- Food Ingredients & Additives

- Saccharin Market

Saccharin Market Size, Share, Trends, Growth, and Forecasts for 2025 - 2032

Saccharin Market by Product Type (Sodium Saccharin, Calcium Saccharin, Liquid Saccharin), Application (Food and Beverages, Pharmaceuticals, Tabletop Sweetener), by Distribution Channel (Offline, Online), and Regional Analysis for 2025 - 2032

Saccharin Market Size and Trends Analysis

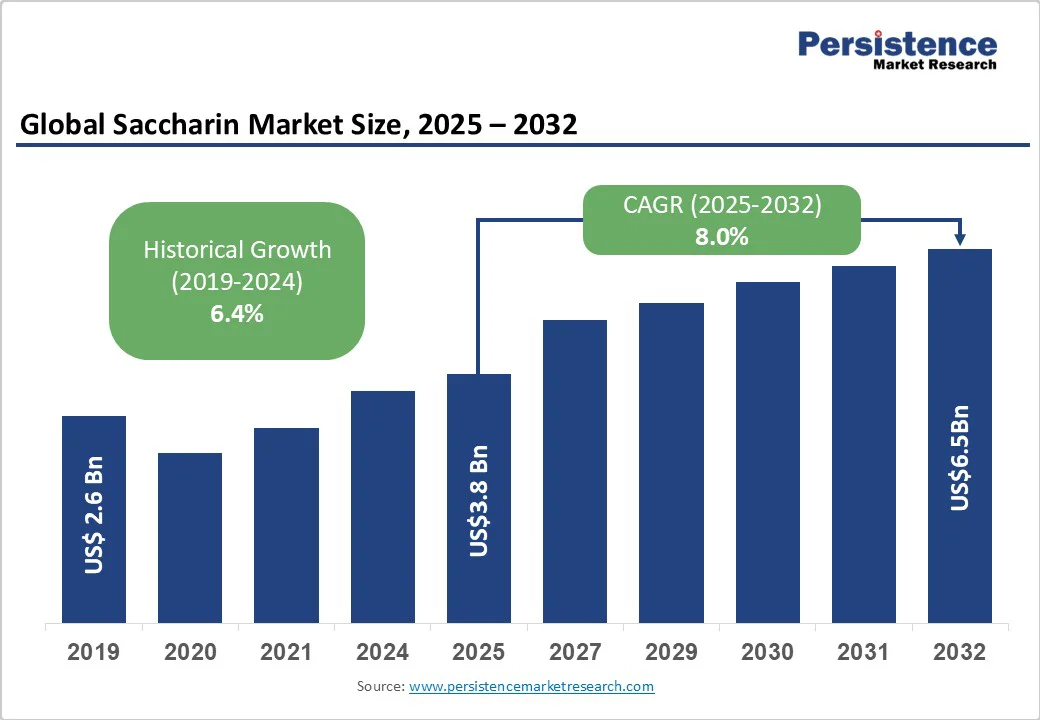

The global saccharin market size is expected to be valued at US$3.8 billion in 2025 and is projected to reach US$6.5 billion in 2032, growing at a CAGR of 8.0% during the forecast period of 2025-2032. The growth of the saccharin market is driven by rising health awareness and increasing demand for low-sugar products. The surge in lifestyle-related conditions such as obesity is prompting food companies to reformulate products with alternatives, including saccharin.

Key Industry Highlights:

