- Medical Devices

- Spine Surgery Robots Market

Spine Surgery Robots Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Spine Surgery Robots Market by Source (Systems, Instrument & Accessories, Services & Others), Type (Minimally Invasive, Open Surgery), Application (Spinal Fusion, Vertebral Compression Fractures, Spinal Deformities, Others), End-user (Hospitals, Ambulatory Surgical Centers, Others), and Regional Analysis from 2026 to 2033

Spine Surgery Robots Market Share and Trends Analysis

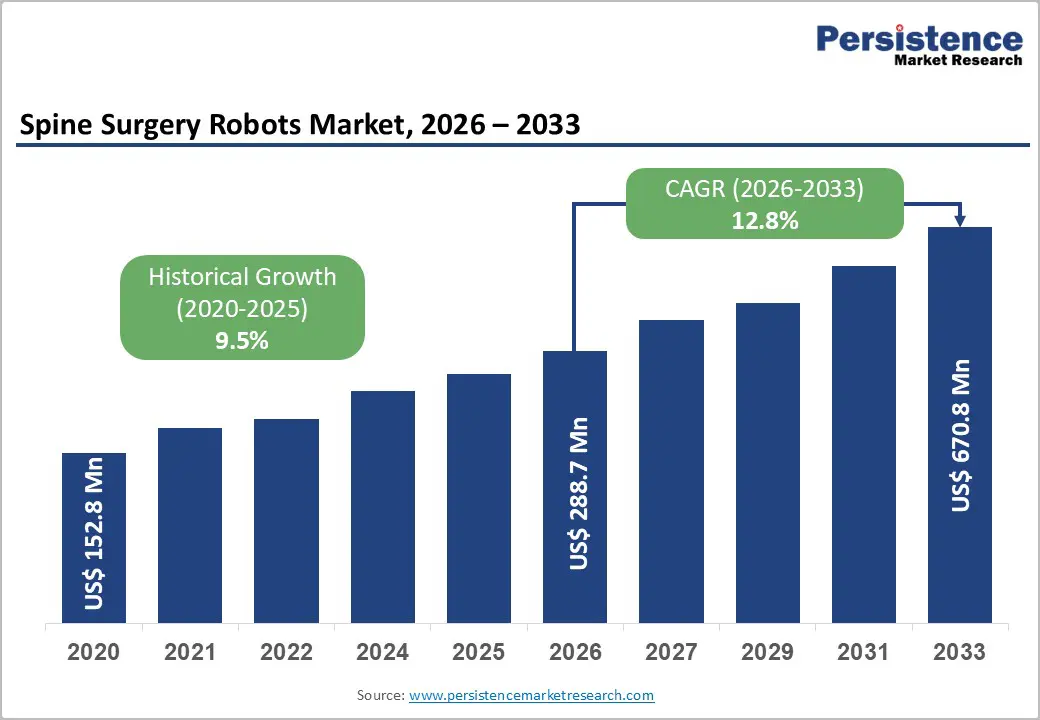

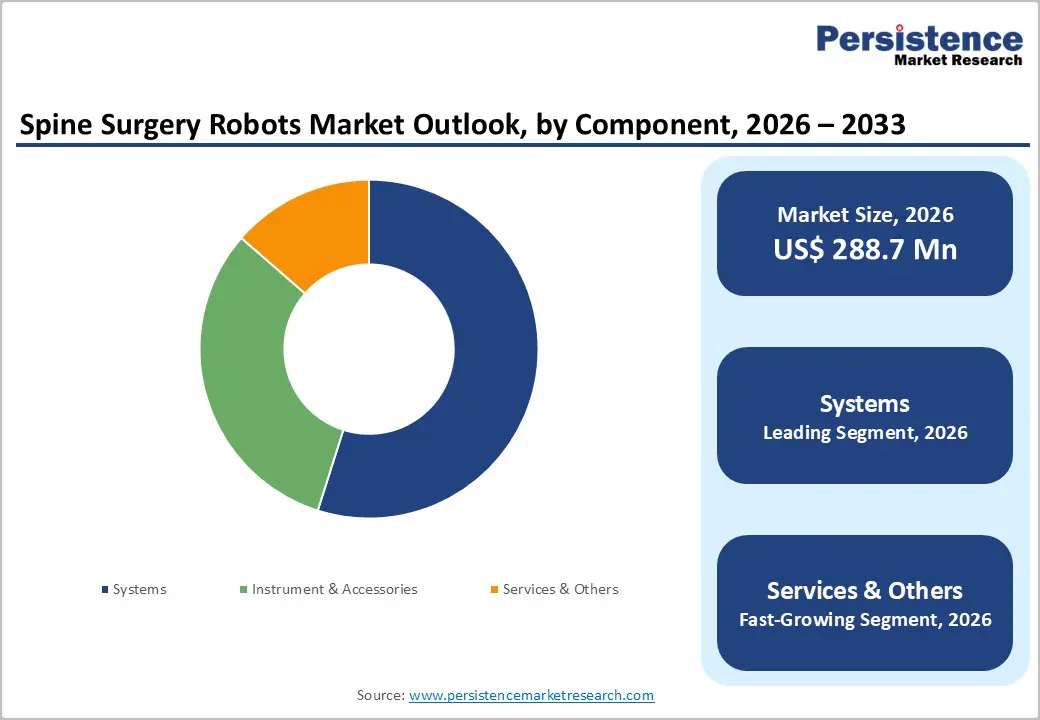

