- Telecommunications

- Subsea Cables Market

Subsea Cables Market Size, Trends, Share, and Growth Forecast, 2025 - 2032

Subsea Cables Market by Component Type (Single Core, Multi Core), Voltage (Medium Voltage, High Voltage, Extra High Voltage), End-user (Offshore Wind Power Generation, Inter-country & island connection, Offshore Oil & Gas), and Regional Analysis for 2025 - 2032

Subsea Cables Market Size and Trends Analysis

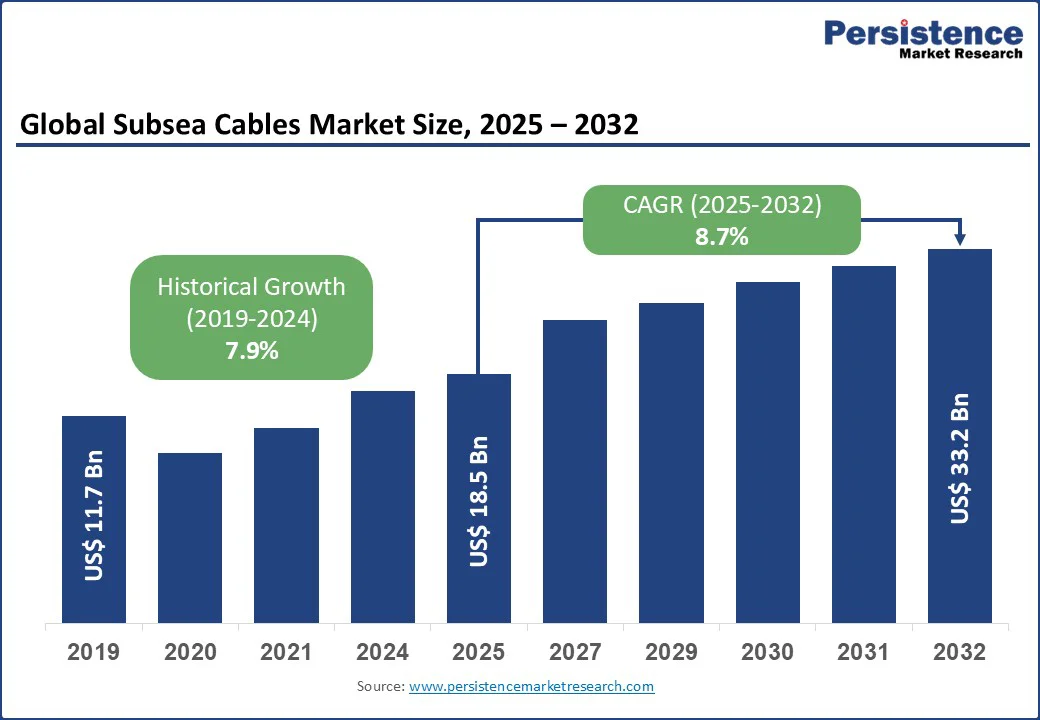

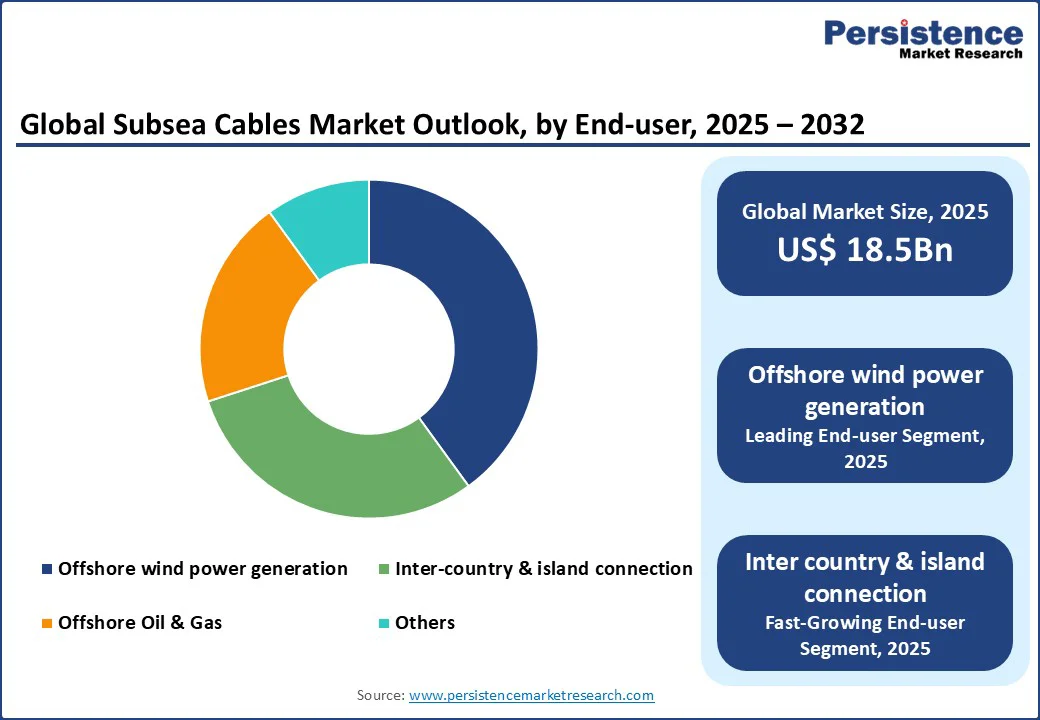

The global subsea cables market size is likely to be valued at US$18.5 Bn in 2025 and expected to reach US$33.2 Bn by 2032, registering a robust CAGR of 8.7% during the forecast period from 2025 to 2032. The industry has experienced significant growth, fueled by the increasing demand for reliable power transmission, advancements in offshore renewable energy technologies, and a global push toward sustainable energy infrastructure.