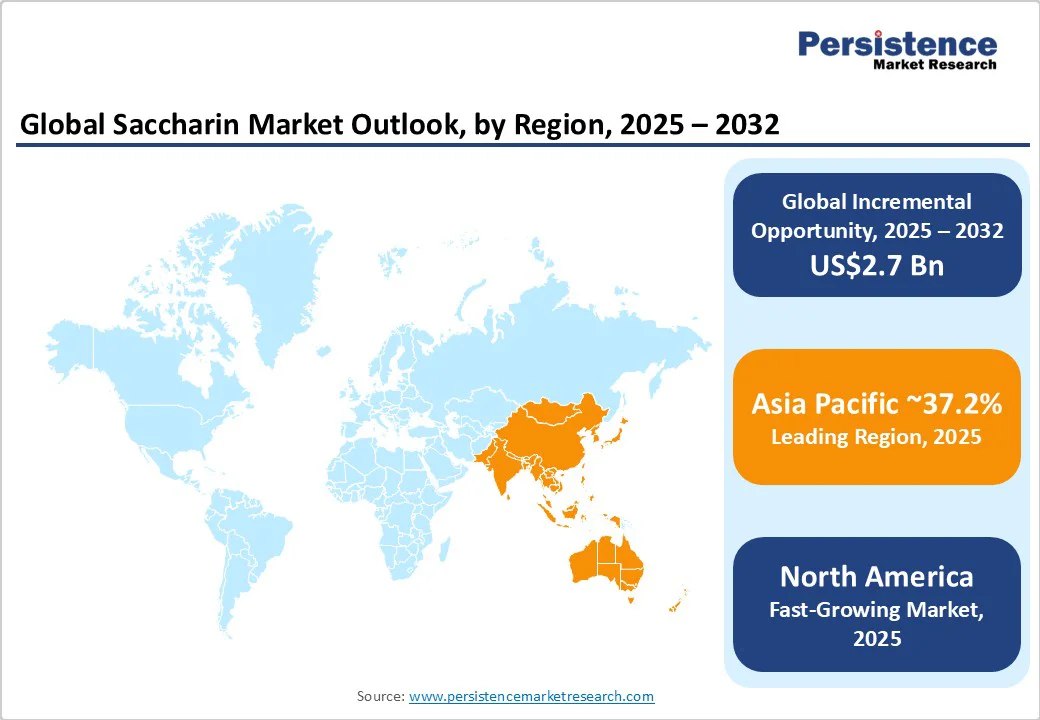

- Leading Region: Asia Pacific, with about 37.2% share in 2025, owing to China’s large-scale production and cost advantages.

- Fastest-growing Region: North America, backed by surging diabetes concerns and increasing sugar-reduction initiatives.

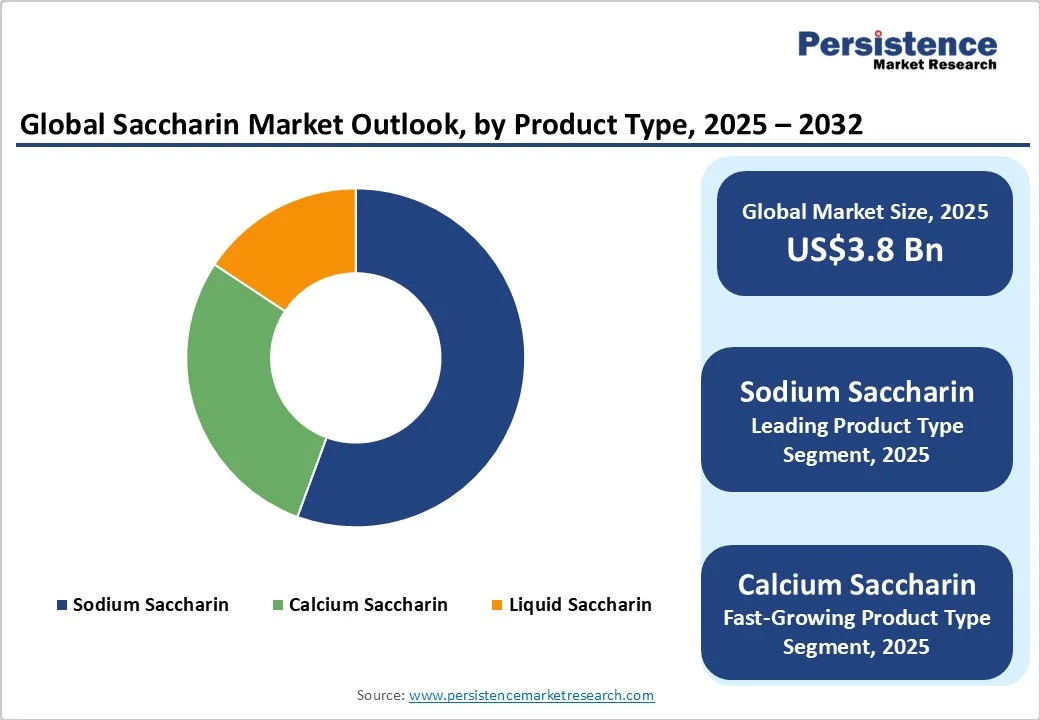

- Leading Product Type: Sodium saccharin holds nearly 55.6% share in 2025, as it dissolves easily and is heat stable.

