- Smart Packaging

- Polycoated Cup Stock Market

Polycoated Cup Stock Market Size, Share, and Growth Forecast, 2026 - 2033

Polycoated Cup Stock Market by End‑use Industry (Foodservice, Quick‑Service & Delivery‑Centric F&B Chains, Others), Product Form (Cups, Cup Blanks/Cut‑Outs, Others), Coating Type, Cup Size, and Regional Analysis for 2026 - 2033

Polycoated Cup Stock Market Size and Trends Analysis

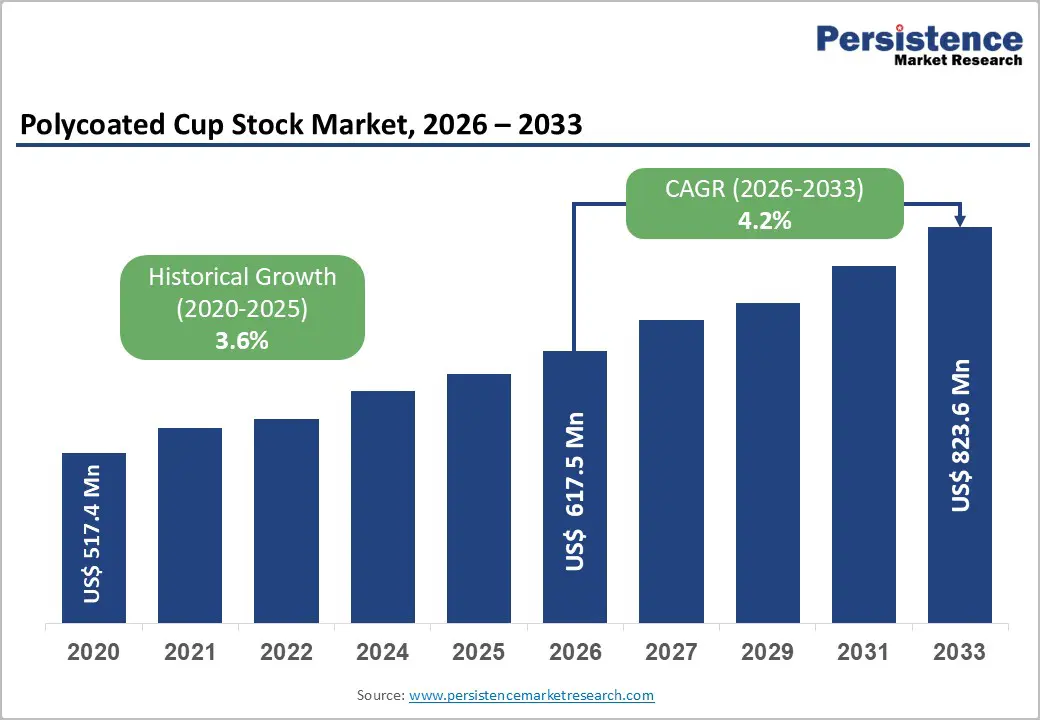

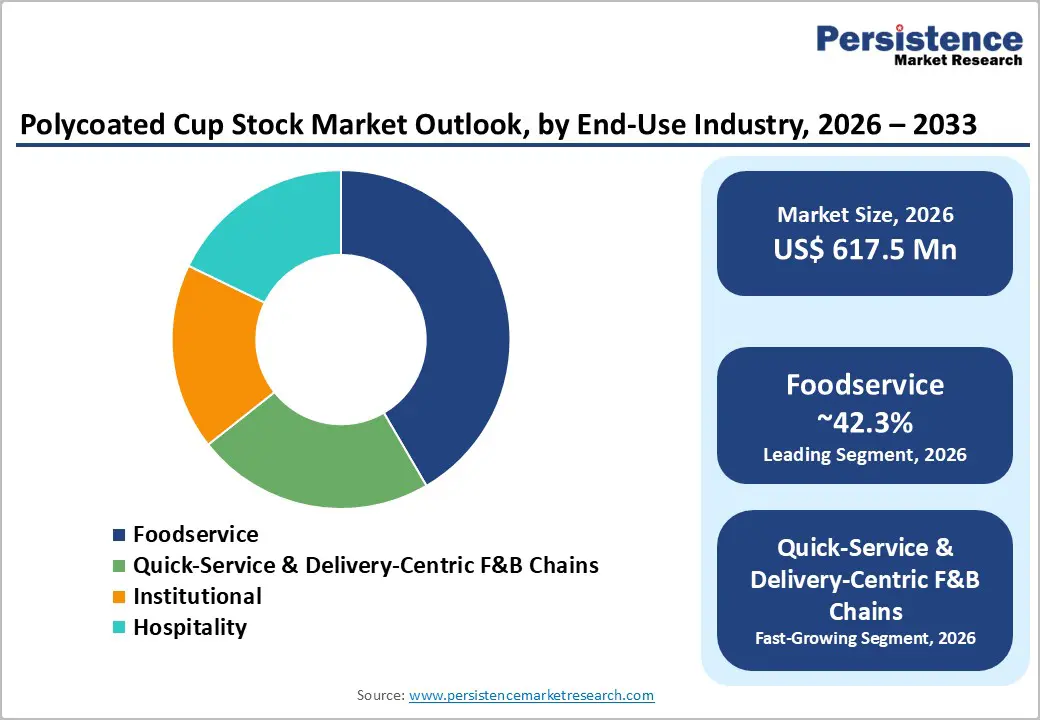

The global polycoated cup stock market size is likely to be valued at US$617.5 million in 2026 and is expected to reach US$823.6 million by 2033, growing at a CAGR of 4.2% between 2026 and 2033, driven by structural growth in foodservice, takeaway beverages, and digital ordering ecosystems.

Rising penetration of online food delivery and sustained consumption of hot and cold beverages continue to support unit demand for coated cupboard board. Regulatory pressure on single-use plastics and packaging taxes is also accelerating the transition from conventional polyethylene (PE) coatings toward recyclable and plant-based barrier technologies. As a result, value growth increasingly reflects both volume expansion and product-level premiumization within the broader paper cup and cupstock value chain.

