- Semiconductor Materials & Components

- PoC Platform & Technology Market

PoC Platform & Technology Market Size, Share, and Growth Forecast, 2026 - 2033

PoC Platform & Technology Market by Platform Type (Lateral Flow Assay (LFA) Platforms, Molecular PoC Platforms, Immunoassay PoC Platforms, Microfluidic/Lab-on-Chip Platforms, Biosensor-Based Platforms, Digital & Connected PoC Platforms, Others (Emerging/Hybrid Platforms)), Application (Infectious Disease Testing, Glucose & Chronic Disease Monitoring, Cardiology & Metabolic Testing, Respiratory Diseases, Pregnancy & Fertility Testing, Oncology, Others.), End User (Hospitals & Clinics, Diagnostic Laboratories, Home Care/Self-Testing, Pharmacies & Retail Clinics, Emergency Care & Ambulatory Centers, Others) and Regional Analysis for 2026 - 2033

PoC Platform & Technology Market Size and Trends Analysis

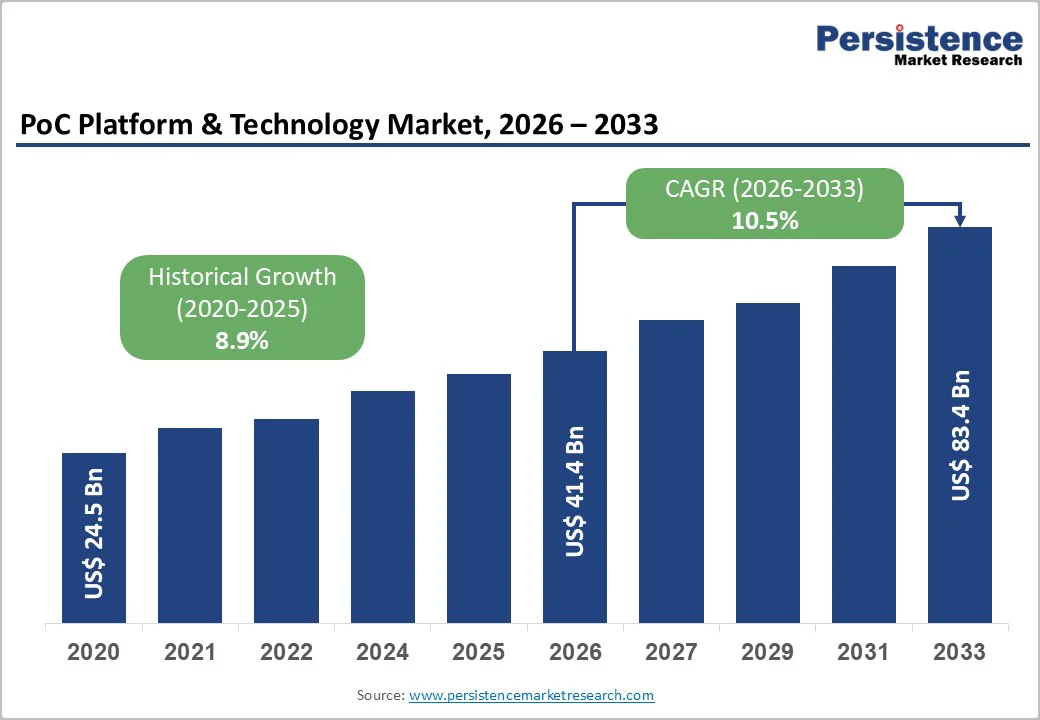

The Global PoC Platform & Technology Market size was valued at US$41.4 billion in 2026 and is projected to reach US$ 83.4 billion by 2033, growing at a compound annual growth rate (CAGR) of 10.5% between 2026 and 2033. This robust expansion reflects the fundamental shift in diagnostic paradigms toward decentralized, patient-centric healthcare delivery.

