth rate, driven by the North Sea Transition Deal’s £1 Bn investment in hybrid oil-renewables systems and 150 platform decommissionings requiring precise monitoring. The country’s emphasis on operational efficiency and resilience has also accelerated the adoption of integrated subsea control modules capable of remote diagnostics and real-time flow assurance.

OSPAR’s low-emission mandates project a with Netherlands’ umbilical innovations adding momentum. By integrating emission-reduction technologies with next-generation controls, Dutch operators are adding momentum to the regional market’s push toward sustainability.

Asia Pacific Subsea Monitoring & Controls Market Trends

Asia Pacific is the fastest-growing region, with a 25% share in 2025, driven by energy diversification. China’s 14th Five-Year Plan allocates US$ 20 Bn to South China Sea deepwater, deploying sensors for territorial fields. India’s ONGC invests US$ 5 Bn in Krishna-Godavari basins, emphasizing shallow-water monitoring.

Australia’s Timor Sea LNG projects integrate topside systems. Offshore wind, with India’s 30 GW target by 2030, drives hybrid control demand, led by Kongsberg’s sensor fusion.

The push toward hybrid subsea control systems that can manage both oil and renewable installations is expected to gain traction, with Kongsberg pioneering innovations in sensor fusion platforms that unify environmental, production, and safety monitoring. The focus here lies in ensuring reliability and efficiency across long subsea tie-backs, where robust monitoring solutions minimize flow assurance challenges and guarantee consistent LNG supply.

Competitive Landscape

The subsea monitoring & controls market is highly competitive, with players focusing on digital integration and sustainability to capture market share. Key companies include TechnipFMC, Baker Hughes, Halliburton, Kongsberg Gruppen, Aker Solutions, Siemens, FMC Technologies, Proserv, Oceaneering, Cameron International, holding over 60% market share through diverse portfolios and global networks.

Businesses are investing in AI-driven predictive tools (e.g., Halliburton’s SAMS), pursue mergers for tech synergy (Aker-TechnipFMC), and developing green solutions for offshore wind, ensuring compliance and market expansion. The Aker Solutions-TechnipFMC collaboration, for example, reflects the industry’s push toward technological synergy, combining expertise in subsea equipment design, digitalization, and project execution to offer integrated solutions. Such alliances are not only expanding product capabilities but also improving cost efficiencies for operators navigating increasingly complex offshore projects.

Key Developments

- In 2024, CSignum, a leader in underwater and underground data networking, is proud to announce the launch of its latest innovation, the EM-2 wireless platform for IoT sensor data and control from above the surface to below. The EM-2 interfaces to many common underwater sensors to wirelessly communicate data from under the water to above the surface or directly on land.

- In 2025, Operating at 200kHz, the ISA200 offers an impressive measurement range exceeding 250 meters (820 feet) with exceptional accuracy to within 1 mm. Engineered for the most demanding subsea environments, the ISA200 is depth rated to 6,000 meters (19,685 feet) and delivers a precise 15.2° conical beam, providing reliable long-range performance for a wide range of applications.

Companies Covered in Subsea Monitoring & Controls Market

- TechnipFMC

- Baker Hughes

- Halliburton

- Kongsberg Gruppen

- Aker Solutions

- Siemens

- FMC Technologies

- Proserv

- Oceaneering

- Cameron International

- Others

Frequently Asked Questions

The global subsea monitoring & controls market is projected to reach US$ 4.5 Bn in 2025.

Deepwater E&P growth and IoT/AI innovations drive the market, enhancing safety and efficiency in offshore operations.

The market is expected to grow at a CAGR of 4.9% from 2025 to 2032.

Digital twins and offshore wind integration offer opportunities for predictive monitoring and renewable applications.

TechnipFMC, Baker Hughes, Halliburton, Aker Solutions, and Kongsberg Gruppen are key players.