- Dominant Application: Food and beverage, approximately 39.4% share in 2025, because the ingredient provides zero-calorie sweetness for reformulated products.

- Key Distribution Channel: Offline recorded about 71.3% share in 2025, due to product visibility, promotions, and consumer trust in familiar retail outlets.

- Recent Findings: In 2025, studies showed saccharin's potential in improving the efficacy of existing antibiotics. Research from Brunel University demonstrated that saccharin could revive old antibiotics by disrupting bacterial defenses.

| Key Insights | Details |

|---|---|

|

Saccharin Market Size (2025E) |

US$3.8 Bn |

|

Market Value Forecast (2032F) |

US$6.5 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

8.0% |

|

Historical Market Growth (CAGR 2019 to 2024) |

6.4% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Increasing Incidence of Lifestyle Diseases

The surging rates of obesity, diabetes, and metabolic disorders are prompting consumers and manufacturers to seek low- or no-calorie alternatives to sugar, which directly boosts saccharin demand. Saccharin provides intense sweetness without adding calories or affecting blood sugar, making it suitable for sugar-free food, beverages, and tabletop sweeteners.

Health authorities’ campaigns to reduce sugar intake in countries such as the U.S., Europe, and parts of Asia Pacific further reinforce its adoption. In 2024, several Europe-based soft drink brands reformulated products using saccharin blends to meet new sugar-reduction targets, reflecting the sweetener’s role as a practical solution for health-conscious consumers. The combination of rising health awareness and regulatory encouragement positions saccharin as a preferred ingredient in functional, low-sugar product lines.

Surging Application in Personal Care Products

Saccharin’s use in the personal care segment is expanding as it improves sweetness in products such as toothpaste, mouthwash, and chewable vitamins without adding sugar. Calcium saccharin, in particular, is favored for low-sodium formulations targeting health-conscious consumers or patients with hypertension.

In 2025, leading oral care brands in North America and Europe incorporated saccharin-based sweeteners into their sugar-free toothpastes and mouth rinses to enhance taste while maintaining safety standards. Beyond oral care, it is also used in cosmetics and flavored gels to improve palatability. The versatility and stability of saccharin in these formulations make it a crucial additive, driving steady growth in the personal care segment.

Barrier Analysis - Potential Impact on the Gut Microbiome

Emerging research suggests that saccharin may impact the gut microbiota, potentially influencing metabolism and overall health. Recent studies have shown that high consumption of artificial sweeteners, including saccharin, tends to alter microbial diversity, potentially contributing to glucose intolerance or other metabolic changes.

Bitter or Metallic Aftertaste Limiting Adoption

One of the key challenges for saccharin is its inherent bitter or metallic aftertaste, which can affect consumer acceptance in certain foods and beverages. This taste profile makes it less suitable as a standalone sweetener in sensitive products, including flavored dairy, baked goods, or fruit-based drinks.

Manufacturers primarily use saccharin in combination with other sweeteners, such as sucralose or stevia, to mask unpleasant flavors while maintaining cost advantages. For example, several beverage brands in Europe launched sugar-reduced sodas with saccharin-sucralose blends to improve palatability. Despite these strategies, taste concerns continue to hinder the broad adoption of saccharin in premium or natural-focused product lines.

Opportunity Analysis - Saccharin as a Versatile Scaffold in Medicinal Chemistry

The saccharin molecule is now recognized as a ‘privileged scaffold’ in drug discovery, providing a stable framework for designing novel compounds. Researchers are developing novel methods to modify and functionalize saccharin derivatives, which can enhance the bioavailability, selectivity, and pharmacokinetic properties of potential drugs.

In 2024, several studies demonstrated new synthetic routes that facilitate the easy incorporation of saccharin into heterocyclic compounds, enabling the creation of customized molecules for therapeutic applications. This versatility positions saccharin not just as a sweetener but as a valuable chemical building block in medicinal chemistry, creating opportunities for collaborations between chemical manufacturers and pharmaceutical companies.