The market's acceleration is driven by three interconnected macroeconomic forces: the rising prevalence of chronic diseases, including diabetes affecting 537 million adults globally, projected to reach 783 million by 2045 and cardiovascular conditions, the persistent demand for rapid infectious disease diagnostics, and regulatory frameworks promoting diagnostic capacity strengthening through international collaborations such as the World Health Assembly Resolution 76.5.

Technological convergence of artificial intelligence, Internet-of-Things connectivity, and microfluidic innovations is enabling more accessible, accurate, and cost-effective diagnostic solutions at the point of care.

Key Industry Highlights:

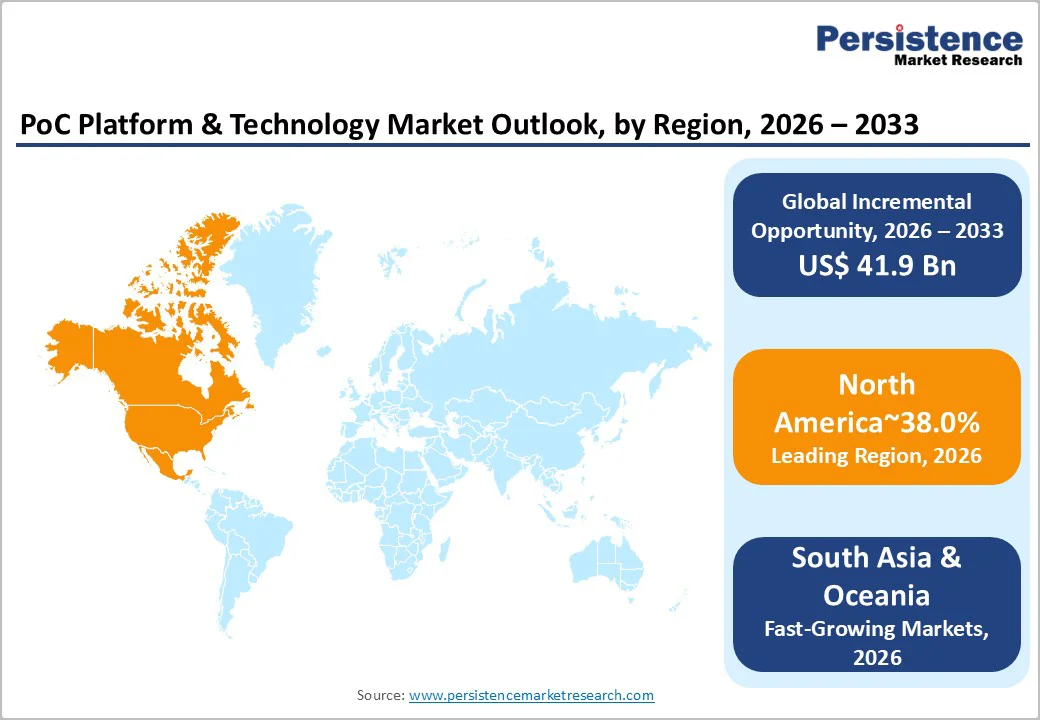

- North America Leads Market Share: North America commands 38% of the global PoC market, driven by advanced healthcare infrastructure, strong reimbursement systems, and established diagnostics innovation hubs.

- East Asia Fastest-Growing Region: East Asia holds 26% market share and is expanding rapidly, supported by large-scale government screening programs in China and AI-integrated PoC innovations in Japan and South Korea.

