- Smart Packaging

- Seam Tapes Market

Seam Tapes Market Size, Share, and Growth Forecast, 2026 - 2033

Seam Tapes Market by Product Type (Multi-layered, Single-layered, Others), Backing Material (PU/Polyurethane, PVC, Others), Application, and Regional Analysis for 2026 - 2033

Seam Tapes Market Size and Trends Analysis

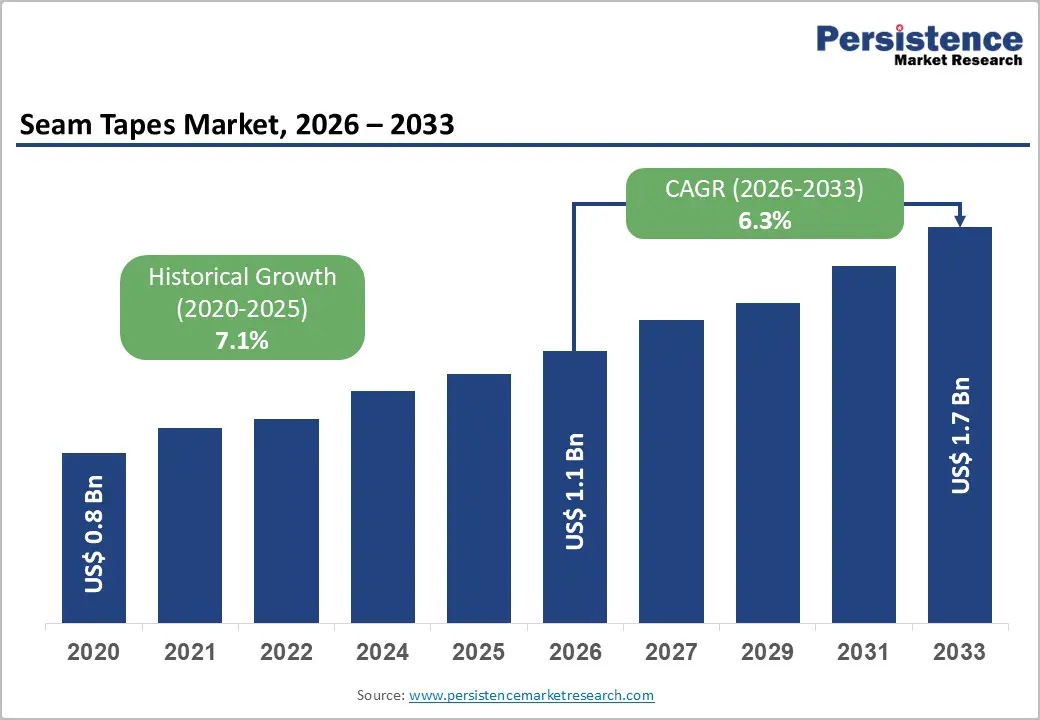

The global seam tapes market size is likely to be valued at US$1.1 billion in 2026 and is expected to reach US$1.7 billion by 2033, growing at a CAGR of 6.3% between 2026 and 2033, driven by expanding demand for waterproof and breathable garments, automation in garment manufacturing, and technical advancements in polyurethane (PU) and thermoplastic polyurethane (TPU) seam constructions. Although raw-material price volatility and regulatory compliance costs present structural risks, sustained demand across sportswear, medical textiles, and automotive interiors supports a stable mid-single-digit growth trajectory through 2033.

Key Industry Highlights:

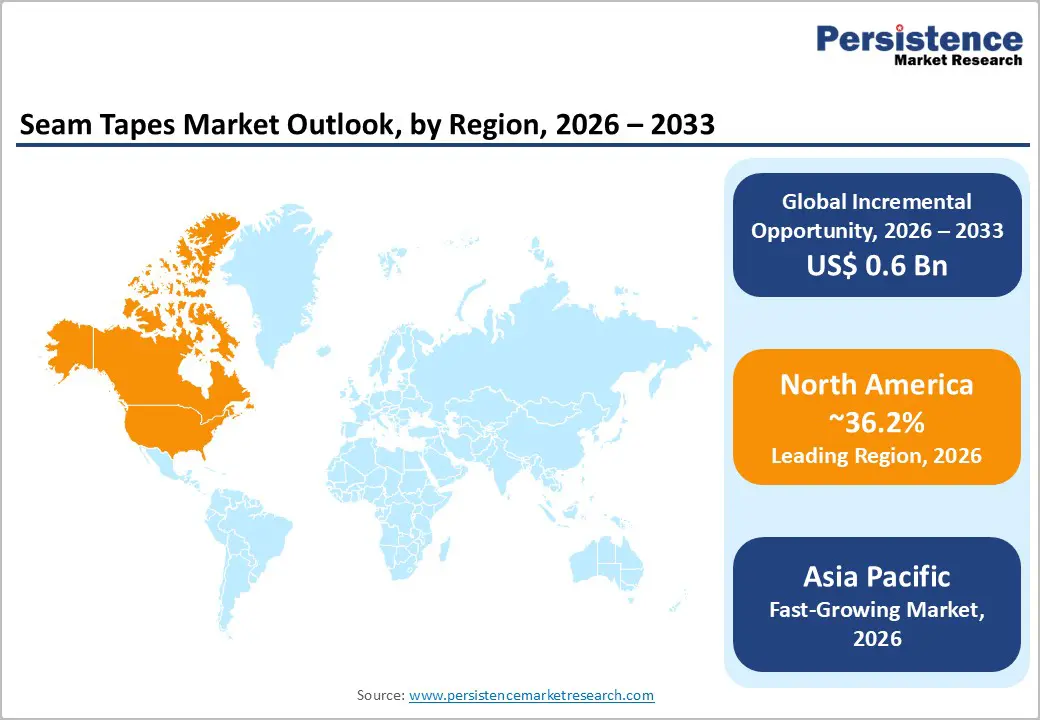

- Leading Region: North America is projected to lead the market with approximately 36.2% revenue share, supported by strong demand from U.S.-based performance apparel brands, automotive OEMs, and increasing nearshoring investments in technical textile converting capacity.

- Fastest-Growing Region: Asia Pacific is the fastest-growing regional market, driven by expanding garment export hubs in China, Vietnam, India, and Bangladesh, as well as increasing automation adoption in high-volume apparel manufacturing facilities.

- Investment Plans: Manufacturers across North America, Europe, and the Asia Pacific are investing in automation-compatible heat-activated seam tapes, low-VOC adhesive systems, and recyclable TPU film technologies, aligning with sustainability regulations and high-speed production requirements.

