- Smart Packaging

- Shipping Supply Market

Shipping Supply Market Size, Share, and Growth Forecast, 2026 - 2033

Shipping Supply Market by Material (Corrugated Paper/Paperboard, Plastic, Others), Product Type (Corrugated Boxes, Protective Packaging, Others), End-user, and Regional Analysis for 2026 - 2033

Shipping Supply Market Size and Trends Analysis

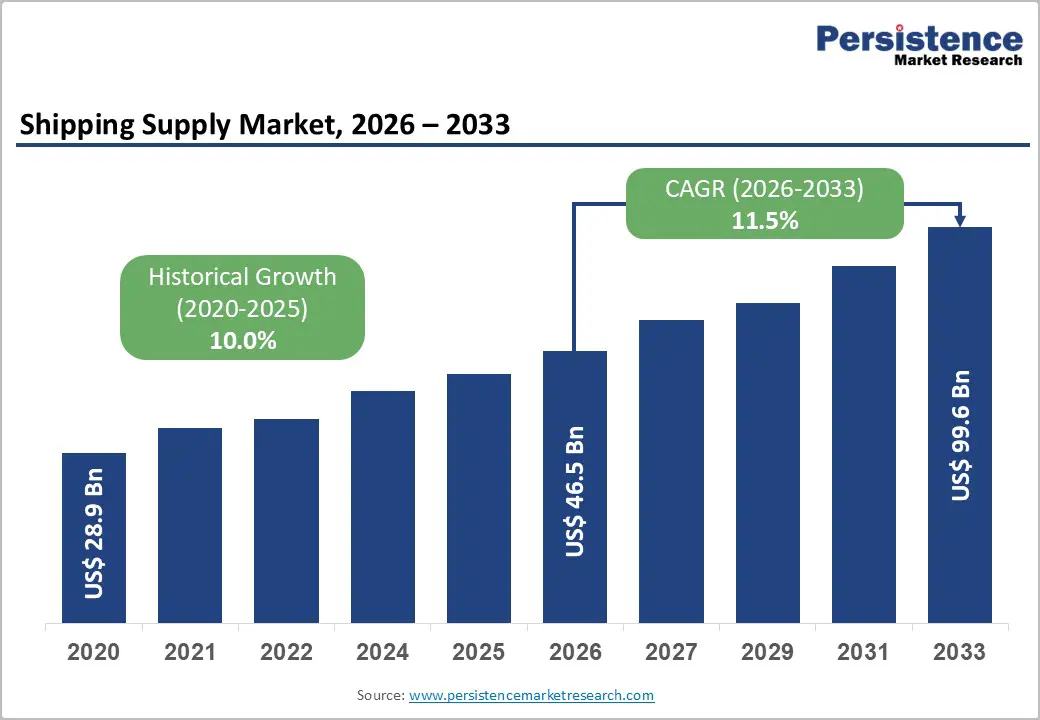

The global shipping supply market is forecast to expand from US$46.5 billion in 2026 to US$99.6 billion by 2033, registering a CAGR of 11.5% during the forecast period from 2026 to 2033, driven by sustained growth in global e-commerce and cross-border trade, increasing substitution of bulk paper-based and engineered packaging for single-use plastics, and rising investments in automated fulfillment and protective packaging for high-value goods.

Regulatory tightening on packaging waste, particularly in Europe, alongside consolidation among global paper and corrugated packaging players, is reshaping supply chains, capital deployment strategies, and competitive positioning. The market presents strategic opportunities in fiber-based packaging solutions, advanced protective materials for fragile products, and circular product-service models for large shippers.

