- Beauty & Personal Care

- Seamless Masks Market

Seamless Masks Market Size, Share, and Growth Forecast, 2026 - 2033

Seamless Masks Market by Product Type (Face Masks, Bandanas, and Others), Material Type (Cotton Blend Masks, Silicone Masks, Fabric Masks, and Others), Price Range (Less than 10 US$, US$ 10 - US$ 20, US$ 20 - US$ 30, and More than US$ 30), Sales Channel (Online Retailing, Hypermarkets/Supermarkets, Modern Trade, Convenience Stores, Medical Stores, Others) and Regional Analysis for 2026 - 2033

Seamless Masks Market Size and Trends Analysis

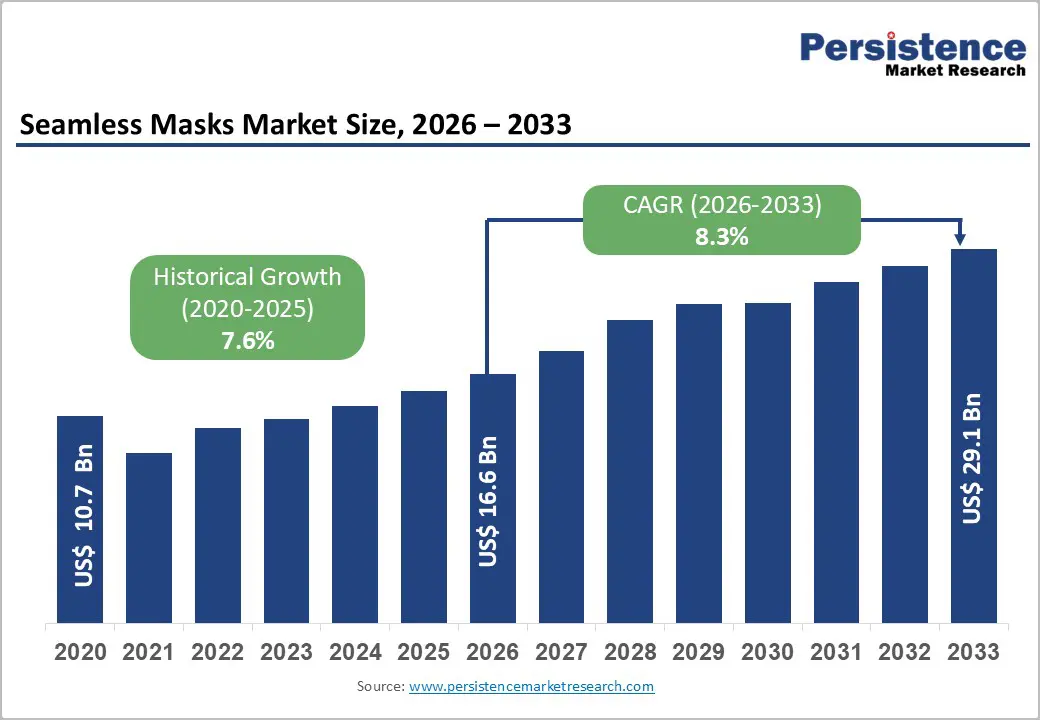

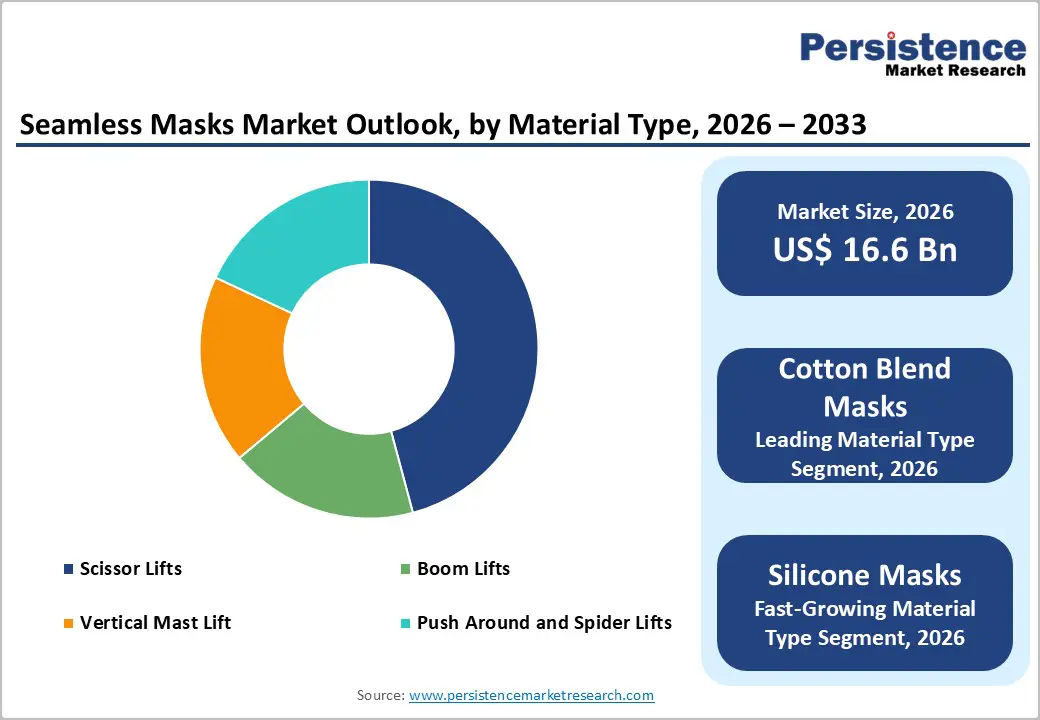

The global seamless masks market size is likely to be valued at US$ 16.6 billion in 2026 and is projected to reach US$ 29.1 billion by 2033, growing at a CAGR of 8.3% between 2026 and 2033.

This substantial growth trajectory reflects heightened consumer awareness of personal health and the importance of protective equipment, as well as advancements in manufacturing technologies. The market expansion is primarily driven by increasing urbanization, rising air pollution levels, growing emphasis on occupational safety standards, and escalating demand for comfortable, durable protective solutions. The transition from pandemic-driven reactive consumption toward sustained wellness-oriented purchasing patterns establishes seamless masks as essential lifestyle products across both developed and emerging economies.

Key Industry Highlights:

- Leading Product Type: Face masks dominate the product segmentation, with a revenue share above 40%, while bandanas are the fastest-growing product type, capturing lifestyle-conscious consumers. Cotton-blend masks command a material share above 30%, with silicone masks emerging as the fastest-growing material category, supporting advanced technology integration.