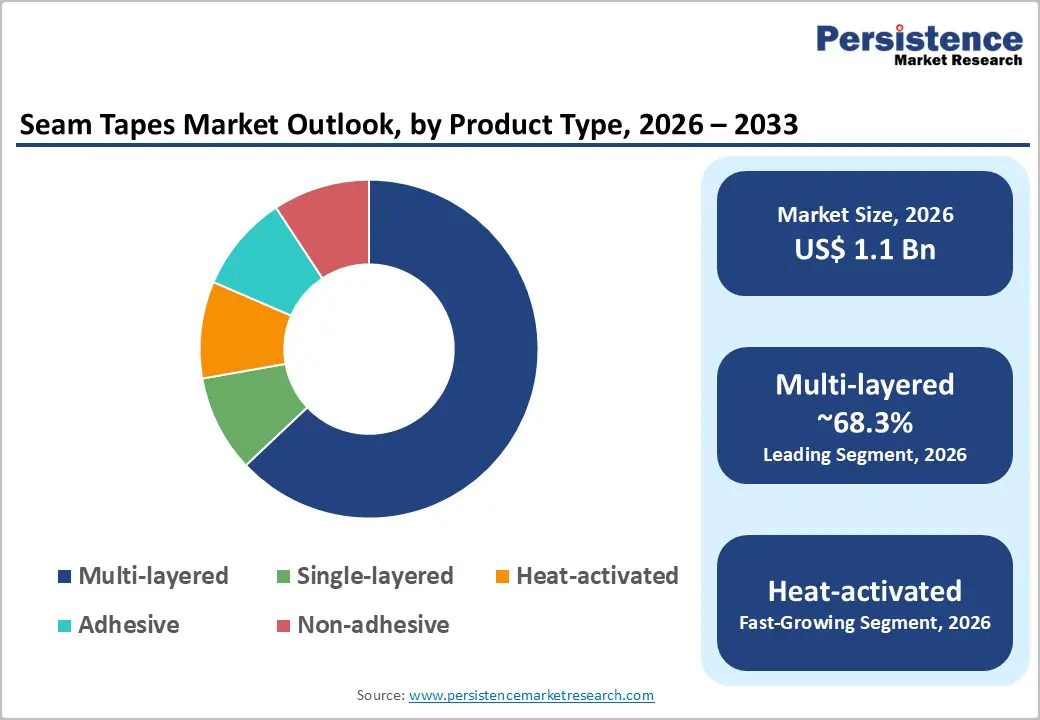

- Dominant Product Type: Multi-layered seam tapes are anticipated to account for 68.3% market share, owing to superior waterproofing performance, durability, and higher average selling prices in performance apparel and technical textile applications.

- Leading Backing Material: PU (Polyurethane)-backed seam tapes are expected to hold a 62.7% share, driven by their flexibility, breathability, and strong adhesion to stretch fabrics used in sportswear, intimate apparel, and protective garments.

| Key Insights | Details |

|---|---|

|

Seam Tapes Market Size (2026E) |

US$1.1 Bn |

|

Market Value Forecast (2033F) |

US$1.7 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.3% |

|

Historical Market Growth (CAGR 2020 to 2025) |

7.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising Demand for Performance and Waterproof Apparel

The increasing consumer preference for performance-oriented clothing is the most significant driver of demand for seam tape. Waterproof and breathable garments require sealed seams to maintain barrier integrity, particularly in outdoor apparel, sportswear, military garments, and rainwear. As participation in outdoor recreation and athletic activities continues to expand, brands are integrating seam-sealing technologies to differentiate their products by durability and comfort. Seam tapes enable efficient waterproofing compared with traditional liquid seam sealants, reducing drying time and labor costs in production. In addition, premiumization trends in athletic apparel increase the volume of tape used per garment, especially in multi-panel constructions. PU-backed seam tapes are widely specified due to their elasticity and wearer comfort. Manufacturers are shifting toward higher-performance, multi-layered seam tapes with breathable properties, increasing average selling prices, and enhancing supplier margins.

Manufacturing Automation and Process Efficiency

Automation in textile and footwear manufacturing significantly accelerates the adoption of seam tape. Heat-activated and pressure-sensitive adhesive (PSA) seam tapes support roll-to-roll processing and automated application systems, reducing human error and production downtime. Modern garment factories increasingly use programmable seam-sealing machines, particularly in the Asia Pacific and North America. Automated application improves bonding consistency and reduces rework rates, which directly lowers operating costs for large OEMs. The automotive industry also utilizes seam tapes in interior sealing to prevent water ingress, further expanding industrial demand. Capital investments in automated seam-sealing equipment create long-term procurement cycles for tape suppliers, improving demand predictability and strengthening supplier relationships with OEMs.

Material Innovation and Sustainability Advancements

Advances in backing films and adhesive chemistry are broadening the applications of seam tape. Innovations include ultra-thin PU films, low-temperature adhesives compatible with recycled polyester, and bio-based materials aligned with sustainability goals. Textile brands increasingly demand recyclable or reduced-VOC constructions. TPU and advanced acrylic systems improve abrasion resistance and chemical stability, supporting growth in footwear and industrial chemical protective clothing. Suppliers that develop compatible materials for stretch fabrics and technical laminates gain a competitive advantage. Technical innovation allows suppliers to command premium pricing, access regulated markets such as medical textiles, and differentiate products in performance apparel segments.