Key Industry Highlights:

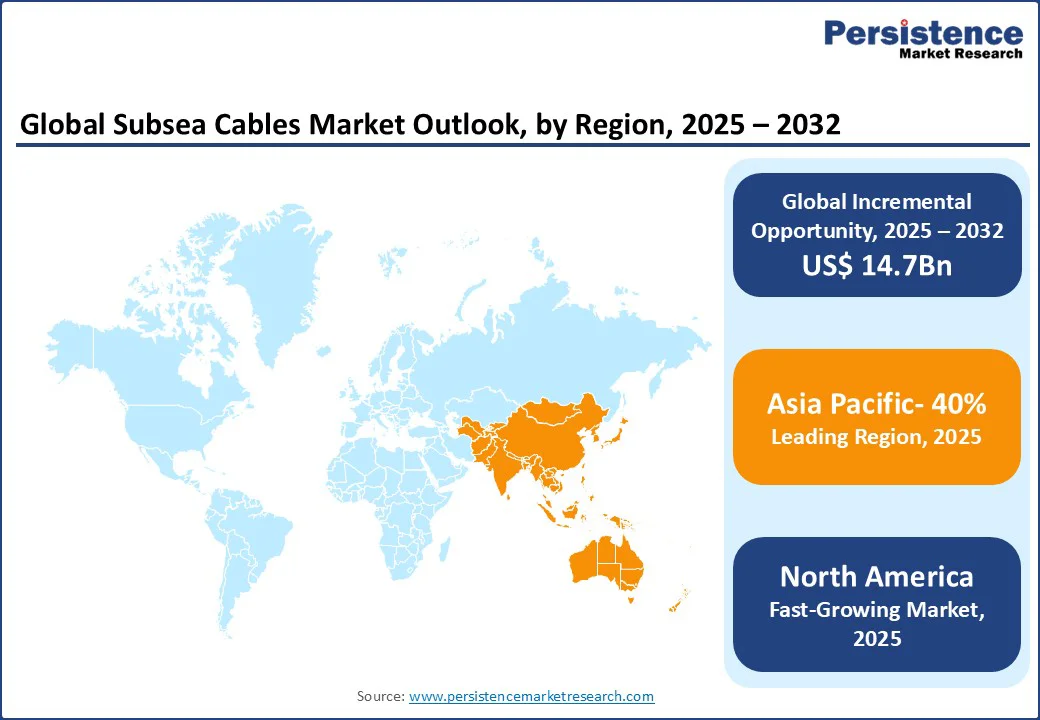

- Leading Region: Asia Pacific accounts for a 40% share in 2025, driven by massive investments in offshore wind projects, rapid industrialization, and expanding inter-country connectivity in countries such as China and Japan.

- Fastest-growing Region: The growth in North America is propelled by increasing adoption of offshore wind energy, government incentives, and growing demand for data connectivity in the United States.

- Dominant Component Type: Multi core cables account for approximately 55% share in 2025, owing to their high-capacity power transmission and reliability in harsh marine environments.

- Leading End-user: Offshore wind power generation leads with a 40% share, reflecting its critical role in supporting the global transition to renewable energy sources.

