- Pharmaceuticals

- Psychedelic Drugs Market

Psychedelic Drugs Market Size, Share, and Growth Forecast, 2026 - 2033

Psychedelic Drugs Market by Drug Type (Ketamine, Psilocybin, Lysergic Acid Diethylamide (LSD), 3,4-Methylenedioxymethamphetamine (Ecstasy), Others), Application (Major Depressive Disorder, Others), And Regional Analysis for 2026 - 2033

Psychedelic Drugs Market Size and Trends Analysis

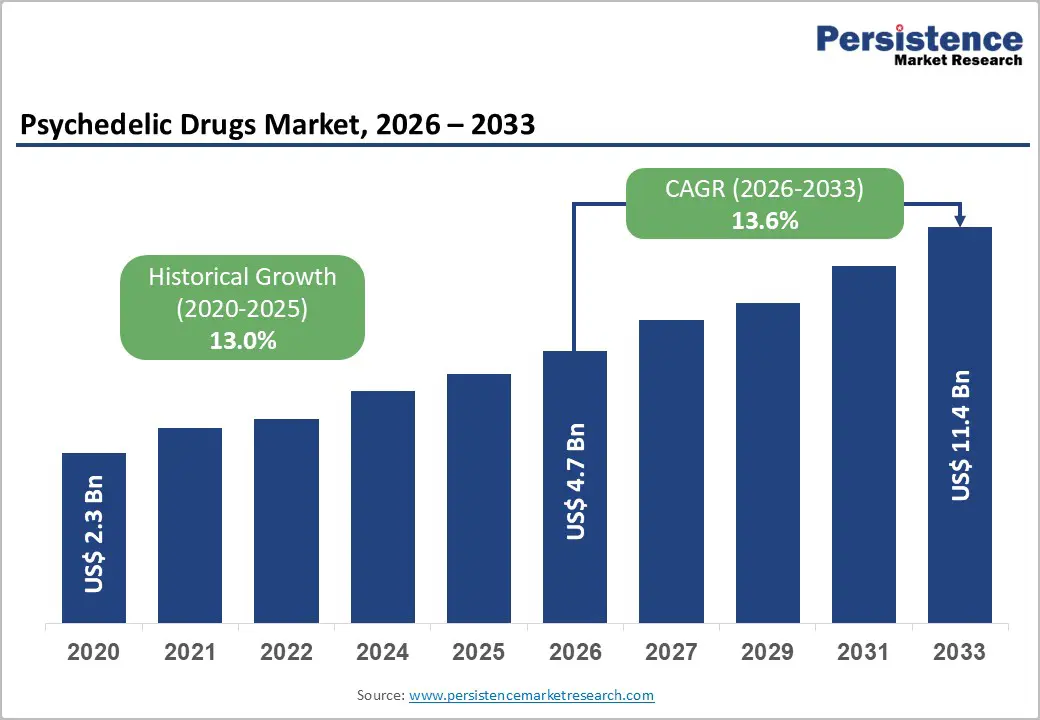

The global psychedelic drugs market size is likely to be valued at US$4.7 billion in 2026 and is expected to reach US$11.4 billion by 2033, growing at a CAGR of 13.6% during the forecast period from 2026 to 2033, driven by growing recognition of mental health disorders and increasing clinical research into novel psychiatric treatments.

According to the World Health Organization (WHO), approximately 332 million people worldwide were living with depression in 2025, with 5.7% of adults affected globally, highlighting the substantial unmet needs for more effective therapies. The WHO also reported in 2025 that over 1 billion people worldwide live with mental health conditions, underscoring the rising demand for innovative treatment approaches. Ongoing clinical studies evaluating compounds such as psilocybin, MDMA, and DMT for depression, PTSD, and addiction, alongside evolving regulatory support and expanding investment in neuropsychiatric drug development, is expected to support market growth.