Key Industry Highlights

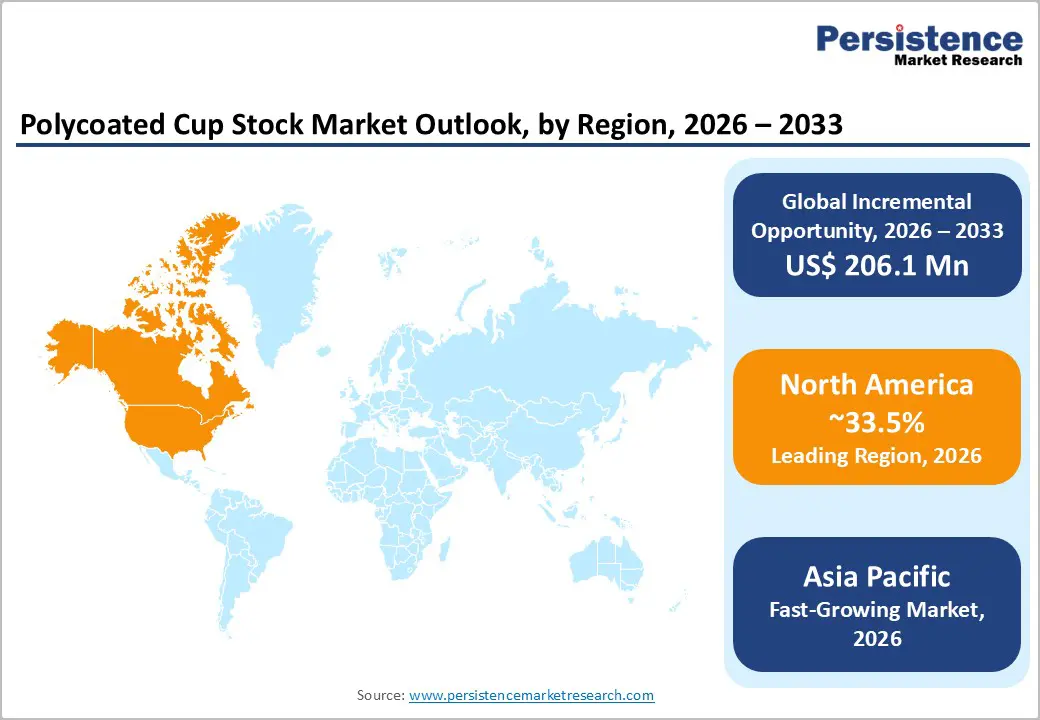

- Leading Region: North America is projected to hold approximately 33.5% share, driven by strong U.S. foodservice demand, high per-capita beverage consumption, and advanced converting infrastructure.

- Fastest-Growing Region: Asia Pacific is likely to expand due to rapid QSR penetration, urbanization, and growth in local cup-converting capacity.

- Investment Plans: Capital allocation toward recyclable and repulpable barrier technologies, recycled-content board production, and regional cup blank converting facilities to align with EPR frameworks and sustainability mandates.

- Dominant End-use Industry: Foodservice is expected to account for approximately 42.3% of the market, supported by takeaway culture, recurring procurement cycles, and branded cup demand from QSR chains and cafés.

- Leading Product Form: Finished cups are estimated to hold approximately 38.4% of market share, integrating printing, forming, and converting margins while meeting large-scale branded foodservice requirements.

| Key Insights | Details |

|---|---|

| Polycoated Cup Stock Market Size (2026E) | US$617.5 Mn |

| Market Value Forecast (2033F) | US$823.6 Mn |

| Projected Growth (CAGR 2026 to 2033) | 4.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Expansion of Foodservice and Digital Delivery Channels

Global foodservice sales continue to expand, with the U.S. restaurant industry alone projected at approximately US$1.5 trillion in 2025. Online food delivery has evolved into a multi-hundred-billion-dollar channel worldwide, fundamentally altering beverage consumption patterns. This sustained macro-level demand translates directly into higher unit consumption of disposable beverage containers and polycoated cup stock. On- and off-premises beverage consumption, including coffee, tea, and cold drinks, provides a consistent baseline for demand. Growth in delivery and quick-commerce is increasing the need for leak-resistant, durable cup constructions and larger serving sizes. Suppliers capable of supporting short production runs, regional converting needs, and rapid replenishment cycles are positioned to gain share in this expanding ecosystem.

Regulatory and Sustainability Pressure

Environmental regulation is reshaping packaging economics across major markets. European Single-Use Plastics legislation, extended producer responsibility (EPR) schemes, and packaging taxation policies such as the U.K. Plastic Packaging Tax are increasing compliance costs for plastic-intensive materials. These regulatory frameworks elevate the commercial value of recyclable and low-plastic alternatives. As a result, conversion from traditional PE-lined cupstock toward recyclable, water-based, fluorine-free, or repulpable barrier technologies is accelerating. Brand owners are actively seeking materials that reduce lifecycle emissions and support circularity claims. This transition is driving research and development spending, premium pricing for compliant solutions, and differentiated regional demand patterns depending on regulatory enforcement levels.

Technology and Material Innovation

Barrier coating technologies are evolving from pilot-stage concepts to commercial-scale applications. Repulpable coatings, bio-based polymers such as PLA, and renewable PE solutions are increasingly engineered to be compatible with existing cup-converting lines. These innovations reduce the historical trade-off between moisture resistance and recyclability. Technical improvements in coating adhesion, heat sealing, and forming performance enable converters to maintain operational efficiency while upgrading sustainability credentials. Cup makers adopting advanced barrier systems gain access to environmentally conscious customers and can mitigate landfill and EPR exposure. Investment in coating chemistry optimization and coating-machine calibration has become a near-term competitive differentiator among cupstock producers.