The global spine surgery robots market is projected to grow from US$ 288.7 million in 2026 to US$ 670.8 million by 2033, at a CAGR of 12.8% over the forecast period.

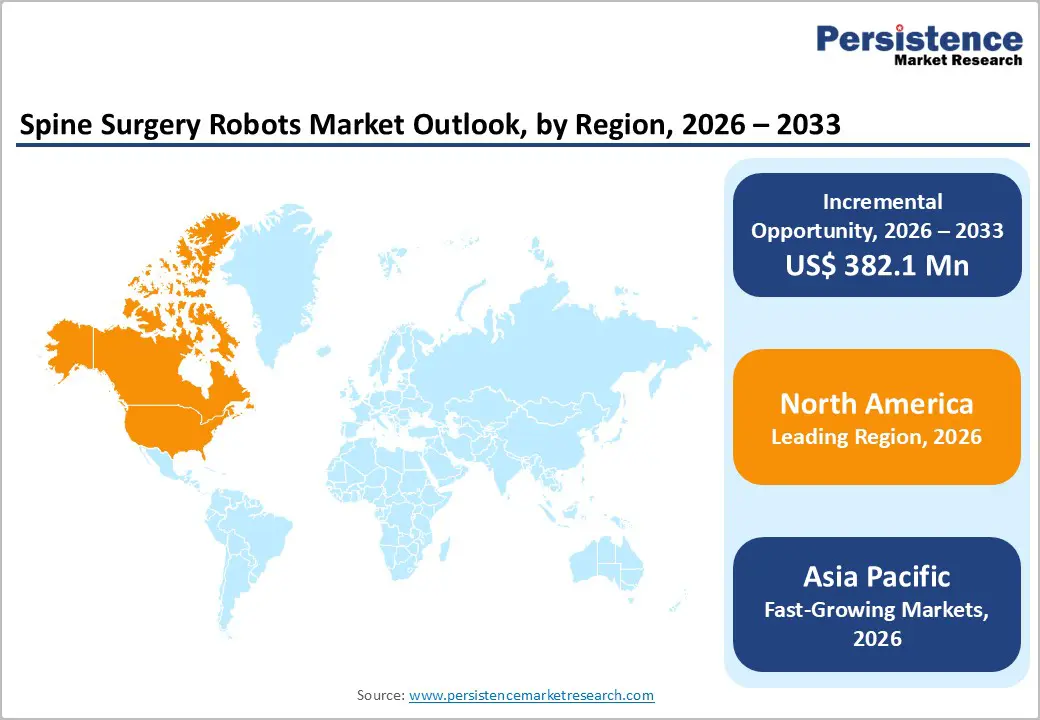

The market is expanding rapidly, driven by increasing adoption of minimally invasive procedures, demand for surgical precision, and technological advancements. North America dominates due to early adoption, high healthcare spending, and advanced hospital infrastructure. The Asia-Pacific region is the fastest-growing, supported by rising procedural volumes, improved healthcare access, and substantial government investments in medical robotics.