Key Industry Highlights

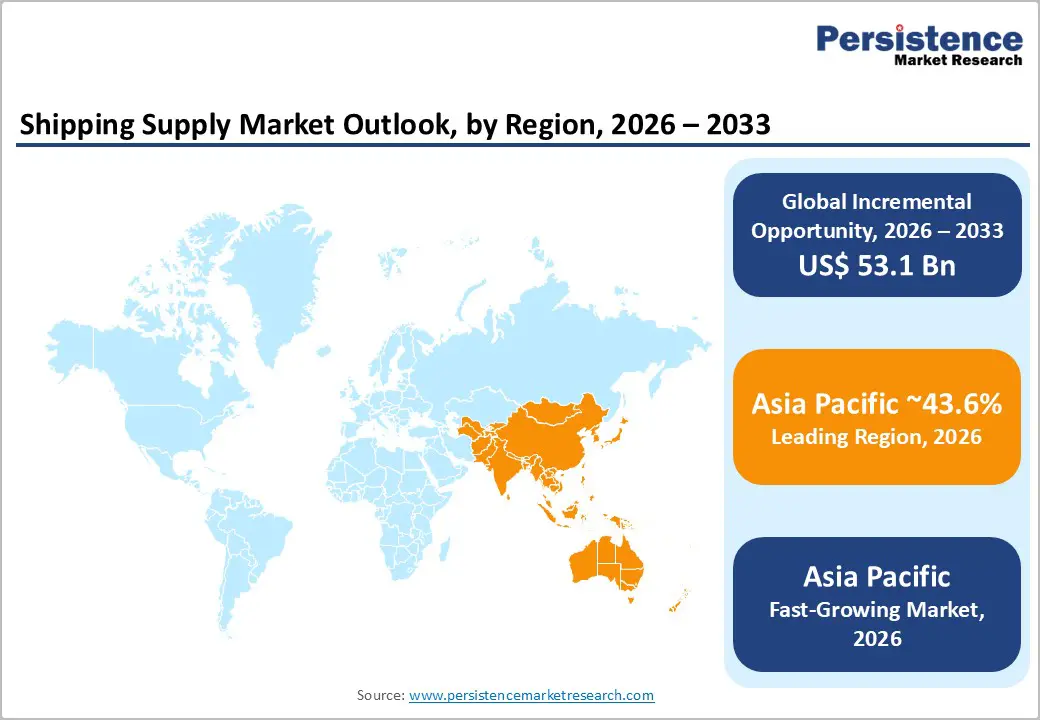

- Leading Region: Asia Pacific is projected to account for approximately 43.6% of the global market share, supported by large-scale manufacturing activity, export-oriented supply chains, and rapid expansion of e-commerce fulfillment infrastructure across China, Japan, India, and ASEAN economies.

- Fastest-Growing Region: Asia Pacific, registering the highest regional growth rate, driven by continued investment in containerboard capacity, rising domestic consumption, and accelerating cross-border e-commerce volumes, particularly in China and India.

- Investment Plans: Major packaging producers are prioritizing capacity expansion, automation, and recycled-fiber sourcing, with capital investments concentrated in high-speed corrugated converting lines, containerboard mills, and fiber-based protective packaging solutions to support sustainability compliance and high-volume fulfillment requirements.

