- Metals & Minerals

- Stainless Steel Forgings Market

Stainless Steel Forgings Market Size, Share, and Growth Forecast, 2026 – 2033

Stainless Steel Forgings Market by Product Type (Castings, Hot/Cold Forged Parts, Sintered Parts), Process (Open Die Forging, Closed Die Forging, Impression Die Forging, Extrusion, Others), Application (Automotive, Aerospace, Industrial, Building & Construction, Consumer Goods, Aviation, Others), and Regional Analysis for 2026-2033

Stainless Steel Forgings Market Share and Trends Analysis

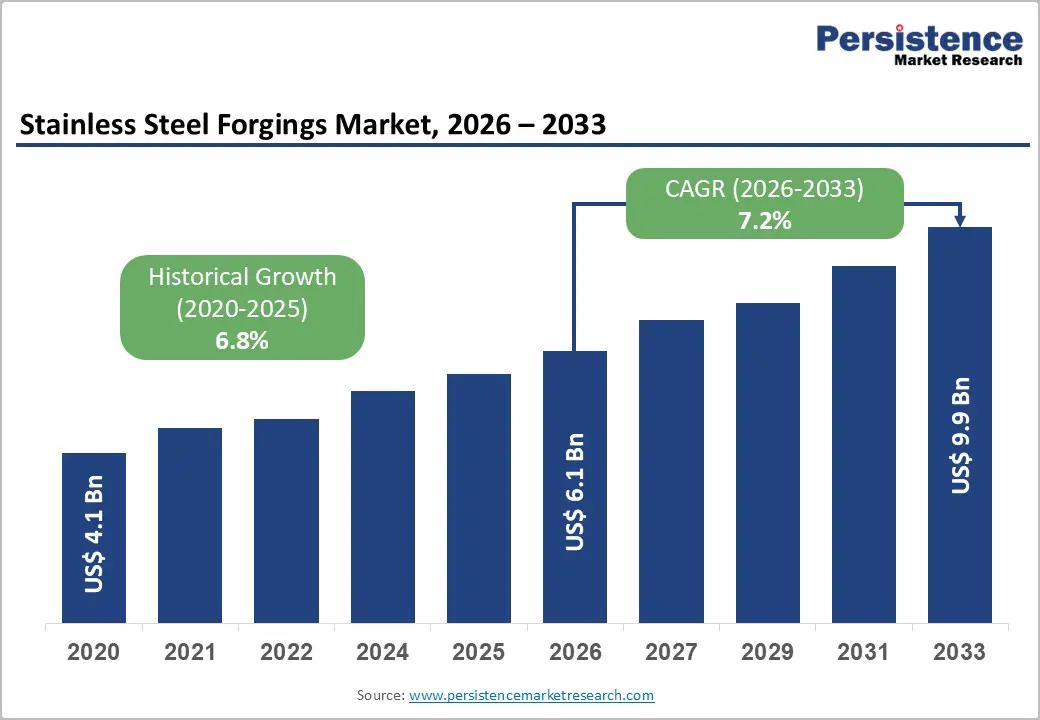

The global stainless steel forgings market size is likely to be valued at US$ 6.1 billion in 2026, and is projected to reach US$ 9.9 billion by 2033, growing at a CAGR of 7.2% during the forecast period 2026−2033. The market demonstrates a structurally resilient growth outlook, supported by expanding industrialization, infrastructure renewal, and long-term capital expenditure cycles across transportation, energy, and process industries. Demand acceleration originates from increasing requirements for high-strength, corrosion-resistant components in safety-critical and high-temperature operating environments, which directly elevates adoption of forged stainless steel over cast or fabricated alternatives. Industrial automation, electrification of mobility platforms, and higher efficiency thresholds across manufacturing systems reinforce preference for precision-forged components with superior fatigue resistance and dimensional stability. Regulatory tightening around emissions, safety, and lifecycle performance indirectly stimulates stainless steel forgings usage, as compliance frameworks favor durable materials with predictable mechanical behavior. Supply-side modernization, including digital forging presses, simulation-led die design, and controlled metallurgy, improves yield efficiency and consistency, enabling broader application penetration.