Key Industry Highlights:

- Dominant Segment: Robotic systems dominated the spine surgery robots market in 2025, accounting for a 54.9% share, driven by widespread adoption of core robotic platforms, growing demand for surgical accuracy, and increasing use in minimally invasive spine procedures across hospitals and specialty spine centers.

- Dominant Region: North America led the market in 2025, with a 44.8% share, supported by advanced surgical infrastructure, early adoption of robotic technologies, and high spine-procedure volumes. The Asia-Pacific region emerged as the fastest-growing region due to the rising incidence of spinal disorders, expanding healthcare access, and increased investment in surgical robotics.

- Market Drivers: Market growth is driven by the increasing prevalence of degenerative spine disorders, the demand for minimally invasive surgeries, the need for greater surgical precision, reduced complication rates, and ongoing technological advancements in navigation, imaging, and AI-assisted robotics.

- Market Opportunity: Key opportunities include expansion into outpatient and ambulatory surgery centers, integration of AI-driven planning and navigation software, growth in emerging markets, development of cost-effective robotic systems, and long-term revenue from software upgrades and service-based models.

| Key Insights | Details |

|---|---|

| Spine Surgery Robots Market Size (2026E) | US$ 288.7 Mn |

| Market Value Forecast (2033F) | US$ 670.8 Mn |

| Projected Growth (CAGR 2026 to 2033) | 12.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 9.5% |

Market Dynamics

Driver - Rising prevalence of spinal disorders

Spinal disorders, particularly low back pain, represent a substantial and increasing global health burden that drives demand for advanced surgical solutions such as spine surgery robots. According to the World Health Organization and Global Burden of Disease data, 619 million people worldwide suffered from low back pain in 2020, and this figure is projected to rise to 843 million by 2050 due to population growth and ageing.

Low back pain alone accounts for the largest share of musculoskeletal disability globally, contributing significantly to years lived with disability (YLDs) and overall healthcare utilization. This high prevalence of spinal conditions underscores a persistent need for precision surgical interventions, supporting greater adoption of robotic assistance in complex spine procedures where traditional methods may be insufficient.

Beyond low back pain, broader spinal pathology also imposes significant clinical demand. Meta-analyses estimate that approximately 266 million individuals worldwide have both degenerative spine disease and clinically relevant low back pain annually, highlighting the volume of patients who may require surgical evaluation or intervention.

Degenerative conditions such as disc degeneration affect more than 400 million people globally each year, indicating widespread structural spinal problems that can progress to surgical necessity. These high prevalence figures translate into substantial surgical caseloads, increasing the need for technologies that enhance surgical precision, safety, and outcomes, attributes that spine surgery robots are designed to deliver. Consequently, the growing epidemiological burden of spinal disorders directly supportsthe expansion of the spine surgery robotics market.

Restraints - High capital and operational costs

One of the most significant restraints on the spine surgery robots market is the high upfront capital cost of purchasing robotic surgical platforms. Leading systems, including those used in spine and general surgery, typically cost between USD 1.0 million and USD 2.5 million per unit, depending on capabilities and configuration, with some systems extending toward the upper end of this range, particularly in advanced healthcare settings. These figures far exceed the cost of traditional surgical equipment and represent a substantial budgetary commitment for hospitals, especially for mid-sized and small facilities. In many national health systems, such expenditure must be justified against competing priorities such as essential diagnostic imaging or emergency care infrastructure, limiting the pace of adoption in resource-constrained environments.

Beyond initial acquisition, ongoing operational and maintenance costs further restrain market growth. Robotic systems typically incur annual service and maintenance fees of USD 100,000 to USD 200,000, and disposable instruments alone can add USD 700 to USD 3,000 per procedure, significantly increasing the cost per case compared to traditional spine surgery methods. These recurrent expenses must be absorbed by hospital operating budgets or passed on to patients, increasing overall procedural costs.

