- Food Ingredients & Additives

- Popcorn Market

Popcorn Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Popcorn Market is segmented by Product Type (Ready-to-Eat Popcorn and Microwave Popcorn), by Flavor (Salted/Plain, Butter, Cheese, Caramel, and Others), by Sales Channel (Supermarkets/Hypermarkets, Convenience Stores, Specialty Stores, Online Retail, and Others), and Regional Analysis, 2026 - 2033

Popcorn Market Share and Trends Analysis

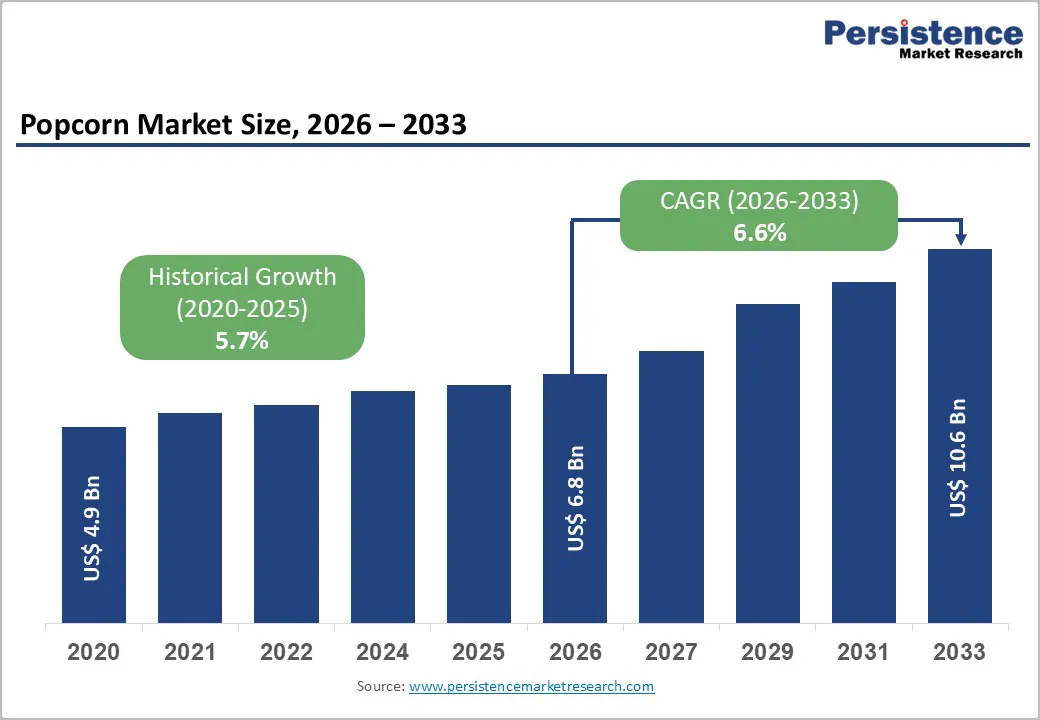

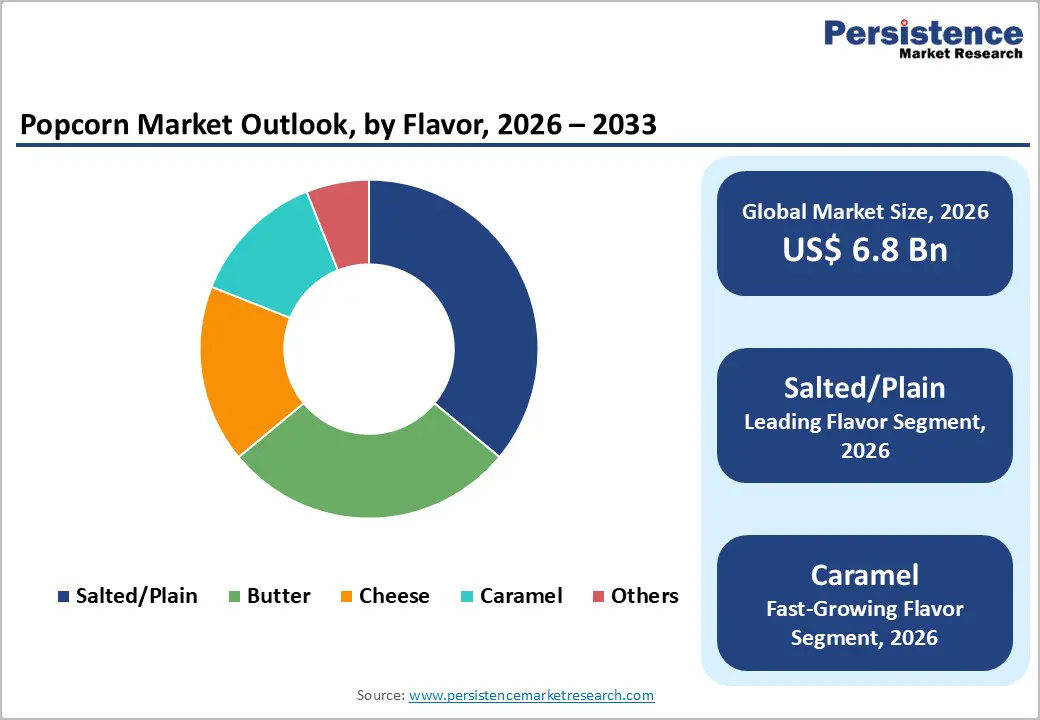

The global popcorn market size is expected to reach US$ 6.8 billion in 2026 and US$ 10.6 billion by 2033, growing at a CAGR of 6.6% over the forecast period 2026 to 2033.