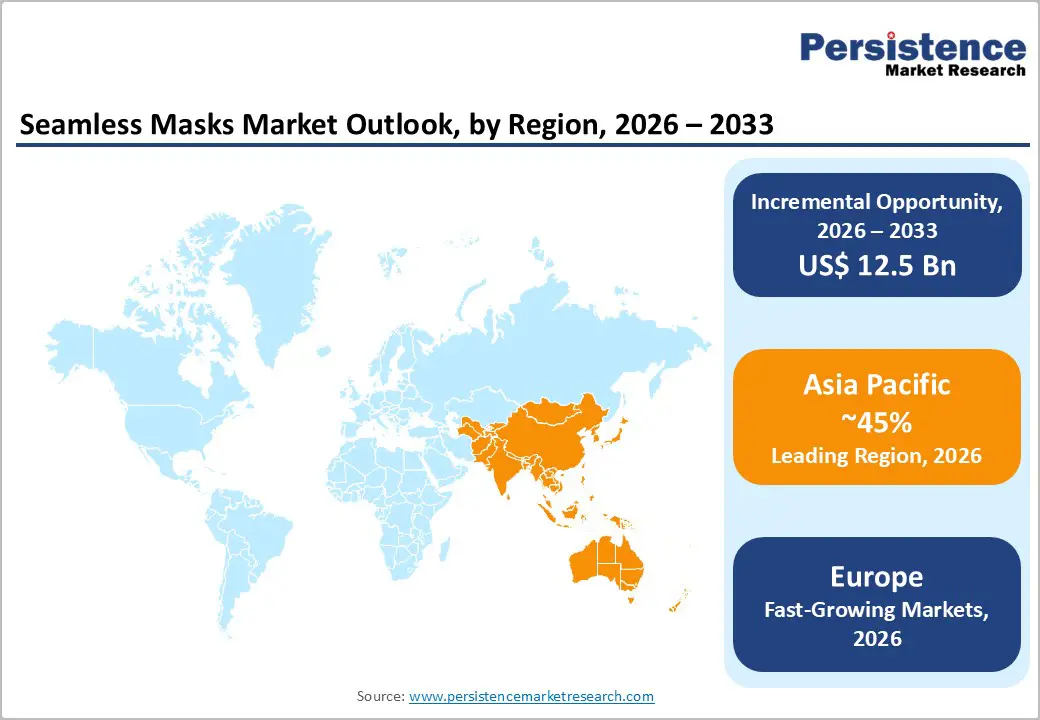

- Regional Leadership: Asia Pacific establishes global market leadership with a revenue share above 45%, while Europe is the fastest-growing region, reflecting premium consumer positioning and regulatory-driven institutional demand, particularly in Germany, the UK, and France.

- Leading Sales Channel: Online retailing channels dominate distribution with above 35% market share, while hypermarkets and supermarkets represent the fastest-growing sales channel, reflecting omnichannel retail evolution and consumer preference for convenient shopping experiences.

- Leading Price Range: The budget price segment (below US$ 10) maintains market dominance through volume penetration, while the US$ 10-US$ 20 mid-premium category demonstrates the fastest growth as quality-conscious consumers prioritize value optimization and extended product lifecycles.

- Strategic market developments emphasize innovation-driven product differentiation, regional manufacturing expansion in high-growth markets, and digital commerce platform optimization, positioning market leaders for sustained competitive advantage through technology integration and consumer preference building.

| Key Insights | Details |

|---|---|

| Seamless Masks Market Size (2026E) | US$ 16.6 Bn |

| Market Value Forecast (2033F) | US$ 29.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 8.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 7.6% |

Market Dynamics

Drivers - Rising Health Consciousness and Air Quality Concerns

Global health awareness has fundamentally reshaped consumer behaviour toward personal protective equipment, driving sustained adoption of seamless masks. The World Bank projects global healthcare investment in innovative protective gear to surpass US$15 billion by 2025, reflecting strong demand momentum. Air pollution remains the most critical driver, especially across the Asia-Pacific, where major cities in China, India, and Southeast Asia continue to record hazardous levels of particulate matter. This persistent exposure has led individuals, workplaces, and public institutions to shift from occasional to year-round mask usage, positioning seamless masks as daily essentials. Their superior comfort reduced ear pressure, improved breathability, and better aesthetics have further strengthened consumer preference over traditional mask formats.

According to the WHO, ambient air pollution in urban and rural regions contributes to strokes, heart disease, lung cancer, and acute and chronic respiratory illnesses. Additionally, 2.4 billion people remain exposed to high household pollution from cooking with biomass, kerosene, and coal. Combined indoor and outdoor pollution causes around 7 million premature deaths annually, underscoring the urgency of protective solutions. Ahead of the Second WHO Global Conference on Air Pollution and Health in March 2025, global health leaders are calling for rapid action as air pollution continues to drive a mounting noncommunicable disease burden worldwide.

Regulatory Framework Expansion and Occupational Safety Standards

Regulatory bodies worldwide are establishing increasingly stringent requirements for protective equipment specifications. The European Union's Personal Protective Equipment Regulation (EU 2016/425) and equivalent frameworks across North America have mandated comprehensive testing protocols, quality assurance certifications, and performance benchmarks for mask manufacturers. These regulations create structural market advantages for established manufacturers with certified production capabilities while establishing barriers to entry for non-compliant competitors. The European Agency for Safety and Health at Work reported that over 30% of European manufacturing firms upgraded PPE policies in 2023 to include enhanced protection standards. Occupational health regulations across developed economies continue to tighten, particularly in the healthcare and industrial sectors, driving institutional procurement volumes and establishing a consistent baseline demand irrespective of pandemic cycles.