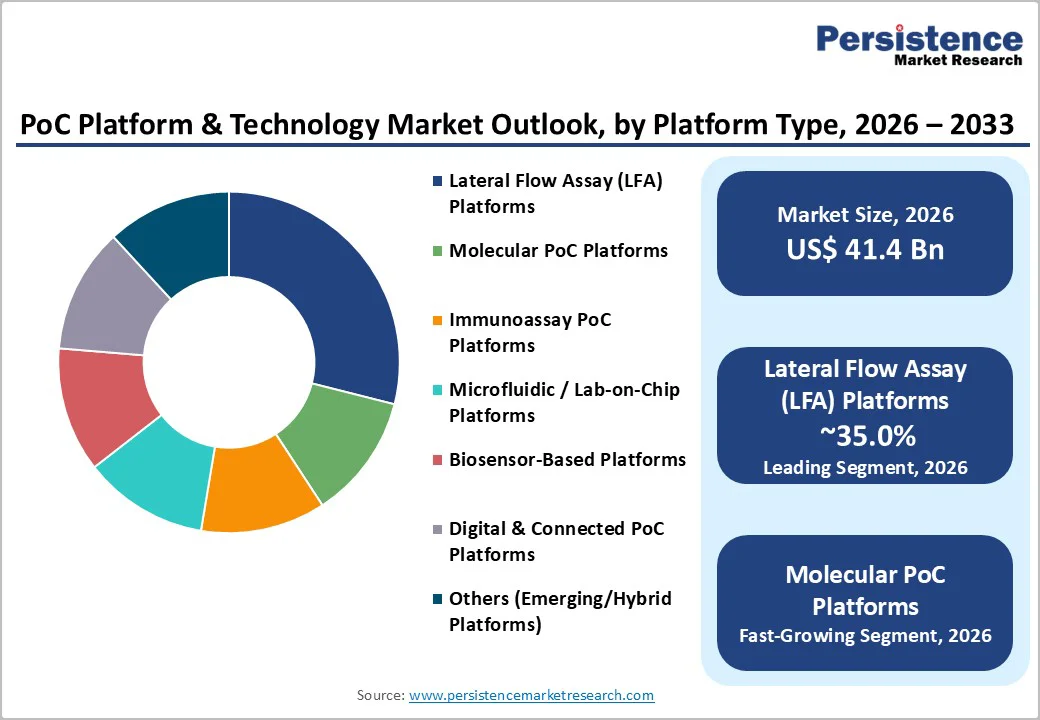

- Lateral Flow Assays Dominate: LFA platforms maintain market leadership with 35% share in 2026, due to simplicity, low cost, regulatory familiarity, and global manufacturing scale.

- Molecular PoC Platforms Grow Fastest: Molecular diagnostics are the fastest-expanding segment, with syndromic testing and AI integration enhancing clinical utility and multiplex pathogen detection.

- Chronic Disease Monitoring Drives Demand: Glucose and chronic disease testing are the fastest-growing applications, reflecting rising prevalence of diabetes, cardiovascular, and metabolic disorders globally.

- Emerging Markets Offer Opportunities: Asia-Pacific and sub-Saharan Africa present substantial growth potential through government health initiatives, rural healthcare expansion, and localized PoC device manufacturing.

| Global Market Attributes | Key Insights |

|---|---|

| PoC Platform & Technology Market Size (2026E) | US$ 41.4 Bn |

| Market Value Forecast (2033F) | US$ 83.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 10.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 8.9% |

Market Dynamics

Growth Drivers

Healthcare System Decentralization and Access Expansion

The global healthcare landscape is undergoing systematic decentralization, shifting diagnostic capabilities from centralized laboratory facilities to primary care settings, urgent care clinics, pharmacies, and patient homes. This transformation represents a fundamental restructuring of diagnostic delivery models, with the PoC Platform & Technology Market serving as the enabling infrastructure.

The World Health Organization's Diagnostics Taskforce, established in response to Resolution WHA76.5, explicitly emphasizes point-of-care testing at the primary health care level as essential to achieving universal health coverage. In emerging markets, particularly India, government initiatives such as the "Make in India" scheme and the "Ayushman Bharat" program are systematically expanding PoC device manufacturing capacity and accessibility, with projections indicating 150 million units of glucose monitoring devices in testing volume by 2033, signifying large-scale market penetration.

