- Specialty & Fine Chemicals

- Pyrene Market

Pyrene Market Size, Share, and Growth Forecast 2026 - 2033

Pyrene Market by Concentration (Above 98%, 95% to 98%), Application (Dye Production, Synthetic Resin Manufacturing, Insecticides, Plasticizers, Other), and Regional Analysis for 2026 - 2033

Pyrene Market Size and Trend Analysis

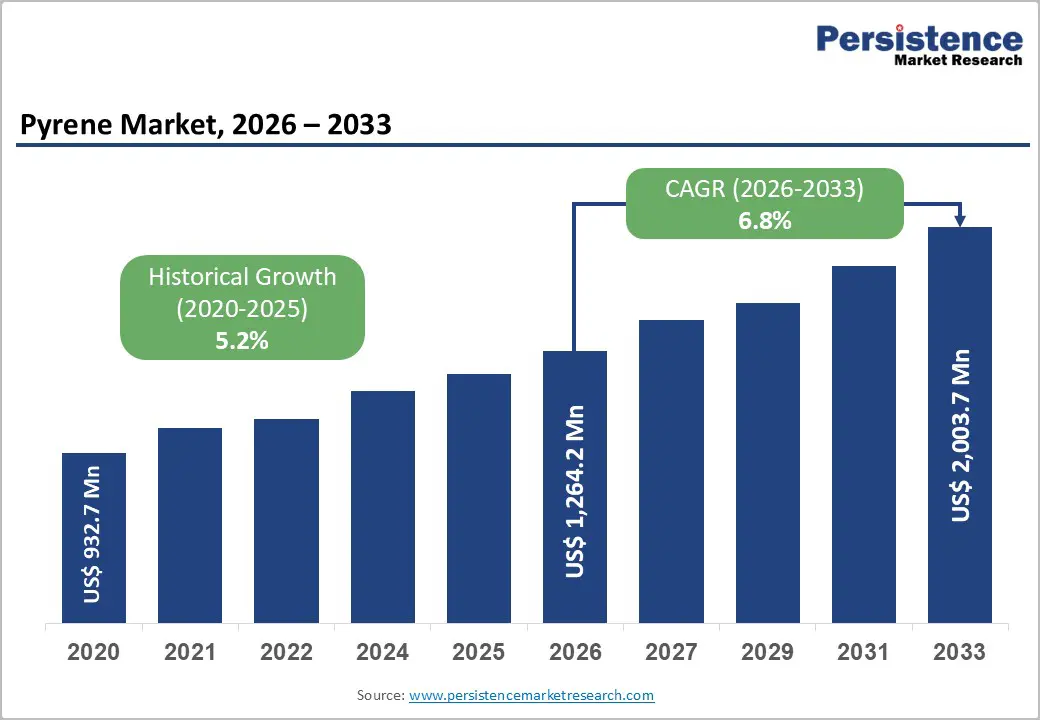

The global pyrene market size is supposed to be valued at US$ 1,264.3 Mn in 2026 and is projected to reach US$ 2,003.7 Mn by 2033, growing at a CAGR of 6.8% between 2026 and 2033.

This expansion is primarily driven by escalating demand from dye manufacturing and synthetic resin production industries, coupled with increasing adoption of pyrene derivatives as fluorescent probes in pharmaceutical research and environmental monitoring applications. The versatility of pyrene in producing naphthalene tetracarboxylic acid and its growing utilization in optical brightener manufacturing further accelerates market momentum across industrial applications.

Key Industry Highlights:

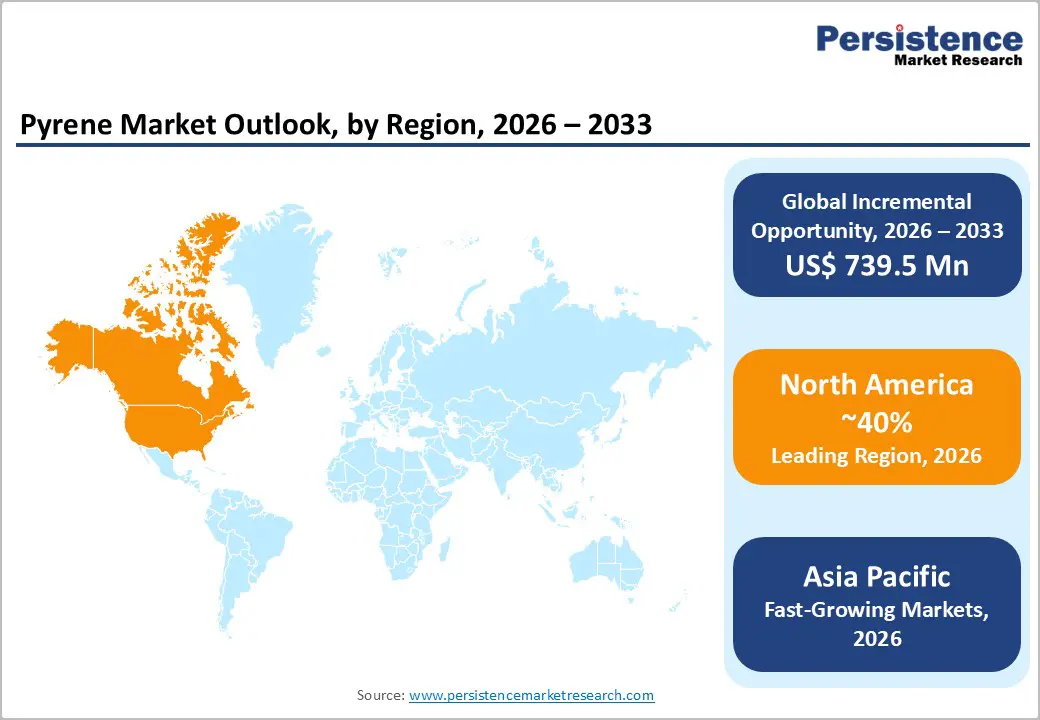

- Leading Region: North America maintains the largest pyrene market share, approximately 40% of global value, driven by robust pharmaceutical research infrastructure, advanced electronics manufacturing, and a strong regulatory framework that supports high-specification pyrene utilization in pharmaceuticals and optoelectronic applications, thereby sustaining regional market leadership.

- Fastest Growing Region: Asia Pacific demonstrates the fastest market growth at a projected CAGR exceeding 9% during the 2026-2033 forecast period, propelled by rapid industrialization, manufacturing capacity expansion in China and India, and increasing R&D investments across pharmaceutical and advanced materials sectors, creating substantial demand growth.