Barrier Analysis - Recycling Infrastructure and Technical Limits

Although recyclable barrier technologies are advancing, collection and repulping infrastructure remains inconsistent across regions. Used beverage cups often face contamination challenges, limited dedicated collection streams, and varying municipal waste policies. These structural constraints complicate recyclability claims at scale. In markets where recycling systems are immature, transitioning to recyclable coatings may increase supplier costs by mid-single-digit percentage points without immediate economic return. The absence of harmonized infrastructure slows widespread adoption despite significant advances in innovation.

Cost Volatility in Fiber and Resin Inputs

Polycoated cupstock production sits at the intersection of pulp, energy, and polymer markets. Fluctuations in pulp pricing, resin feedstocks, and energy costs create margin volatility. Additionally, coating line upgrades or retrofits required for new barrier chemistries are capital-intensive, raising entry barriers for smaller mills and converters. A 10-15% rise in pulp or polymer input costs can materially compress margins for mid-tier suppliers lacking scale advantages or value-added differentiation. Cost pass-through mechanisms are not always immediate, increasing short-term financial pressure.

Opportunity Analysis - Premium Recyclable and Repulpable Cupstock

Corporate sustainability commitments and regulatory shifts are generating demand for validated recyclable cup solutions. If 10-15% of replacement demand in developed markets transitions to recyclable barrier systems by 2030, this represents a multi-tens-of-million-dollar incremental opportunity within the existing market base. Cupstock producers that offer third-party validated repulpable technologies, traceable sourcing, and documented end-of-life performance can command premium pricing. Long-term supply agreements with major foodservice chains increasingly incorporate sustainability performance criteria, creating defensible competitive positioning.

Regional Converting and Local Cup Blanking

Growth in quick-service restaurants and private-label beverage programs favors localized cup production. Shipping finished cups incurs higher freight costs due to bulk and storage inefficiencies, whereas shipping blanks offers logistical advantages. If regional converters capture 20-30% more local cup-conversion demand over the next five years, cup-blank volumes could grow faster than finished-cup shipments. Investments in regional coating and blanking facilities enable shorter lead times, reduced transportation costs, and improved responsiveness to customer design requirements.

Category-wise Analysis

End-use Industry Insights

The foodservice segment, including restaurants, cafés, institutional catering, and quick-service restaurants (QSRs), is the largest and is projected to maintain its 42.3% share through 2033. High beverage throughput, takeaway culture, and recurring procurement cycles drive sustained volume demand. Global coffee chains such as Starbucks, Tim Hortons, and Costa Coffee, along with fast-food operators such as McDonald’s and Burger King, require consistent print quality, structural integrity, and heat resistance, favoring premium-grade cupstock with reliable PE or advanced barrier coatings. Large chains typically operate centralized procurement systems with forecast-based ordering, creating predictable volume streams for mills and converters. Long-term supply contracts, vendor-managed inventory models, and multi-year sustainability roadmaps further support production stability and investment planning across the value chain.

Delivery-oriented QSR formats and cloud kitchens are projected to record the highest CAGR within the end-use category, supported by digital ordering platforms such as Uber Eats, DoorDash, Zomato, and Swiggy. Higher beverage bundling frequency, combo meals, and preferences for larger portions increase cupstock consumption intensity per transaction. Growth in drive-through and takeaway-focused outlets across North America and Asia Pacific reinforces this upward trajectory. Converters serving this segment must meet shorter lead times, seasonal promotional runs, and customized branding requirements. Engineered barrier systems designed for leak resistance, double-wall compatibility, and secure lid fit are particularly important for transport durability. Suppliers investing in high-speed forming lines, flexible printing capabilities, and rapid replenishment models are expected to capture disproportionate growth as digital foodservice ecosystems expand.

Product Form Insights

Finished cups are anticipated to sustain a 38.4% of market share in 2026. This segment integrates coating, printing, cutting, and forming margins, resulting in higher revenue realization per ton of board. Foodservice operators frequently purchase branded, ready-to-use cups in bulk, particularly for national promotional campaigns and standardized store formats. Integrated packaging companies such as Huhtamaki and Graphic Packaging International leverage in-house design studios, flexographic and digital printing lines, and automated forming systems to capture greater value addition. Customization, brand differentiation, and strict quality assurance standards contribute to this segment’s leadership, especially among multinational beverage chains.