Key Industry Highlights

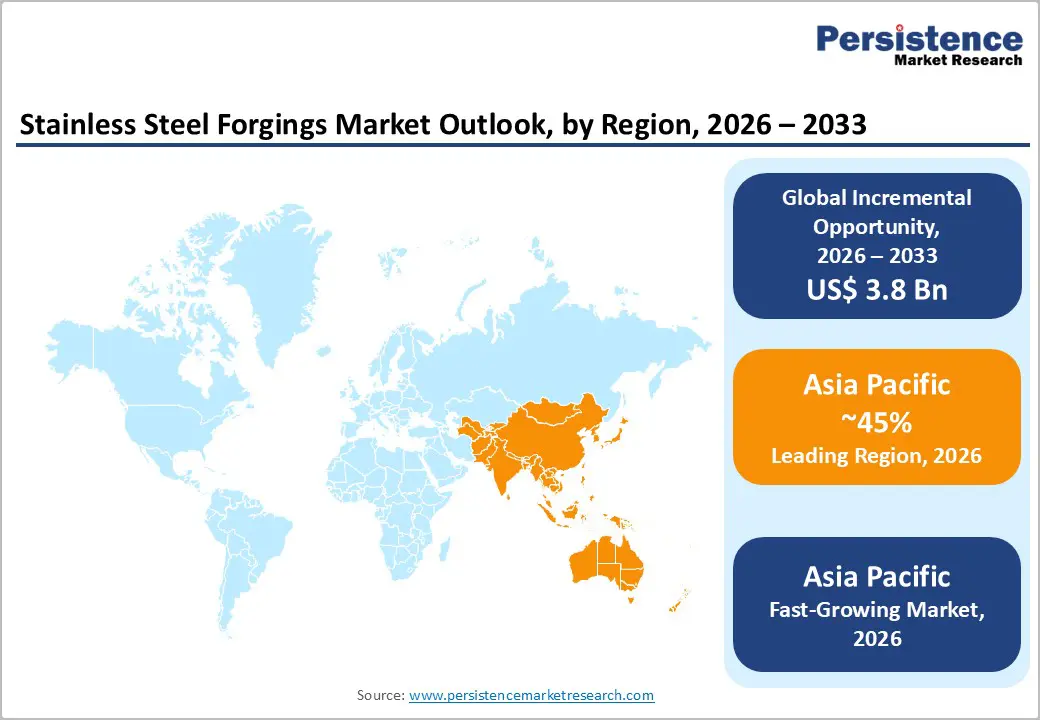

- Dominant Region: Asia Pacific is expected to dominate with around 45% market share in 2026, fueled by entrenched presence of concentrated manufacturing clusters and integrated supply chains.

- Fastest-growing Market: Asia Pacific is forecasted to be the fastest-growing market from 2026 to 2033, supported by industrial modernization and surging demand for high-performance components in electric vehicle (EV), renewable energy, and aerospace applications.