India's National Health Mission has standardized rapid diagnostic tests for malaria, tuberculosis, and HIV across rural healthcare networks, with ASHA workers deploying PoC solutions in underserved regions. This decentralization generates multiple value-creation opportunities for the PoC Platform & Technology Market: reduced patient wait times (from weeks in centralized labs to minutes at point of care), lower healthcare system costs through prevention and early intervention, and dramatically improved accessibility in regions with limited laboratory infrastructure.

Chronic Disease Prevalence and Continuous Monitoring Demand

The epidemiological shift toward chronic, non-communicable diseases is creating sustained demand for PoC diagnostic platforms capable of enabling early detection, continuous monitoring, and timely therapeutic intervention. Diabetes exemplifies this trend: affecting 537 million individuals globally as of 2024, with projections of 783 million by 2045, the disease demands frequent glucose monitoring functionality ideally suited to PoC testing infrastructure. The glucose monitoring segment currently represents the second-largest application category in the PoC Platform & Technology Market and is expanding faster than infectious disease testing, driven by the adoption of continuous glucose monitoring (CGM) systems integrated with digital connectivity and cloud platforms. Cardiovascular diseases, oncology biomarkers, and metabolic disorder diagnostics collectively represent high-volume, recurring testing scenarios. These chronic disease management patterns contrast sharply with infectious disease testing, which are episodic events.

The structural difference chronic disease monitoring requiring ongoing engagement versus infectious disease requiring point-in-time diagnosis creates a more stable, predictable revenue foundation for PoC Platform & Technology Market participants. Healthcare systems increasingly recognize that decentralized, frequent monitoring via PoC devices reduces hospitalization rates and improves clinical outcomes, justifying capital investment in distributed testing infrastructure. The integration of PoC results with electronic health records (EHRs) through cloud-based data management systems further strengthens the value proposition, enabling clinicians to access real-time patient data and make informed decisions across geographically dispersed patient populations.

Market Restraining Factors

Intensified Regulatory Scrutiny and Quality Compliance Costs

The regulatory landscape for point-of-care testing is becoming increasingly rigorous, creating barriers to entry for new technologies. In the United States, the CLIA regulatory updates effective January 2025 have tightened accuracy standards for analytes like HbA1c, enforcing stricter proficiency testing requirements (+/- 6% thresholds).

The European Union's transition to the In Vitro Diagnostic Regulation (IVDR) has increased the clinical evidence data required for certification, leading to extended approval timelines and supply chain disruptions for legacy devices. These heightened compliance costs can deter smaller innovators and slow the commercialization of novel biomarker platforms.

Key Market Opportunities

Emerging Market Penetration and Rural Healthcare Infrastructure Development

Emerging markets, particularly in Asia-Pacific and sub-Saharan Africa, present substantial market expansion opportunities for the PoC Platform & Technology Market through a convergence of favorable macroeconomic trends, government health initiatives, and technology adoption patterns.

The Asia-Pacific diagnostic testing market is projected to grow at significant rate in 2033, significantly exceeding North America and Europe growth rates. China's government has established systematic programs to incorporate lateral flow assays into large-scale community screening initiatives managed by the Chinese CDC, with local manufacturers such as Wondfo and Innovita scaling production to meet both domestic and export demand. India's rural healthcare infrastructure expansion, accelerated through government-backed programs like the National Health Mission, is creating deployment pathways for PoC devices in primary health centers, with approximately 150 million units of glucose testing devices projected for the Indian market by 2029, representing massive addressable volume. Digital health integration in these emerging markets is proceeding at accelerated pace compared with developed economies, with Q2 2025 APAC digital health funding reaching US$1.2 billion across 102 deals (4% year-over-year growth despite 11% global decline), demonstrating investor confidence in the region's diagnostic innovation trajectory.

Investment capital increasingly targets diagnostic innovation in emerging markets, with leading investors recognizing the alignment between technological leapfrogging adoption of advanced PoC technologies without transitional infrastructure investment and unmet healthcare needs. Japan and South Korea are pioneering AI-integrated PoC innovations and robotic diagnostic systems, while India and Indonesia are witnessing surge in demand across healthcare sectors, creating demonstration effects that influence global adoption curves.