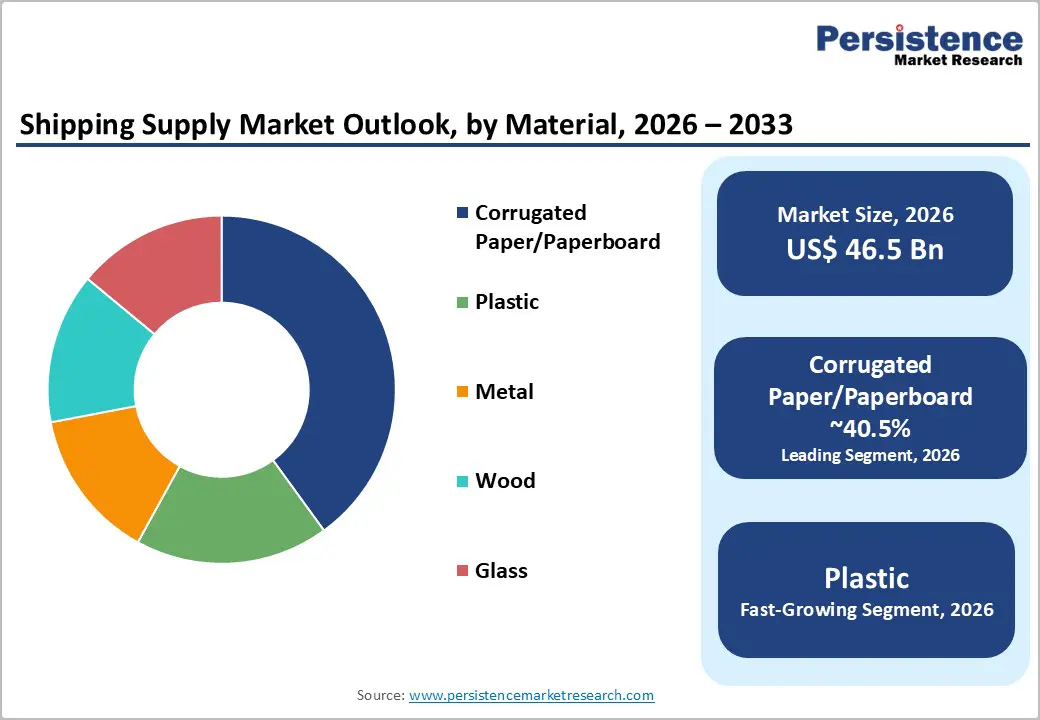

- Dominant Material: Corrugated paper/paperboard, to hold an estimated 40.5% revenue share in 2026, driven by cost efficiency, recyclability, regulatory preference for fiber-based materials, and widespread use in e-commerce and industrial shipping applications.

- Leading Product Type: Corrugated boxes are estimated to represent approximately 49.2% of total revenue share, supported by universal applicability across industries, compatibility with automated packing systems, and scalability for high-volume logistics and distribution operations.

| Key Insights | Details |

|---|---|

| Shipping Supply Market Size (2026E) | US$46.5 Bn |

| Market Value Forecast (2033F) | US$99.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 11.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 10.0% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Expansion of E-Commerce and Cross-Border Retail

E-commerce remains the most significant demand catalyst for shipping supplies. Global online retail sales continue to represent a growing share of total retail trade, driving sustained demand for corrugated cartons, protective packaging, and poly mailers. Retail e-commerce sales are projected to exceed US$6.4 trillion, supporting strong parcel volumes across domestic and international routes. Higher parcelization rates, characterized by smaller average shipment sizes and more frequent deliveries, increase per-unit packaging consumption and elevate demand for protective solutions. Growth in categories such as consumer electronics, apparel, and perishables further accelerates the adoption of premium protective packaging, enabling shipping supplies to grow faster than overall retail volumes.

Regulatory and Sustainability Shifts Toward Recyclable Materials

Packaging regulations are tightening across major economies, accelerating the transition toward recyclable and fiber-based shipping materials. The European Union’s Packaging and Packaging Waste Regulation introduces extended producer responsibility, reuse targets, and recycled-content requirements, significantly influencing material selection and packaging design. In response, manufacturers and retailers are shifting away from single-use plastics toward recyclable corrugated boxes and engineered, fiber-based protective inserts. These changes elevate the value proposition of sustainable shipping supplies and increase the total cost of ownership advantages for circular packaging solutions. Large, vertically integrated suppliers benefit disproportionately due to their ability to invest in recycling infrastructure, reclaimed fiber supply, and compliance-ready packaging formats.

Industry Consolidation and Investment in Automated Packaging Technologies

The shipping supply industry is undergoing consolidation as major packaging companies pursue scale efficiencies across containerboard production, converting operations, and logistics services. Large-scale mergers, acquisitions, and capacity expansions enable higher throughput, lower unit costs, and broader geographic coverage. Concurrently, capital investment in high-speed converting equipment, automated box manufacturing systems, and engineered protective technologies is improving productivity and enabling more customized packaging formats. These investments enhance service levels for high-volume shippers while raising barriers to entry for smaller regional suppliers that lack automation capabilities, reinforcing the competitive advantage of large incumbents.

Barrier Analysis - Volatility in Raw Materials and Energy Costs

Shipping supply manufacturers face persistent volatility in raw material costs, particularly for containerboard, pulp, polymers, and energy inputs. Fluctuations driven by timber supply constraints, pulp market cycles, and energy price instability directly affect production costs and margins. Smaller converters without long-term supply contracts are particularly exposed to these fluctuations. Price swings of approximately 10-25% over successive quarters can significantly alter per-unit margins, disrupt procurement planning, and trigger capacity rationalization. Such volatility complicates pricing strategies and reduces margin visibility across the supply chain.