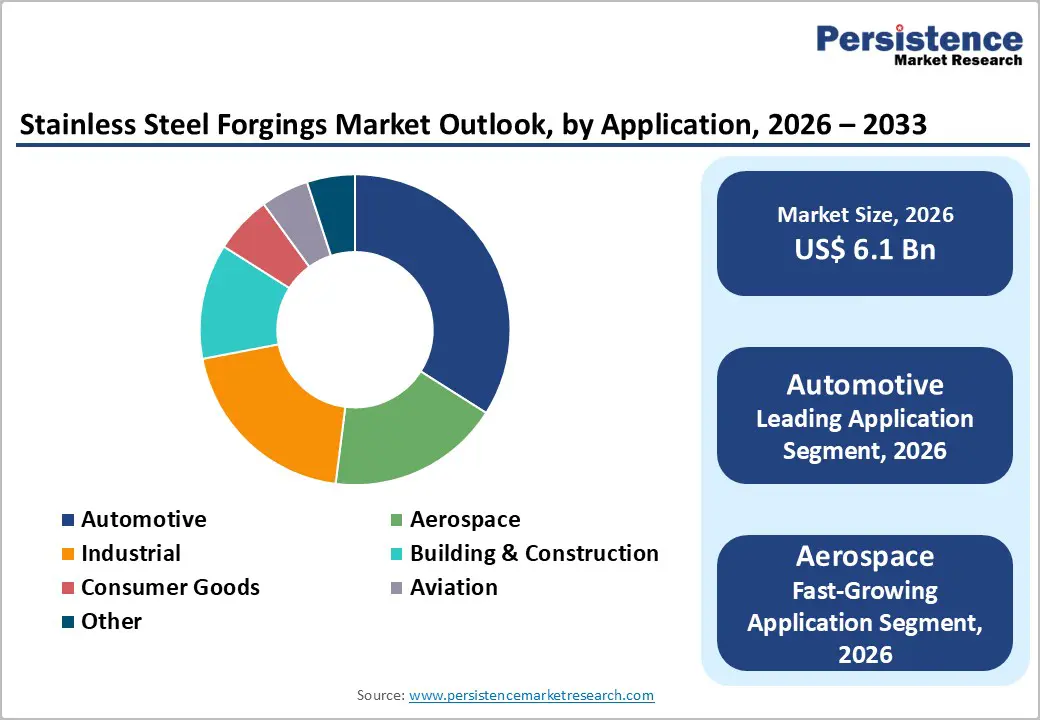

- Leading Application: Automotive applications are likely to lead with a 34% revenue share in 2026, underpinned by sustained vehicle production, electrification, and strict emission norms.

- Fastest-growing Application: Aerospace applications are anticipated to be the fastest-growing through 2033, driven by fleet modernization, lightweight materials, and stringent safety standards.

| Report Attribute | Details |

|---|---|

|

Stainless Steel Forgings Market Size (2026E) |

US$ 6.1 Bn |

|

Market Value Forecast (2033F) |

US$ 9.9 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

7.2% |

|

Historical Market Growth (CAGR 2020 to 2025) |

6.8% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Expansion of Infrastructure-Intensive Industries

Rising activity across infrastructure-intensive industries strengthens demand for forged stainless steel components through direct linkage with large-scale construction, energy systems, transport networks, and industrial facilities that operate under demanding mechanical and environmental conditions. These sectors require components that withstand high loads, vibration, pressure, and thermal variation while maintaining dimensional stability over extended service periods. Forging enhances internal grain flow and mechanical consistency, supporting superior strength and fatigue resistance compared with fabricated or cast forms. Decision-makers in capital-heavy industries prioritize materials that align with safety mandates, engineering certifications, and long operational lifecycles, reinforcing preference for forged stainless steel in critical applications such as pressure vessels, structural connectors, flow control systems, and heavy machinery assemblies.

Infrastructure-driven industries also operate within long project timelines and fixed capital expenditure frameworks, placing emphasis on reliability, predictable performance, and reduced lifecycle risk. Stainless steel forgings support these objectives through corrosion resistance in aggressive environments, compatibility with high-temperature and high-pressure operations, and reduced failure probability during continuous use. Engineering contractors and original equipment manufacturers integrate forged components early in design stages to minimize inspection intensity, limit maintenance intervention, and avoid costly downtime. Standardization requirements across large infrastructure projects further favor forged products due to repeatable quality, compliance with international specifications, and scalability in high-volume production.

Capital-Intensive Manufacturing Requirements

High upfront investment requirements constrain capacity expansion and new participant entry across this segment of advanced metal forming. Production relies on heavy-tonnage forging presses, high-temperature furnaces, precision dies, automated material handling, and advanced inspection systems. Stainless grades demand tighter thermal windows, higher deformation forces, and superior surface integrity, which elevates equipment specifications and narrows acceptable process variability. Long procurement and installation cycles for critical assets extend project lead times, delaying revenue realization and heightening exposure to demand fluctuations. Capital lock-in limits operational agility, restricting rapid shifts across alloy grades, geometries, and batch sizes. Fixed-cost intensity raises breakeven thresholds, placing pressure on margins during periods of uneven order flow. These dynamics reinforce advantages for incumbents with depreciated assets and established customer pipelines, while smaller operators face structural barriers that suppress competitive entry and capacity diversification.