Barrier Analysis - Raw Material Price Volatility

Seam tapes rely on polymer-based backings such as PU, PVC, and TPU, as well as specialty adhesives derived from petrochemical feedstocks. Fluctuations in crude oil and resin pricing directly affect manufacturing costs. When polymer feedstock prices increase by 15–25% year-over-year, suppliers often experience margin compression before contractual price adjustments take effect. Converters operating under fixed-supply contracts may face temporary pressure on profitability. Cost pass-through mechanisms typically lag by six to twelve months, creating short-term financial strain and procurement uncertainty.

Regulatory and Environmental Compliance Costs

Regulations governing volatile organic compounds (VOCs), PFAS substances, and plasticizers require continuous reformulation of products. Compliance efforts increase R&D spending and certification timelines. Sustainability commitments by apparel brands also require the use of recyclable materials and traceable supply chains. Reformulation programs typically increase per-unit costs by 3–7% during transition phases. Certification and testing cycles can extend from six to eighteen months, delaying product commercialization and raising operational complexity.

Opportunity Analysis - Expansion in Medical and Surgical Apparel

The surgical and medical apparel segment represents the fastest-growing application category. Healthcare institutions require seam-sealed gowns and protective garments that ensure barrier protection against fluids and pathogens. Seam tapes designed for sterilization compatibility, biocompatibility, and low particulate emission can achieve premium pricing. As healthcare expenditure rises and surgical procedure volumes increase globally, demand for certified medical seam-sealing solutions is expected to outpace growth in traditional apparel. Strategically, suppliers that invest in ISO-compliant manufacturing and medical-grade documentation can access higher-margin procurement contracts.

Regional Converting in Emerging Markets

Asia Pacific and selected Latin American markets present opportunities for localized seam tape converting. Expanding textile manufacturing clusters in India, Vietnam, and Indonesia create demand for in-region supply to reduce lead times and shipping costs. Nearshoring strategies adopted by global brands encourage regional supplier development. Establishing technical support centers near garment manufacturing hubs improves customer retention and supports customized tape development. Investment in localized production facilities enhances supply chain resilience and strengthens long-term OEM relationships.

Category-wise Analysis

Product Type Insights

Multi-layered seam tapes are anticipated to account for approximately 68.3% of market share in 2026, maintaining their dominance across performance-driven apparel and technical textile applications. These constructions integrate a backing film (PU/TPU), pressure-sensitive or reactive adhesive layers, and protective release liners to deliver superior mechanical strength, hydrostatic resistance, and stretch compatibility. PU and TPU-based multi-layer tapes are extensively used in performance outerwear, ski jackets, rainwear, tents, and technical footwear, where waterproof integrity must withstand repeated flexing and laundering. For example, premium outdoor brands such as The North Face and Columbia Sportswear incorporate multi-layer seam sealing in high-performance jackets to meet waterproof ratings above 10,000 mm hydrostatic head. Higher average selling prices, greater tape consumption per garment (particularly in multi-panel athletic designs), and demand for durable waterproof-breathable constructions reinforce this segment’s value leadership.

Heat-activated seam tapes are projected to register the fastest growth, supported by compatibility with automated garment manufacturing lines and increasing regulatory pressure to reduce solvent emissions. These tapes eliminate VOC-intensive liquid sealants and remove drying or curing stages, shortening production cycles and lowering energy consumption. Manufacturers supplying global brands such as Nike and Adidas are integrating heat-activated sealing systems to enhance throughput consistency and reduce reject rates. Adoption is particularly strong in Asia-based contract manufacturing hubs where high-volume sportswear production demands speed and process standardization. Suppliers must balance established multi-layer portfolios with next-generation adhesive chemistries and automation-compatible heat-activated solutions to capture incremental growth and align with sustainability mandates.

Backing Material Insights

PU-backed seam tapes are anticipated to hold approximately 62.7% of the market share in 2026, driven by their optimal balance of flexibility, breathability, and strong adhesion to stretch and knit fabrics. PU’s soft hand feel and elastic recovery make it particularly suitable for sportswear, yoga apparel, medical protective garments, and intimate apparel where wearer comfort and mobility are critical. PU films can be manufactured in ultra-thin gauges while maintaining waterproof barrier performance, preserving garment drape and aesthetic quality. Major global material innovators such as Bemis Associates and Toray Industries supply advanced PU film technologies for seam sealing and bonding in performance textiles. The segment’s dominance is further supported by compatibility with laminated breathable membranes used in mid- to high-tier outdoor garments.