The market is primarily driven by consumers' growing preference for whole-grain, fiber-rich snacking alternatives with a healthier profile than traditional potato chips. Shifting consumer behavior, characterized by increased at-home entertainment and the proliferation of streaming services, has solidified popcorn as a staple of home viewing. Furthermore, rapid innovation in gourmet flavor profiles and the expansion of organized retail channels in emerging economies are significantly lowering the barrier to entry for premium brands.

Key Industry Highlights

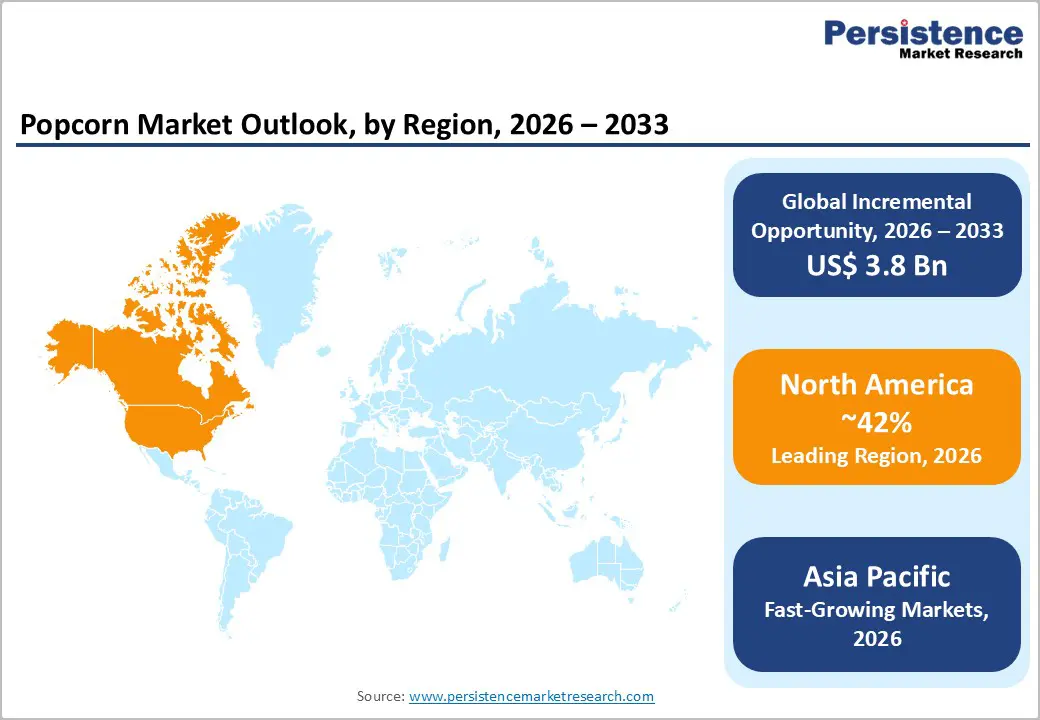

- Leading Region: North America dominated the market in 2025 with a 42% share, driven by a mature snacking culture and a strong presence of major industry players.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region through 2033, fueled by increasing disposable incomes and the expansion of home-streaming entertainment in China and India.