Cost structure rigidity further reinforces restraint through energy intensity, compliance burden, and yield sensitivity. High-temperature operations drive elevated power and fuel consumption, while stringent metallurgical tolerances increase scrap risk during setup, die changes, and process tuning. Regulatory requirements related to safety, emissions, and traceability necessitate continuous investment in monitoring, testing, and certification systems, adding overheads independent of throughput. Capital recovery depends on sustained high utilization and extended production runs, which conflicts with fragmented demand across aerospace, chemical processing, power generation, and heavy engineering applications. Shorter order cycles and customized specifications dilute scale benefits, weakening returns on large fixed assets.

Electrification and energy transition-driven component demand

The acceleration of electrified transport, renewable power generation, and grid modernization intensifies demand for components engineered for high mechanical stress, thermal variation, and corrosive operating conditions. Forged stainless steel aligns with these requirements through high load tolerance, structural uniformity, and resistance to oxidation and chemical exposure. Electric drivetrains, battery enclosures, inverter housings, and charging hardware require materials that maintain dimensional stability under continuous vibration and temperature fluctuation. Forging processes deliver refined grain structures that support consistent performance in critical applications where failure risks translate into safety, warranty, and regulatory consequences. This alignment between electrification system requirements and forged material capabilities establishes a clear growth pathway tied to long-term industrial transformation.

Energy transition initiatives focused on renewable generation and electrified infrastructure further reinforce demand for durable forged components across wind, solar, hydrogen, and power distribution systems. Turbine shafts, mechanical connectors, flanges, and high-pressure fittings operate in environments marked by moisture, salinity, and cyclic loading, favoring forged stainless steel over cast or fabricated alternatives. Grid expansion and charging network deployment increase reliance on components with predictable lifecycle performance and low maintenance intervention. Capital investment strategies increasingly prioritize materials that support asset longevity and operational reliability, strengthening procurement preference for forged solutions.

Category-wise Analysis

Product Type Insights

Hot and cold forged parts are anticipated to secure around 48% of the stainless steel forgings market share in 2026, reflecting widespread adoption across automotive, industrial machinery, and energy equipment manufacturing. These forgings deliver optimized grain structure alignment, superior mechanical strength, and consistent dimensional accuracy, which align with performance specifications required for rotating shafts, fasteners, flanges, and structural connectors. Manufacturing scalability, process maturity, and compatibility with automation platforms support high-volume production while maintaining quality consistency. Equipment manufacturers prefer hot and cold forged stainless steel parts due to predictable lifecycle performance and reduced risk of in-service failure, reinforcing sustained demand leadership.

Sintered parts are expected to be the fastest-growing segment during the 2026–2033 forecast period, propelled by demand for complex geometries, material utilization efficiency, and cost optimization in medium-load applications. Powder metallurgy-based sintering enables near-net-shape production with minimal machining, which reduces material waste and energy consumption. Advancements in powder quality and sintering control expand feasible mechanical performance thresholds, enabling broader industrial acceptance. Adoption increases across consumer goods, precision instruments, and select automotive subsystems where weight optimization and design flexibility provide competitive advantage.

Process Insights

Closed die forging is poised to dominate with a forecasted market share of 42% in 2026, powered by capability to produce high-strength components with complex geometries and tight dimensional tolerances. The process ensures controlled material flow within precision-engineered dies, supporting refined grain alignment, high fatigue resistance, and consistent mechanical performance. Such attributes align with stringent requirements across transportation platforms, power generation equipment, and heavy industrial systems where reliability and load endurance remain critical. High repeatability supports volume manufacturing with minimal variation, while established tooling standards and skilled workforce availability strengthen cost efficiency, production stability, and long-term process leadership across specification-driven applications.

Extrusion is estimated to be the fastest-growing segment from 2026 to 2033, fueled by rising demand for long, uniform cross-section components used in structural, architectural, and industrial applications. This process supports efficient material utilization, streamlined production cycles, and lower waste generation compared to traditional forming methods. Design flexibility enables integration of functional features such as channels, ribs, and mounting profiles within a single profile, supporting lightweight and space-efficient engineering objectives. Compatibility with automated cutting, machining, and surface finishing processes improves throughput and scalability. Expanding infrastructure development, industrial fabrication, and modular construction practices continue to strengthen adoption momentum across diversified end-use environments.