Restraint - Supply Chain Vulnerabilities and Raw Material Cost Volatility

Global supply chain disruptions continue to affect the cost structures and production schedules of seamless mask manufacturers. Volatility in raw material prices, particularly for petrochemical-derived materials used in nylon, polyester, and spandex blends, directly affects production economics and pricing strategies. Sourcing risks for specialized materials, such as silicone compounds and performance fabrics, creates supply security challenges. Additionally, labor cost inflation in manufacturing hubs and logistics expenses adds structural pressure on profitability. These constraints disproportionately affect small and medium-sized enterprises lacking economies of scale or alternative supplier networks.

Opportunity - Sustainability-Driven Innovation and E-Commerce Expansion: Unlock High-Value Growth Opportunities in the Seamless Mask Market

Growing consumer preference for eco-conscious personal care products is creating strong opportunities for premium-priced, sustainable, seamless masks made from biodegradable or recycled materials. European surveys show that over 60% of consumers now favor reusable masks due to rising environmental concerns, enabling brands to target a high-value segment with superior margins and stronger loyalty. Innovations such as bio-cellulose masks, fermented-ingredient formulations, and advanced natural fiber composites further strengthen differentiation from low-cost commodity competitors while aligning with global sustainability expectations. At the institutional level, government-led sustainability initiatives and corporate environmental commitments are accelerating procurement shifts toward certified eco-friendly mask solutions, offering manufacturers a stable anchor demand.

Simultaneously, the rapid expansion of direct-to-consumer (D2C) e-commerce channels is reshaping the seamless mask market. Online platforms already capture more than 35% of market revenue, driven by broader digital adoption and consumer preference for convenient, personalized purchasing. E-commerce enables manufacturers to bypass intermediaries, reduce distribution costs, and retain greater margin value. Social media marketing, influencer collaborations, and data-driven engagement strategies allow emerging brands to scale quickly without heavy retail investments. Additionally, subscription-based delivery models present opportunities for recurring revenue generation and higher customer lifetime value, strengthening long-term competitiveness.

Category-wise Analysis

Product Type Insights

Face masks remain the dominant product segment in the seamless masks market, accounting for over 40% of total revenue. Their leadership is supported by sustained demand across healthcare, industry, sports, and daily consumer applications. Face masks offer an optimal balance of protection, long-wear comfort, and aesthetic appeal, making them the default choice for routine use. The normalization of mask-wearing during pandemic years continues to influence post-pandemic buying behavior, maintaining stable replacement cycles. Manufacturers further reinforce this dominance through ongoing investments in ergonomic designs, breathable materials, and style variations that enhance both performance and user appeal.

Meanwhile, Bandanas represent the fastest-growing product type, driven by their dual appeal as protective gear and lifestyle accessories. This segment is especially popular among younger consumers and fitness-oriented users who value multifunctionality. Bandanas offer versatility, serving as face coverings, headwear, or fashion elements, allowing brands to target broader lifestyle segments. Their growth rate substantially exceeds the market average, signaling a shift toward adaptable, style-driven protective products. Manufacturers are expanding offerings with vibrant color ranges, innovative patterns, and premium fabrics to attract consumers willing to pay higher prices for personalized and fashion-forward designs.

Material Type Insights

Cotton Blends Lead While Silicone Emerges as Fastest-Growing Seamless Mask Material

Cotton-blend masks remain the dominant material type in the seamless mask market, accounting for over 30% of total revenue in 2025, driven by their superior comfort, breathability, and consumer familiarity. Blends such as cotton-polyester and cotton-nylon offer enhanced moisture-wicking, reduced skin irritation, and easy machine-washability, making them ideal for prolonged daily use. Their strong global availability, mature supply chains, and cost-efficient production enable competitive pricing, further reinforcing market leadership.

Growing environmental awareness also boosts preference for cotton-based materials over fully synthetic alternatives. Manufacturers prefer advanced weaving techniques and functional coatings to improve filtration while preserving softness and comfort, positioning cotton blends as reliable, comfort-focused solutions.

In contrast, silicone masks represent the fastest-growing segment, driven by technology integration and premium durability. Silicone’s high elasticity supports an ergonomic, customizable fit, minimizing pressure points and enabling all-day usability. Its non-porous nature allows effortless cleaning and long-term reuse, significantly reducing per-use cost. Moreover, silicone masks enable embedded smart features, such as sensors, app connectivity, and real-time monitoring, which attract tech-savvy consumers and institutional buyers in healthcare and industrial environments. Backed by premium pricing and rising adoption, this segment is expected to record a CAGR well above the overall market.