- Dominant Segment: The Salted/Plain flavor held a 36% market share in 2025, maintaining its position as the preferred choice among health-conscious and traditional snackers.

- Fastest Growing Segment: Caramel is the fastest-growing flavor category, benefiting from the rising premiumization of gourmet popcorn and the popularity of sweet-and-savory blends.

- Key Market Opportunity: The growth of Subscription-Based and Direct-to-Consumer (D2C) models offers a high-value avenue for artisanal brands to build direct loyalty and test innovative flavor profiles.

| Key Insights | Details |

|---|---|

| Global Popcorn Market Size (2026E) | US$ 6.8 Bn |

| Market Value Forecast (2033F) | US$ 10.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.7% |

Market Dynamics

Driver - Rising Health Consciousness and Preference for Functional Snacks

A fundamental driver for the industry is the global rise in health awareness, which has repositioned popcorn from a theatre novelty to a functional snack. According to the United States Department of Agriculture (USDA), popcorn is a 100% unprocessed whole grain that provides significant levels of dietary fiber and polyphenols. In 2025, more than 42% of global consumers preferred snacks with health-positive attributes, favoring air-popped and lightly seasoned variants. Brands like Amplify Snack Brands (with SkinnyPop) have successfully capitalized on this trend by promoting non-GMO, gluten-free, and low-calorie certifications. This health-centric demand is particularly strong among Millennials and Gen Z, who increasingly view popcorn as a satisfying meal replacement or a post-workout recovery snack.

Restraints - Intense Competition from Alternative Salty Snacks

Despite its strong position, popcorn faces significant competition from a wide range of salty snacks, including extruded puffs, pretzels, and vegetable crisps. The savory snack market is highly saturated, with established players constantly launching crossover products that mimic popcorn’s light texture. Manufacturers report that strong competition from alternative snacks can affect CAGR in intensifying urban markets. Furthermore, price sensitivity in the gourmet segment remains a hurdle, as consumers may switch to cheaper private-label alternatives during periods of economic inflation, limiting the revenue potential for premium-positioned brands in price-conscious demographics.

Opportunity - Growth of Subscription-Based and Direct-to-Consumer (D2C) Models

The digital transformation of the retail landscape has opened new avenues for brand loyalty through subscription services. Online popcorn sales increased by 48% between 2023 and 2025, with subscription-based deliveries rising by 26%. This model allows brands to offer exclusive limited-edition flavors and artisanal kernels directly to the consumer’s doorstep, bypassing traditional retail shelf-space battles. High-growth startups are leveraging influencer-driven marketing and social media campaigns to reach Gen Z, who prioritize convenience and personalized experiences. The ability to collect first-party data through D2C platforms enables manufacturers to optimize their product development cycles and respond rapidly to emerging flavor trends.

Category-wise Analysis

Flavor Insights

Salted/Plain popcorn remains the dominant flavor category, accounting for 36% of the market in 2025. Its universal appeal and perception as the healthiest option drive consistent volume sales. However, Caramel is projected to be the fastest-growing flavor segment over the forecast period. The premiumization of sweet-and-savory blends has made Caramel and Kettle Corn variants highly popular in the gourmet and gift-giving sectors. Brands are increasingly launching indulgent combinations like Salted Caramel with dark chocolate drizzles to target evening snacking occasions, a trend that is particularly prevalent in North America and Europe.

Sales Channel Insights

Supermarkets and hypermarkets are the leading sales channel, accounting for over 45% of global popcorn revenue in 2025. These large-format stores provide the shelf space needed to carry extensive flavor varieties and multi-pack formats, attracting bulk-buying families. Meanwhile, Online Retail is the fastest-growing distribution channel. The surge in e-commerce is driven by the rise of niche gourmet brands and the convenience of subscription boxes. In 2025, digital platforms contributed significantly to the accessibility of organic and non-GMO popcorn variants in regions with limited physical health-food store presence, such as parts of the Asia Pacific and Latin America.