Especially in healthcare systems with constrained reimbursement policies or limited insurance coverage for robotic procedures, these operational costs reduce hospitals' financial incentives to scale their robotic programs. Smaller healthcare centers, which often cannot achieve the high procedural volumes needed to spread these costs, may therefore delay or forgo investment in robotic systems.

Opportunity - Development of cost-effective robotic systems

A major opportunity in the spine surgery robotics market lies in developing cost-effective robotic systems that reduce acquisition and operational barriers for hospitals. Traditional surgical robots can cost between USD 1.5 million and USD 2.5 million per unit, with maintenance and training adding further expenses, which limits accessibility for many facilities.

By contrast, emerging locally developed systems in countries such as India are reportedly priced 50-60% lower than imported alternatives, enabling broader adoption across Tier-2 and Tier-3 cities and reducing financial strain on healthcare providers. This trend toward cheaper platforms can expand market penetration and support more equitable access to robotic spine surgery across diverse healthcare settings.

The shift toward cost-efficient robotics not only improves affordability but also aligns with global healthcare cost containment goals. Studies show that robotic surgery, although initially expensive, can reduce hospital length of stay by 1-2 days, resulting in 15-20% lower per-case total expenditure due to fewer complications and faster recovery. Affordable systems, paired with shorter stays, help hospitals achieve better value-based care outcomes, making such investments more justifiable despite their high initial costs.

Moreover, innovations such as leasing, financing, and indigenous manufacturing create pathways for sustainable adoption, particularly in developing markets where healthcare budgets are constrained yet demand for advanced spine care is rising.

Category-wise Analysis

By Component Insights

Systems dominates with 54.9% share of the global market in 2025, because it delivers the core robotic platform that enables robotics-assisted procedures with precision and safety. Data from the U.S. Centers for Medicare & Medicaid Services (CMS) indicate that robotic-assisted surgeries have expanded across many procedure types, reflecting broad clinical utilization of full systems rather than isolated components. The U.S. Food and Drug Administration (FDA) has cleared multiple complete robotic systems specifically for spinal applications, underscoring regulatory confidence in integrated platforms for tasks such as pedicle screw placement.

Furthermore, studies in surgical journals indicate that robotic systems significantly improve accuracy in spinal instrumentation compared with freehand techniques, thereby increasing clinical preference for complete systems. Because these platforms encompass navigation, imaging, and robotic control, they are the principal revenue and functional drivers of robotic spine surgery adoption.

By Method Insights

Minimally invasive techniques dominate in spine surgery, accounting for 60.6% of cases in 2025, because they are associated with smaller incisions, less tissue disruption, and faster recovery compared with traditional open procedures. Clinical data indicate that patients undergoing minimally invasive lumbar fusion tend to have shorter hospital stays (e.g., approximately 3.35 vs. 3.6 days for open surgery in one national cohort) and lower costs in certain cases due to reduced resource use.

Minimally invasive approaches also result in lower blood loss and reduced complication rates, including fewer infections and shorter postoperative rehabilitation periods, while yielding similar outcomes. These benefits align with broader surgical preferences for interventions that improve patient recovery trajectories and reduce overall healthcare utilization, thereby encouraging the adoption of minimally invasive methods over open techniques in spinal care.

Regional Insights

North America Spine Surgery Robots Market Trends

North America dominates the spine surgery robots market, with a 44.8% share in 2025, owing to high procedural volumes, advanced surgical infrastructure, and supportive healthcare policies that encourage the adoption of innovation. In the United States, the Centers for Medicare & Medicaid Services (CMS) reports that robot-assisted surgeries, including musculoskeletal and spine procedures, are widely reimbursed under Medicare, which drives hospital investment in robotic platforms.