Price Range Insights

The less-than-10 US$ budget segment dominates the market, contributing more than 35% of total revenue due to strong volume-driven demand, especially across emerging economies and highly price-sensitive consumer groups in 2025. Its affordability enables mass adoption among lower-income households and bulk institutional buyers, resulting in substantial cumulative revenue despite lower per-unit margins. Manufacturers operating in this segment focus heavily on production efficiency, streamlined supply chains, and cost optimization to remain competitive. The segment’s continued momentum is closely tied to rapid urbanization, population growth, and deeper product penetration in developing regions.

The US$10-US$20 mid-premium segment stands out as the fastest-growing category, supported by rising consumer preference for enhanced durability, comfort, and value-added features. This segment appeals to buyers seeking a superior balance between affordability and performance without transitioning into luxury-priced offerings. Growth rates significantly outpace both the budget and ultra-premium tiers, reflecting a broader shift toward quality-driven purchasing behavior. Products in this range often incorporate advanced materials, improved manufacturing processes, and differentiated functional attributes, allowing manufacturers to achieve stronger margins. Expansion is further fueled by increasing disposable incomes, evolving safety standards, and wider adoption of higher-quality protective equipment in both developing and mature markets.

Sales Channel Insights

Online retailing dominates the seamless mask market, accounting for more than 35% of revenue, establishing digital platforms as the leading commerce channel. Consumers increasingly prefer e-commerce due to convenience, broad product variety, transparent pricing, and flexible delivery options. Direct-to-consumer models further strengthen manufacturers’ margin capture, reduce dependency on intermediaries, and build long-term customer loyalty. Digital engagement tools, social media marketing, influencer partnerships, and targeted advertising enhance brand visibility and efficiently reach core demographic groups.

Consolidation around major marketplaces such as Amazon, Alibaba, and Flipkart provides massive reach but intensifies competition. Additionally, subscription-based replenishment and loyalty programs significantly improve retention and generate predictable recurring revenue.

Hypermarkets and supermarkets have emerged as the fastest-growing institutional sales channel, driven by consumers’ preference for one-stop convenience and the ability to evaluate products physically. These modern trade environments encourage impulse purchases and enable easy product comparison, supporting higher conversion rates. Their expansive geographic footprint across developed and emerging markets accelerates market penetration for seamless masks. The rise of private-label programs and exclusive retail partnerships enables retailers to offer differentiated assortments with improved margins. Strong promotional capabilities, in-store visibility, and cross-merchandising further stimulate demand. Growth is particularly pronounced in the Asia Pacific, where rapid urbanization continues to expand modern retail infrastructure.

Regional Insights and Trends

Asia Pacific Seamless Masks Market Trends

Asia Pacific dominates the seamless masks market, accounting for over 45% of global revenue in 2026. The region’s growth outpaces international averages, supported by China’s large-scale manufacturing ecosystem, India’s expanding middle class and urgent pollution-mitigation needs, and Southeast Asia’s rapid urbanization. Established consumer behavior in China, Japan, and South Korea, where masks function as both protective and lifestyle products, continues to reinforce high-volume demand. Competitive manufacturing advantages across the region, including cost-efficient production and integrated supply chains, strengthen price competitiveness and enable rapid market expansion.

Escalating air quality concerns significantly amplify demand. As of December 8, 2025, northwestern, central, and southeastern China reported “unhealthy” air quality with AQI levels above 150 and dangerously high PM2.5 concentrations. Although China’s 2024 national average PM2.5 level fell to 31 µg/m³ (“moderate”), it remains 6.2 times higher than the WHO guideline, placing the country among the world’s 25 most polluted nations. According to UNEP, nearly 75% of the Asia Pacific’s population is exposed to unsafe pollution levels. A new CCAC-supported report outlines 25 science-based policy actions that can deliver safe air quality for 1 billion people by 2030. In India, the cities of Delhi, Kanpur, and Ghaziabad exemplify severe PM2.5 exposure, and the AQLI 2025 update confirms that all residents breathe air exceeding WHO limits.