Therapeutic Potential of Saccharin Metal Complexes

Recent research has revealed that saccharin, especially in its thio derivative form (thiosaccharin), can form metal complexes with significant biological activity. Studies demonstrated that these complexes show promising anticancer and antimicrobial effects in both in vitro and in vivo models.

Such findings suggest that saccharin-based metal complexes could serve as novel therapeutic agents, creating a niche market for pharmaceutical-grade saccharin derivatives. This trend provides chemical manufacturers with an opportunity to broaden beyond food and beverage applications into high-value pharmaceutical research.

Category-wise Analysis

Product Type Insights

Sodium saccharin is likely to account for nearly 55.6% share in 2025. It dissolves easily in water, making it ideal for beverages, syrups, and liquid pharmaceutical formulations. It is also cheaper to manufacture compared to other salts, which strengthens its position in large-scale applications such as soft drinks and tabletop sweeteners. A recent report by the European Food Safety Authority (EFSA) in 2024 reaffirmed its safety within approved limits. It gave food and beverage companies more confidence to continue using sodium saccharin for reformulated low-sugar products.

Calcium saccharin is predicted to witness a considerable CAGR through 2032 because it is gaining traction mainly in pharmaceuticals and personal care products, where sodium content is a concern. For example, it is increasingly used in sugar-free toothpaste and mouthwash formulations, since it provides sweetness without contributing sodium that may affect patients with hypertension. With global trends shifting toward low-sodium diets, calcium saccharin offers a niche alternative that supports health-focused product development, thereby augmenting its steady growth.

Application Insights

The food and beverage segment is predicted to account for a 39.4% share in 2025. Saccharin is a zero-calorie sweetener that helps companies reduce sugar while maintaining sweetness. Its stability under high temperatures and long shelf life make it ideal for soft drinks, baked goods, sauces, and syrups. Recent trends in sugar reduction, driven by health concerns over obesity and diabetes, have led to an increase in its use in reformulated products. For example, several Europe-based beverage brands in 2024 reformulated soft drinks using sodium saccharin blends to meet new sugar reduction targets while keeping costs low.

Saccharin is widely used in pharmaceuticals, primarily to enhance palatability in oral medications and chewable tablets. It is particularly important in pediatric and geriatric formulations, where taste can significantly impact compliance. Calcium saccharin is often preferred in these products due to low sodium content, which is suitable for patients with hypertension. In 2025, several pharmaceutical companies in North America and Europe began using saccharin-based blends in syrups and effervescent tablets to enhance sweetness without affecting the active ingredients, highlighting its crucial role in patient-friendly drug formulations.

Distribution Channel Insights

Offline channels are poised to account for nearly 71.3% of the share in 2025. This is because supermarkets, hypermarkets, and specialty stores are expanding rapidly, as consumers still prefer buying familiar brands in person, especially for food, beverages, and tabletop sweeteners. Promotions, in-store sampling, and visibility bolster purchase decisions. In the Asia Pacific and North America, retail chains introduced sugar-reduction sections and health-focused aisles in 2024, which prominently feature saccharin-based products, thereby boosting offline sales.

Online channels are speculated to exhibit a steady growth rate in the foreseeable future owing to their convenience, wide product variety, and access to specialty sweeteners that may not be available in local stores. E-commerce platforms also offer subscription models and bulk purchasing options, appealing to health-conscious consumers and institutional buyers. In Europe, 2025 saw a significant rise in online purchases of low-calorie and sugar-free products, with saccharin-based sweeteners included in curated ‘sugar-reduction kits’ sold by renowned online grocery platforms.

Regional Insights

Asia Pacific Saccharin Market Trends

In 2025, Asia Pacific is likely to account for nearly 37.2%. Saccharin production is centered in China, which accounts for the vast majority of supply and also leads regional exports. South Korea and India are smaller contributors, but India has recently increased its output to reduce reliance on imports and meet rising domestic demand. On the consumption side, China, South Korea, Pakistan, Bangladesh, Thailand, and India are key end users.

Thailand has emerged as a prominent importer, taking in large volumes to serve its food and beverage industries. Bangladesh and India are also showing steady increases in demand value, pushed by sugar-reduction trends and cost advantages of saccharin compared to natural sweeteners. Trade dynamics in Asia Pacific are shifting as export prices have fallen, pressuring producers to rely more on volume.