Key Industry Highlights:

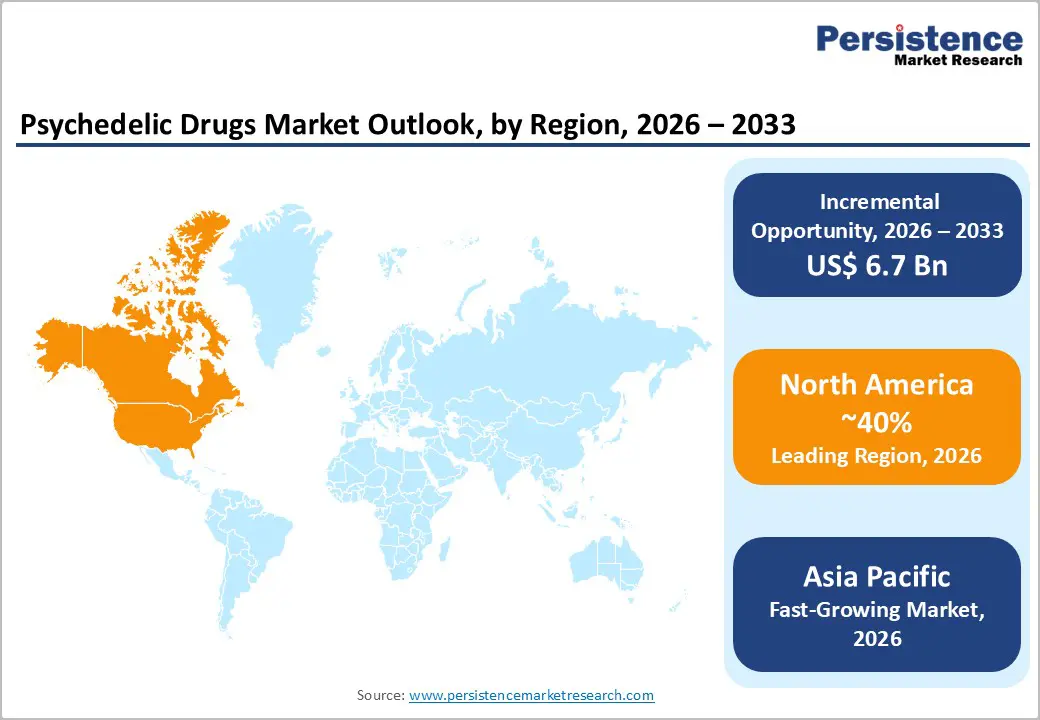

- Leading Region: North America is anticipated to be the leading region, accounting for 40% of the market in 2026, driven by U.S. leadership in clinical research, regulatory advancements, and commercialization initiatives.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region, supported by expanding research activities, evolving regulatory frameworks, and growing demand for innovative mental health treatments.