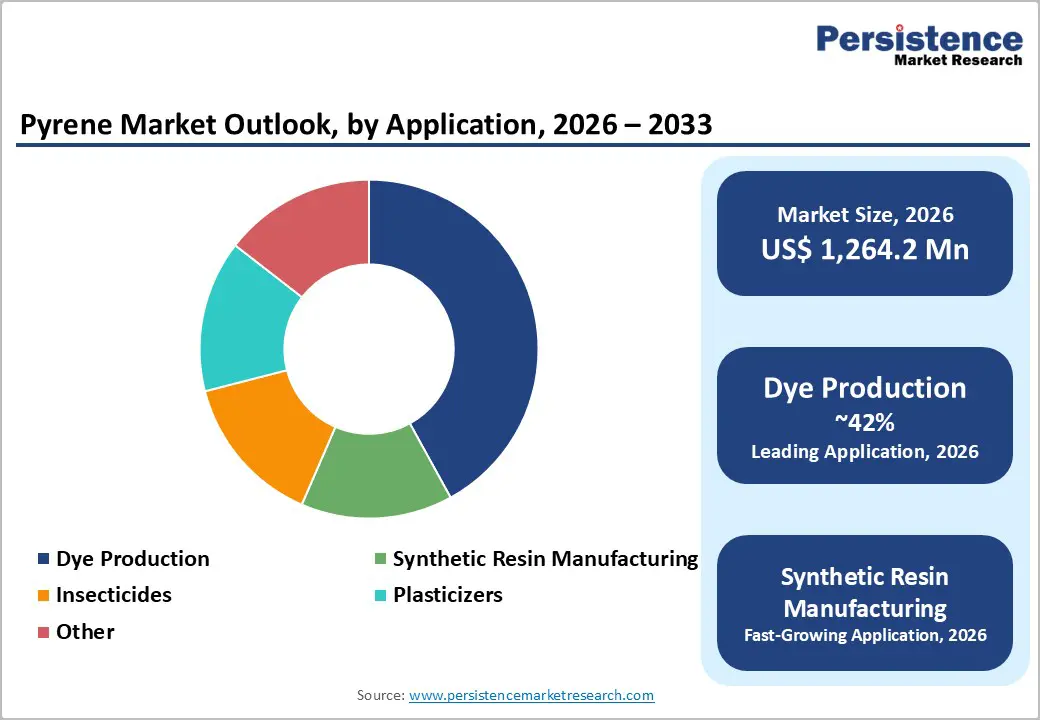

- Dominant Segment: Dye production is the dominant application segment, capturing approximately 42% of market demand, driven by pyrene's use as a chemical precursor for synthetic dyes, colorants, and fluorescent compounds across the textile, coating, and specialty materials industries, thereby sustaining market value generation.

- Fastest Growing Segment: Synthetic resin manufacturing for advanced electronics and optoelectronic applications represents the fastest-growing application segment, with accelerated expansion driven by OLED technology adoption, organic semiconductor development, and photovoltaic applications where pyrene derivatives enable superior device performance.

- Key Market Opportunity: Environmental Monitoring Revolution - Environmental monitoring and pollution control applications represent a high-potential growth opportunity supported by regulatory requirements for water quality assessment, air pollution monitoring, and soil contamination analysis, where pyrene-based detection systems enable unprecedented sensitivity and selectivity across environmental matrices.

| Key Insights | Details |

|---|---|

|

Pyrene Market Size (2026E) |

US$ 1,264.3 Mn |

|

Market Value Forecast (2033F) |

US$ 2,003.7 Mn |

|

Projected Growth CAGR (2026-2033) |

6.8% |

|

Historical Market Growth (2020-2025) |

5.2% |

Market Dynamics

Drivers - Rising Industrial Applications in Synthetic Resin and Plasticizer Manufacturing

Pyrene's utilization in synthetic resin manufacturing and plasticizer production is a significant growth catalyst, supported by expanding construction and automotive sectors that require advanced polymer materials. As a polycyclic aromatic hydrocarbon derived from coal tar distillation, pyrene plays a vital role in producing specialized resins with enhanced thermal stability and mechanical properties. According to BAIINFO data, China's coal tar distillation industry, which had approximately 27.4 million tonnes per year of capacity as of 2021, provides substantial raw material for pyrene extraction. The country's coal tar production reached approximately 20 million tons in 2018, establishing a robust supply chain for pyrene-based derivatives.

Furthermore, pyrene derivatives are increasingly used in epoxy resins for electrical insulation and as additives in electrical insulating oils, driven by growing electrical and electronics manufacturing activities. The compound's integration into plasticizer formulations enhances the flexibility and durability of polymer products, catering to diverse industrial requirements across packaging, construction materials, and automotive components.

Expanding Demand from Dye and Optical Brightener Industries

The pyrene market is experiencing robust growth driven by its critical role in producing fluorescent dyes and optical brightening agents, which are essential across textile, paper, and detergent applications. Pyrene serves as a precursor for synthesizing pyranine and other fluorescent whitening agents with strong ultraviolet absorption, making them indispensable for enhancing product aesthetics. The optical brightener market has witnessed significant growth, driven by increasing demand for enhanced whiteness in textiles and paper products worldwide. Furthermore, pyrene's strong fluorescence emission spectrum sensitivity to solvent polarity positions it as a preferred molecular probe in pharmaceutical research, where it aids in studying protein conformation and drug formulation systems. The chemical industry's shift toward high-performance fluorescent compounds, particularly biphenyl- and benzoxazole-based derivatives, has driven increased pyrene consumption in specialty coating and laser dye applications.

Restraints - Stringent Regulatory Restrictions and Environmental Compliance Requirements

The European Union's REACH Regulation (EU) 2025/660, effective from April 22, 2026, imposes significant restrictions on polycyclic aromatic hydrocarbons (PAHs), including pyrene, in certain applications. The regulation restricts pyrene and seventeen other PAHs in clay targets used for shooting to concentrations not exceeding 0.005% by weight (50 mg/kg). Furthermore, pyrene's classification as a persistent, bioaccumulative, and toxic (PBT) and very persistent and very bioaccumulative (vPvB) substance under REACH Annex XIV requires authorization for placement on the market, creating administrative and compliance burdens for manufacturers.