Trade Disruptions and Logistics Inefficiencies

Global shipping supply chains are vulnerable to port congestion, trade policy uncertainty, and inland logistics constraints, which increase lead times and working capital requirements. Extended replenishment cycles force manufacturers and buyers to hold higher safety stock levels, increasing inventory carrying costs. In Asia Pacific, inconsistent vessel schedules and container availability create irregular demand signals, complicating production planning for corrugated box and pallet manufacturers. Multi-week shipment delays can materially increase inventory exposure and heighten the risk of obsolescence, particularly for customized or client-specific packaging solutions.

Opportunity Analysis - Fiber-Based Protective Packaging and Recycled-Content Premiums

Growing demand for recyclable, paper-based alternatives to foam and plastic protective materials represents a significant value-creation opportunity. Engineered corrugated inserts, molded fiber cushions, and certified recycled-content packaging solutions command higher average selling prices and offer superior margin profiles. Substituting just 5-10% of polymer-based protective packaging with fiber-based alternatives across parcel shipments could generate an incremental US$1-3 billion opportunity by 2030, depending on adoption rates and pricing differentials. This opportunity favors suppliers with strong R&D capabilities, advanced converting assets, and access to recycled fiber inputs.

Value-Added Service Models for Large Shippers

Large e-commerce platforms and manufacturing enterprises increasingly outsource packaging design, kitting, and return-logistics functions to reduce the total cost of ownership. Shipping supply providers that offer integrated service bundles, including on-site packaging engineering, reusable packaging loops, and recycling programs, can capture recurring revenue streams and strengthen customer retention. Service-adjacent offerings can contribute an estimated 10-15% of supplier revenue in mature customer relationships, improving lifetime value and supporting premium valuations. Integration of tracking, traceability, and anti-tamper features further enhances competitiveness in regulated and high-value product categories.

Category-wise Analysis

Material Insights

Corrugated Paper/Paperboard is anticipated to account for approximately 40.5% of the total revenue share, due to its cost efficiency, light weight, high structural strength, and recyclability, making it well-suited for high-volume shipping applications. It dominates parcel and palletized shipments for durable and non-perishable goods across e-commerce, retail distribution, and industrial supply chains. Strong recycling infrastructure and regulatory preference for fiber-based materials further support its widespread adoption.

Global and regional converters continue to expand corrugated converting capacity and invest in lightweight yet high-performance board grades to serve large e-commerce fulfillment networks. Examples include standardized shipping cartons for online retail orders and heavy-duty corrugated boxes used in industrial components and consumer electronics distribution. Commitments by retailers and logistics providers to circular packaging models further reinforce demand, particularly for premium recycled-content corrugated solutions.

Plastic materials, including poly mailers, stretch films, and flexible protective packaging, are likely to be the fastest-growing material category in specific shipping applications. Their lightweight properties, moisture resistance, and cost competitiveness make them particularly attractive for small parcels, apparel shipments, and moisture-sensitive products. Growth is driven by rising volumes of direct-to-consumer apparel, footwear, and small electronics shipped through e-commerce platforms, where dimensional weight optimization is critical.

Innovation in recyclable, mono-material plastic formats and reduced-thickness films is supporting adoption while addressing sustainability concerns. Although long-term growth may moderate as fiber-based alternatives improve performance, plastics are expected to retain strong demand in applications requiring water resistance and minimal packaging weight.

Product Type Insights

Corrugated boxes are anticipated to hold approximately 49.2% of the market share, due to their universal applicability, scalability for mass production, and compatibility with automated packaging lines. They are widely used across retail distribution, industrial manufacturing, and cross-border logistics for transporting goods ranging from consumer products to machinery components.

Integrated paper and packaging companies supply both standardized shipping cartons and customized box formats designed for specific product dimensions and load requirements. Examples include high-volume e-commerce shipping boxes, bulk transport cartons for food and beverage products, and reinforced corrugated containers for industrial equipment. Their adaptability, cost efficiency, and recyclability ensure that corrugated boxes remain the backbone of global shipping operations.