Regional Insights

North America Popcorn Market Trends and Insights

North America is the largest regional market, accounting for 42% of the market in 2025. The United States remains the primary engine of growth, supported by a deeply rooted movie-going culture and a mature snack industry. A defining trend in this region is the premiumization of snacks by Millennials and Gen Z, who are driving demand for functional popcorn. For instance, the introduction of Khloud Protein Popcorn in 2025, offering 7 grams of protein per serving, exemplifies how brands are positioning popcorn as a competitor to traditional protein bars.

The regulatory environment in the U.S., overseen by the FDA, emphasizes labeling transparency and the elimination of synthetic additives. Innovation is also fueled by strategic collaborations; in September 2024, Smartfood partnered with rap icon Flavor Flav to enhance brand visibility. The region’s extensive retail network and the rapid adoption of e-commerce ensure that it remains at the forefront of global trends, with Ready-to-Eat formats leading the market, accounting for nearly 68% of the domestic market share.

Asia Pacific Popcorn Market Trends and Insights

Asia Pacific is the fastest-growing market, projected to expand at a high CAGR through 2032. This growth is underpinned by rising disposable incomes and rapid urbanization in China, India, and South Korea. The expansion of streaming platforms like Netflix and Amazon Prime has replicated the cinema experience at home, boosting demand for RTE and microwave popcorn. In India, the gourmet segment has experienced a substantial surge, with brands such as 4700BC reporting triple-digit growth in retail and e-commerce sales.

Manufacturing advantages in the region enable cost-effective production of diverse flavor profiles that cater to local palates, such as Sichuan Pepper- or curry-seasoned popcorn. The growing influence of Western snacking cultures and the proliferation of modern retail formats are significant catalysts. In Japan, the market is characterized by a high demand for premium, beautifully packaged popcorn suitable for gifting. As the middle class continues to expand, the region is expected to account for a larger portion of the global value share, particularly in the innovative flavor and organic segments.

Competitive Landscape

The popcorn Market is a moderately fragmented landscape where global snack giants coexist with a vibrant ecosystem of gourmet startups. Leaders such as PepsiCo and Conagra Brands hold the majority of the market share in 2025. These incumbents utilize their massive distribution networks and marketing budgets to maintain dominance in the mass-retail and microwave segments.

Smaller, niche players such as Quinn Snacks and Amplify Snack Brands are driving the innovation curve, focusing on sustainability, clean-label ingredients, and unconventional flavors. A significant trend in the landscape is the entry of entertainment brands into retail; in June 2024, Netflix launched its own line of retail popcorn to enhance the at-home viewing experience. Strategic mergers and acquisitions are common as larger firms seek to acquire high-growth artisanal brands to diversify their portfolios and appeal to health-conscious younger demographics.

Key Developments:

- In May 2025, Pop Secret moved beyond its microwave roots by launching ready-to-eat popcorn, signaling a strategic push into on-the-go snacking and broader retail shelf presence. The expansion aligns the brand with rising demand for convenient, pre-popped snack formats.

- In May 2024, Popzup Popcorn elevated its gourmet positioning with the launch of Truffle Butter & Cracked Black Pepper Popcorn, tapping into premium flavor experimentation. The introduction targets consumers seeking indulgent, restaurant-inspired snack experiences at home.

Companies Covered in Popcorn Market

- PepsiCo

- Conagra Brands

- Amplify Snack Brands

- Campbell Soup Company

- Intersnack Group

- Calbee Inc.

- General Mills

- Opopop

- Preferred Popcorn

- Krackle Foods Private Limited

- Quinn Snacks

- Others

Frequently Asked Questions

The global popcorn market is projected to be valued at US$ 6.8 Bn in 2026.

Rising Health Consciousness and Preference for Functional Snacks is driving demand for Popcorn market.

The Global Popcorn market is poised to witness a CAGR of 6.6% between 2026 and 2033.

Growth of Subscription-Based and Direct-to-Consumer (D2C) Models is key opportunity for key players in the market.

The market is led by global giants such as PepsiCo, Conagra Brands, Amplify Snack Brands, Campbell Soup Company, Intersnack Group, General Mills, and others.