- Historical Growth: The industry recorded a CAGR of 7.9% from 2019 to 2024, driven by early adoption of offshore wind projects and inter-country connectivity initiatives.

| Key Insights | Details |

|---|---|

|

Subsea Cables Market Size (2025E) |

US$18.5 Bn |

|

Market Value Forecast (2032F) |

US$33.2 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

8.7% |

|

Historical Market Growth (CAGR 2019 to 2024) |

7.9% |

Market Dynamics

Driver - Rising Demand for Renewable Energy and Inter-Country Connectivity

The global surge in demand for renewable energy, particularly offshore wind power, is a primary driver of the subsea cables market. According to the International Energy Agency (IEA), global offshore wind capacity is expected to increase 15-fold by 2040, requiring extensive subsea cable networks to connect offshore wind farms to onshore grids. Countries such as the UK, Germany, and China are making significant investments in offshore wind projects, which have created a strong need for high-capacity subsea cables to ensure efficient and reliable power transmission. The demand for these cables is further fueled by the growing importance of inter-country and island connectivity, exemplified by projects such as the North Sea Link connecting Norway and the UK.

In Europe, long-term energy strategies include several large-scale subsea cable initiatives aimed at strengthening regional energy security and supporting the transition toward renewable power sources. Beyond energy, subsea cables are also playing a critical role in global digital infrastructure. The rapid expansion of data centers and the continuous growth of digital services require robust and high-speed communication systems. Major technology companies, including Google and Microsoft, are actively investing in advanced transoceanic cable networks to ensure uninterrupted connectivity and meet the surging global demand for data transmission.

Restraint - High Installation and Maintenance Costs

The industry encounters notable challenges primarily due to the substantial costs tied to installation and maintenance. Deploying cables in deep-sea environments demands specialized vessels, advanced technology, and highly skilled professionals, resulting in heavy capital investments. The financial burden does not end with installation; maintenance expenses remain equally significant. Repairs in harsh marine conditions require intricate operations, extended downtime, and considerable resources, which can disrupt energy transmission and communication reliability.

Another hurdle is the shortage of trained personnel capable of handling the complexities of subsea cable projects. This issue is particularly pronounced in developing regions, where technical expertise and infrastructure are often limited. Such constraints create barriers for smaller companies that lack the financial strength to compete with larger players. Collectively, these challenges increase entry barriers, slow market expansion in cost-sensitive regions, and highlight the need for innovation, cost optimization, and capacity building within the subsea cable industry.

Opportunity - Advancements in Cable Technology and Sustainable Energy Solutions

Technological innovations in subsea cable design are unlocking strong growth opportunities for the industry. The adoption of high-voltage direct current (HVDC) cables is gaining momentum, as these systems reduce transmission losses over long distances, making them ideal for large-scale offshore wind projects and intercontinental power connections. Projects such as the Viking Link, which connects the UK and Denmark, highlight the efficiency of HVDC technology in enabling reliable cross-border energy transfer.

At the same time, increasing global emphasis on sustainability is encouraging the development of recyclable and eco-friendly insulation materials, ensuring that subsea cables align with stricter environmental standards while minimizing ecological impact. Beyond renewable energy, the expansion of offshore oil and gas exploration in regions such as the Middle East and Latin America is further driving demand, as subsea cables are essential for powering offshore platforms and supporting critical operations. These advancements broaden the scope of subsea cable applications and reinforce their role in future energy and communication networks.

Segmental Insights

Component Type Insights

By component, the market is segmented into single core and multi core cables. Multi Core cables dominate, holding approximately 55% share in 2025, due to their ability to handle high-capacity power transmission and enhanced reliability in challenging marine environments. Multi core cables are widely used in offshore wind farms and inter-country connections, as they can transmit multiple power streams simultaneously, reducing the need for multiple cable installations. Their robust design ensures durability against underwater currents and pressure, making them ideal for long-distance energy transmission.

Single Core cables are the fastest-growing segment, driven by their increasing adoption in smaller-scale offshore projects and island connectivity initiatives. Single Core cables are preferred for their simplicity and lower installation costs in shallow waters, making them suitable for emerging markets and smaller offshore wind installations.

Voltage Insights

The subsea cables market is segmented into medium voltage, high voltage, and extra high voltage. High Voltage cables lead with a 50% share in 2025, driven by their widespread use in large-scale offshore wind projects and long-distance power transmission. High Voltage cables, typically operating between 66 kV and 220 kV, offer a balance of efficiency and cost-effectiveness, making them the preferred choice for connecting offshore wind farms to onshore grids.

Extra high voltage cables represent the fastest-growing market segment, fueled by their role in ultra-long-distance and intercontinental power transmission. Projects such as the EuroAsia interconnector highlight their importance, as these cables enable efficient, high-capacity energy transfer with minimal losses, strengthening global grid connectivity and cross-border energy security.