Application Insights

Automotive applications are likely to be the leading segment with a projected 34% of the stainless steel forgings market revenue share in 2026 due to sustained vehicle production volumes and increasing material performance requirements. Platform electrification, stricter emission norms, and higher safety benchmarks intensify demand for components with superior strength, thermal stability, and corrosion resistance. Forged stainless steel enables reliable performance in drivetrain assemblies, steering systems, exhaust components, and structural safety parts operating under high stress and temperature variation. Consistency in mechanical properties supports large-scale production programs and global supply chains. Long service life, recyclability, and compliance with regulatory standards strengthen adoption across passenger vehicles, commercial fleets, and emerging electric mobility platforms.

Aerospace applications are anticipated to be the fastest-growing segment from 2026 to 2033, fueled by fleet modernization, lightweight material substitution, and stringent safety certification standards. Next-generation aircraft platforms emphasize fuel efficiency, structural reliability, and extended maintenance intervals, increasing reliance on high-integrity forged components. Forged stainless steel supports critical systems such as landing gear elements, engine mounts, fasteners, and control mechanisms requiring fatigue endurance and resistance to extreme operating environments. Precision forging enables tight dimensional control essential for aerospace qualification processes.

Regional Insights

North America Stainless Steel Forgings Market Trends

North America maintains a significant presence in the stainless steel forgings market landscape, underpinned by advanced manufacturing capabilities, established automotive production, and aerospace engineering expertise. Strong industrial standards and stringent safety and quality regulations drive consistent demand for high-performance forged components. Automotive platforms increasingly require durable drivetrain parts, braking systems, and structural assemblies that meet safety, emissions, and fuel-efficiency benchmarks. Aerospace and defense sectors contribute through high-stress engine components, landing gear assemblies, and structural airframe parts requiring fatigue resistance, corrosion protection, and precision tolerances. Well-developed supply chains, access to high-quality stainless steel feedstock, and adoption of modern forging technologies such as closed die and precision forging ensure reliable output and consistent product quality, supporting long-term manufacturing contracts and global exports.

Emerging trends in electrified mobility, renewable energy infrastructure, and industrial automation are driving incremental growth in North America. Increased deployment of electric vehicles, energy storage systems, and high-efficiency industrial machinery raises demand for components capable of withstanding thermal cycling, high mechanical loads, and corrosive environments. Advanced process integration, including digital forging, automated finishing, and in-line quality monitoring, improves production efficiency while minimizing scrap and downtime. Collaboration between engineering firms and forging manufacturers fosters development of specialized stainless steel grades and complex geometries for lightweight, high-strength applications. Expansion of maintenance, repair, and overhaul activities for automotive, aerospace, and energy equipment further supports market uptake.

Europe Stainless Steel Forgings Market Trends

Europe demonstrates a well-established market position in stainless steel forgings, driven by mature automotive manufacturing, aerospace production, and precision engineering industries. Strong regulatory frameworks emphasizing safety, emission reduction, and material traceability create consistent demand for high-quality forged components with strict dimensional and mechanical tolerances. Automotive applications rely on stainless steel forgings for drivetrain assemblies, braking systems, and structural elements to meet rigorous safety and performance standards. Aerospace and defense sectors further support adoption through critical engine components, landing gear parts, and high-stress structural elements requiring fatigue resistance and corrosion protection. Concentrated industrial clusters, advanced metallurgy expertise, and well-developed supply networks enable efficient production scaling, consistent quality assurance, and timely delivery to global customers, reinforcing stability and strategic importance in global manufacturing operations.

High-value manufacturing trends, including lightweight vehicle architectures, electric mobility, and energy-efficient industrial equipment, are shaping growth dynamics. Increasing focus on electrified drivetrains, renewable energy installations, and industrial automation intensifies demand for forged components capable of withstanding thermal and mechanical stress while maintaining long-term reliability. Integration of digital forging technologies, precision process control, and automation enhances yield, reduces scrap, and supports flexible production for complex geometries. Collaboration between manufacturers and research institutions drives material innovation, including high-performance stainless steel grades suitable for hybrid and electric power systems.