FDA regulations in the U.S. impose a limit of 0.25 mg/kg on benzo (a) pyrene for carbon black food-contact materials, restricting its use in food-contact applications. These regulatory constraints reduce the addressable market segments and increase compliance costs for manufacturers, thereby limiting market expansion in certain application domains and creating barriers to market entry for smaller producers.

Supply Chain Volatility and Raw Material Price Fluctuations

The pyrene market faces considerable challenges due to volatility in raw material prices, particularly coal tar and crude oil derivatives, which significantly influence production economics and pricing stability. Geopolitical tensions and trade disruptions further exacerbate supply chain uncertainties, impacting the sourcing and transportation of essential inputs.

The market’s reliance on a limited number of specialized producers heightens supply risks, as any operational disruptions can lead to temporary shortages. In China, the coal tar deep-processing sector remains fragmented, with the top ten producers holding less than 30% market share, increasing vulnerability to market shocks. Furthermore, environmental regulations mandating production curtailment and capacity optimization have constrained coal tar output, intensifying supply-side challenges and limiting manufacturers’ ability to maintain consistent raw material availability.

Opportunity - Explosive Growth in Environmental Monitoring and Pollution Control Applications

Environmental monitoring and remediation present a significant growth opportunity for the pyrene market, driven by stringent regulatory requirements for water quality, air pollution, and soil contamination assessments. Pyrene, classified as a persistent organic pollutant (POP), serves as a key indicator of combustion-related and petroleum-derived contamination in environmental matrices. Advanced research highlights the effectiveness of silicon nanowire-based optical sensors with pyrene-functionalized receptors, achieving detection limits as low as 2 × 10 ppb and quantification at 0.01 ppb across an extensive dynamic range.

Regulatory authorities in North America and Europe mandate the detection of pyrene in drinking water, wastewater, and ecological systems, thereby reinforcing demand for high-precision analytical technologies. Government investments in environmental protection and pollution control further stimulate the adoption of pyrene-based detection systems by consulting firms, water treatment facilities, and regulatory agencies.

Expansion in Pharmaceutical and Advanced Material Applications

Emerging applications in pharmaceutical formulations and advanced electronic materials offer significant growth prospects for the pyrene market, driven by technological advances and innovation-driven sectors. The pharmaceutical industry exhibits rising demand for pyrene derivatives as fluorescent probes in drug development, particularly for analyzing molecular interactions and protein conformational changes.

Pyrene’s sensitivity to environmental polarity enhances its utility in determining micellar concentrations and studying biological systems, a trend supported by increasing biopharmaceutical research investments. Merck KGaA’s €2 billion R&D expenditure in 2024 underscores the industry’s commitment to innovative chemical solutions, including high-potency APIs and novel modalities such as cell and gene therapies. Concurrently, pyrene’s role in organic electronics and semiconductor technologies is expanding, positioning it as a critical component in next-generation photoluminescent coatings and smart material applications.

Category-wise Analysis

By Concentration Insights

The above 98% concentration segment dominates the global market, accounting for nearly 65% of the total share due to stringent purity requirements in pharmaceutical, research, and advanced electronics applications. These high-purity grades command premium pricing as they are indispensable for specialized uses where even minimal impurities can compromise product performance or research accuracy. Pharmaceutical manufacturers typically require pyrene certified under US Pharmacopeia (USP) or European Pharmacopoeia (EP) standards with purity levels of at least 99.0% for intermediates and analytical reference materials.

Similarly, research institutions and academic laboratories specify ultra-pure grades for fluorescence spectroscopy, electronic device fabrication, and critical scientific studies. Leading producers such as Merck KGaA, BASF SE, and Haihang Industry Co., Ltd. employ advanced purification technologies to ensure quality differentiation and regulatory compliance.