Protective packaging, encompassing cushioning foams, air pillows, molded fiber inserts, and paper-based cushioning systems, is the fastest-growing product segment within the shipping supply market. Growth is fueled by increasing shipments of fragile and high-value goods such as consumer electronics, cosmetics, pharmaceuticals, and home appliances. Rising expectations for damage-free delivery, particularly in same-day and next-day fulfillment models, are accelerating the adoption of engineered protective solutions.

Innovation in fiber-based protective inserts is shifting demand toward sustainable, higher-value products that offer both impact protection and recyclability. Suppliers offering customized protective kits for fulfillment centers are capturing premium margins and long-term supply contracts.

Regional Insights

North America Shipping Supply Market Trends - E-Commerce Fulfillment Scale, Lightweighting & State-Level EPR Pressure

North America represents a significant share of the global shipping supply market, underpinned by advanced e-commerce logistics infrastructure, high parcel density, and mature recycling systems. The U.S. dominates regional demand, accounting for the majority of corrugated packaging consumption, protective materials usage, and industrial dunnage volumes. Growth is primarily driven by omnichannel retail expansion, accelerated fulfillment timelines, and rising shipments of fragile, high-value goods such as electronics and home appliances. Major e-commerce platforms and logistics providers increasingly require standardized, automation-ready packaging formats, reinforcing demand for precision-engineered corrugated boxes and protective inserts.

Leading packaging producers such as International Paper, WestRock, and Packaging Corporation of America continue to invest in high-speed converting lines and box plant modernization to serve national distribution networks. Large retailers and brands, including Amazon, Walmart, and Target, have also expanded initiatives to reduce packaging weight, eliminate excess void fill, and increase recycled content, directly influencing material selection across the supply chain. These commitments are accelerating the adoption of lightweight corrugated grades and molded fiber protective solutions in place of traditional plastic cushioning.

Although North America lacks a unified federal packaging regulation framework, state-level extended producer responsibility (EPR) programs, particularly in California, Oregon, and Colorado, are shaping material preferences and procurement strategies. These policies increase reporting and cost obligations for packaging producers, incentivizing investments in recyclable, fiber-based materials and closed-loop supply chains. In response, converters and material suppliers are expanding recycled-fiber sourcing and regional mill capacity to ensure compliance while controlling input costs. Overall, North America’s shipping supply market reflects a balance between operational efficiency, regulatory adaptation, and corporate sustainability mandates, supporting steady long-term growth.

Europe Shipping Supply Market Trends - Regulation-Led Fiber Packaging & Integrated Supplier Scale

Europe remains a major shipping supply market, distinguished by high regulatory rigor, advanced recycling infrastructure, and strong adoption of fiber-based packaging solutions. Germany, the U.K., France, and Spain serve as core demand centers, supported by resilient manufacturing output and continued growth in cross-border and domestic e-commerce. Corrugated packaging and paper-based protective materials dominate regional shipping supply demand, reflecting long-standing consumer and regulatory preference for recyclable formats.

The regulatory environment plays a defining role in shaping the European market. The European Union’s evolving packaging waste and sustainability framework, including stricter recyclability standards, labeling rules, and waste-reduction requirements, has increased compliance complexity but also created predictable, policy-driven demand for compliant shipping materials. These regulations are encouraging brand owners and logistics providers to standardize packaging formats and reduce material complexity, benefiting large integrated suppliers with diversified fiber portfolios.

Major European packaging companies such as Smurfit Kappa, DS Smith, and Mondi have responded by investing heavily in fiber-based innovation, including molded pulp protective packaging and high-strength lightweight containerboard. These investments support substitution away from plastic void fill while maintaining product protection standards. Consolidation activity, including mergers and capacity rationalization among large players, is reshaping competitive dynamics by improving pricing discipline and expanding geographic reach. As a result, Europe’s shipping supply market is increasingly characterized by scale advantages, regulatory alignment, and premium sustainable packaging solutions, rather than purely cost-driven competition.