The Centers for Disease Control and Prevention (CDC) notes that back problems and spinal disorders account for one of the leading causes of disability, with tens of millions of adults reporting chronic back pain annually, generating consistent demand for surgical intervention. Additionally, the U.S. Food and Drug Administration (FDA) has cleared numerous robotic systems for use in spine surgery, reflecting regulatory acceptance. These factors, combined with extensive surgeon training networks and high healthcare expenditure, sustain North America’s leadership in the adoption of spine-surgery robotics.

Europe Spine' Surgery Robots Market Trends

Europe is a significant region in the spine surgery robots market due to its aging population, high burden of spinal disorders, and well-developed healthcare systems that support advanced surgical care. Eurostat data indicate that more than 20% of the EU population was aged 65+ in 2024, a demographic group strongly associated with degenerative spine conditions and surgical demand. The World Health Organization reports that musculoskeletal conditions rank among the top causes of disability in Europe, with low back pain affecting a substantial portion of adults and driving clinical demand for precise interventions.

Many European countries provide robust public healthcare coverage that includes advanced surgical technologies, and national health agencies have increasingly incorporated robot-assisted procedures into clinical guidelines for complex spine surgeries. These demographic and healthcare factors together make Europe a key regional market.

Asia Pacific Spine Surgery Robots Market Trends

Asia-Pacific is the fastest-growing region in the spine surgery robots market due to rapidly expanding healthcare infrastructure, a large and ageing population with rising spinal disorder prevalence, and increasing surgical capacity. The United Nations estimates that by 2050, nearly one-third of East Asian populations will be aged 60 or older, driving demand for treatment of degenerative spine conditions. The World Health Organization notes that musculoskeletal disorders, including low back pain, are among the leading causes of disability globally, with substantial incidence in South and East Asia as lifestyles change and injury burdens rise.

Many APAC countries are also increasing healthcare spending; for example, India’s health expenditure rose to about 3.2% of GDP in 2022, enabling investment in advanced surgical technologies. These demographic and health system trends accelerate the adoption of robotic spine surgery in the region.

Competitive Landscape

The spine surgery robots market is highly competitive, led by companies like Medtronic, Globus Medical, Stryker, and Johnson & Johnson. Competition is driven by technological innovation in robotic systems, AI-assisted navigation, and imaging integration, along with strategic partnerships, training programs, and cost-effective solutions, which enable differentiation and expand adoption, particularly in minimally invasive and complex spinal procedures globally.

Key Industry Developments:

- In September 2025, Medtronic announced the launch of a global hub for AI and robotics in surgery, designed to accelerate the development, integration, and deployment of advanced surgical technologies. The hub aimed to support innovation in robotic-assisted procedures, AI-driven planning, and workflow optimization across multiple surgical specialties, reinforcing Medtronic’s leadership in transforming surgical care worldwide.

- In September 2024, Medtronic expanded its AiBLE™ spine surgery ecosystem by introducing new technologies and forming a partnership with Siemens Healthineers. The collaboration aimed to enhance surgical planning, imaging integration, and AI-driven workflow solutions for spine procedures. This initiative strengthened Medtronic’s position in the robotic spine surgery market, enabling hospitals to access more advanced, interoperable, and efficient robotic-assisted spinal surgery solutions.

Companies Covered in Spine Surgery Robots Market

- Medtronic plc

- Zimmer Biomet

- Globus Medical, Inc.

- TINAVI Medical Technologies Co., Ltd.

- Point Robotics MedTech, Inc.

- NuVasive, Inc.

- Brainlab AG

- Curexo, Inc.

- Accelus, Inc.

- Synaptive Medical

- Others

Frequently Asked Questions

The global spine surgery robots market is projected to be valued at US$ 288.7 Mn in 2026.

Rising spinal disorder prevalence, minimally invasive surgery demand, technological advancements, and expanding healthcare infrastructure drive growth.

The global spine surgery robots market is poised to witness a CAGR of 12.8% between 2026 and 2033.

Expansion in emerging markets, AI integration, cost-effective systems, outpatient adoption, and recurring software-service revenue opportunities.

Medtronic plc, Zimmer Biomet, Globus Medical, Inc., TINAVI Medical Technologies Co., Ltd., Point Robotics MedTech, Inc., NuVasive, Inc.