By Application Insights

Dye production constitutes the largest application segment in the pyrene market, representing approximately 42% of global demand. This dominance is driven by pyrene’s role as a key chemical precursor in the manufacture of synthetic dyes, colorants, and fluorescent compounds. Through oxidation, pyrene converts to pyrene quinone, enabling the production of reducing dyes widely used in textiles, paper, and specialty coatings.

The global dyes and pigments industry continues to expand, particularly in Asia-Pacific markets where textile manufacturing is growing rapidly. Pyrene derivatives are essential in synthesizing azo, reactive, and direct dyes for coloring synthetic fibers, natural textiles, and specialty materials. Manufacturers rely on pyrene to develop advanced formulations that meet stringent standards for color fastness, brightness, and environmental compliance, supporting growth in apparel, automotive interiors, and consumer goods.

Regional Insights

North America Pyrene Market Trends

North America holds the largest share of the global pyrene market, accounting for approximately 40% of the total value. This leadership is supported by the region’s advanced pharmaceutical infrastructure, strong research and development ecosystem, and prominent position in electronics and semiconductor manufacturing. The expanding U.S. pharmaceutical sector drives significant demand for pyrene-based compounds used as intermediates, fluorescent probes, and reference standards. Maintained funding from the National Institutes of Health sustains requirements for high-purity pyrene across academic institutions, clinical research organizations, and pharmaceutical manufacturers.

Furthermore, the presence of leading suppliers such as Merck KGaA and BASF SE ensures reliable supply and technical support. Growing adoption of pyrene in OLED displays, organic semiconductors, and photovoltaic devices, combined with favorable regulatory frameworks, reinforces North America’s status as the highest-value market segment.

Europe Pyrene Market Trends

Europe ranks as the second-largest pyrene market, contributing approximately 30% of global demand. Market dynamics are shaped by stringent regulatory frameworks, a strong focus on sustainable chemistry, and specialization in high-performance materials. The European Union’s REACH Regulation enforces comprehensive chemical safety standards, with the recent amendment (EU 2025/660) imposing restrictions on polycyclic aromatic hydrocarbons in specific applications. Despite these measures, pyrene remains authorized for pharmaceutical, research, and advanced electronics uses, subject to compliance with registration and documentation requirements.

Leading companies, including Merck KGaA, maintain significant regional presence, supported by the European Green Deal’s emphasis on climate neutrality and green chemistry. Research institutions across Germany, the UK, France, and Spain drive demand for pyrene in spectroscopy, environmental monitoring, and electronic material development, reinforcing Europe’s role as an innovation hub.

Asia Pacific Pyrene Market Trends

Asia Pacific is projected to be the fastest-growing regional market for pyrene, with a CAGR exceeding 9% during the forecast period. This growth is fueled by rapid industrialization, large-scale manufacturing expansion, and rising investments in research and development. China leads the region with its extensive chemical manufacturing infrastructure, coal tar-derived feedstock availability, and strategic focus on advanced materials, semiconductors, and pharmaceutical innovation.

India demonstrates strong potential, supported by expanding R&D capabilities, pharmaceutical production, and government initiatives such as the Production-Linked Incentive (PLI) scheme, which encourages investment in pyrene manufacturing and purification technologies. Japan and South Korea sustain demand through advanced electronics and semiconductor sectors, while Southeast Asian nations, including Vietnam and Indonesia, offer emerging opportunities driven by industrial growth, favorable labor costs, and increasing foreign direct investment.

Competitive Landscape

The global pyrene market is moderately consolidated, dominated by leading multinational chemical corporations and specialized fine chemical manufacturers with extensive production capacity and global distribution networks. Key players such as Merck KGaA, BASF SE, Haihang Industry Co., Ltd., and Henan Tianfu Chemical Co., Ltd. collectively create oligopolistic structures that shape pricing and competitive strategies. Merck KGaA leverages its diversified portfolio to cross-sell pyrene products while maintaining premium positioning through superior quality and technical support. BASF SE focuses on integration strategies, including acquisitions and proprietary synthesis technologies, to enhance cost efficiency. Market consolidation is accelerating as smaller firms struggle to achieve scale, driving mergers, digital transformation, and customized product development. Investments in R&D for advanced applications and sustainable production methods remain critical for long-term competitiveness.