End-user Insights

By end-user, the market is divided into offshore wind power generation, inter-country and island connection, and offshore oil & gas. Offshore wind power generation leads with a 40% share in 2025, driven by the global shift toward renewable energy and the rapid expansion of offshore wind farms. Subsea cables are essential for transmitting electricity from offshore turbines to mainland grids, supporting projects such as the Hornsea Project in the UK, one of the world’s largest offshore wind farms.

Inter country & island connection is the fastest-growing application, as countries increasingly invest in cross-border energy sharing and island electrification. Projects such as the Australia-Asia PowerLink, which aims to deliver solar energy from Australia to Singapore via subsea cables, highlight the growing demand for reliable connectivity solutions in this segment.

Regional Insights

North America Subsea Cables Market Trends

North America is emerging as the fastest-growing region with the United States playing a central role. The country is experiencing strong momentum in offshore wind development, particularly along the East Coast, where large-scale projects such as Vineyard Wind are creating significant demand for subsea power cables. Federal incentives, coupled with state-level renewable energy mandates, are accelerating the transition toward clean energy, reinforcing the need for robust transmission infrastructure.

Beyond energy, the surge in demand for global data connectivity is driving massive investments in subsea communication cables. Leading technology companies, including Google, Amazon, and Microsoft, are expanding transoceanic cable networks to ensure seamless connectivity and support growing digital services.

Europe Subsea Cables Market Trends

Europe commands a substantial share of the industry, with strong contributions from the UK, Germany, and Denmark. The UK leads through its ambitious offshore wind expansion, which requires extensive subsea transmission networks to support large-scale renewable integration. Germany’s energy transition policy, centered on shifting from fossil fuels to renewable sources, has intensified investments in subsea infrastructure, particularly for offshore wind projects and cross-border connections such as NordLink with Norway.

Denmark, recognized as a pioneer in offshore wind, uses subsea cables not only to strengthen its domestic energy supply but also to export surplus clean energy to neighboring countries, enhancing regional cooperation. In addition, stringent European Union regulations targeting carbon reduction and energy security are reinforcing the demand for advanced subsea cable systems. Collectively, these initiatives position Europe as a critical hub for innovation and large-scale deployment in the subsea cables market.

Asia Pacific Subsea Cables Market Trends

Asia Pacific dominates the global subsea cables market, expected to account for 40% share in 2025, driven by countries such as China, Japan, and Australia. China leads the region with substantial investments in offshore wind, supported by large-scale projects such as the Jiangsu Offshore Wind Farm, which drive demand for advanced subsea cable networks. Japan is also a key contributor, with its renewable energy transition accelerated by the Fukushima disaster and the push to reduce dependence on nuclear power. This shift increases the need for subsea cables to connect offshore wind farms and island-based power grids.

Australia is emerging as an important player in renewable energy exports, highlighted by initiatives such as the Australia-Asia PowerLink, which enhance regional interconnectivity. Additionally, rapid industrialization, strong government incentives, and the requirement for reliable electricity transmission across island nations such as Indonesia are further strengthening Asia Pacific’s position in the industry. These combined efforts underscore the region’s role as a driving force in both renewable energy growth and subsea communication infrastructure.

Competitive Landscape

The global subsea cables market is highly competitive, with global and regional players competing through innovation, competitive pricing, and reliability. The rise of sustainable cable materials and high-capacity HVDC systems intensifies competition, as companies strive to meet the diverse needs of energy and connectivity sectors. Strategic partnerships, mergers, and certifications for environmental and safety standards are key differentiators in this dynamic market.

Key Developments

- August 2025: The U.S. Federal Communications Commission (FCC) approved updates to its regulations on subsea communications cables. The changes aim to streamline approval processes, introduce more protections for submarine cable infrastructure, and help accelerate the deployment of new systems.

- July 2025: NEC Corporation, with a consortium led by Singtel, struck a contract to build the AUG East submarine cable system spanning Singapore to Japan (brackets of intervening countries), aiming for high-capacity connectivity and completion by late 2029.

Companies Covered in Subsea Cables Market

- ALE USA Inc.

- SubCom, LLC

- NEC Corporation

- Prysmian S.p.A

- Nexans

- Google LLC

- Amazon.com, Inc.

- Microsoft

Frequently Asked Questions

The subsea cables market is projected to reach US$18.5 Bn in 2025.

Rising demand for renewable energy, technological advancements in subsea cable design, and government initiatives for cross-border energy connectivity are key drivers.

The subsea cables market is poised to witness a CAGR of 8.7% from 2025 to 2032.

Innovations in high-voltage direct current (HVDC) cables and sustainable materials, along with expanding offshore energy projects, present significant growth opportunities.

Prysmian S.p.A, Nexans, SubCom, LLC, and NEC Corporation are among the leading players, known for their advanced subsea cable solutions.