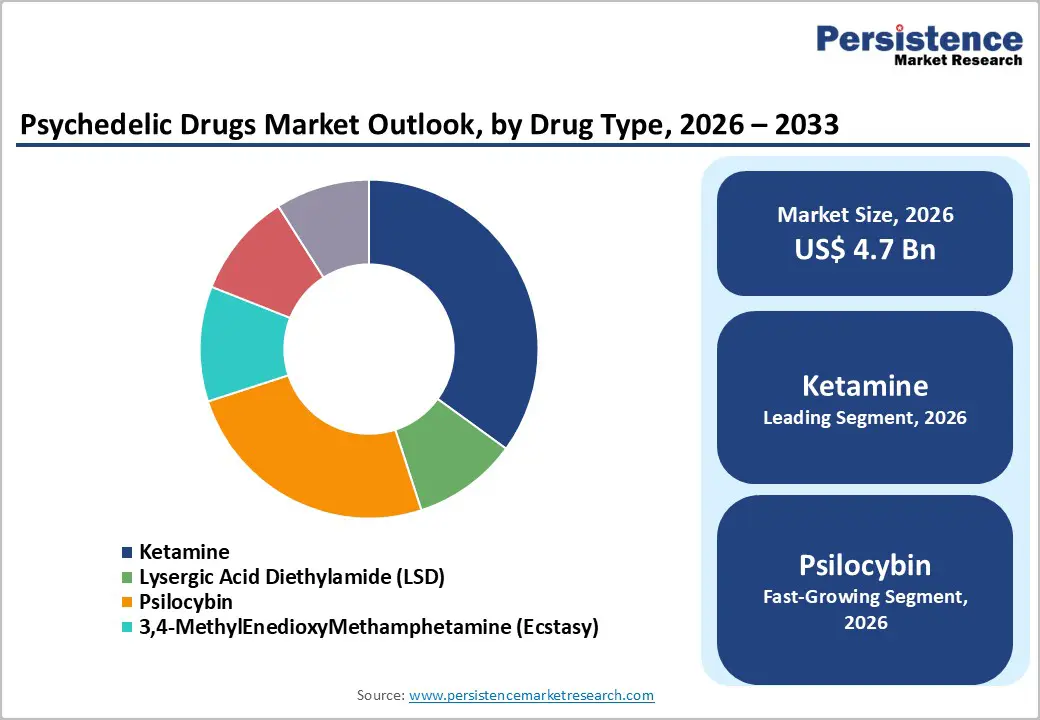

- Leading Drug Type: Ketamine is projected to represent the leading drug type in 2026, accounting for 35% of the revenue share in 2026, due to its established clinical adoption for depression treatment.

- Leading Application: Treatment resistant depression (TRD) is anticipated to be the leading application, accounting for over 40% of the revenue share in 2026, supported by significant unmet clinical needs and expanding therapeutic use.

- Key Opportunity: The expanding clinical development and potential regulatory approval of psychedelic-assisted therapies for depression, PTSD, addiction, and other treatment-resistant mental health disorders present the most significant growth opportunity in the psychedelic drugs market.

DRO Analysis

Driver - Rising Prevalence of Mental Health Disorders and Unmet Needs in Treatment-Resistant Cases

Conditions such as major depressive disorder, anxiety disorders, post-traumatic stress disorder, and substance use disorders continue to affect millions of people worldwide. Despite widespread availability of antidepressants and psychotherapy, many patients fail to achieve adequate symptom relief, leading to a significant treatment gap.

This unmet need has encouraged healthcare providers, researchers, and pharmaceutical companies to explore psychedelic-assisted therapies as potential alternatives capable of delivering meaningful clinical improvements in difficult-to-treat psychiatric conditions across diverse patient populations.

Growing awareness of mental health issues and increasing acceptance of novel therapeutic approaches are accelerating investments in psychedelic drug development. Clinical studies involving compounds such as psilocybin, MDMA, and DMT have demonstrated promising outcomes in patients who have not responded effectively to conventional treatments. Regulatory agencies are also supporting research through expedited pathways for innovative psychiatric therapies.

Restraint - Cultural Stigma and Public Perception Challenges

Many psychedelic substances have historically been associated with recreational use, legal restrictions, and social controversies, creating persistent concerns among patients, healthcare professionals, and policymakers. Negative perceptions developed over several decades continue to influence public attitudes toward psychedelic-assisted treatments. Individuals remain hesitant to consider these therapies due to misconceptions regarding safety, efficacy, and potential misuse.

Public perception challenges also affect regulatory decision-making, reimbursement policies, and investment strategies within the psychedelic drugs market. Healthcare providers often require extensive education and clinical evidence before integrating new treatment modalities into routine practice. Policymakers adopt cautious approaches toward approving psychedelic-based therapies because of societal concerns and historical regulatory frameworks. Limited awareness regarding controlled therapeutic applications contributes to uncertainty among stakeholders.

Opportunity - Technological Convergence and Next-Generation Compounds

Researchers are increasingly combining psychedelic therapies with digital health platforms, artificial intelligence, neuroimaging technologies, and precision medicine tools to improve treatment outcomes and patient monitoring. These technologies enable better understanding of brain activity, individualized treatment planning, and enhanced therapeutic support throughout the treatment process.

Digital platforms can also facilitate remote patient engagement, data collection, and long-term follow-up, improving accessibility and efficiency. The convergence of advanced technologies with psychedelic medicine is helping pharmaceutical companies develop more effective and scalable therapeutic solutions for mental health disorders.