Government commitment to "Make in India" policies and comparable programs across Southeast Asia are establishing local manufacturing ecosystems for PoC devices, reducing supply chain dependency on developed markets and improving product affordability through localized production economics. These emerging market opportunities offer the PoC Platform & Technology Market access to billions of currently underserved patients while establishing long-term market presence before competitors establish entrenched positions.

Molecular PoC Platform Expansion and Syndromic Testing Integration

Molecular point-of-care platforms represent the fastest-growing segment within the PoC Platform & Technology Market, driven by technological advances enabling rapid sample-to-answer analysis with sensitivity and specificity approaching laboratory-standard molecular diagnostics. The point-of-care molecular diagnostics market is, reflecting compound annual growth rates substantially exceeding lateral flow assay segment expansion. Syndromic testing simultaneous detection of multiple pathogens from a single patient sample within a single assay is expanding the clinical utility of molecular PoC platforms beyond single-target diagnostics, enabling empiric antimicrobial treatment decisions informed by multiplex pathogen detection rather than broad-spectrum empiricism.

bioMérieux's BIOFIRE SPOTFIRE system exemplifies this trend, delivering automated syndromicresults within timeframes aligned with typical patient visits, receiving FDA clearance and CLIA waiver in 2024, and enables up to four modules of multiplexed testing. The integration of AI into molecular PoC platforms accelerates result interpretation, algorithmic signal deconvolution for multiplex data, on-board quality control automation, and real-time workflow optimization, positioning molecular platforms as early adopters of AI integration compared with immunoassay and biosensor modalities.

Clinical advantages of molecular PoC expansion include improved diagnostic accuracy for respiratory infections (influenza, RSV, COVID-19), reduced unnecessary antibiotic prescribing through targeted pathogen identification, and faster patient disposition decisions in emergency departments. The PoC Platform & Technology Market benefits from this molecular expansion through expanded addressable patient populations, underpenetrated molecular testing in primary care relative to hospital settings, and higher per-test revenue economics compared with immunoassay testing.

Category-wise Analysis

Platform Type Insights

Lateral flow assay platforms maintain market leadership as the dominant technology within the PoC Platform & Technology Market, commanding 35.0% market share in 2026, driven by their simplicity of operation, low manufacturing cost, minimal equipment requirements, and established regulatory pathways. LFA technology, foundational to rapid diagnostic testing for pregnancy, infectious diseases (COVID-19, influenza, malaria), and cardiac markers, has achieved global manufacturing capacity through thousands of diagnostic companies and contract manufacturers.

Technological advancement within the LFA segment is progressively enhancing diagnostic sophistication, with multiplex detection assays enabling simultaneous detection of multiple biomarkers within a single test, addressing a historical LFA limitation of single-analyte detection. Companies such as QuidelOrtho and Abingdon Health are advancing beyond traditional single-analyte strips to enable simultaneous biomarker detection with sub-nanogram sensitivity, reflecting market maturity toward integrated diagnostic systems capable of replacing or augmenting laboratory-based assays in decentralized settings. Strategic mergers and acquisitions continue to reshape the LFA competitive landscape, with large diagnostics companies acquiring specialized innovators to integrate niche technologies into existing portfolios.

Molecular PoC platforms represent the fastest-expanding technology segment within the PoC Platform & Technology Market, driven by technological breakthroughs enabling nucleic acid amplification (PCR-based testing) and detection at point-of-care settings previously accessible only through centralized laboratory infrastructure.

End Use Industry Insights

Infectious disease testing commands the largest share of the PoC Platform & Technology Market, accounting for 38.0% market share in 2026, reflecting both historical prevalence (established PoC testing infrastructure for malaria, tuberculosis, and HIV in endemic regions) and pandemic-accelerated demand (COVID-19 expanded PoC testing capacity globally and normalized rapid point-of-care diagnostics in healthcare systems).