North America Saccharin Market Trends

In North America, saccharin use is primarily propelled by regulation and consumer attitudes. In the U.S., saccharin is approved for use in foods, drinks, and tabletop sweeteners, with well-known brands such as Sweet’N Low still utilizing it. Canada banned saccharin in food items decades ago, but recent reviews suggest regulators are reconsidering its wide use after new safety evaluations. The demand for saccharin in North America is further supported by growing concerns about obesity and diabetes.

Food and beverage companies are under pressure to reduce sugar, and saccharin remains one of the most cost-effective options for zero-calorie formulations. It is also used in pharmaceuticals and personal care products, where low cost and stability matter more than taste. At the same time, research findings are affecting consumer perception. A 2025 study published in Neurology linked heavy artificial sweetener intake, including saccharin, to quicken cognitive decline. Such reports have made consumers more cautious and have encouraged manufacturers to blend saccharin with alternatives such as stevia or sucralose to balance cost and health concerns.

Europe Saccharin Market Trends

In Europe, saccharin has recently been given a fresh regulatory review. In 2024, the European Food Safety Authority increased its acceptable daily intake level from 5 mg/kg to 9 mg/kg of body weight. This decision was based on updated studies that showed the earlier cancer concerns in animals are not relevant for humans. The review also highlighted that the way saccharin is manufactured matters.

Saccharin produced through the Remsen-Fahlberg process was considered safe, but the Maumee process raised questions due to possible impurities. Hence, regulators are recommending that only the Remsen-Fahlberg process should be used for saccharin approved in Europe. Authorities are also tightening purity standards. Calcium saccharin now requires meeting a 99% purity level, and strict limits for lead and arsenic contamination have been introduced. These changes aim to ensure safe products and more consistent quality across the market in Europe.

Competitive Landscape

The saccharin market is mainly influenced by a divide between bulk producers and specialized suppliers. China-based firms dominate the bulk production side, supplying large volumes at low costs to global markets. These manufacturers focus on price competition and account for a major share of exports worldwide. Competition is not only among saccharin producers but also with alternative sweeteners. Ingredients such as stevia, sucralose, erythritol, and new options, including tagatose, are putting pressure on saccharin suppliers by delivering better taste profiles or being marketed as healthier and natural.

Business Strategies

Leading saccharin companies follow cost leadership through bulk production in China, while global firms emphasize development in blends and regulatory compliance. Market expansion into pharmaceuticals and personal care is surging. Differentiators include purity grades, safety certifications, and taste-masking technologies. Emerging trends involve sweetener combinations and sustainable, traceable supply chains.

Key Industry Developments:

- In April 2025, the Institute of Food Technologists (IFT) released new resources to help the food and beverage industry in understanding and utilizing sugar alternatives, including saccharin. These resources aimed to support manufacturers in formulating products that meet consumer preferences for reduced sugar content.

- In April 2025, researchers at Shanghai Jiao Tong University introduced N-(acyldithio) saccharin, a stable and user-friendly disulfurating reagent. This compound was designed for efficient sulfur transfer in organic synthesis.

Companies Covered in Saccharin Market

- Salvi Chemical Industries Ltd.

- Henan Kaifeng Pingmei Shenma Xinghua Fine Chemical Co., Ltd.

- JMC Corporation

- Vishnu Chemicals Ltd.

- Shanghai Fortune Techgroup Co. Ltd.

- Kyung-In Synthetic Corporation

- Tianjin Changjie Chemical Co. Ltd.

- Sigma-Aldrich Corp (Merck KGaA)

- Productos Aditivos SA

- PMC Specialties Group

- Cumberland Packing Corp.

- Mubychem Group

- Anhui Suntran Chemical

- Foodchem

- Shree Vardayini Chemical Industries Pvt Ltd.

- Others

Frequently Asked Questions

The saccharin market is projected to reach US$ 3.8 Bn in 2025.

Rising health awareness and sugar-reduction initiatives are the key market drivers.

The saccharin market is poised to witness a CAGR of 8.0% from 2025 to 2032.

Development of saccharin derivatives for pharmaceuticals and increasing use in sugar-free beverages are the key market opportunities.

Salvi Chemical Industries Ltd., Henan Kaifeng Pingmei Shenma Xinghua Fine Chemical Co., Ltd., and JMC Corporation are a few key market players.