The development of next-generation psychedelic compounds represents another major growth opportunity for the market. Companies are investing in novel formulations designed to optimize therapeutic benefits while reducing side effects, treatment duration, and operational complexity. Researchers are exploring synthetic analogs, modified molecular structures, and targeted delivery systems that may offer improved safety profiles and greater regulatory acceptance.

Category-wise Analysis

Drug Type Insights

Ketamine is expected to account for 35% of revenue in 2026, due to established clinical use, growing physician familiarity, and increasing acceptance in psychiatric treatment settings. Unlike many emerging psychedelic compounds that remain under clinical evaluation, ketamine-based therapies have already achieved significant integration into treatment protocols for severe mental health conditions. A notable example includes the ketamine-derived therapy Spravato developed by Janssen, which has become one of the most widely recognized psychedelic-related treatments in modern psychiatric care.

Psilocybin-based therapies are likely to represent the fastest-growing segment, supported by increasing scientific validation, expanding clinical research programs, and rising investor interest in next-generation mental health treatments. Psilocybin has attracted significant attention owing to its potential to produce long-lasting therapeutic benefits when administered within structured clinical settings. A prominent example includes the psilocybin therapy program developed by COMPASS Pathways, which has emerged as one of the most advanced clinical initiatives in the field.

Application Insights

Treatment-resistant depression (TRD) is projected to lead the market, capturing around 40% of the revenue share in 2026. Healthcare providers and researchers increasingly view psychedelic-assisted therapies as promising alternatives for addressing persistent depressive symptoms that remain difficult to manage using traditional approaches. For instance, Spravato has been widely utilized for individuals experiencing treatment-resistant depression.

Post-traumatic stress disorder (PTSD) is likely to be the fastest-growing application. Rising recognition of the long-term psychological impact of trauma and the limitations of existing treatment options has increased interest in innovative therapeutic approaches. A notable example includes the MDMA-assisted therapy program developed by MAPS, which has significantly advanced clinical interest in psychedelic treatments for PTSD and contributed to rapid segment growth.

Regional Insights

North America Psychedelic Drugs Market Trends

North America is anticipated to be the leading region, accounting for a market share of 40% in 2026, supported by advanced clinical research, favorable funding environments, and growing acceptance of innovative psychiatric therapies. The region benefits from strong participation from biotechnology companies, academic institutions, and healthcare providers focused on addressing treatment-resistant mental health conditions. A notable example includes COMPASS Pathways, which continues to advance late-stage psilocybin research and strengthen North America's clinical development landscape through partnerships and trial expansion initiatives.

U.S. Psychedelic Drugs Market Trends

The U.S. is expected to dominate the regional market, accounting for approximately 75% of the market share in 2026. Strong clinical trial activity continues to support innovation across depression, PTSD, and addiction treatment applications. Several states have expanded pathways for psychedelic research and supervised therapeutic programs. Academic institutions are conducting advanced studies on psilocybin and MDMA-assisted therapies. Venture capital investment remains robust, supporting biotechnology startups and drug developers.

Canada Psychedelic Drugs Market Trends

Canada is likely to be a significant market for psychedelic drugs, holding approximately 25% of the market share in 2026. The country has encouraged clinical investigation of psychedelic compounds for mental health applications. Canadian healthcare stakeholders are increasingly evaluating psychedelic-assisted therapies for depression and trauma-related disorders. Regulatory authorities continue to review pathways for controlled therapeutic access. Academic research institutions are expanding studies focused on efficacy and safety outcomes.

Europe Psychedelic Drugs Market Trends

Europe is likely to be a significant market for psychedelic drugs in 2026, due to strong scientific expertise, established pharmaceutical infrastructure, and growing awareness of unmet psychiatric treatment needs. Research programs evaluating psilocybin, MDMA, and related compounds are expanding across multiple countries. For example, ATAI Life Sciences which continues to invest in next-generation psychedelic therapies and clinical programs that contribute to Europe's expanding innovation ecosystem.

U.K. Psychedelic Drugs Market Trends

The U.K. is likely to be a significant market for psychedelic drugs, supported by leading universities conducting advanced studies on psilocybin and other psychedelic compounds for mental health applications. Biotechnology companies are increasingly establishing partnerships with academic institutions to accelerate drug development. Investor interest remains strong due to promising clinical outcomes reported in recent studies.