The COVID-19 pandemic created structural changes in healthcare system diagnostics capabilities: centralized laboratories rapidly decentralized testing to emergency departments, urgent care clinics, and retail pharmacies; point-of-care test volume increased 55% year-over-year during pandemic peaks; and healthcare systems invested in permanent PoC infrastructure expecting future infectious disease surges. This pandemic-driven infrastructure investment persists as baseline capacity, supporting sustained growth in infectious disease PoC testing post-pandemic, as respiratory viruses (influenza, RSV) and gastrointestinal pathogens (norovirus, rotavirus) require seasonal rapid diagnostic confirmation.

Glucose and chronic disease monitoring applications represent the fastest-growing segment within the PoC Platform & Technology Market, driven by the rising prevalence of diabetes, cardiovascular disease, and metabolic disorders that require frequent monitoring and timely therapeutic adjustments.

Regional Insights and Trends

North America Market Trend

North America commands 38% of the global PoC Platform & Technology Market share, reflecting advanced healthcare infrastructure, high per capita healthcare spending, established reimbursement mechanisms, and concentrated presence of leading diagnostics manufacturers and innovation hubs. The United States dominates North American diagnostics, with the broader clinical diagnostics market.

The region's leadership sustained by multiple structural factors: robust healthcare infrastructure with widespread hospital and clinic networks supporting PoC adoption, advanced reimbursement systems with established coverage for PoC tests across multiple clinical applications, and substantial R&D investment from both public sources (NIH funding) and private sector diagnostics companies.

Regulatory environments in North America have historically supported PoC innovation through FDA's established approval pathways for in vitro diagnostics and point-of-care tests. The recent FDA regulatory evolution initial LDT oversight rule, subsequent rescission (September 2025), and reversion to enforcement discretion creates ongoing regulatory uncertainty impacting longer-term investment planning. Healthcare institutions across North America have established PoC testing infrastructure driven by pandemic-accelerated adoption during COVID-19 testing in emergency departments, urgent care clinics, and retail pharmacies and sustained by recognition of operational benefits.

East Asia Market Trend

East Asia represents the fastest-growing region within the PoC Platform & Technology Market, commanding 26% of global market share in 2026 and expanding more rapidly than North America and Europe.

China has emerged as a dominant force in the regional PoC Platform & Technology Market, The Chinese CDC has systematically adopted lateral flow assays in large-scale community screening programs for infectious diseases (hepatitis, HIV, tuberculosis), creating procurement scale that incentivizes local manufacturing expansion. Wondfo and Innovita, Chinese PoC device manufacturers, are progressively scaling production to serve both domestic demand and export markets across Southeast Asia and South Asia.

Japan presents a distinct growth trajectory within East Asia, characterized by advanced healthcare infrastructure, an aging population, and innovation in AI-integrated and connected PoC systems. Japan's healthcare system extensively utilizes point-of-care testing in outpatient settings, with well-established reimbursement mechanisms that support the adoption of PoC diagnostics. The country is pioneering innovations in portable ultrasound systems with AI image analysis assistance, wearable cardiac monitors with AI arrhythmia detection, and smartphone-enabled diagnostic readers—technologies establishing benchmark standards that progressively diffuse globally.

South Korea similarly demonstrates advanced PoC technology adoption, with strong focus on AI integration, robotics, and connected diagnostic systems. APAC digital health funding reached US$1.2 billion in Q2 2025, with AI-powered diagnostics ventures capturing 63% of capital allocation, indicating investor prioritization of the region's innovation trajectory.

Europe Market Trend

Europe commands 24% of the global PoC Platform & Technology Market share, reflecting mature healthcare infrastructure, stringent regulatory standards, and innovation in integrated diagnostic networks.

Germany, France, and the United Kingdom represent the largest European PoC diagnostics markets, with Germany's significant presence in diagnostics manufacturing and precision medicine innovation driving regional leadership.