TPU-backed seam tapes are gaining strong momentum owing to superior abrasion resistance, hydrolysis stability, and recyclability potential compared to conventional PU. Their mechanical robustness makes them well-suited for heavy-duty outdoor gear, mountaineering apparel, protective workwear, and technical footwear. TPU tapes are increasingly specified in footwear manufacturing lines operated by global brands such as Puma, where durability and structural reinforcement are essential. Growth is also supported by the rising industry focus on mono-material garment concepts that enhance recyclability at end of life. Flexible production capabilities that enable rapid switching between PU and TPU backings, along with in-house film extrusion expertise, significantly enhance supplier responsiveness to evolving performance and sustainability requirements.

Regional Insights

North America Seam Tapes Market Trends - Premium Performance Apparel Innovation, EV Manufacturing Expansion, and PFAS-Compliant Adhesive Transition

North America is projected to account for approximately 36.2% of the market share in 2026, positioning it as the leading regional market. Demand is anchored by well-established outdoor and performance apparel brands, a technologically advanced automotive sector, and a growing medical and protective textiles industry. The region benefits from high consumer spending on premium waterproof apparel, technical footwear, and safety garments, reinforcing value-driven demand for high-performance seam tapes. The United States dominates regional consumption, supported by innovation-driven brands such as Patagonia and VF Corporation (parent company of The North Face and Vans), which emphasize durable waterproof constructions and responsible material sourcing.

Sustainability commitments, such as Patagonia’s expansion of PFAS-free durable water repellent (DWR) treatments, have accelerated the shift toward low-VOC, solvent-free seam sealing systems. In parallel, automotive OEMs, including General Motors, continue to invest in electric-vehicle production facilities across the Midwest and Southern U.S., increasing demand for interior sealing, battery enclosure insulation, and vibration-resistant bonding materials that incorporate advanced adhesive tapes.

Following supply chain disruptions, nearshoring trends have prompted U.S.-based apparel brands to diversify sourcing toward Mexico and domestic facilities. Investments in automated cutting and heat-sealing equipment by regional converters strengthen local finishing capacity, reducing lead times for performance garment manufacturers. Construction-sector diversification is also evident, with companies such as 3M expanding their advanced adhesive tape portfolios for building-envelope sealing and infrastructure applications. Suppliers that prioritize premium-grade films, PFAS-compliant adhesive technologies, regulatory certifications (including CPSIA and EPA-aligned standards), and localized warehousing will sustain competitive advantage in this mature yet innovation-intensive market.

Europe Seam Tapes Market Trends - REACH-Driven Chemical Compliance and Automotive-Integrated Advanced Sealing Systems

Europe represents a highly regulated and quality-driven seam tape market characterized by strong automotive engineering, performance apparel innovation, and stringent chemical governance. Germany leads regional demand, supported by automotive OEMs such as Volkswagen Group and BMW Group, which integrate advanced sealing systems into vehicle interiors, battery modules, and acoustic insulation assemblies. Industrial textiles and protective clothing manufacturers across Central Europe further contribute to steady consumption. The U.K. and France play influential roles in performance apparel and technical design.

Brands such as Arc'teryx (with significant European distribution expansion) and Decathlon continue to invest in waterproof product lines using heat-bonded seam constructions to improve garment durability while reducing stitch-based leak points. Europe’s regulatory framework, particularly REACH compliance under the European Chemicals Agency, directly shapes adhesive selection, limiting hazardous solvent content and accelerating adoption of recyclable TPU-based seam tapes.

Sustainability initiatives under the European Green Deal and circular textile strategies are influencing product development. Several European converters have expanded R&D in bio-based polyurethane films and mono-material garment systems to meet recyclability targets. Cross-border regulatory harmonization simplifies market access across EU member states; however, it raises compliance costs and increases documentation rigor for polymer and adhesive suppliers. Deep regulatory expertise, traceability transparency, and proven low-emission product portfolios are essential for market entry and sustained expansion within Europe’s compliance-intensive environment.