Key Market Developments

- October 2025: Merck KGaA announced a definitive agreement to acquire JSR Life Sciences' chromatography business for enhancing downstream purification solutions for antibody therapies and biopharmaceutical manufacturing, demonstrating strategic emphasis on life sciences applications incorporating pyrene derivatives and related chemical compounds.

- April 2025: Regulation (EU) 2025/660 amended REACH Annex XVII, restricting 18 polycyclic aromatic hydrocarbons, including pyrene in clay targets to 50 mg/kg (0.005% by weight) concentration limits, effective from April 22, 2026, reflecting regulatory evolution impacting certain pyrene applications.

- December 2024: BASF SE conducted its Research Press Briefing 2025, highlighting annual research and development investments of approximately €2 billion in 2024, with a focus on sustainable chemical production, including methane pyrolysis technology development in collaboration with ExxonMobil.

Top Companies in the Pyrene Market

Merck KGaA (Darmstadt, Germany) represents a global market leader with comprehensive pyrene product portfolios spanning research-grade compounds, pharmaceutical intermediates, and specialized fine chemicals. The company's Science & Lab Solutions business unit recorded sales of €4.7 billion in 2024, serving academic institutions, research organizations, and pharmaceutical manufacturers requiring high-specification pyrene compounds and related analytical materials. Merck's vertical integration across production, purification, quality assurance, and customer support establishes competitive advantages in complex regulatory environments.

BASF SE (Ludwigshafen, Germany) operates as a diversified chemical corporation with substantial pyrene production capacity and specialization in specialty chemicals and advanced materials. The company's process solutions and pharmaceutical manufacturing services integrate pyrene and pyrene-derived compounds into customized formulations supporting customer innovation initiatives across the pharmaceutical and electronics sectors. BASF's global supply chain infrastructure and technical expertise position the company as a reliable supplier for global pyrene demand.

Haihang Industry Co., Ltd (Jinan, China) established itself as a leading pyrene manufacturer and supplier serving pharmaceutical, research, and specialty chemical industries across Asia Pacific and global markets. The company's integrated operations spanning research, production, and quality control enable competitive pricing and rapid response to customer requirements, sustaining market share growth in emerging markets and cost-sensitive application segments.

Companies Covered in Pyrene Market

- Merck KGaA

- BASF SE

- Haihang Industry Co., Ltd

- Henan Tianfu Chemical Co., Ltd

- BOC Sciences

- Sourcechem Co., Ltd.

- Otto Chemie Pvt. Ltd.

- NATIONAL ANALYTICAL CORPORATION

- Tokyo Chemical Industry (India) Pvt. Ltd.\

- China Qingdao Hongjin Chemical Co., Ltd.

- Spectrum Chemical

- Biosynth

- Carbone Scientific Co., Ltd.

- Glentham Life Sciences

- Thermo Fisher Scientific Inc.

- Kishida Chemical Co., Ltd.

- Sigma-Aldrich

Frequently Asked Questions

The global pyrene market is projected to be valued at US$ 1,264.3 million in 2026 and is expected to expand to US$ 2,003.7 million by 2033, representing substantial growth opportunities across pharmaceutical, research, and electronics applications during the forecast period.

Primary demand drivers include surging pharmaceutical research applications requiring high-purity pyrene for drug development, expanding electronics sector adoption of pyrene-based organic semiconductors and OLEDs for next-generation display technologies, and increasing environmental monitoring requirements necessitating pyrene-based analytical systems for pollution detection.

Dye production represents the dominant application segment, capturing approximately 42% of the global pyrene market demand, driven by pyrene's utilization as an essential chemical precursor for synthetic dyes, colorants, and fluorescent compounds across textile, coating, and specialty materials industries.

North America maintains the largest pyrene market share at approximately 40% of global value, while Asia Pacific demonstrates the fastest growth rate, exceeding 9% CAGR during the 2026-2033 forecast period, driven by rapid industrialization and manufacturing expansion in China and India.

Environmental monitoring and pollution control applications represent significant growth opportunities supported by regulatory requirements for water quality assessment, with pyrene-based detection systems enabling unprecedented sensitivity in environmental analysis, while advanced electronics applications in OLED and organic photovoltaics create high-value opportunities.