Regulatory environments in Europe are characterized by stringent standards through the In Vitro Diagnostic Regulation (IVDR), which mandates comprehensive clinical evidence, post-market surveillance, and quality management systems for all IVD devices, including PoC platforms. The IVDR implementation established CE marking requirements and imposed more rigorous clinical-evidence standards than previous IVD Directive frameworks, thereby extending time-to-market for novel PoC innovations and increasing development costs.

Europe's healthcare systems emphasize preventive medicine, early disease detection, and cost-effectiveness, supporting PoC testing adoption where clinical evidence demonstrates diagnostic accuracy and health economic benefit. Private diagnostics companies and hospital networks across Europe have invested substantially in PoC infrastructure, particularly following pandemic-accelerated adoption of rapid COVID-19 testing.

Competitive Landscape

The Global PoC Platform & Technology market is largely consolidated, dominated by key players such as Abbott Laboratories, Roche, Co-Diagnostics, Vital Biosciences, and LumiraDx. These companies lead through continuous innovation in molecular, immunoassay, and clinical chemistry platforms and strategic partnerships that expand their reach in hospitals, primary care centers, and decentralized healthcare settings. High regulatory requirements, complex technology development, and clinical validation create significant entry barriers, limiting smaller competitors.

Market growth is driven by mergers, acquisitions, and product launches, as well as the adoption of AI, microfluidics, and robotics to enhance diagnostic speed and accuracy. Abbott and Roche lead in molecular and multi-assay PoC technologies, while Vital Biosciences and Co-Diagnostics focus on decentralized and rapid testing solutions. The market is expected to grow steadily, fueled by rising demand for accessible, rapid diagnostics and the expansion of healthcare infrastructure globally.

Key Industry Developments

- July 29, 2024, Roche completed the acquisition of LumiraDx’s multi-assay point-of-care platform, which consolidates immunoassay and clinical chemistry tests on a single instrument with potential molecular testing expansion. This strengthens Roche’s PoC portfolio and advances decentralized diagnostics in primary care and resource-limited settings globally.

- July 25, 2023, Vital Biosciences introduced the VitalOne point-of-care lab testing platform, capable of delivering over 50 lab-grade test results within 20 minutes at primary care sites. Integrating microfluidics, robotics, and computer vision, this platform exemplifies a disruptive PoC technology aimed at decentralizing diagnostics and improving patient access to care.

Companies Covered in PoC Platform & Technology Market

- Abbott Laboratories

- Becton, Dickinson and Company

- bioMérieux

- Chembio Diagnostics

- Cue Health

- Danaher Corporation (Cepheid)

- F. Hoffmann-La Roche Ltd

- HemoCue

- iHealth Labs

- Illumina (Verifi)

- LumiraDx

- Mesa Biotech

- Nova Biomedical

- QIAGEN

- QuidelOrtho

- Scanwell Health

- Siemens Healthineers

- Thermo Fisher Scientific

- Trinity Biotech

- Werfen

Frequently Asked Questions

The global PoC Platform & Technology Market is projected to be valued at US$ 41.4 Bn in 2026.

The Lateral Flow Assay (LFA) Platforms Segment is expected to account for approximately 40% of the global PoC Platform & Technology Market by Platform Type in 2026.

The market is expected to witness a CAGR of 10.5% from 2026 to 2033.

The PoC Platform & Technology Market growth is driven by healthcare system decentralization, expanding access to diagnostics in primary care and home settings, and rising demand for continuous monitoring of chronic diseases such as diabetes, cardiovascular disorders, and metabolic conditions.

Key market opportunities in the PoC Platform & Technology Market include emerging market penetration and rural healthcare infrastructure expansion in Asia-Pacific and sub-Saharan Africa, alongside rapid growth of molecular PoC platforms and syndromic testing integration enhanced by AI and multiplex capabilities.