Asia Pacific Shipping Supply Market Trends - Manufacturing Scale, Export Logistics & Rapid Capacity Expansion

Asia Pacific is projected to lead the global shipping supply market with an estimated 43.6% share and is the fastest-growing regional market, driven by large-scale manufacturing activity, export-oriented supply chains, and rapid expansion of e-commerce ecosystems. China remains the single largest national market, supported by its dominant role in global manufacturing and fulfillment. Japan, India, and ASEAN economies follow, each contributing to regional growth through rising domestic consumption and expanding logistics networks.

Significant investment in containerboard capacity and converting operations continues across the region. Chinese producers such as Nine Dragons Paper and Lee & Man Paper have expanded recycled containerboard output to support domestic e-commerce and export packaging demand. In India, rising online retail penetration and government-supported manufacturing initiatives are driving increased consumption of corrugated boxes and protective packaging, prompting both local and multinational suppliers to add regional production capacity. ASEAN countries are emerging as alternative manufacturing and fulfillment hubs, increasing demand for standardized shipping supplies.

Regulatory enforcement varies across Asia Pacific markets; however, restrictions on single-use plastics and national recycling targets are gradually influencing material transitions. Countries such as China and India have introduced phased plastic controls that encourage fiber-based alternatives, while Japan continues to emphasize material efficiency and recyclability through industry standards. As a result, the region is witnessing growing adoption of corrugated packaging and paper-based protective solutions, even as plastic materials remain relevant in moisture-sensitive and lightweight shipping applications. Asia Pacific’s combination of scale, cost competitiveness, and evolving sustainability policies positions it as the primary growth engine for the global shipping supply market.

Competitive Landscape

The global shipping supply market exhibits a hybrid structure, combining large global players with extensive scale and integration alongside numerous regional and local specialists. Consolidation is most pronounced at the containerboard and large-converter level, where vertical integration supports cost leadership and automation. Fragmentation persists in niche product categories such as poly mailers, foam inserts, and pallets. Competitive positioning depends on scale, sustainability credentials, service integration, and geographic reach.

Recent years have seen significant consolidation among leading packaging companies, resulting in expanded global footprints and enhanced technical capabilities. Large-scale mergers have reshaped the competitive landscape by combining containerboard production, converting operations, and innovation resources. Parallel investments in automated converting equipment and sustainable material development have increased throughput and customization capacity, widening the capability gap between global leaders and smaller regional players.

Leading companies emphasize scale expansion through consolidation, cost efficiency via vertical integration, premium positioning through sustainable and engineered packaging solutions, and service bundling that includes kitting, returns, and recycling. Differentiation increasingly depends on circular supply capabilities and integrated logistics partnerships.

Key Industry Developments

- In August 2025, Amcor introduced the AmFiber™ Performance Paper packaging in North America, prequalified for curbside recycling, providing manufacturers with a higher-performance and sustainable paper alternative to traditional shipping materials.

- In March 2025, Hinojosa Packaging Group and KHS Group introduced the Bottle Chip Carrier system, a fully recyclable cardboard solution that replaces traditional plastic film for bottle transit packaging, enhancing stackability and reducing carbon emissions across beverage supply chains.

Companies Covered in Shipping Supply Market

- International Paper

- WestRock

- Smurfit Kappa

- DS Smith

- Mondi

- Packaging Corporation of America

- Oji Holdings

- Nippon Paper Industries

- Nine Dragons Paper

- Lee & Man Paper

- Stora Enso

- Georgia-Pacific

- Pratt Industries

- Cascades

- Metsä Board

- Rengo Co., Ltd.

- Saica Group

- Mayr-Melnhof Karton

Frequently Asked Questions

The global shipping supply market is likely to be valued at US$46.5 billion in 2026.

By 2033, the shipping supply market is expected to reach US$ 99.6 billion.

Key trends include rising adoption of corrugated and fiber-based packaging, increasing use of engineered protective packaging for fragile goods, and growing automation in packaging and converting operations.

The corrugated paper/paperboard material segment is the leading category, accounting for approximately 40.5% of total market share, driven by cost efficiency, recyclability, and widespread application in e-commerce and industrial shipping.

The shipping supply market is projected to grow at a CAGR of 11.5% between 2026 and 2033.

Major companies include International Paper, WestRock, Smurfit Kappa, DS Smith, and Mondi.