Asia Pacific Seam Tapes Market Trends - Export-Oriented Garment Manufacturing Scale and Automated Heat-Sealing Adoption

Asia Pacific is the fastest-growing regional market, driven by concentrated textile manufacturing ecosystems and the rising domestic apparel consumption. China, Vietnam, India, and Bangladesh serve as global garment export hubs, supplying international brands and creating consistent, high-volume demand for seam-sealing tapes used in rainwear, sportswear, and industrial uniforms. China remains the region’s largest production base, supported by vertically integrated textile supply chains and strong domestic brands such as Anta Sports, which has expanded high-performance outdoor and winter sports apparel lines in recent years.

Vietnam’s rise as a strategic sourcing destination for global brands, including Nike, has accelerated investment in automated seam-sealing machinery across contract manufacturing facilities. India and Bangladesh continue upgrading factory infrastructure under export competitiveness programs, strengthening demand for cost-efficient yet durable PU-based tapes. Japan plays a specialized role in high-value technical textiles, with companies such as Toray Industries leading innovations in advanced breathable membranes and polyurethane films that integrate with seam sealing systems. Factory modernization initiatives across Southeast Asia, supported by Industry 4.0 adoption, are increasing the uptake of heat-activated tapes compatible with high-speed automated lines.

Localized converting operations, competitive labor structures, and proximity to raw material suppliers provide cost advantages for regional tape manufacturers. Export-oriented garment production serving European and North American brands further reinforces volume growth. Capturing Asia Pacific growth requires a combination of scale manufacturing, cost efficiency, rapid technical support, and strong partnerships with OEM garment exporters and automated equipment suppliers.

Competitive Landscape

The global seam tapes market is moderately concentrated, with multinational adhesive and performance-material companies holding significant shares. Vertical integration across adhesive formulation and converting operations strengthens competitive positioning. Smaller regional converters compete on price and proximity to garment manufacturing clusters. Product differentiation is based on performance, compliance, and technical service capabilities. Market leaders prioritize innovation in adhesive chemistry, regional manufacturing expansion, and sustainability alignment. Technical service support and long-term OEM contracts differentiate suppliers. Co-development partnerships and automated application solutions represent emerging strategic models.

Key Industry Developments:

- In April 2025, Avery Dennison Corporation unveiled its new Flashing and Seaming Portfolio of pressure-sensitive adhesive tapes designed for building envelope applications, including waterproofing and sealing solutions for windows, doors, roofing, and insulation systems, aimed at strengthening its position in construction-related sealing markets.

Companies Covered in Seam Tapes Market

- Bemis Associates

- Toray Industries

- 3M

- H.B. Fuller

- Loxy AS

- Sealon Co., Ltd.

- Himel Corp.

- Gerlinger Industries GmbH

- DingZing Advanced Materials Inc.

- San Chemicals, Ltd.

- Framis Italia S.p.A.

- Protechnic S.A.

- Essentra plc

- Sika AG

- Avery Dennison Corporation

- Nitto Denko Corporation

- Coats Group plc

- Sympatex Technologies GmbH

Frequently Asked Questions

The global seam tapes market is estimated to be valued at approximately US$1.1 billion in 2026.

By 2033, the seam tapes market is projected to reach approximately US$1.7 billion.

Key trends include the shift toward multi-layered high-performance constructions (70% share), increasing adoption of heat-activated solvent-free adhesive systems, the rising demand for recyclable TPU-backed tapes, and integration of seam sealing technologies into automated garment production lines.

Multi-layered seam tapes represent the leading product segment, accounting for an anticipated 68.3% of market share, owing to superior waterproofing, durability, and higher average selling prices in performance outerwear and technical textile applications.

The seam tapes market is projected to grow at a CAGR of 6.3% approximately between 2026 and 2033.

Major companies include Bemis Associates, Toray Industries, 3M, H.B. Fuller, and Loxy AS.