Germany Psychedelic Drugs Market Trends

Germany is anticipated to dominate the regional market, accounting for around 35% share in 2026, as the country benefits from a strong healthcare infrastructure and advanced clinical research capabilities. Universities and research centers are conducting studies focused on psychedelic-assisted treatments for depression and anxiety disorders. Growing interest in innovative psychiatric therapies is encouraging collaboration between academia and industry participants.

Asia Pacific Psychedelic Drugs Market Trends

The Asia Pacific region is likely to be the fastest-growing region, driven by increasing mental health awareness, expanding healthcare investments, and growing interest in innovative psychiatric therapies. Countries across the region are strengthening research activities while evaluating the therapeutic potential of psychedelic compounds for depression, PTSD, and addiction treatment. For instance, MindMed, which continues advancing psychedelic drug research and contributes to growing interest that influences Asia Pacific market development.

China Psychedelic Drugs Market Trends

China is projected to dominate the regional market, holding around a 30% share in 2026. Academic institutions are expanding research efforts related to neurological and psychiatric disorders. Rising awareness of mental health challenges is encouraging interest in new treatment approaches. Biotechnology companies are investing in advanced drug discovery and clinical development capabilities. The country also benefits from a strong pharmaceutical manufacturing ecosystem.

India Psychedelic Drugs Market Trends

India is expected to emerge as a significant market, accounting for approximately a 22% regional share in 2026, driven by the country's expanding pharmaceutical industry, providing a strong foundation for future psychedelic drug research and manufacturing activities. Academic institutions are showing greater interest in neuroscience and psychiatric innovation. Healthcare providers are increasingly discussing the need for alternative treatment options for resistant mental health conditions.

Competitive Landscape

The global psychedelic drugs market exhibits a moderately fragmented structure, driven by the presence of established pharmaceutical manufacturers, specialty mental health therapy developers, and emerging biotechnology companies focused on novel neuropsychiatric treatments. The market is evolving rapidly as increasing clinical evidence supporting psychedelic-assisted therapies attracts investments from both traditional pharmaceutical firms and innovative biotech enterprises.

With key leaders, including Johnson & Johnson, Jazz Pharmaceuticals, Pfizer, Teva Pharmaceutical Industries, Hikma Pharmaceuticals, and Baxter International, the competitive landscape continues to strengthen through innovation and expanding psychiatric treatment portfolios. These players compete through clinical research investments, product portfolio expansion, regulatory strategy development, manufacturing capabilities, strategic partnerships, and geographic expansion initiatives.

Key Industry Developments:

- In May 2026, the U.S. Department of Veterans Affairs (VA) launched a randomized clinical trial evaluating MDMA-assisted therapy for veterans with post-traumatic stress disorder (PTSD) and alcohol use disorder, marking a significant advancement in psychedelic-based mental health treatment research and supporting the growing clinical development of psychedelic therapies.

- In April 2026, the U.S. FDA announced measures to fast-track the development and review of psychedelic therapies for serious mental illnesses, issuing priority review vouchers to companies developing psilocybin- and methylone-based treatments for depression and PTSD, following a federal initiative to accelerate innovative mental health therapies.

Companies Covered in Psychedelic Drugs Market

- Janssen (Johnson & Johnson)

- Jazz Pharmaceuticals

- Pfizer

- Hikma Pharmaceuticals

- Fresenius Kabi

- B. Braun Medical

- Teva Pharmaceutical Industries

- Sun Pharma (Taro)

- Accord Healthcare

- Sandoz

- Mylan (Viatris)

- Baxter International

Frequently Asked Questions

The global psychedelic drugs market is projected to reach US$4.7 billion in 2026.

The psychedelic drugs market is expected to grow at a CAGR of 13.6% from 2026 to 2033.

Development of next-generation psychedelic compounds and expansion of regulated therapeutic applications for psychiatric disorders present significant market opportunities.

Janssen (Johnson & Johnson), Jazz Pharmaceuticals, Pfizer, Hikma Pharmaceuticals, and Fresenius Kabi are the leading players.