Cup blanks and die-cut sidewall pieces are expected to grow more rapidly, particularly in regions where local cup-forming operations are expanding. Blanks reduce freight and storage costs compared to shipping fully formed cups and allow converters to optimize production scheduling closer to end markets. This model is gaining traction in Asia Pacific and parts of Eastern Europe, where regional cup manufacturers are scaling capacity. Paperboard mills that offer cut-to-size services, rapid artwork changes, and small-batch printing for private-label beverage brands are positioned for a higher CAGR than traditional exporters of finished cups. Localization enhances supply chain resilience, reduces lead times, and enables faster replenishment cycles, thereby supporting the structural shift toward decentralized cup manufacturing ecosystems.

Regional Insights

North America Polycoated Cup Stock Market Trends - QSR-Driven, Compliance-Intensive Market with Rising Fiber-Based Barrier Adoption

North America is projected to lead, accounting for approximately 33.5% of the market share in 2026, with the U.S. representing the primary demand center. High per-capita coffee consumption, estimated by the National Coffee Association at over 60% of U.S. adults consuming coffee daily, underpins steady cup demand across hot and cold beverage categories. The region’s dense quick-service restaurant ecosystem, led by brands such as Starbucks, McDonald’s, Dunkin’, and Tim Hortons, generates recurring procurement cycles for coated cupstock. Starbucks alone operates more than 16,000 stores in the U.S., reinforcing long-term volume commitments for paperboard suppliers and converters.

Primary growth drivers include resilient restaurant traffic, continued drive-through expansion, and strong penetration of delivery platforms such as DoorDash and Uber Eats. McDonald’s and Starbucks have both expanded drive-through and digital pickup formats in recent years, increasing takeaway beverage throughput and reinforcing demand for structurally robust, heat-resistant cupstock. Corporate sustainability programs also shape procurement specifications. For example, Starbucks has piloted fiber-based cup innovations and recyclable barrier technologies in select U.S. markets in partnership with packaging suppliers, signaling a gradual migration toward improved end-of-life performance.

Regulatory oversight remains a defining factor. The U.S. Food and Drug Administration enforces strict food-contact compliance for coated paperboard materials. At the state level, extended producer responsibility frameworks are advancing; California’s SB 54 (Plastic Pollution Prevention and Packaging Producer Responsibility Act) establishes phased recycling and source-reduction targets through 2032. Such policies influence material selection and encourage the development of repulpable barrier coatings. In response, companies including Graphic Packaging International and WestRock have expanded investments in coated recycled board capacity and fiber-based barrier R&D. Suppliers that combine regulatory documentation, traceability systems, and scalable regional converting capacity maintain competitive positioning in this compliance-intensive environment.

Europe Polycoated Cup Stock Market Trends - Policy-led Transition toward Recyclable Barrier Cup Stock in Mature Café Markets

Europe represents a mature but policy-driven polycoated cup stock market, with Germany, the U.K., France, and Spain serving as key demand centers. Consumption patterns reflect strong café culture and takeaway beverage formats, particularly in urban markets. Large multinational chains such as Costa Coffee (U.K.), McCafé (Germany and France), and Pret A Manger rely on standardized procurement of packaging across European operations, thereby sustaining baseline demand for coated cupboard substrates.

The European Union’s Single-Use Plastics Directive and Packaging and Packaging Waste Regulation reforms require labeling, recycling targets, and material transparency. For example, Huhtamaki has introduced recyclable paper cups with water-based dispersion barriers in several European markets, designed to improve repulpability within existing paper recycling streams. Similarly, Stora Enso and Metsä Board have invested in fiber-based barrier board solutions to reduce fossil-based polymer content while maintaining moisture resistance.