Europe Seamless Masks Market Trends

Europe represents the fastest-growing regional segment with substantial premium market positioning supported by stringent regulatory frameworks and health-conscious consumer demographics. The European protective face mask market was valued at US$ 1.69 billion in 2024 and is projected to grow at an 8.1% CAGR. Within the seamless masks subcategory, European market growth rates exceed overall regional averages, reflecting specific product format preferences. Germany, the United Kingdom, France, and Spain represent core European markets with established premium consumer segments and robust institutional procurement.

Germany leads European markets with 21.3% regional share, reflecting advanced healthcare systems, stringent occupational safety standards, and high per-capita spending on protective equipment. The UK represents the fastest-growing European market, driven by rising health consciousness and regulatory modernization. France and Spain demonstrate steady growth, supported by healthcare sector expansion and investments in industrial safety. The regulatory environment is characterized by comprehensive certification requirements under the EU Medical Device Regulation (MDR) and Personal Protective Equipment Regulation (PPER), creating significant barriers to entry while ensuring quality consistency. Sustainability initiatives across Europe are driving rapid adoption of reusable seamless masks, with market research indicating 60%+ European consumer preference for eco-friendly options. This segment supports premium pricing and enhanced margins, attracting manufacturer investment in sustainable material development.

Competitive Landscape

The seamless masks market exhibits moderate consolidation, with dominant positions held by multinational corporations such as Hanes, No Nonsense, and MoKo, alongside numerous regional competitors and emerging manufacturers. Market concentration remains relatively balanced between large-scale manufacturers with extensive distribution networks and specialized regional players addressing niche segments.

Leading companies typically command 15-25% combined market share, with the remainder distributed across mid-tier manufacturers and specialized suppliers. The market structure reflects moderate fragmentation rather than extreme consolidation, fostering competitive dynamism and incentives for innovation while preventing monopolistic market domination.

Competitive positioning centers on product differentiation through material innovation, design optimization, distribution network breadth, and brand recognition rather than pure cost leadership. Established manufacturers leverage brand equity, customer relationships, and manufacturing expertise to maintain market positions despite competitive new entrants. Regional competitors frequently compete through pricing advantages, localized product customization, and specialized distribution channels serving specific geographic or customer segments. Emerging startups introduce disruptive innovation and agile business models but typically lack the scale and distribution infrastructure of established competitors, constraining their overall market impact.

Key Developments:

- In 2021, TEAM Technologies Inc. acquired ViruDefense Inc., a producer of fully domestically manufactured N95 respirator masks. The financial terms of the acquisition were not disclosed.

- In 2020, Kim Kardashian introduced seamless face masks under her SKIMS brand, strengthening the line’s lifestyle and comfort-focused portfolio. As part of the launch, the brand donated 10,000 masks to charitable organizations.

- In 2020, UK-based seamless knitwear manufacturer Skinwear Ltd. released a range of antimicrobial seamless knitted masks to support global efforts to combat the COVID-19 pandemic.

Companies Covered in Seamless Masks Market

- LEIGH SHOECASE COMPANY

- Hanes

- No Nonsense

- MoKo

- KG GROUP OF NJ LLC

- WALLBIG

- Yangzhou Chuntao Accessory Co., Ltd.

- Hoo-Rag Bandanas

- Other Market Players

Frequently Asked Questions

The Seamless Masks market is estimated to be valued at US$ 16.6 Bn in 2026.

The primary demand driver for the seamless masks market is the rising need for comfortable, breathable, and irritation-free protective wear, driven by increasing air pollution, continued health and hygiene awareness, and consumer preference for reusable, aesthetics-focused mask solutions.

In 2026, the Asia Pacific region will dominate the market with an exceeding 45% revenue share in the global Seamless Masks market.

Among material types, cotton blend masks have the highest preference, capturing beyond 30% of the market revenue share in 2026, surpassing other material types.

LEIGH SHOECASE COMPANY, Hanes, No Nonsense, MoKo, KG GROUP OF NJ LLC, and WALLBIG are a few leading players in the Seamless Masks market.