Asia Pacific Stainless Steel Forgings Market Trends

Asia Pacific is expected to dominate with an estimated 45% of the stainless steel forgings market share in 2026, reflecting strong industrialization, concentrated manufacturing clusters, and vertically integrated supply chains. Automotive and industrial machinery production forms a significant portion of consumption, where high-strength, corrosion-resistant forged components are essential for powertrains, safety-critical assemblies, and heavy-duty equipment. Availability of large-scale steelmaking capacity enables cost-efficient procurement of high-quality feedstock, supporting competitive pricing and shorter lead times for precision forgings. Integration of forging facilities with downstream machining, finishing, and assembly operations enhances operational efficiency and reduces inventory holding costs, creating a favorable ecosystem for high-volume production.

Asia Pacific is forecasted to be the fastest-growing regional market for stainless steel forgings between 2026 and 2033, stimulated by rapid industrial modernization, clean energy adoption, and electrification of mobility platforms. Surge in high-value applications such as electric vehicle motors, renewable energy turbines, and aerospace structural elements increases reliance on forged stainless steel for its dimensional stability and long service life under harsh operational conditions. Strategic government initiatives supporting infrastructure expansion and industrial technology upgrades accelerate deployment of advanced forging technologies. Access to skilled labor and technical expertise facilitates scaling of production capacity while maintaining strict quality control.

Competitive Landscape

The global stainless steel forgings market exhibits a moderately fragmented structure, with several multinational players holding significant but not dominant shares. Key players such as Bharat Forge Limited, LARSEN & TOUBRO LIMITED, ATI, thyssenkrupp AG, and SIFCO Industries, Inc. maintain strong operational footprints across automotive, aerospace, energy, and industrial machinery sectors. These companies leverage advanced forging technologies, including closed die, precision, and impression die processes, to produce high-strength, corrosion-resistant components that meet strict mechanical and dimensional requirements. Certification across international quality standards, including ISO and aerospace-specific approvals, enables access to high-value contracts and ensures compliance with regulatory and safety requirements.

Leading manufacturers focus on long-term contractual agreements with original equipment manufacturers, engineering firms, and infrastructure developers to reinforce market positioning. Integration of downstream operations, such as machining, surface finishing, and testing, enhances efficiency, reduces lead times, and ensures delivery reliability for mission-critical applications. Geographic diversification of production and service networks allows players to respond to regional demand variations and maintain competitive pricing. Operational scale, coupled with technical expertise and innovation in material development, provides differentiation in an otherwise moderately fragmented market.

Key Industry Developments

- In November 2025, the government launched the third round of the Production Linked Incentive (PLI) scheme for specialty steel, targeting fresh investment of about INR 44,000 crore to boost advanced steel production, including forged components, and reduce import dependence in high-value segments such as defense, aerospace, automobiles, and infrastructure.

- In July 2025, Ramkrishna Forgings announced a major expansion with an INR 20 billion forged wheel manufacturing plant in Chennai designed to produce 228,000 wheels annually, marking a strategic move into the forged wheel segment and strengthening supply capabilities for rail and industrial applications.

- In July 2025, AMIC Forging Limited, a specialist in open-die forgings and precision machined components, secured a new order worth approximately INR 54.6 million (about US$ 0.66 million) from a joint venture including Mitsubishi Heavy Industries for supplying high-performance components, strengthening the company’s position in precision engineering.

Companies Covered in Stainless Steel Forgings Market

- Bharat Forge Limited

- LARSEN & TOUBRO LIMITED.

- ATI.

- thyssenkrupp AG

- SIFCO Industries, Inc.

- Precision Castparts Corp.

- NIPPON STEEL CORPORATION.

- Daido Steel Co., Ltd.

- Aubert & Duval

- ELLWOOD Group Inc.

- Ramco Specialties, INC.

- Scot Forge Company

Frequently Asked Questions

The global stainless steel forgings market is projected to reach US$ 6.1 billion in 2026.

Rising demand for durable, high-strength, and corrosion-resistant components in automotive, aerospace, energy, and industrial sectors drives the stainless steel forgings market.

The market is poised to witness a CAGR of 7.2% from 2026 to 2033.

Electrification of transport, adoption of renewable energy, and increasing demand for high-strength, corrosion-resistant forged components across automotive, aerospace, and industrial applications is the key opportunity of the market.

Some of the key market players include Bharat Forge Limited, LARSEN & TOUBRO LIMITED, ATI, thyssenkrupp AG, and SIFCO Industries, Inc.