Extended Producer Responsibility schemes across Germany and France impose reporting and cost obligations on packaging producers, raising compliance thresholds. In 2024 and 2025, multiple European municipalities expanded reusable cup pilot programs, influencing procurement strategies among foodservice operators. Nevertheless, single-use coated cups remain essential for high-volume takeaway channels. Mills are therefore investing in recyclable barrier technologies while collaborating with recycling associations to validate end-of-life performance claims.

Asia Pacific Polycoated Cup Stock Market Trends - Urbanization-Fueled, QSR-Expansion-Driven High-Growth Cup Stock Market

Asia-Pacific is the fastest-growing regional market for polycoated cup stock, driven by rapid urbanization, expansion of middle-class incomes, and accelerating penetration of quick-service restaurants. China and India account for significant incremental volume growth, while Japan emphasizes premium beverage formats and high-quality print performance. Major international brands such as Starbucks, KFC, and McDonald’s continue to aggressively expand their store presence across Tier 1 and Tier 2 cities in China and India, thereby increasing demand for both finished cups and locally converted cup blanks.

In China, domestic beverage chains such as Luckin Coffee have scaled rapidly, surpassing thousands of outlets and stimulating recurring cupstock procurement. India’s café segment, led by Café Coffee Day and expanding international franchises, supports increased consumption of PE-coated substrates. Japan’s convenience store operators, including 7-Eleven Japan and Lawson, maintain strong private-label beverage programs, emphasizing precise forming tolerances and aesthetic print quality. Companies such as APP (Asia Pulp & Paper) and Nine Dragons Paper have strengthened coated paperboard production capacity to serve both domestic converters and export markets.

Environmental regulation remains uneven across countries. While Japan and South Korea maintain advanced recycling systems, other markets are still developing collection infrastructure. China’s evolving packaging waste policies and India’s Plastic Waste Management Rules encourage a gradual reduction in single-use plastics, prompting selective investment in plant-based coatings and renewable polyethylene solutions for urban and export-oriented clients.

Competitive Landscape

The global polycoated cup stock market is moderately fragmented. Large integrated packaging companies dominate the global supply of high-grade cupstock, while numerous regional converters serve local markets.

Competitive differentiation centers on coating innovation, production scale, sustainability validation, and proximity to high-volume foodservice clients. Key strategic priorities include recyclable barrier innovation, vertical integration across fiber and converting operations, geographic expansion near foodservice hubs, and long-term supply agreements incorporating sustainability performance metrics.

Key Industry Developments:

- In August 2025, Univest unveiled a new water-based barrier coating production line enabling fully recyclable and compostable UniCup™ and UniLids™, enhancing sustainable cupstock offerings compatible with both hot and cold beverages.

Companies Covered in Polycoated Cup Stock Market

- Graphic Packaging International

- Stora Enso

- Mondi Group

- WestRock Company

- International Paper

- Smurfit Westrock

- Huhtamaki Oyj

- Metsä Board

- DS Smith

- Sonoco Products Company

- Evergreen Packaging

- Sappi Limited

- Nippon Paper Industries

- APP (Asia Pulp & Paper)

- Oji Holdings Corporation

- Twin Rivers Paper Company

- AR Packaging

- Billerud AB

Frequently Asked Questions

The global polycoated cup stock market is projected to be valued at US$617.5 million in 2026.

The polycoated cup stock market is expected to reach US$823.6 million by 2033.

Key trends include the transition from conventional polyethylene coatings to recyclable and plant-based barrier systems, increasing demand from digital food delivery platforms, regionalization of cup blank production, and greater investment in repulpable coating technologies to meet evolving sustainability regulations.

The foodservice segment is expected to lead the market, accounting for approximately 42.3% of market share in 2026, driven by high beverage throughput in quick-service restaurants, cafés, and takeaway channels.

The polycoated cup stock market is projected to grow at a CAGR of 4.2% between 2026 and 2033.

Major players include Graphic Packaging International, Stora Enso, Mondi Group, WestRock Company, and Huhtamaki Oyj.